26 Stocks to Watch in 2026: Part 1

2026 is just around the corner.

Investment banks, analysts, and investment managers are making their predictions for where the S&P 500 will end 2026.

I’m not here to make a prediction - I know that I don’t know.

Here’s what I do know - buying great businesses is the way to build long-term wealth.

You know that we look for businesses that generate healthy, consistent cash flow and, most importantly, believe in paying the owners.

We want companies that distribute a share of their profits back to us in the form of dividends.

Let’s dive in!

26 Ideas, Two Saturdays

Because 26 companies is a lot to digest at once, I’ve decided to split this list into a two-part series:

Part 1 (Today): The first 13 stocks that have landed on my radar.

Part 2 (Next Saturday): The remaining 13 companies to round out the list.

To be clear, I haven’t completed a deep dive into most of these companies just yet.

These are companies that have piqued my interest, and ones I’ll be watching closely as we move into 2026.

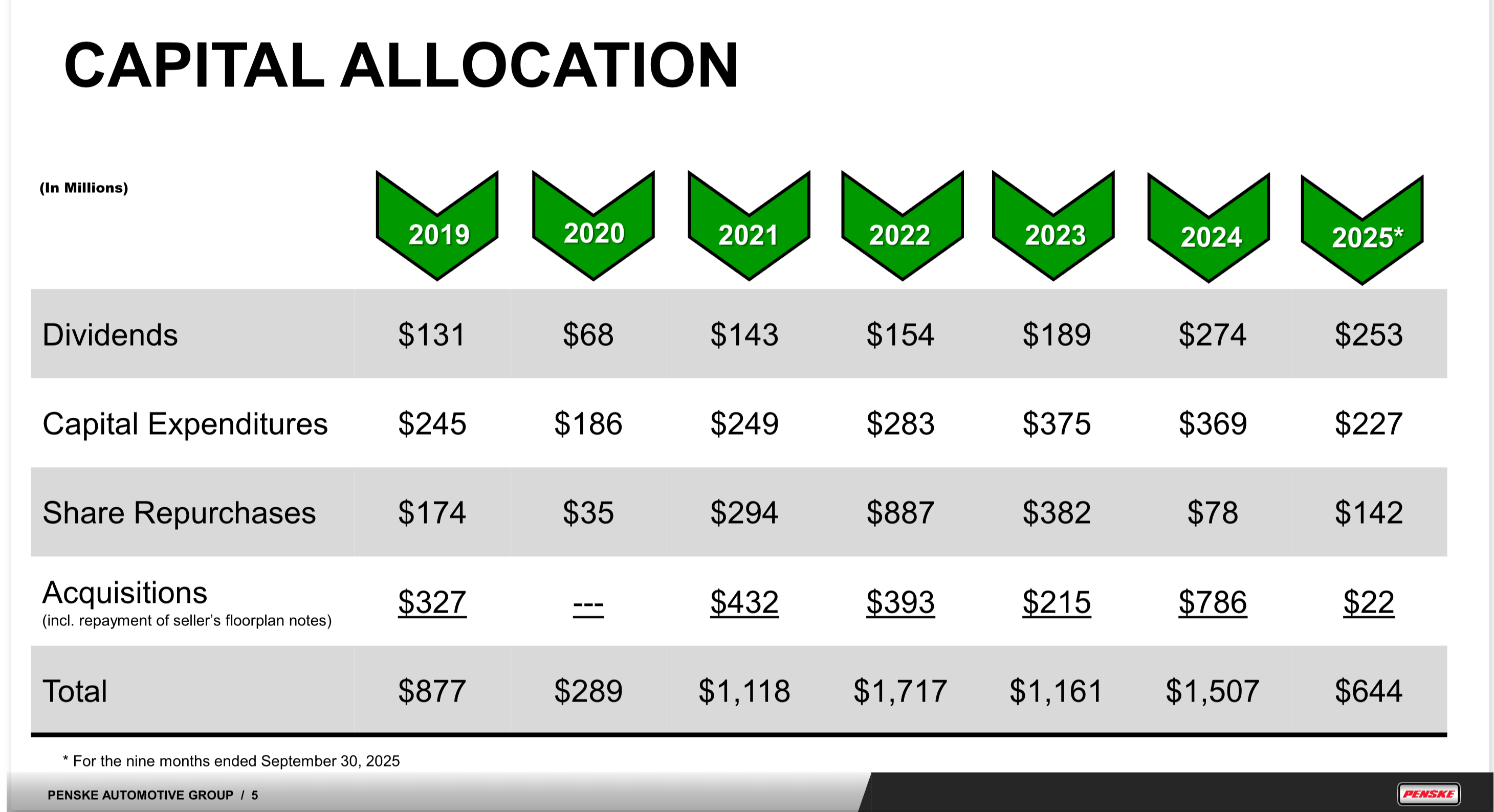

26. Penske Automotive Group ($PAG)

Company Profile

Penske is one of the world’s largest automotive retailers and a leading international transportation services company. They operate hundreds of retail dealerships across the US and UK, alongside a significant commercial truck segment and a large stake in Penske Transportation Solutions.

Why It’s Interesting

Local Monopolies: Dealerships benefit from state laws that limit competition, creating a protected local moat.

The Service Department: While car sales can be cyclical, the service and parts departments provide high-margin, recurring revenue.

Rising Complexity: As vehicles become more complex, owners are less likely to DIY, driving more business back to specialized dealer service centers.

