🔥 Stock Idea: Admiral Group

Admiral Group has nearly 12 million insurance policies, and structural cost advantages.

Despite record profits, it’s got a yield over 6% because of worries about rising claims inflation and new regulatory pressures.

Is this industry leader a buy? Let’s find out!

: Company Profile, Stock Price, News, Rankings | Fortune")

Admiral Group PLC

Admiral is a leading insurance provider that uses technology to keep costs low.

It then passes those savings along to customers.

While they are famous for car insurance, they have spent the last few years branching out into home insurance, pet insurance, and personal loans.

They share a lot of the risk with other big global insurance partners through reinsurance agreements.

That allows Admiral to focus on what they do best - using data to pick the safest drivers and give them great customer service.

Company name: Admiral Group PLC

✍️ ISIN: GB00B02J6338

🔎 Ticker: $ADM

📚 Type: High yield stock

📈 Stock Price: £32.39

💵 Market cap: £9.8 billion

📊 Average daily volume: £34 million

Onepager

Don’t know Admiral Group?

Here are the basics (click on the picture to expand):

Now let’s dive into the full investment case!

1. Do I understand the business model?

Admiral makes most of their money from selling car insurance, but it’s really a data company.

They use over 120 different AI and machine learning models to pick the safest drivers, and figure out exactly how much to charge each person based on their risk of having an accident.

Unlike traditional insurers that keep all the risk on their own books, Admiral uses reinsurance.

In 2025, they used reinsurance deals to pass 78% of their UK car insurance risk to other partners.

This makes the business much safer and allows them to pay out most of their profits as dividends to shareholders.

Revenue Split

Most of the revenue (which they call turnover) comes from UK car insurance.

Here is the split for the 2025 fiscal year:

UK Insurance (Motor, Home, Pet): £5 billion (85% of turnover)

European Insurance (Italy, France, Spain): £674 million (11% of turnover)

Admiral Money (Personal Loans): £226 million (4% of turnover)

Geographic Split

The vast majority of the revenue comes from the United Kingdom.

They have a dominant position in the UK, but they are growing steadily in Europe, particularly in Italy (under the brand ConTe) and Spain.

They recently exited the US market, where they were losing money, to focus on where they are most profitable.

Who are the customers?

Admiral’s customers are individual people looking for insurance for their cars, homes, or pets.

They have 11.8 million policies active.

A growing number of these customers are multi-product, meaning they might have both their car and home insurance with Admiral.

These customers are much more likely to stay with the company for a long time.

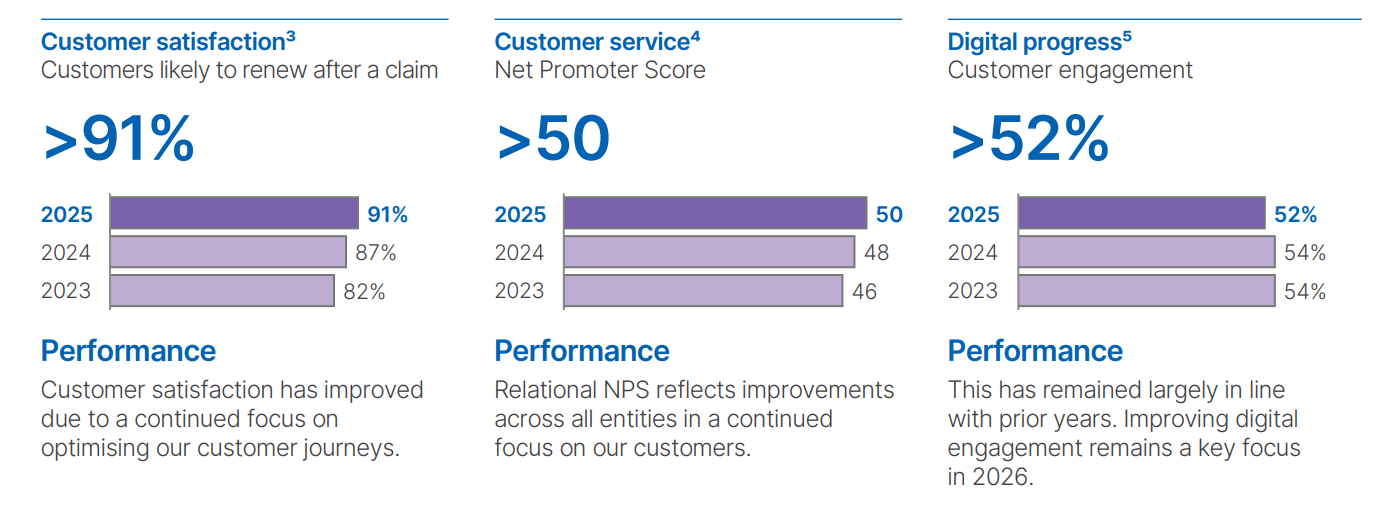

Another great thing to see?

