Best Buys April 2026

A new month, a new Best Buys List.

Each month, I’ll give an overview of my favorite stocks of the month.

Let’s dive into this update and show you some of my favorite stocks.

March 2026

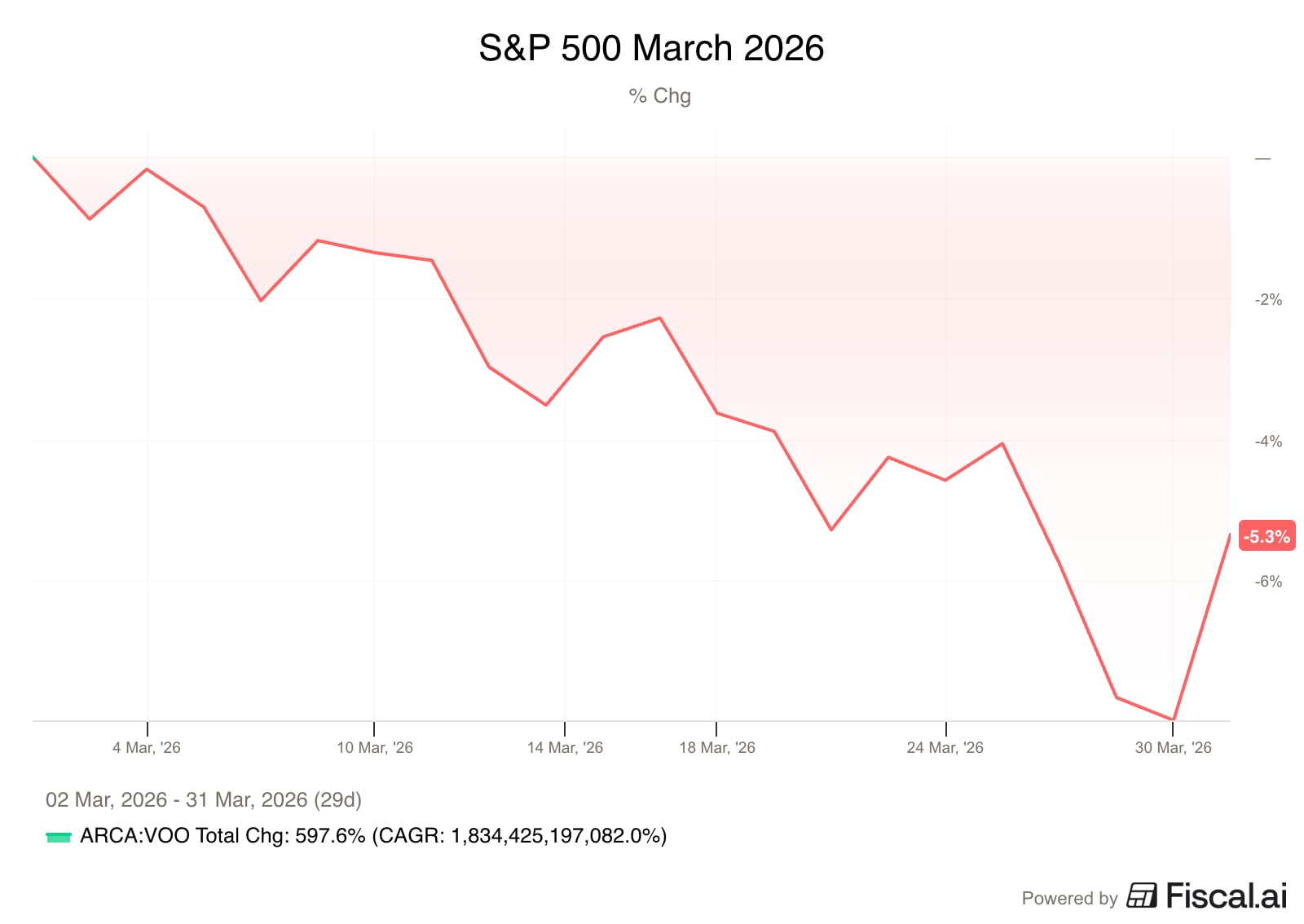

The S&P 500 declined by 5.3% in March.