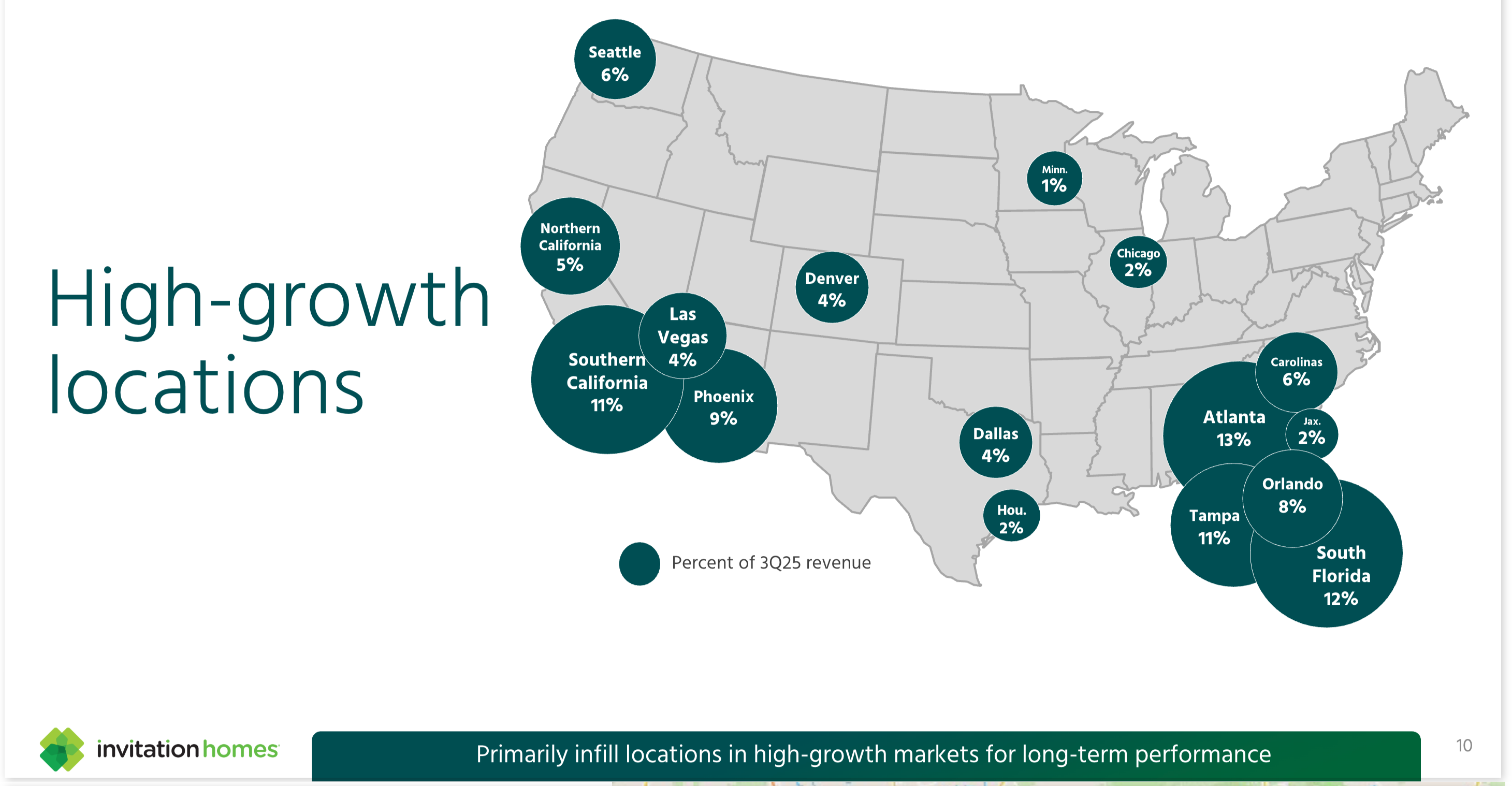

25. Invitation Homes ($INVH)

Company Profile

Invitation Homes is the premier single-family home leasing company in the United States. They own and manage a massive portfolio of high-quality homes in areas with strong job growth and great schools.

Why It’s Interesting

The Rent vs. Buy Gap: With US home prices and mortgage rates high, renting a single-family home has become a more affordable and flexible alternative in many places.

