A historic transition at Berkshire

The 2026 Berkshire AGM marked a historic transition.

This is the second year in a row that I’ve gone to Omaha.

It was interesting seeing Greg Abel take the lead for the first time.

The emphasis remained firmly on value investing and operational excellence.

And I wasn’t surprised that he did not introduce a dividend, as some speculated.

The thing is, Berkshire has maintained a No Dividends policy since 1967.

The company believes it can create more than $1 of market value for every $1 retained and reinvested.

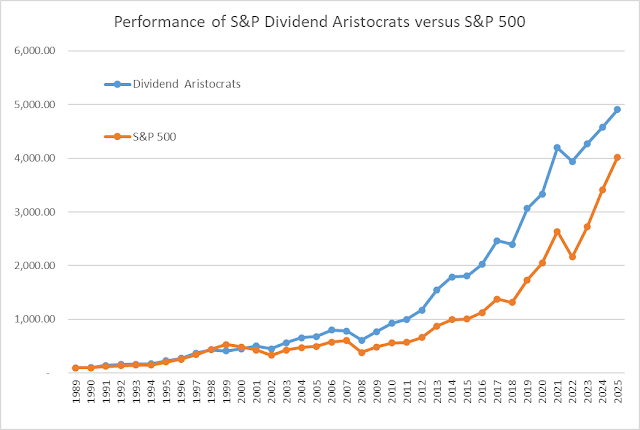

This strategy has consistently outperformed dividend payouts for Berkshire shareholders.

What makes it interesting is that BRK’s portfolio contains many dividend-paying stocks.

Coca-Cola alone pays around $816 million in yearly dividends to Berkshire.

That’s in addition to billions in yearly payouts from its portfolio companies.

Now, that cash doesn’t flow directly to investors.

But there’s another side to this story.

One ETF makes it possible to earn a yield from Berkshire’s holdings.

The VistaShares Target 15 Berkshire Select Income ETF launched in May 2025.

Quite a mouthful. But the pitch is straightforward:

The ETF provides exposure to Berkshire’s top holdings while using options to generate income.

The ETF targets a 15% annual yield, paid monthly at roughly 1.25%.

This may sound attractive.

But as an investor, there are a few things you should keep in mind.

First, the ETF charges a 0.95% annual fee.

So you pay $95 for every $10,000 you invest.

That’s high for most investors.

Second, a large portion of the fund’s payouts may come from “return of capital.”

Why should you care about this?

Here’s what it means.

Part of the money paid out is simply you getting some of your capital back.

Over time, this can reduce the fund’s net asset value (NAV).

If the market crashes, a lower NAV makes recovery very difficult.

Third, the 15% yield target is very ambitious.

Maintaining a payout that high over long periods could be difficult.

The fund may have to rely heavily on return of capital or aggressive options strategies.

This increases the risk of value erosion for investors.

So, overall, it is a tempting proposition.

But very few investors can live with those tradeoffs.

This brings us to a very important question:

How do you generate a high-yield income with less risk

Here’s a suggestion.

Focus on Dividend Growth companies.

These are sound companies that consistently raise their dividends.

As an investor, you may like them because they have certain characteristics.

Strong balance sheets, low debt levels and high cash reserves.

This signals financial health, ensuring they can weather economic challenges.

Sustainable payout ratios:

This indicates they don’t overextend themselves, leaving room for future growth.

Most Dividend-Growers are in sectors that do well even during economic downturns.

A few examples are consumer staples, utilities, healthcare, energy, and industrials.

In other words… What happens when you invest in the right dividend growers?

You have a rising, reliable cash flow that stands the test of time.

If you’re seeking a hedge against inflation, dividend growers also offer a benefit.

As prices rise, so do your dividends.

This ensures your purchasing power remains intact.

What’s more?

Historically, companies that consistently raise their dividends outperform the market.

That’s because they combine regular income with the potential for capital appreciation.

On top of that, you can enjoy the full power of compounding with dividend growth companies.

How?

Warren Buffett is the perfect example.

He reinvests his earnings to boost annual returns over time.

You can apply this principle too when you invest in Dividend-Growers.

As these companies consistently increase their dividend payouts…

Reinvesting your dividends accelerates wealth accumulation faster.

As an example, consider our next buy in Compounding Dividends.

This company uses its cash flow to aggressively buy back shares.

It has retired over 52% of its shares since 2020.

As an investor, here’s what this means for you.