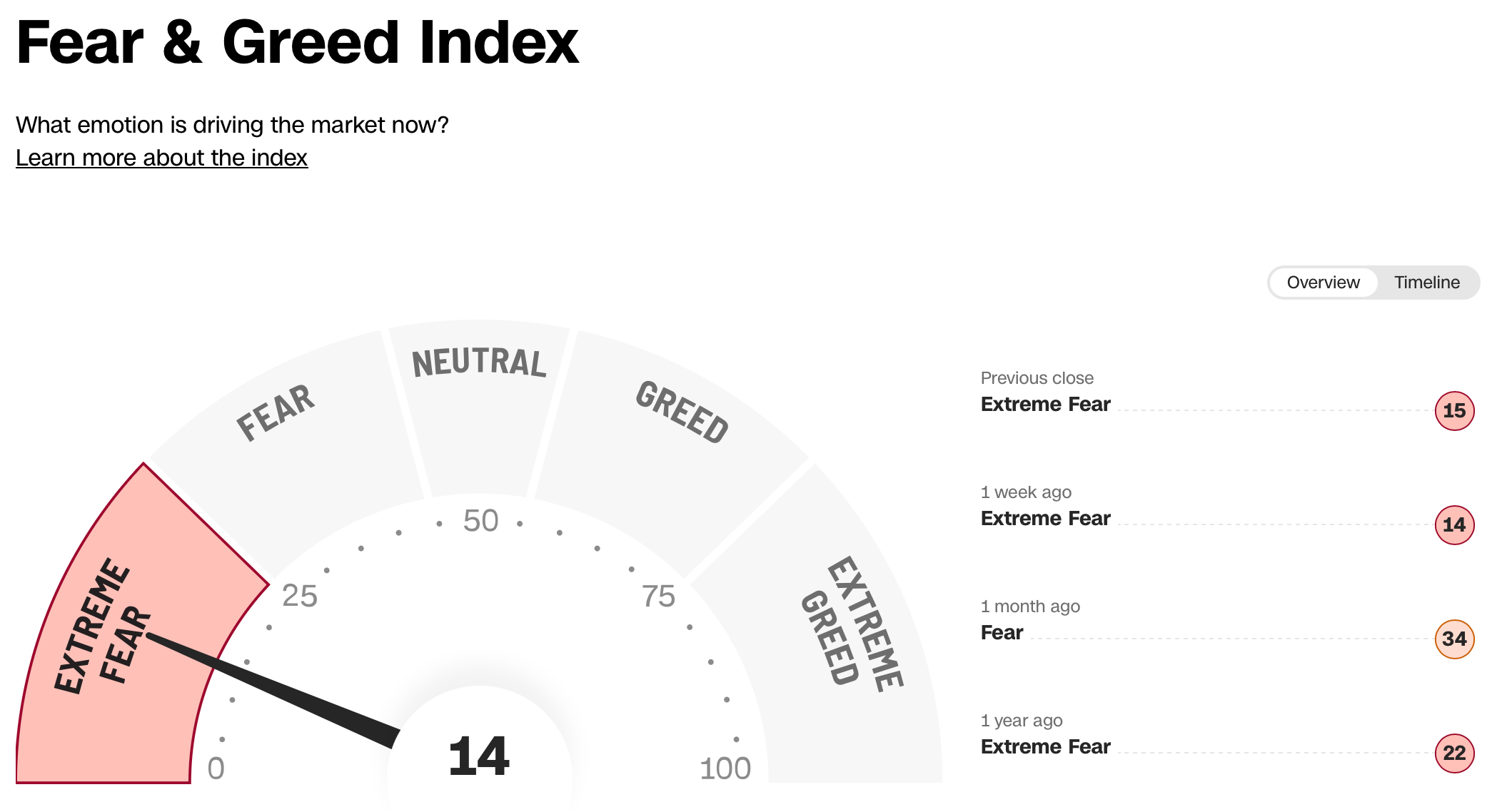

Investors are in Extreme Fear today according to the Fear & Greed Index:

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

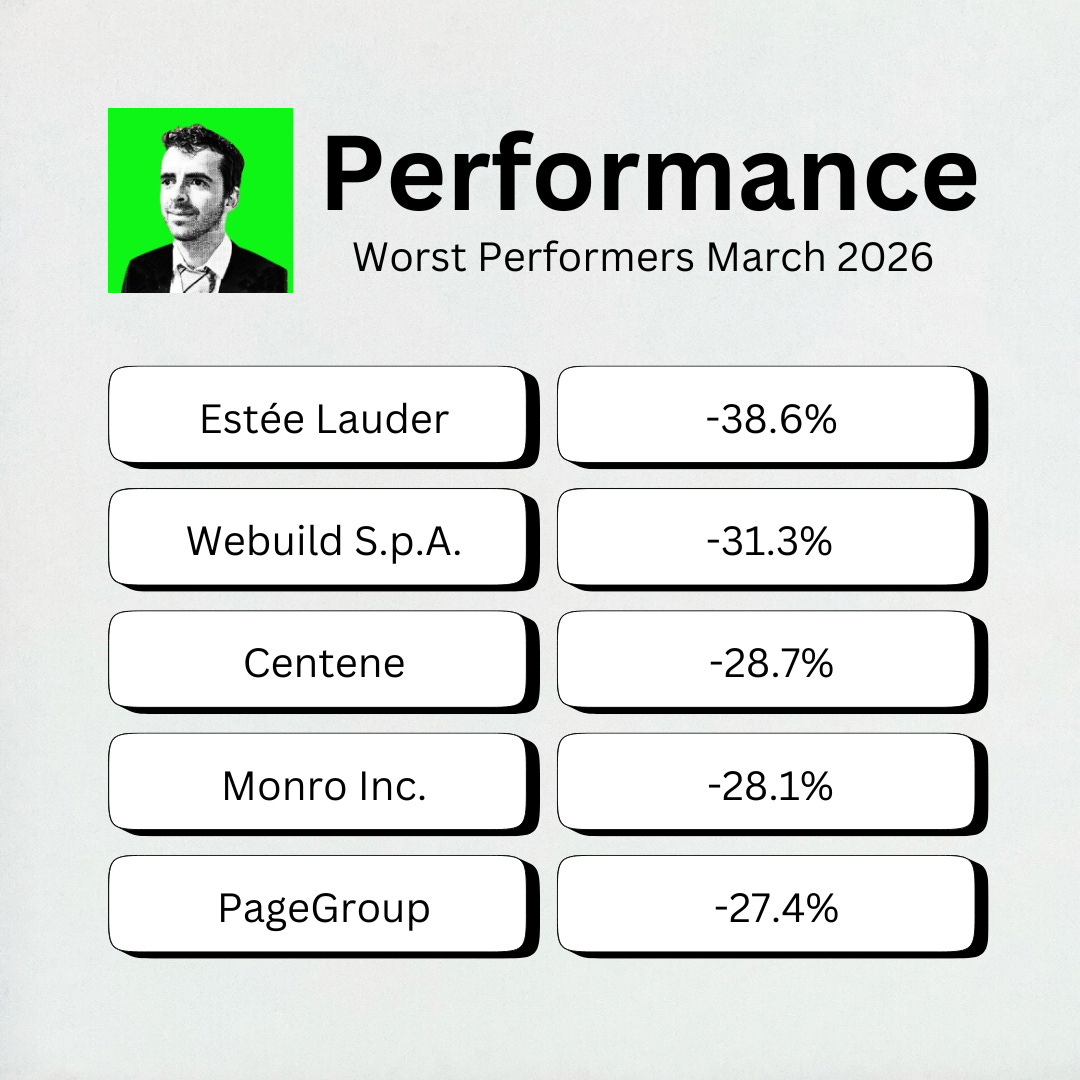

Worst performers

The cheaper we can buy great companies, the better.

The biggest decliner this month? Estée Lauder, losing 38%.

Estée Lauder is a prestige beauty company that makes and sells high-end skincare, makeup, fragrance, and hair care products under brands like La Mer, Clinique, and M·A·C.