Economies of scale: Invitation’s size means lower cost for maintenance and management, that a “mom-and-pop” landlord simply cannot match.

Valuation: Despite strong occupancy rates near 97%, the stock is offering a higher dividend yield than the historical average.

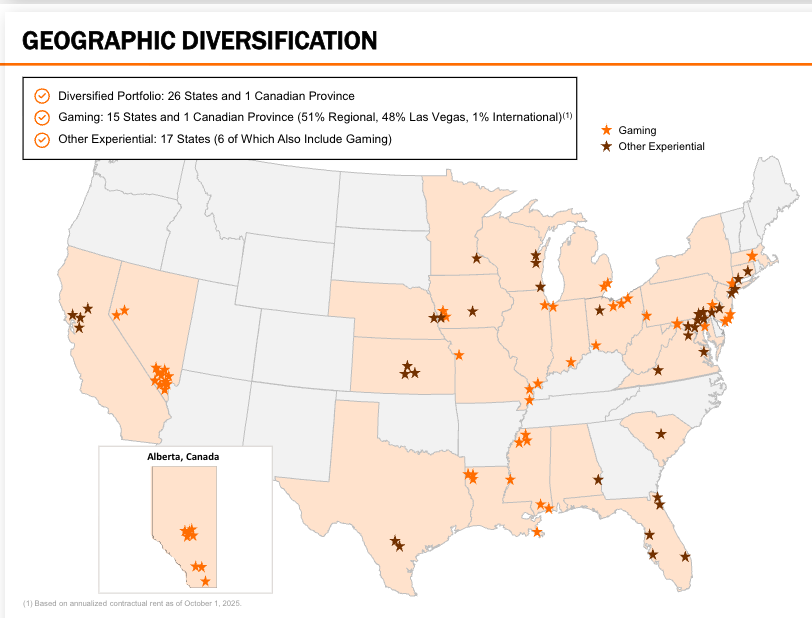

24. VICI Properties ($VICI)

Company Profile

VICI is a real estate investment trust (REIT) that owns one of the largest portfolios of market-leading gaming, hospitality, and entertainment destinations, including the iconic Caesars Palace.