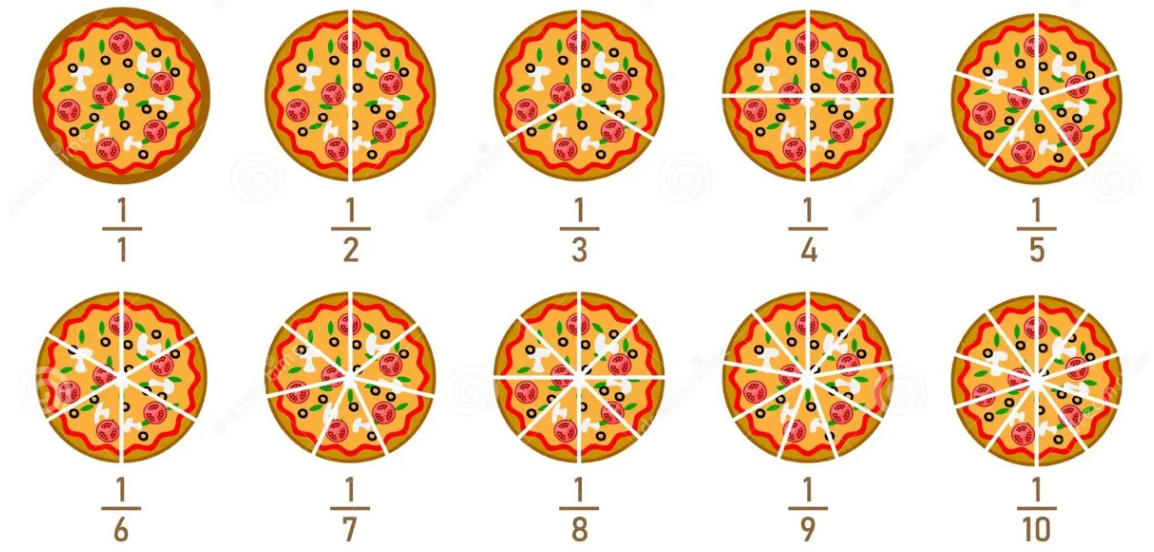

When a company eats itself by retiring shares…

Your percentage ownership of the business grows automatically.

Your Dividends Per Share (DPS) also increases.

Just like a pizza, the fewer slices you cut the business into, the bigger each slice is.

Companies that operate like this are wonderful Dividend-Growers.

They may not appeal to some investors.

But the payout can be great if you stay the course.

Our Recent Buy

That’s why we’re excited about our recent Buy in Compounding Dividends.

It’s a market leader, with more than 60% market share.

It pays a 2%+ dividend, but the Payout Ratio is below 15%.

It uses the rest of its cash to buy back shares at low valuations.

And when you combine market dominance with aggressive share buybacks?

You get a powerful compounding machine you can rely on for many years.

Just think about NVR:

NVR is a homebuilder in the United States.

Between 1993 and 2024, NVR bought back more than 80% of its shares.

Shares outstanding 1993: 17.9 million

Shares outstanding 2024: 3.1 million

82.7% of shares bought back

Zero dividends, no stock splits

The result?

The stock price went from $5.50 to over $9,000.

That is a 1,600-bagger - the kind of wealth creation that changes lives.

But it gets better.

The company is trading at a discount while management keeps buying back shares.

So if you invest today, you’ll be buying a compounding machine at a bargain.

Want the full story on this company?

Give Compounding Dividends a try today.

As a partner, you’ll get the investment case for the 18 Dividend Stocks we own.

That includes the one I just told you about.

But that’s not all.

In addition to Portfolio access, you’ll also get:

📚 Full access to our library of articles on dividend investing.

🔎 Investment cases about new Dividend Growers on our watchlist.

💰 Access to the High Yield Portfolio

🔎 Access to our private community.

The regular subscription fee is $499 per year.

But if you act now, I’ll give you a $100 discount.

You pay only $399.

And I want to make your decision as easy as possible.

So here’s the second part of the deal.

Try Compounding Dividends for 90 days.

If you’re not happy, we’ll refund the entire cost of your subscription.

That’s how confident I am in the dividend stocks we write about.

And there’s one more part of the deal…

The Exclusive Bonuses.

You’ll get:

📘 E-book with one-pagers of all our stocks

📊 Spreadsheet with the dividend growth of the portfolio

🎥 Video course: How to find great dividend stocks

🛒 Report: 3 Dividend Stocks to Buy

⭐ Report: Pieter’s 3 Favorite Stocks

🔍 Report: How to find 100-baggers

💵 10 Dividend Stocks to Own Forever

🏗️ Masterclass: Build Your Dividend Machine

But please note:

Your discount and chance to get all of these exclusive bonuses expires at the end of this week.

So if you want big savings on your subscription, don’t delay.

Click here to start your risk-free trial of Compounding Dividends.

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data