Estée Lauder fell this month due to merger uncertainty and macroeconomic headwinds:

They confirmed they are in discussions for a potential merger with Puig and investors are afraid of dilution or distraction while the company is trying to turn itself around

Management warned that tariffs could cost $100 million, bringing expected profits down

Weakness in China continues to be a problem

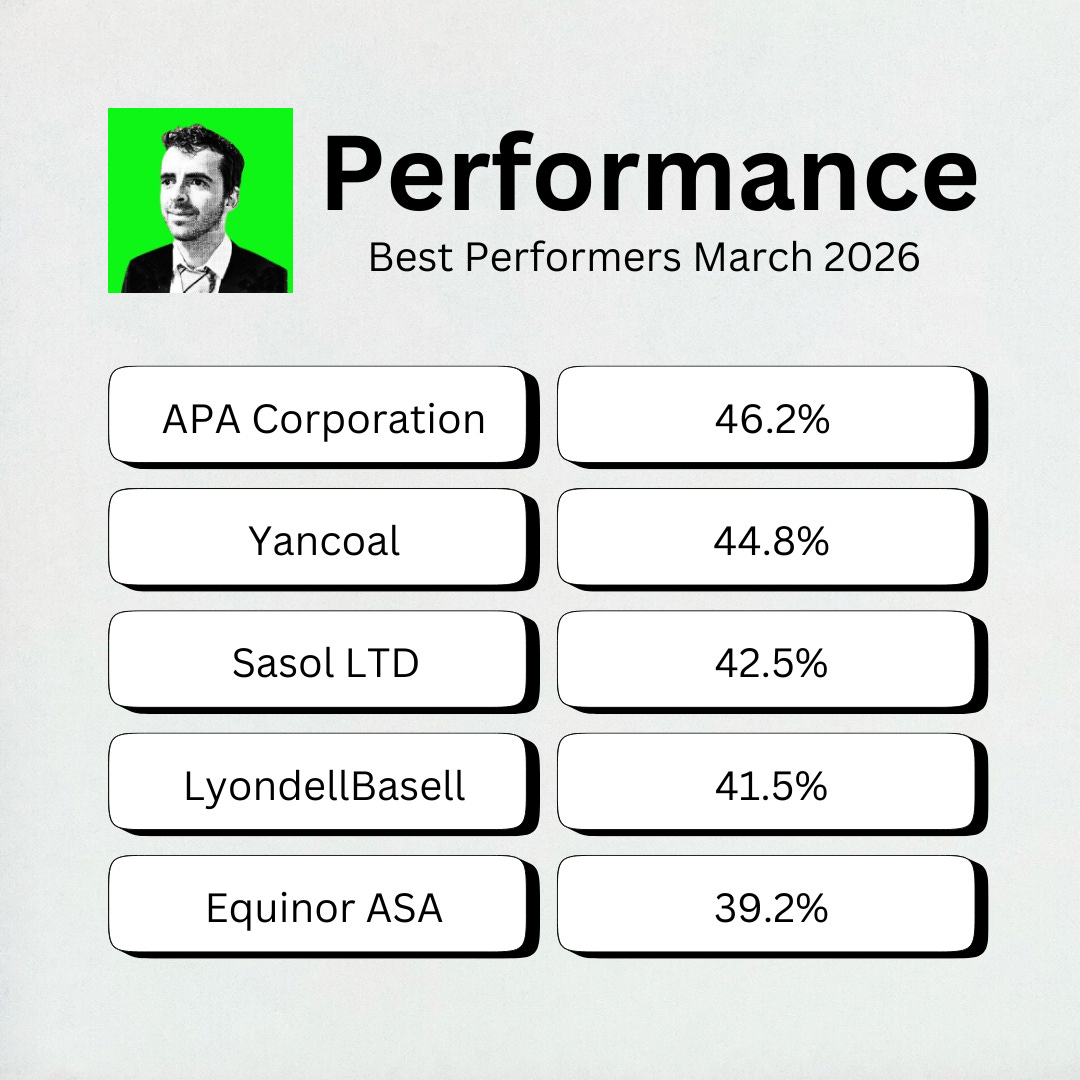

Best Performers

APA Corporation was this month’s best performer, rising 46%!

APA Corporation is an oil and gas exploration and production company. They have operations in the U.S., Egypt, and the North Sea.

APA had a lot of good things come together all at once:

Better Earnings: They earned $0.91 per share, versus analysts’ expected $0.62 by lowering their costs and pumping more oil.

War and Oil Prices: Conflict in the Middle East caused oil prices to rise. Higher oil prices mean higher profits for APA.

Buying Back Shares: The company has been aggressively buying back shares, retiring over 28% of outstanding shares since 2018.

Spotlight: Lower Prices Mean Higher Paychecks

Today’s headlines are scary.

Oil over $100, inflation fears, recession worries, falling stock prices.

It feels like everything is falling apart.

But I’m not panicked, and you shouldn’t be either.

The secret to staying calm?

Think like a business owner, not a speculator.

Thinking Like an Owner

Imagine that you own the busiest gas station in town. It’s been paying your bills and supporting your family for years.

Then a recession hits. You notice:

Customers are choosing regular gas instead of premium

Fewer people are grabbing snacks or coffee inside

Your monthly profit drops about 10% for a few months

Now a local investor knocks on your door and offers to buy your gas station for half of what it was worth last year.

Do you sell?

No way. People still need to drive. Recessions end. Inflation cools down.

You wouldn’t give away a perfectly good business at a bargain price just because things are temporarily slow.

But that’s exactly what happens in the stock market.