Why It’s Interesting

Triple-Net Leases: VICI uses triple-net leases, meaning the tenant pays for taxes, insurance, and maintenance. Their tenants paid 100% of their rent throughout the COVID-19 lockdowns.

Critical Real Estate: You can’t move a casino. The deep integration of these properties into the tenant’s business makes VICI’s cash flow incredibly durable.

High Yield: VICI is getting close to a 6% yield, and it should be able to keep raising the dividend - their leases often have annual rent escalators tied to inflation.

23. Darden Restaurants ($DRI)

Company Profile

Darden is the owner of some of the most recognizable names in casual dining, including Olive Garden, LongHorn Steakhouse, and the recently acquired Ruth’s Chris Steak House.

Why It’s Interesting

Market Share: While many smaller restaurant chains are struggling with rising costs, Darden’s scale allows them to negotiate better prices on everything from shrimp to steak.

Operational Excellence: Management has a “brilliant with the basics” philosophy that has led to consistent same-restaurant sales growth.

Brand Power: Flagship brands like Olive Garden have massive customer loyalty and a value proposition that’s continuing to do well, even in a tighter economy.

22. Mondelēz International ($MDLZ)

Company Profile

Mondelēz is a global snacking giant with a portfolio that includes brands like Oreo, Cadbury, and Milka. They operate in over 150 countries, focusing heavily on biscuits and chocolate.

Why It’s Interesting

Local First Strategy: Unlike other conglomerates that centralize everything, Mondelēz allows local managers to tailor products and marketing to specific regional tastes.

Snack-Sized Moat: People don’t stop buying Oreos during a recession. The low price point and high brand loyalty make their revenue streams relatively stable.

Emerging Market Tailwinds: They have a massive footprint in developing markets where rising middle-class incomes are driving increased snack consumption.

21. H&R Block ($HRB)

Company Profile

H&R Block provides tax preparation services through a vast network of physical offices and digital software. They also offer financial products like the Spruce mobile banking app.

Why It’s Interesting

Tax Complexity: As tax codes become more complex with new deductions and credits, the need for H&R Block’s expert assisted services keeps growing.

Buybacks: Management is aggressive with capital allocation; they have bought back nearly 47% of shares outstanding since 2016.

SaaS Revenue: Their acquisition of Wave (small business accounting) provides a high-growth SaaS revenue stream to complement the seasonal tax business.

20. Mullen Group ($MTL)

Company Profile

Mullen Group is one of Canada’s largest logistics and trucking providers. They provide a wide range of services, including “less-than-truckload,” specialized hauling, and oilfield services.

Why It’s Interesting

Dividend Yield: Mullen is offering a 5% yield that’s well-covered by steady cash flow.

Capital Allocation: Management is known for being patient, only making acquisitions when valuations are attractive and the balance sheet is pristine.

Essential Service: No matter the economic climate, food, medicine, and industrial supplies still need to be moved.