Admiral has very high customer satisfaction scores.

What’s the moat?

Admiral’s moat comes down to low costs.

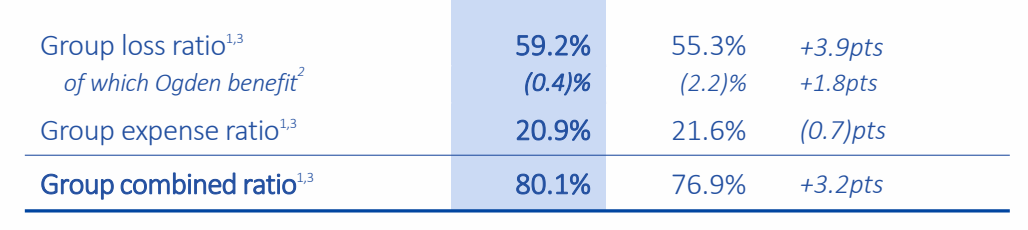

Insurance companies make money on the difference between what they collect in premiums and how much they have to pay out in claims and expenses.

The percentage of premiums spent on claims and expenses is called the Combined Ratio.

Most insurance companies spend about 95p to £1.00 on claims and expenses for every £1 they collect in premiums.

Admiral only spends about 80p.

This comes down to a few things.

First, Admiral has a structural cost advantage.

They are much leaner and more efficient than older insurance companies.