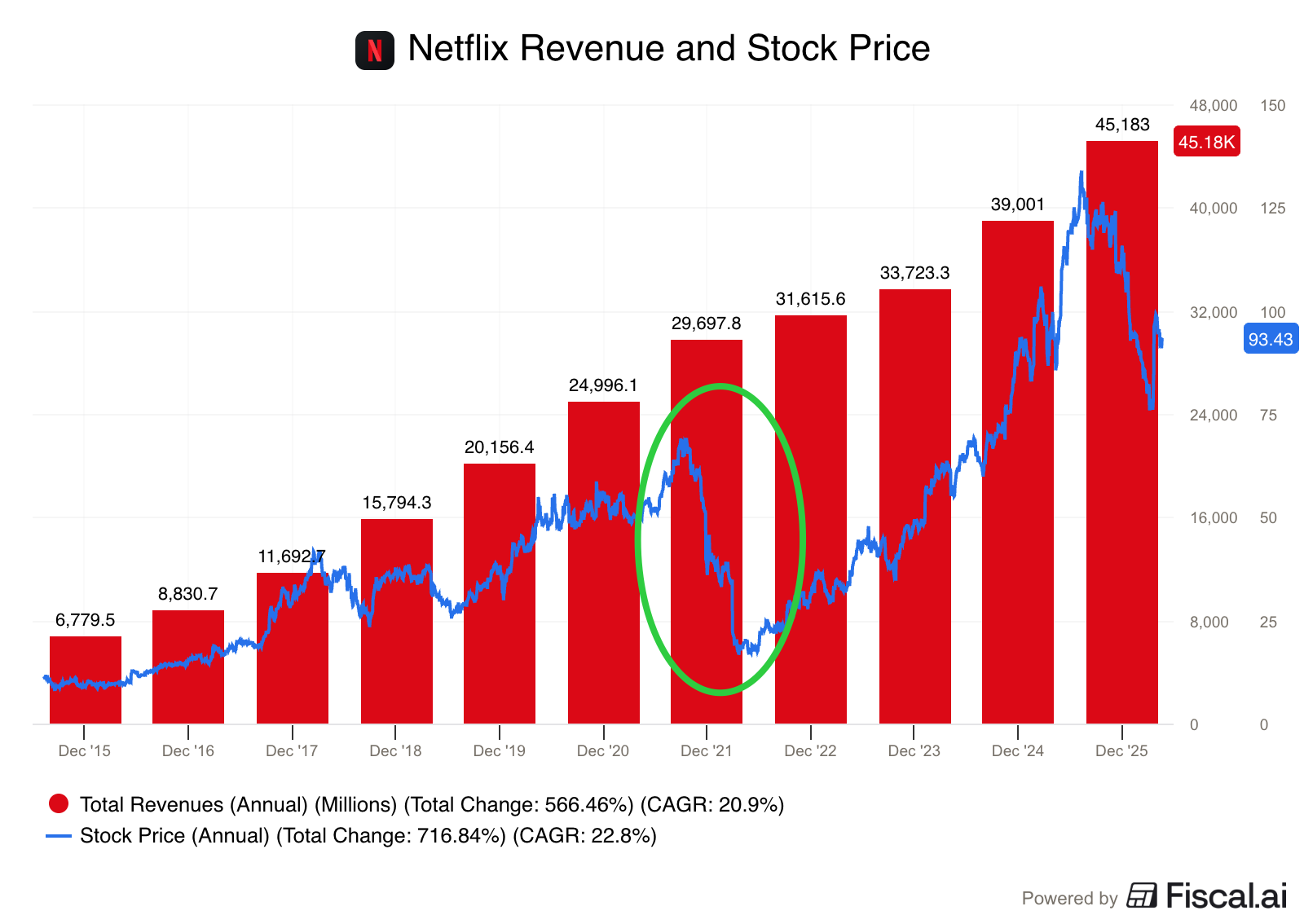

In 2022, Netflix saw a small drop in subscribers.

It barely had an effect on Revenue, but the stock went from around $70 a share down to $17.

The headlines were scary then too.

But if you bought Netflix at $20 a share in 2022, you’ve gained 46% on your investment every single year since then.

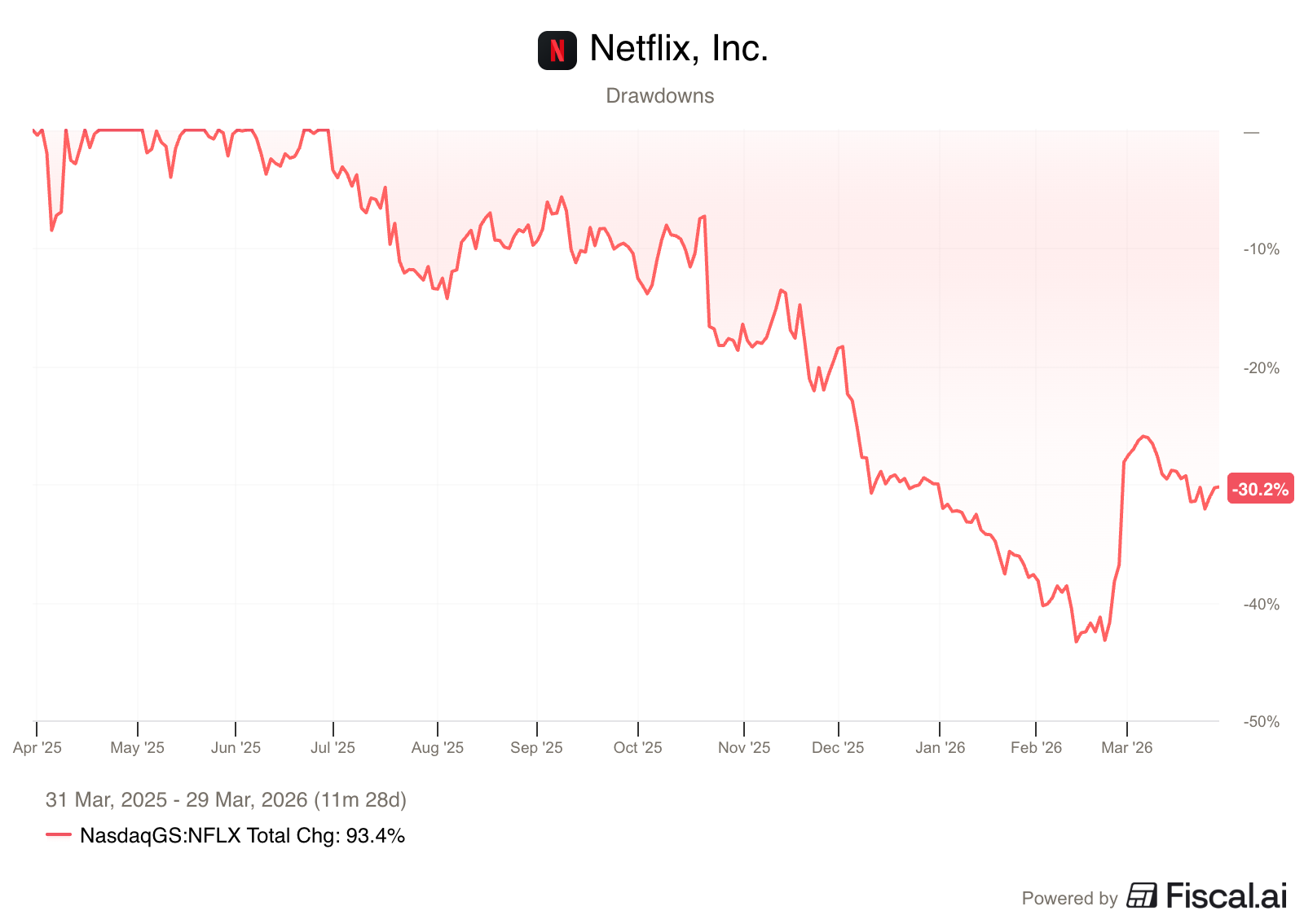

And that includes another -40% drawdown related to the attempt to buy Warner Bros. Discovery.