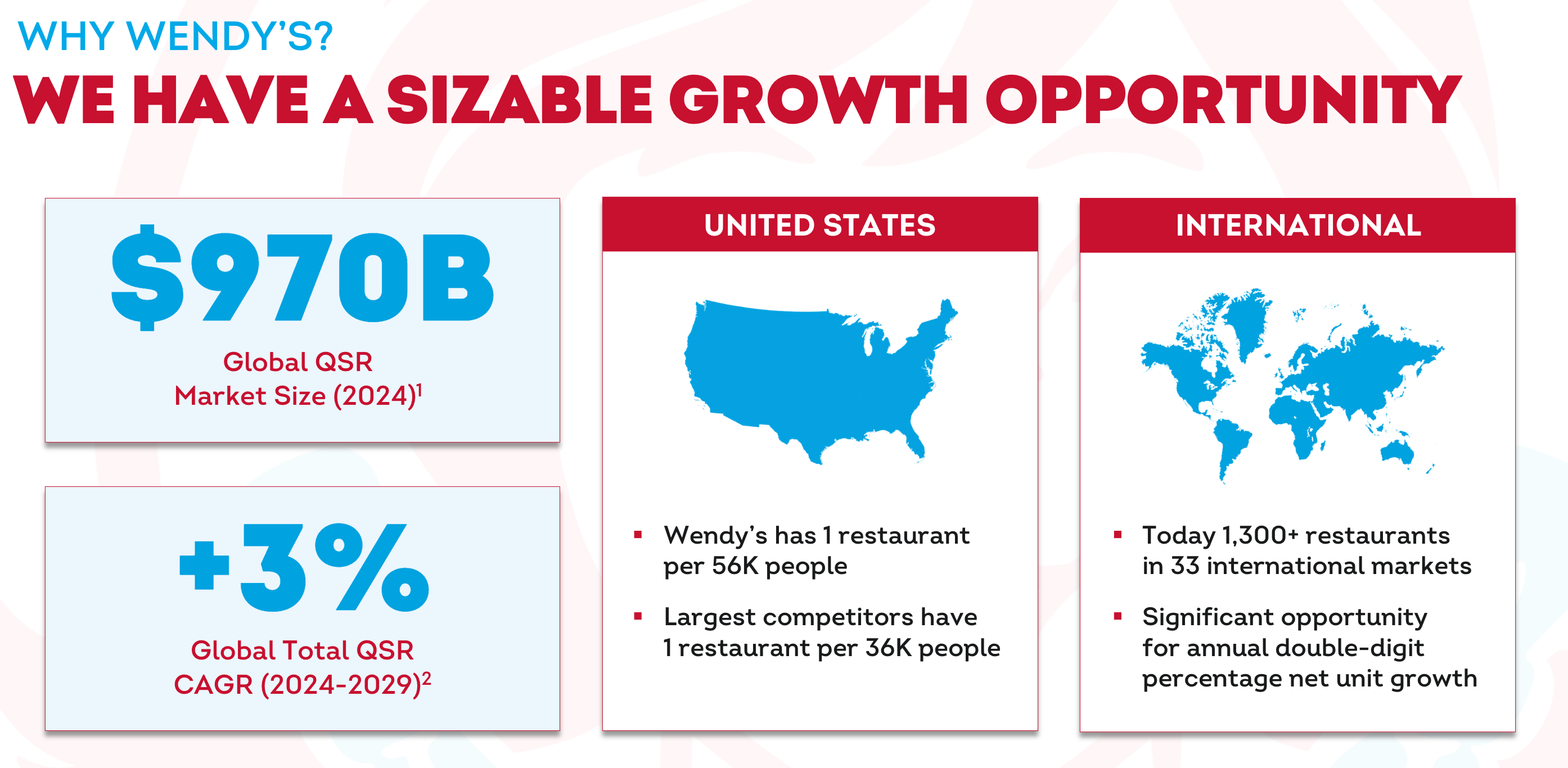

19. Wendy’s ($WEN)

Company Profile

Wendy’s is the world’s third-largest quick-service hamburger company. The vast majority of its thousands of locations are operated by franchisees, creating a high-margin royalty model.

Why It’s Interesting

International Growth: While domestic growth is steady, Wendy’s is seeing significant international expansion, which provides a long-term runway for earnings.

Shareholder Yield: Between a high dividend yield and consistent buybacks, the company is focused on returning cash to owners.

Technology: Their heavy investment in mobile ordering and loyalty programs is increasing how often customers buy, and average ticket sizes.

18. Argan SA ($ARG.PA)

Company Profile

Argan is a French real estate company specializing in the development and leasing of premium logistics warehouses (the backbone of e-commerce).

Why It’s Interesting

European E-commerce Play: As online shopping continues to grow in Europe, the demand for high-spec, modern warehouses will grow along with it.