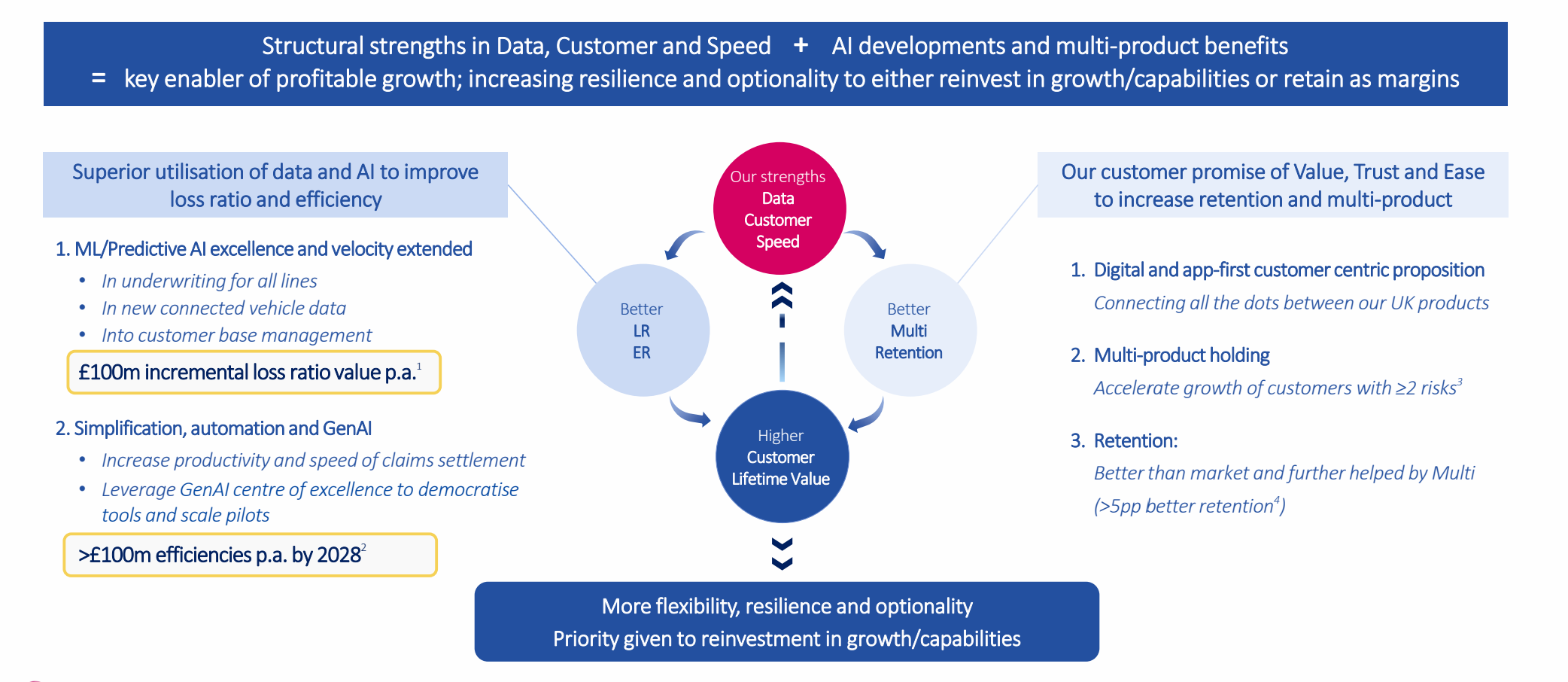

Second, Admiral has invested heavily in data and AI.

They have 20 years of proprietary data that helps them spot good drivers that other companies might miss, process claims faster, and have lower fraud rates.

In 2025 alone, they estimate their AI models added £100 million in value to the business.

These two things work together to drive Admiral’s operating costs down, and reduce the amount they have to pay out in claims.

Third, their reinsurance model means that if there is a huge spike in accidents across the country, Admiral’s partners absorb most of the hit.

That keeps Admiral’s balance sheet safe and healthy.

Put those together, and you have a company that consistently has higher margins than its competitors.

2. Is management capable?

Milena Mondini de Focatiis - CEO

Ms. Mondini de Focatiis has been the CEO since 2021, but she has been with Admiral since 2007.

Was previously Head of UK and European Insurance

Founded ConTe.it, Admiral’s Italian insurance business in 2008 and was previously the CEO

Geraint Jones - CFO

Mr. Jones has been the CFO since 2014 and has been with the company since 2002.

He has overseen a period of massive dividend growth and helped navigate the company through major regulatory changes

The leadership team has reinvested in the business at attractive returns.

Another great sign?

Insiders own a significant portion of the business.

3. Has the company grown the dividend attractively?

We look for:

At least 10 years of dividend growth

5-year dividend growth >5%

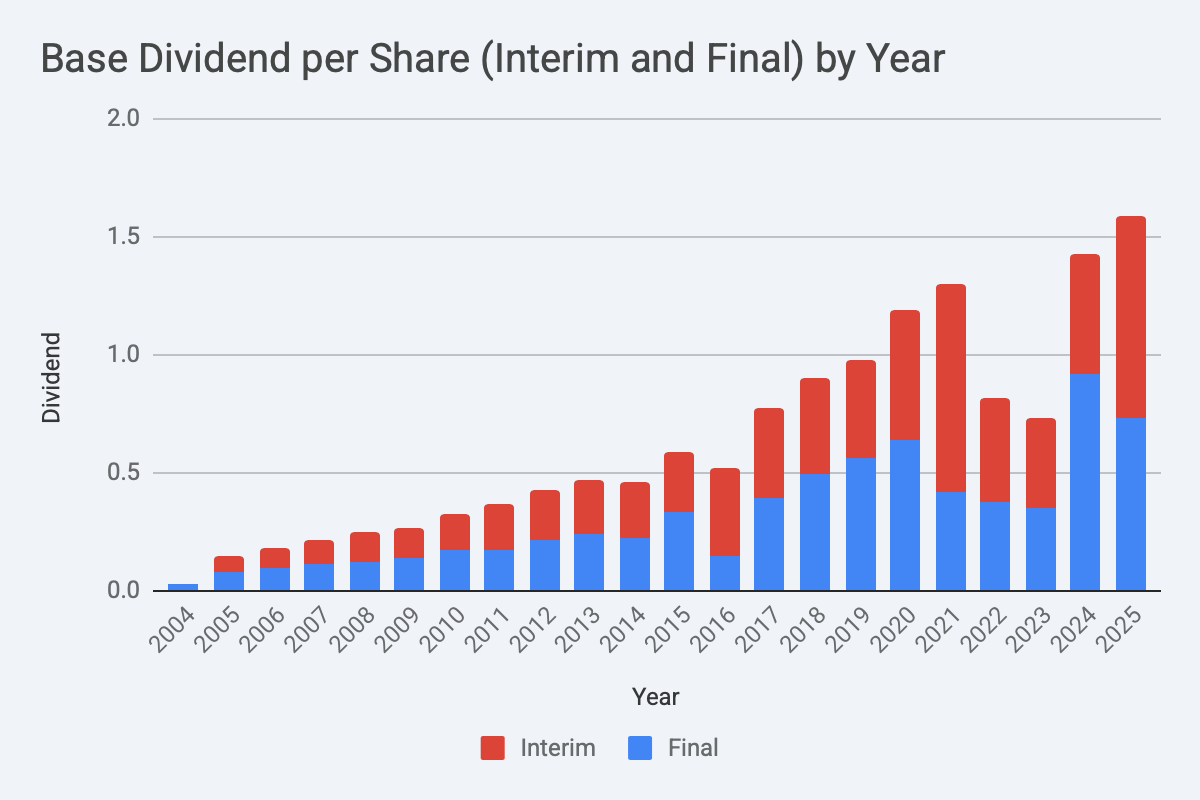

Admiral does have a very strong track record of returning cash to shareholders.

They pay regular dividends 2x per year, but also return extra capital via special dividends.

Over the last 5 years, the dividend has grown at an average rate of about 6% per year.

But Admiral’s dividend growth has not been in a straight line.

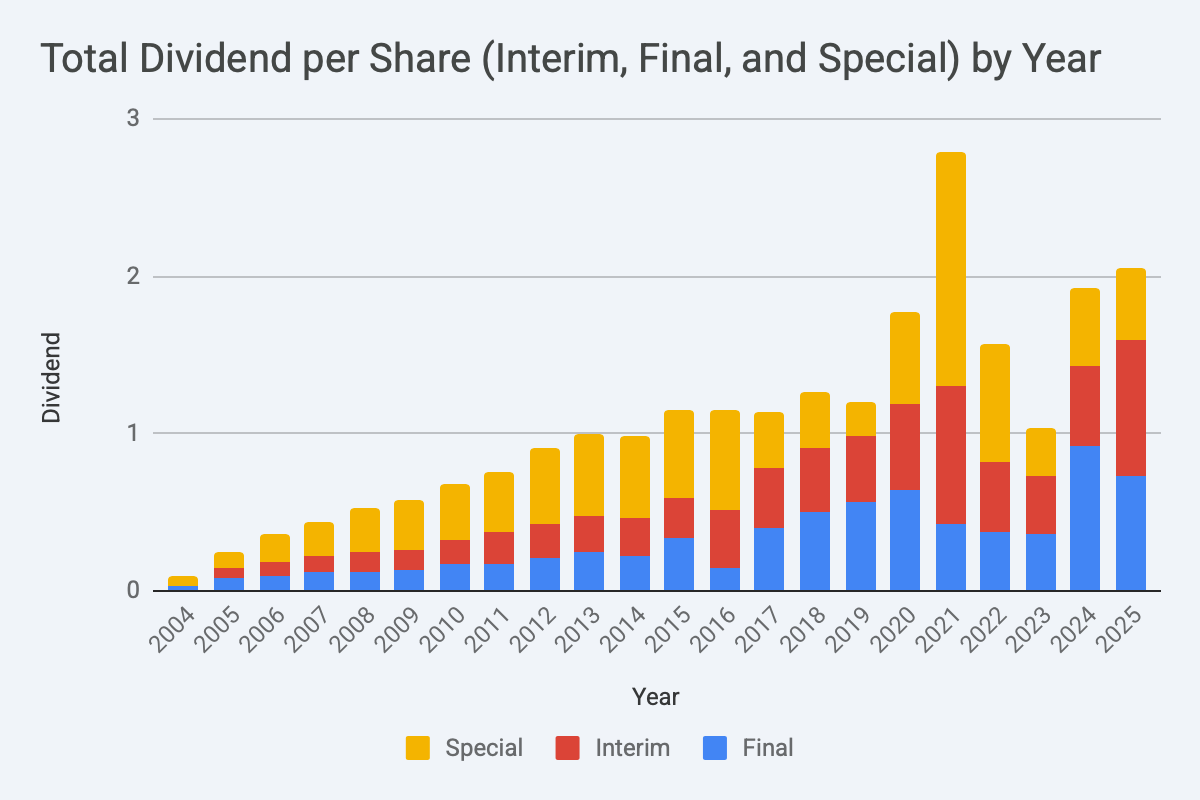

Here’s Admiral’s base Dividend Per Share:

And total Dividends Per Share:

Admiral did reduce their dividends in 2022 and 2023, but after a very large payout in 2021.