That’s the difference between an owner and a speculator.

Owners look at long-term cash flow

Speculators look at today’s price

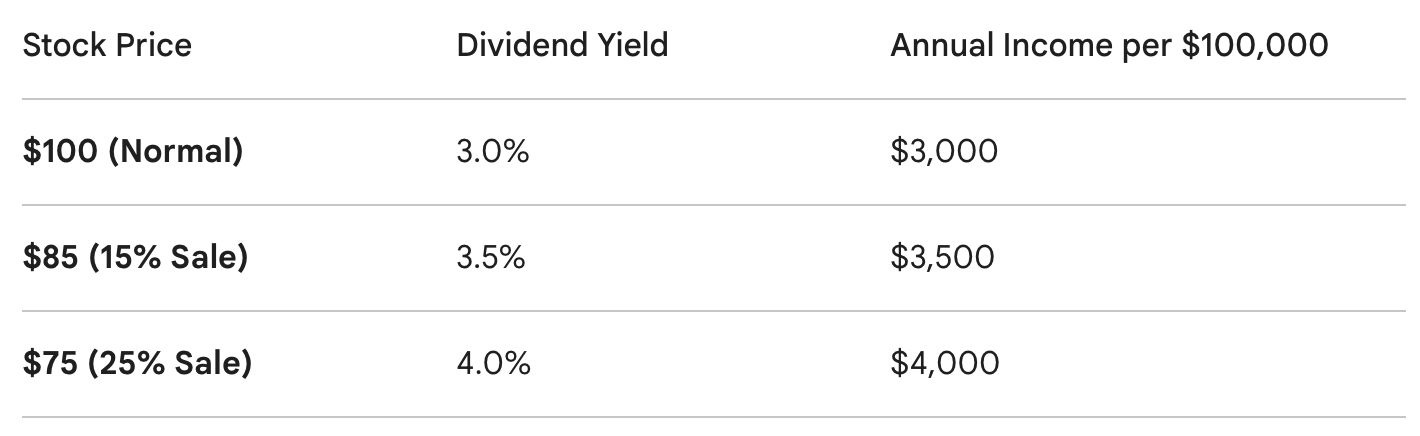

Lower Prices Mean More Income

When the stock market panics, it puts good companies on sale.

For income investors, that’s actually a raise.

Every dollar you invest buys more income than it did before.

Here’s what $100,000 buys you at different price levels:

Buying a great company at a 25% discount doesn’t mean you’re losing money.

It means you’re locking in 33% more passive income. Permanently.

Watch the Business, Not the Price

Instead of checking your stock prices every day, track what the business is actually earning for you.

You can use the Owner’s Earnings Formula:

Your Return = Earnings Growth + Dividend Yield

If a company keeps growing its earnings and keeps paying its dividend, the business is fine.

The daily price is just noise.

What You Should Remember

Speculators see a falling price and think something is broken.

They sell in a panic.

Owners see a falling price and ask: is the business still running well?

If the answer is yes, they see a sale, and they buy more.

While everyone else worries about the next headline, we’ll keep buying more income at better prices.

April Best Buys

I scanned the Buy-Hold-Sell List for great dividend payers at attractive prices to highlight for you this month.

Let’s dive into 5 of the most interesting ones I found!

By monthly tradition, here are our five favorite income stocks for April.

What’s happening in the markets? Where is the income? Let’s get a little bit wiser today.