Yield & Safety: Argan currently has a very attractive yield with a conservative payout ratio.

Inflation Protected: Most of their leases include indexation clauses, meaning rents rise automatically with inflation.

17. Unite Group PLC ($UTG)

Company Profile

Unite Group is the UK’s largest owner, manager, and developer of purpose-built student accommodation. They partner with top-tier universities to provide housing for over 70,000 students.

Why It’s Interesting

Supply-Demand Gap: There is a chronic shortage of high-quality student housing in the UK, leading to high occupancy rates and reliable rent growth.

Recession Resistant: Higher education enrollment tends to stay steady or even increase during economic downturns as people head back to school to retrain.

Institutional Quality: Unite Group has a solid balance sheet and a dominant brand in the student housing sector.

16. Sonoco Products ($SON)

Company Profile

Sonoco is a global provider of consumer, industrial, and healthcare packaging. They have recently pivoted aggressively toward metal packaging through major acquisitions.

Why It’s Interesting

Metal Packaging: The acquisitions of Ball Metalpack and Eviosys have turned Sonoco into a global leader in metal food cans - a highly stable, competitively advantaged industry.

Inflation Protection: Most of their sales are under long-term contracts with price escalators, allowing them to pass on rising raw material costs to customers.

Decades of Dividends: Sonoco has been paying dividends continuously for almost 100 years, showing a deep commitment to its owners.