Let’s look at what happened.

2021

Dividend: 279.0p (The highest ever)

Business Sale: Admiral sold its price comparison websites (like Confused.com) and gave almost all the cash (£500m) back to shareholders in special dividends

COVID Effects: Because of lockdowns, people weren’t driving. Fewer cars on the road meant almost no accidents, so Admiral kept nearly all the premiums as profit.

2022

The Dividend: 157.0p ( -44%)

Inflation: As the world reopened, the cost of car parts, paint, and labor spiked. Used car prices also rapidly increased, making total loss payouts much more expensive.

Normal Driving: People started driving again, accidents went back to normal levels, and the COVID profit disappeared.

Final Windfall: Shareholders received the last bit of cash from the Confused.com sale (45p).

2023

Dividend: 103.0p

Taxes & Accounting Rules: The UK government raised corporation tax from 19% to 25%, and new accounting rules (IFRS 17) changed how profits were reported. At the same time, the extra cash from the business sale was gone.

Lagging Profits: Admiral was raising its prices, but it takes time for those higher prices to turn into business profit.

While we don’t like to see dividend cuts, if we think like business owners, Admiral’s reduction in dividend payments makes a lot of sense.

Some years you might make a lot of profit - like when you sell off a portion of your operations.

Others years, things outside of your control (like a pandemic and supply chain disruptions) might temporarily hurt your profits.

Admiral responded well after this, spending 2024 aggressively raising its prices ahead of the rest of the market.

This did result in them losing some customers, but I like that management made the tough choice here.

Other insurers kept selling cheap insurance that wouldn’t cover the rising cost of repairs.

Because of this, 2024 and 2025 have returned Admiral’s dividend to growth.