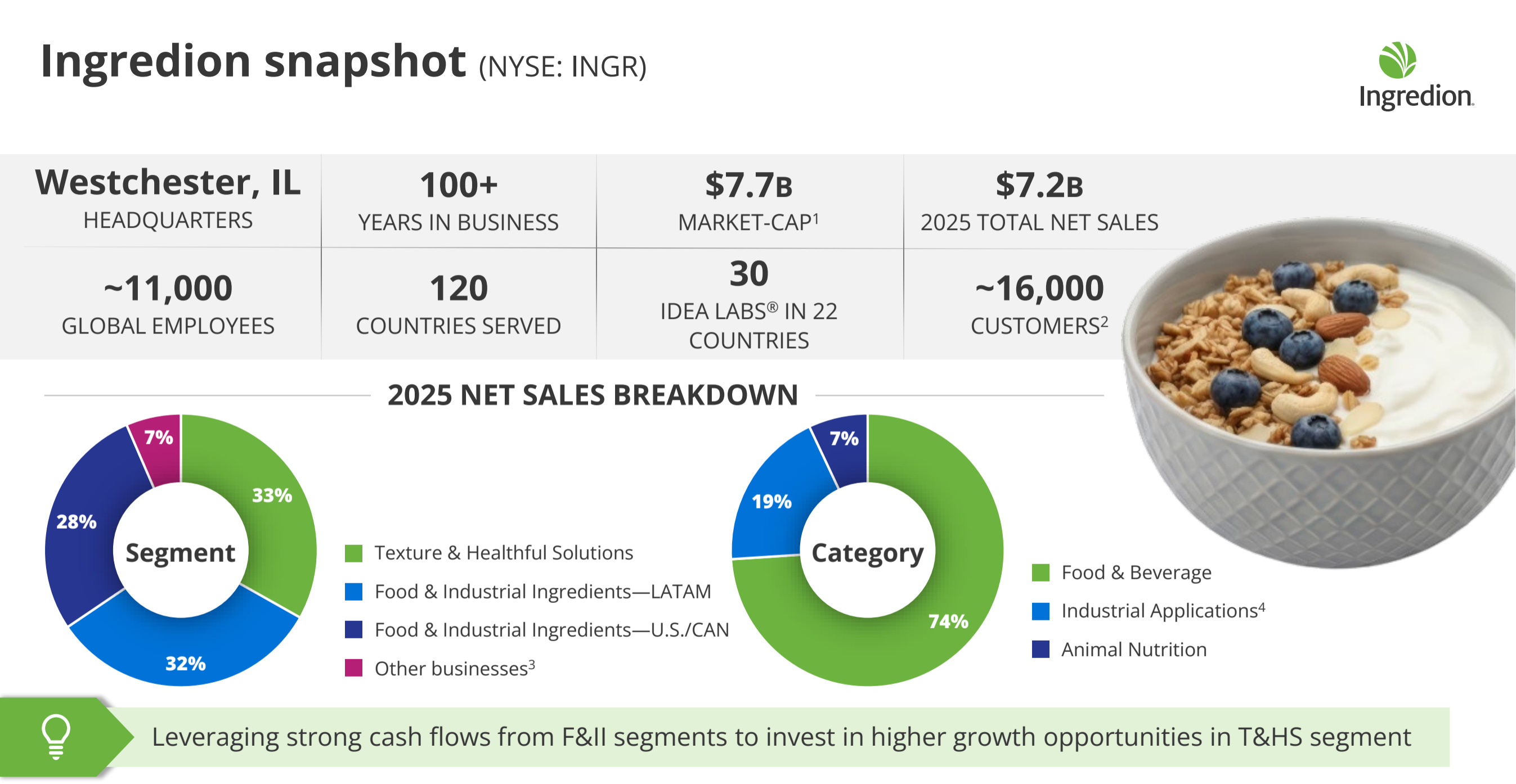

5. Ingredion (INGR)

If you’ve eaten a salad dressing or protein bar recently, there’s a good chance an Ingredion ingredient was in it.

It’s one of the most boring companies you’ll ever come across.

That’s exactly why we love it.

The moat here is simple: scale and switching costs.

Ingredion is one of the only companies with the global reach to supply the world’s largest food brands.

And once a food manufacturer locks in a starch supplier, they almost never switch.

Why?

Because a tiny change in starch quality can ruin the taste of a billion-dollar product.

That’s a powerful reason to stay put.

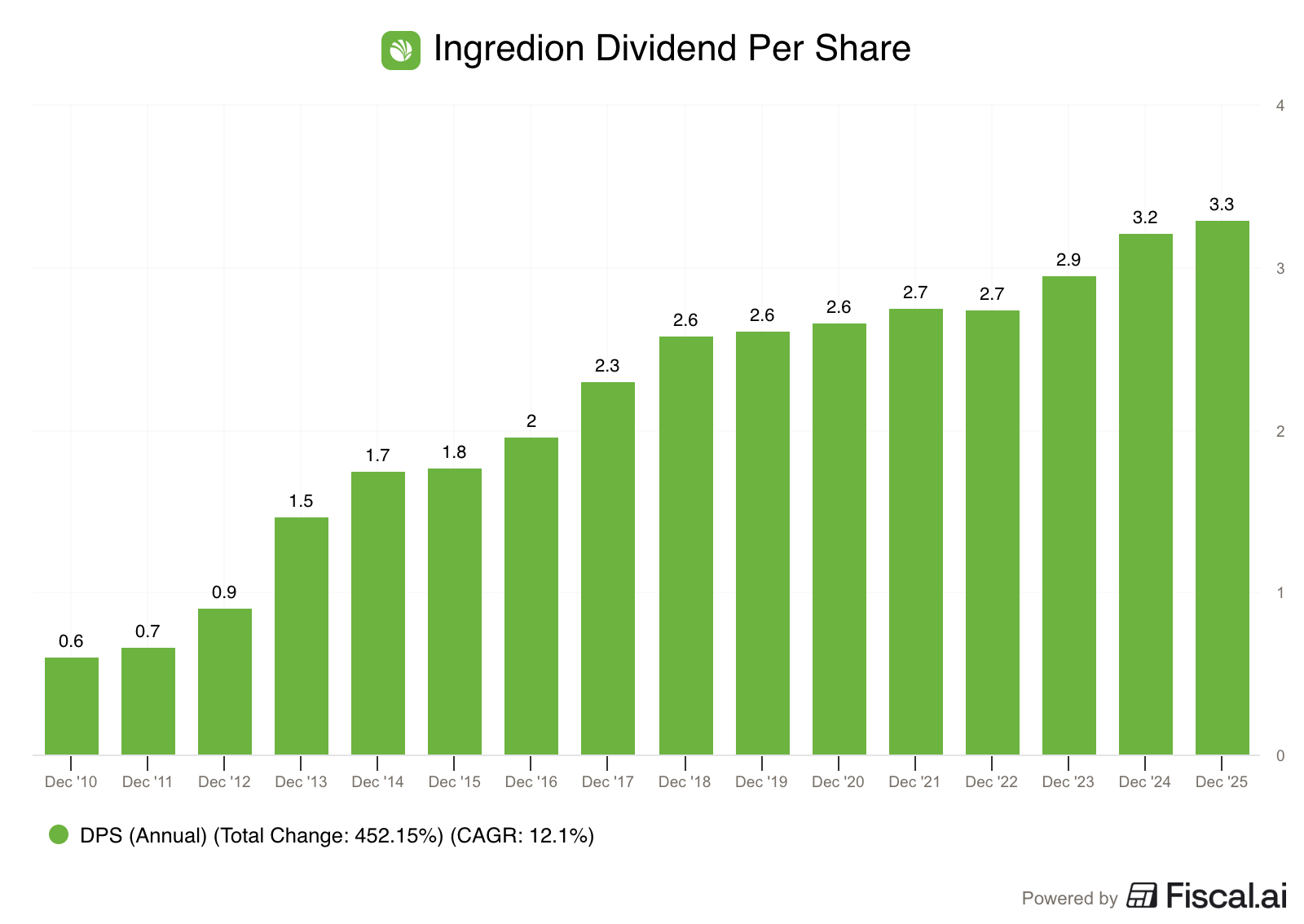

The result? 16 consecutive years of dividend growth.