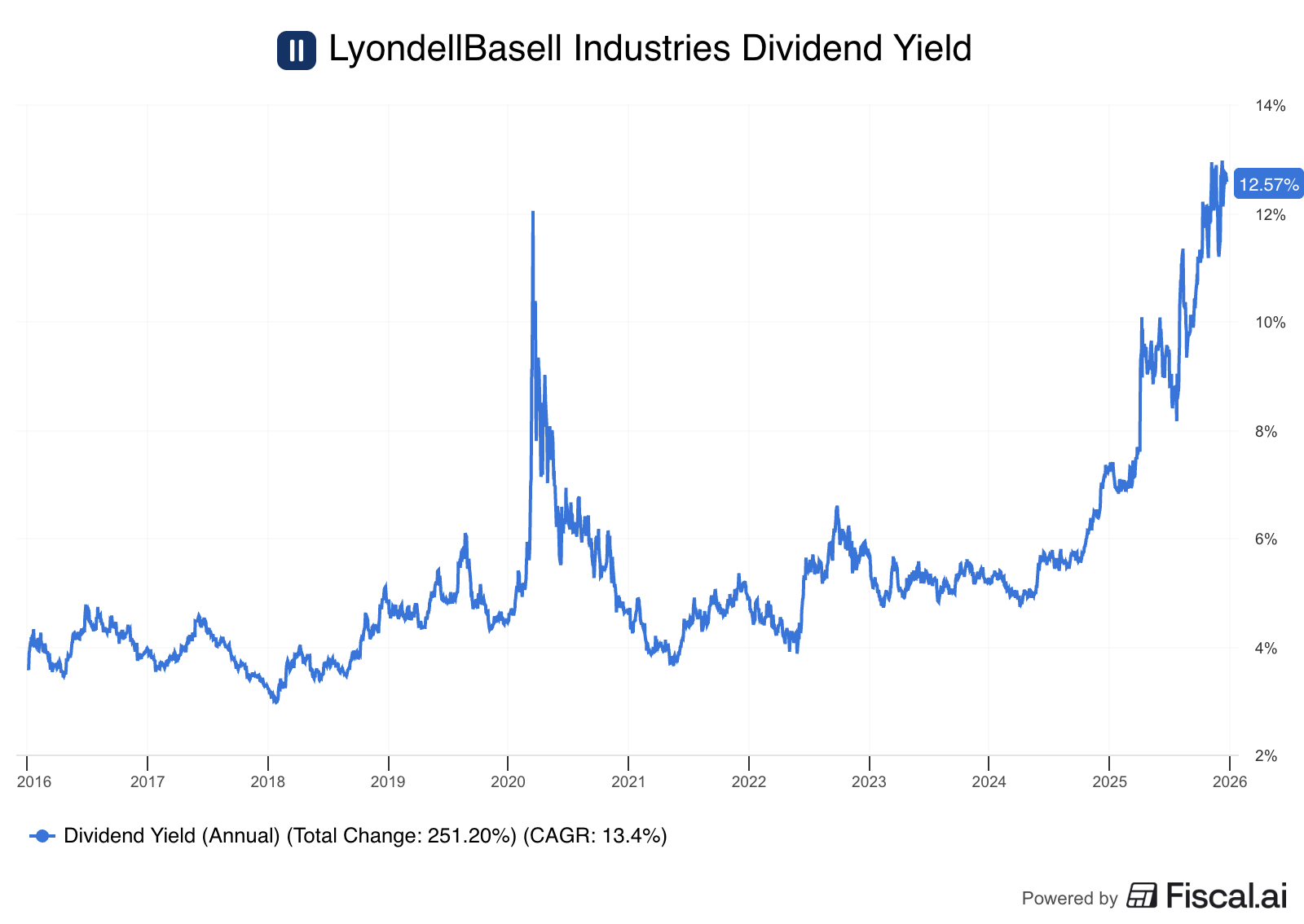

15. LyondellBasell ($LYB)

Company Profile

LyondellBasell is one of the world’s largest plastics, chemicals, and refining companies. They are a global leader in the production of polypropylene and polyethylene.

Why It’s Interesting

Cost Advantage: Because they operate heavily in the US, they have access to low-cost natural gas (feedstock), giving them a massive cost advantage over European and Asian competitors.

Deep Value: The stock has recently traded at some of its lowest valuations in years, paired with a dividend yield that is near historical highs.

Cash Improvement Plan: Management is currently executing a plan to unlock over $1 billion in incremental cash flow by the end of 2026.