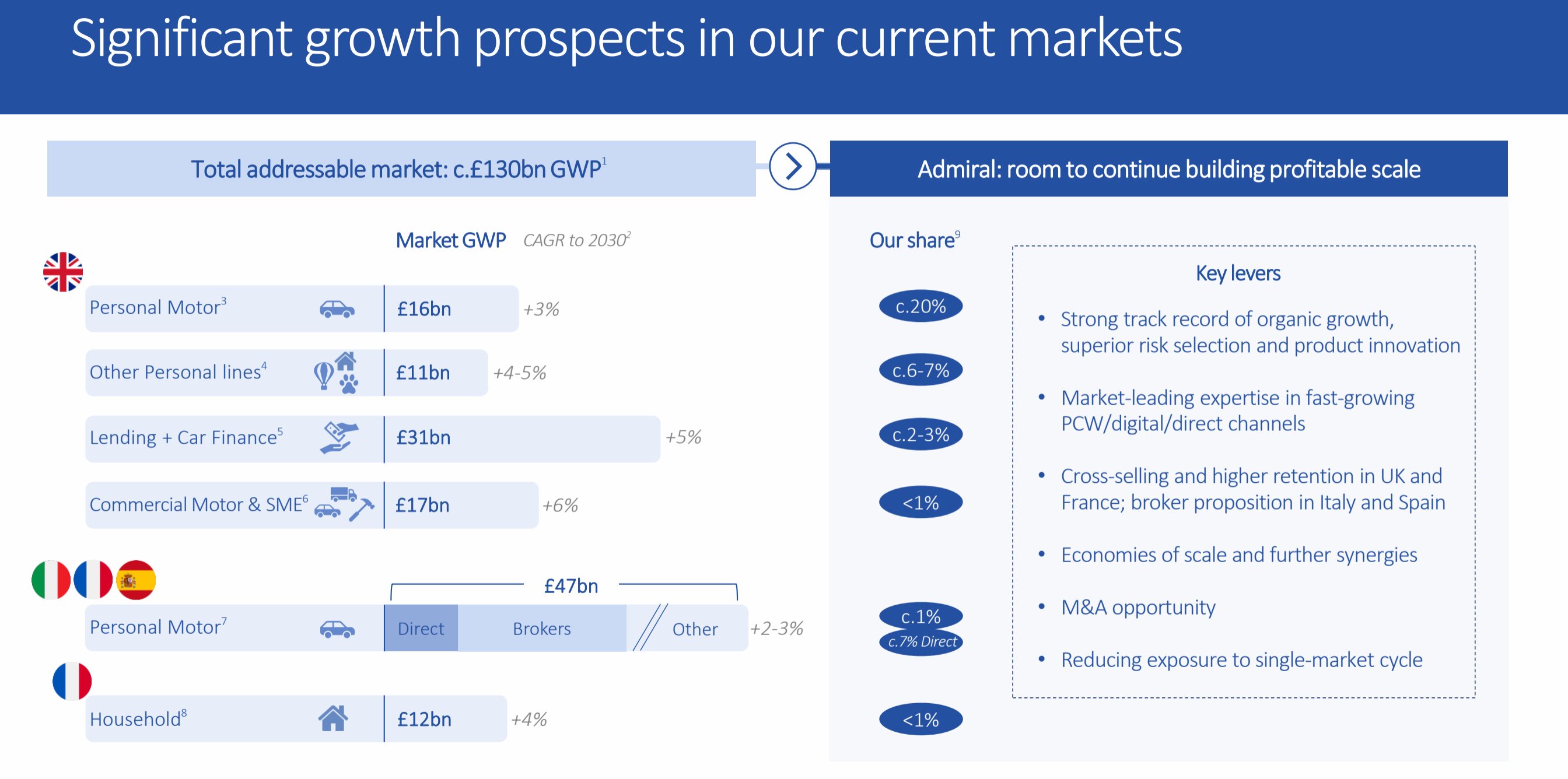

4. Is the company active in an attractive end market?

The UK insurance market is very attractive because it is compulsory.

If you want to drive a car, you must have insurance.

This creates a base level of demand that never goes away, even in a recession.

It’s also got several tailwinds:

Rising Prices: After a few years of low prices, insurance premiums are rising across the market to catch up with inflation.

Technology Shift: As cars get “smarter,” companies with the best data (like Admiral) can price risk much better than traditional players.

Diversification: People are increasingly looking for “all-in-one” providers for their car, home, and pet needs, which plays directly into Admiral’s multi-product strategy.

That market is expected to grow at around 4% per year.

But Admiral is also active in other markets.

In the UK, they are active in:

Home, pet, and travel insurance

Lending and car finance

Commercial motor and small business insurance

These are all expected to grow at between 4% and 6% per year, and Admiral has a very small market share in each.

Their share of the insurance market in the rest of Europe is also much smaller than in the UK, giving Admiral room to grow.

5. What are the main risks for the company?

Regulatory Scrutiny

The UK regulator (FCA) is looking closely at how insurers charge for monthly payments and add-on products. If they force companies to lower these fees, it could hurt Admiral’s other revenue.

Mitigation: Admiral has already lowered its interest rates (APR) on monthly payments and maintains very high customer service scores (rated #1 on Trustpilot) to prove they are providing fair value.

Claims Inflation

The cost of car parts, paint, and labor is going up. If claims become more expensive faster than Admiral can raise its prices, profits could shrink.

Mitigation: Admiral uses real-time data to spot inflation early. They started raising their prices in early 2026, ahead of much of the market, to stay profitable.

Competition

The UK market is fragmented, meaning there are lots of small companies fighting for business. Some might lower prices to an unsustainable level to win customers.

Mitigation: Admiral is disciplined in its underwriting. If prices in the market get too low, Admiral is willing to grow more slowly to ensure every policy they sell is actually profitable.

6. Does the company have a healthy balance sheet?

Because Admiral is an insurance company, we need to change how we look at the balance sheet.

So what do we look at instead?

That’s as far as we can go with this free preview.

Want the rest of the investment case, and to find out if Admiral earns a spot in the Compounding Dividends or High Yield Portfolio?

You can join us here:

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

The 80p combined ratio is the whole thesis and everything else is just supporting evidence. Most investors see an insurance company with a 6% yield and price in the risk of claims inflation without fully pricing in what a 20-year proprietary dataset actually does to your underwriting edge over time. That moat compounds quietly while the market focuses on the headline worry. The best setups usually look like this: a dominant operator in a mandatory market, temporarily discounted because the near-term concern is real but the structural advantage is more durable than the discount implies.