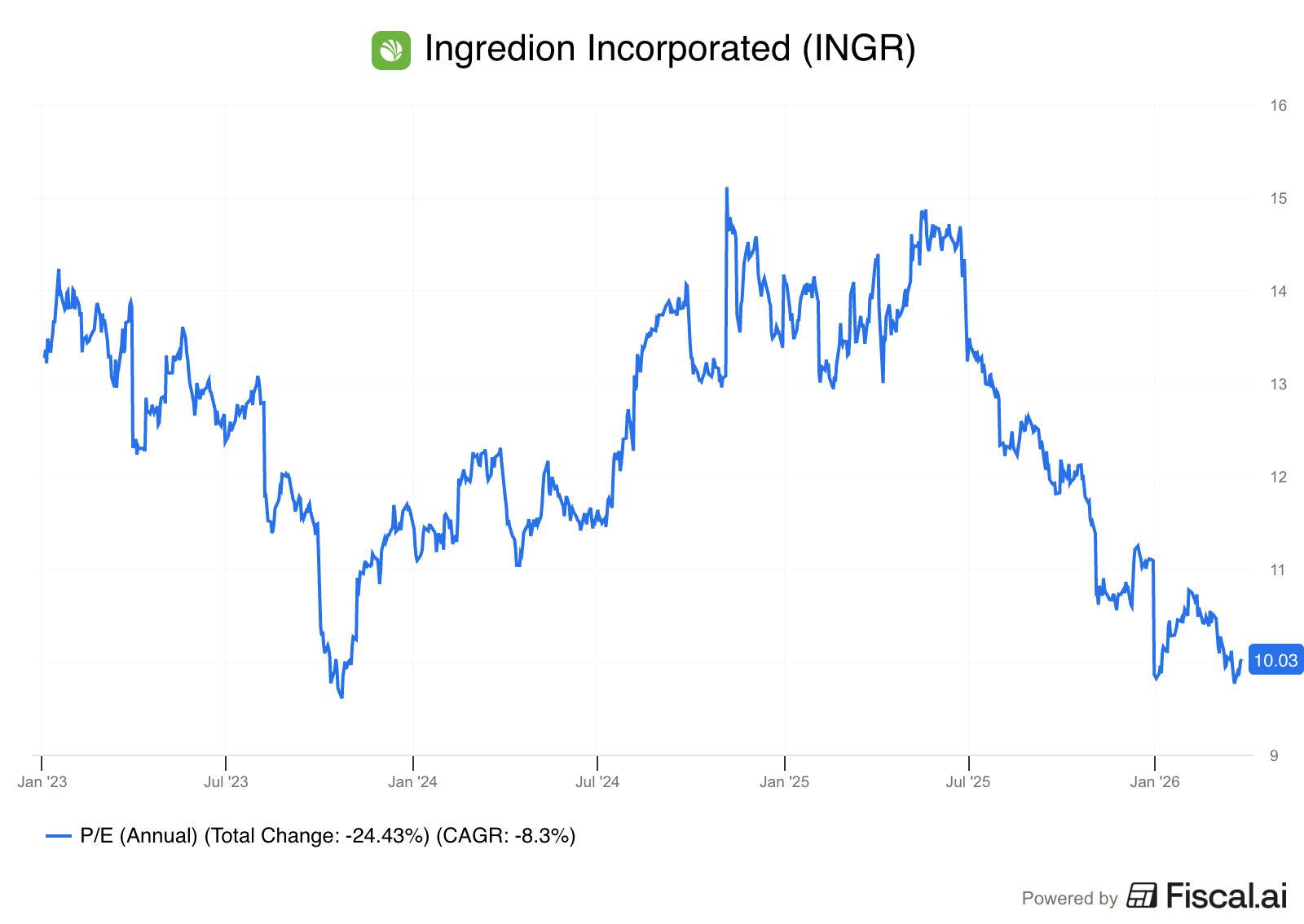

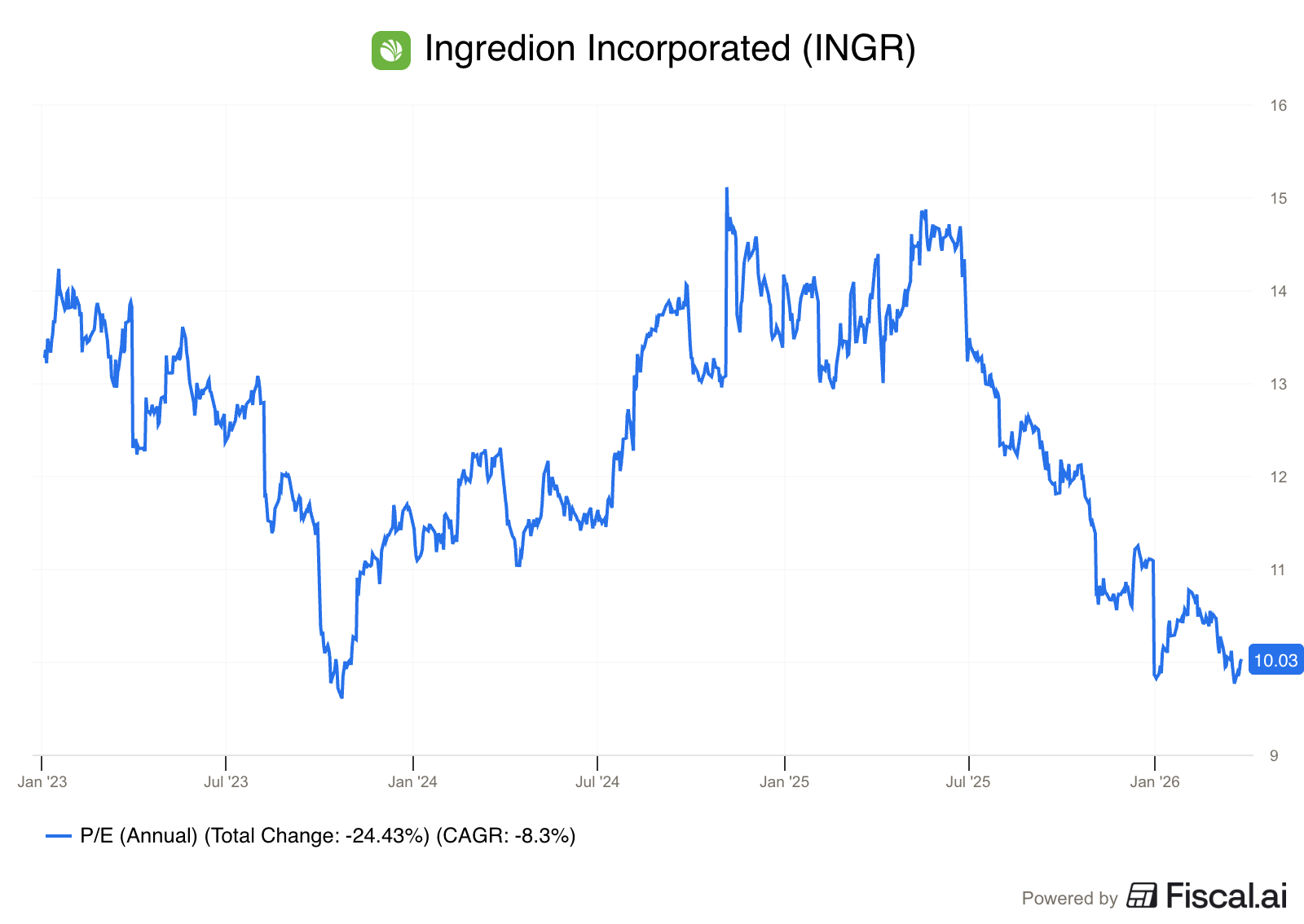

Why is the stock cheap?

Two reasons. First, fluctuating corn prices have spooked some investors about near-term revenue.

Second, nobody talks about Ingredion when there are AI stocks to chase.

That neglect has left the stock at just 10 times earnings.

That gives us the opportunity to buy a defensive staple at a value price.

You get to collect a safe 3% yield today.

With plenty of room for continued dividend hikes as earnings grow, and room for the multiple to expand as well.