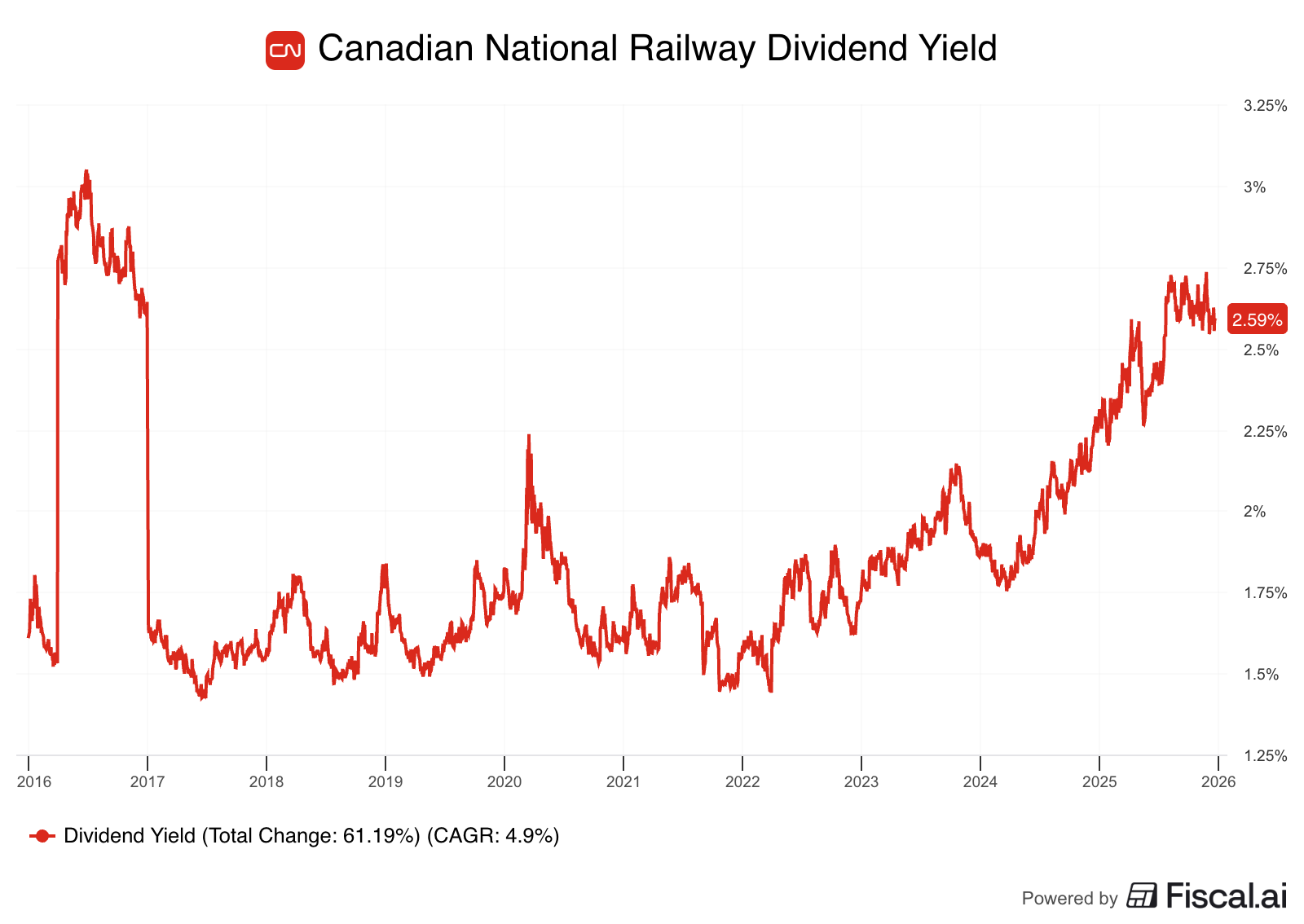

14. Canadian National Railway ($CNI)

Company Profile

CN Rail operates the only railroad in North America that connects the Atlantic, Pacific, and Gulf coasts.

Why It’s Interesting

The Ultimate Moat: You cannot build a new railroad. CN operates a toll booth on the North American economy with minimal competition for long-haul freight.

Valuation: After a period of higher valuation, the stock has become more attractive relative to its peers and its own historical averages.

Efficiency: CN is consistently one of the most efficient railroads in the world, generating massive free cash flow that supports a growing dividend.

Wrapping Up Part One

The thirteen companies we’ve covered today - from the localized monopolies of Penske Automotive to the transcontinental toll booth of Canadian National Railway are all essential pieces of the economic puzzle.

Whether it’s the logistics backbone provided by Mullen Group or the resilient cash Unite Group, VICI Properties, or Argan SA, these aren’t just tickers on a screen.

These businesses provide real-world value, generate healthy cash flow, and prioritize returning capital to us, the shareholders.

As I mentioned at the start, these are some of the names that have earned a spot on my watchlist for 2026.

Coming Next Saturday: The Top 13

We’ve checked off the first half of the list, but we’re just getting started!

In Part Two, I’ll be diving into the final 13 stocks, companies I believe represent some of the highest-quality business models on the planet.

Next week, we’ll look at:

A company that collects a tax on the entire passive investing revolution.

A Duopoly that has dominated the retail landscape for decades.

A Software Giant that is aggressively cannibalizing its own shares.

The Amazon of Industry that keeps the world’s factories running.

Keep an eye on your inbox next Saturday morning for the conclusion of this series.

One Dividend At A Time,

-TJ

P.S…

We will have a limited number of discounted memberships that will reopen later in 2026.

If you want your name on the list, so you get notified before anyone else,

you can do that here:

You’ll also get a copy of my 10 favorite cannibal stocks when you do.

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data