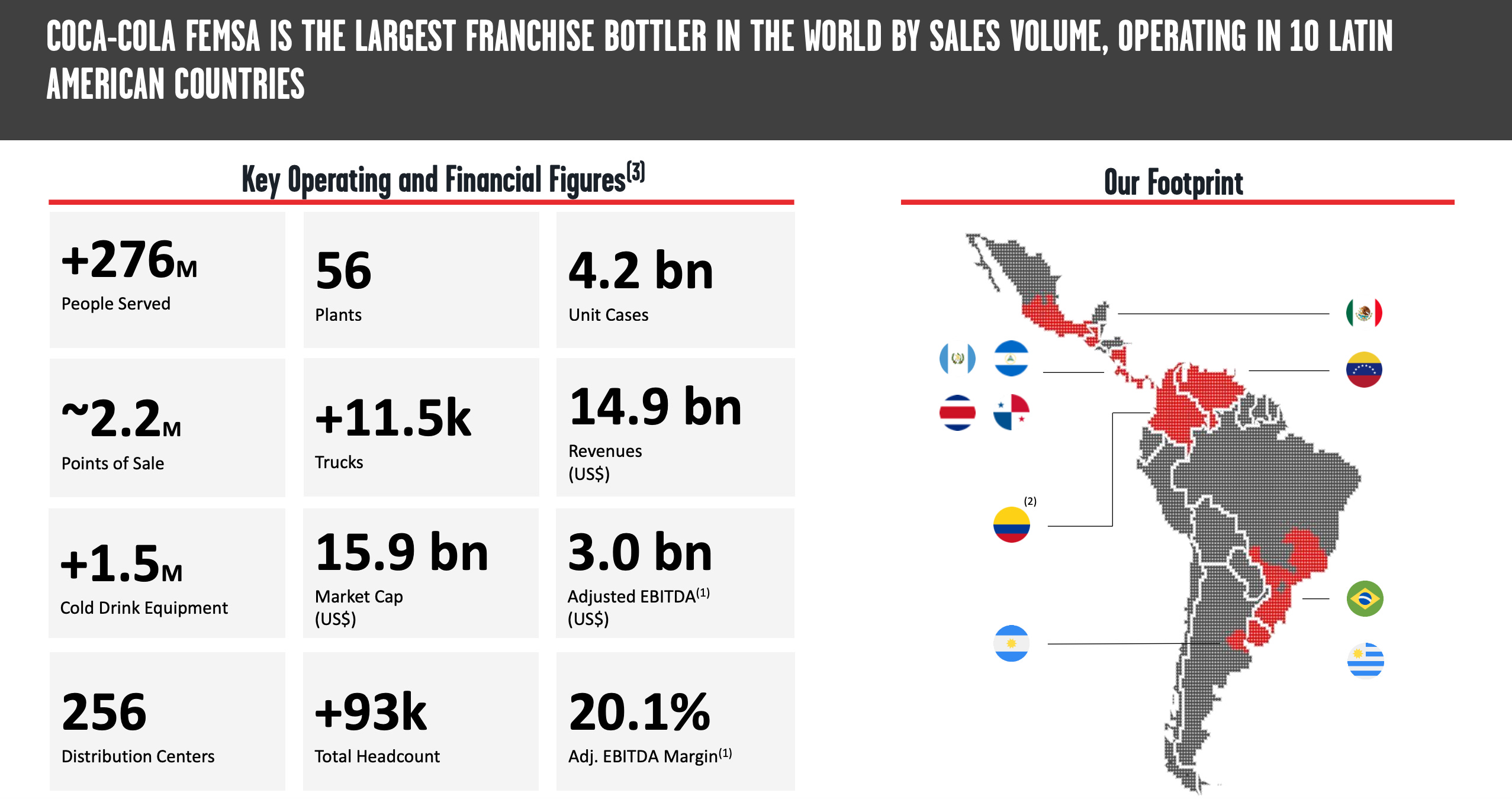

4. Coca-Cola FEMSA (KOF)

Think of KOF is the last mile of Coca-Cola’s empire in fast-growing markets.

They own the trucks. They own the relationships. And they own a distribution network that would cost billions to replicate.

Just like their parent company, Coca-Cola FEMSA has pricing power.

When inflation rises in Mexico or Brazil, KOF simply raises the price of a Coke.

Customers keep buying.

A cold Coke is one of life’s affordable pleasures, recession or not.

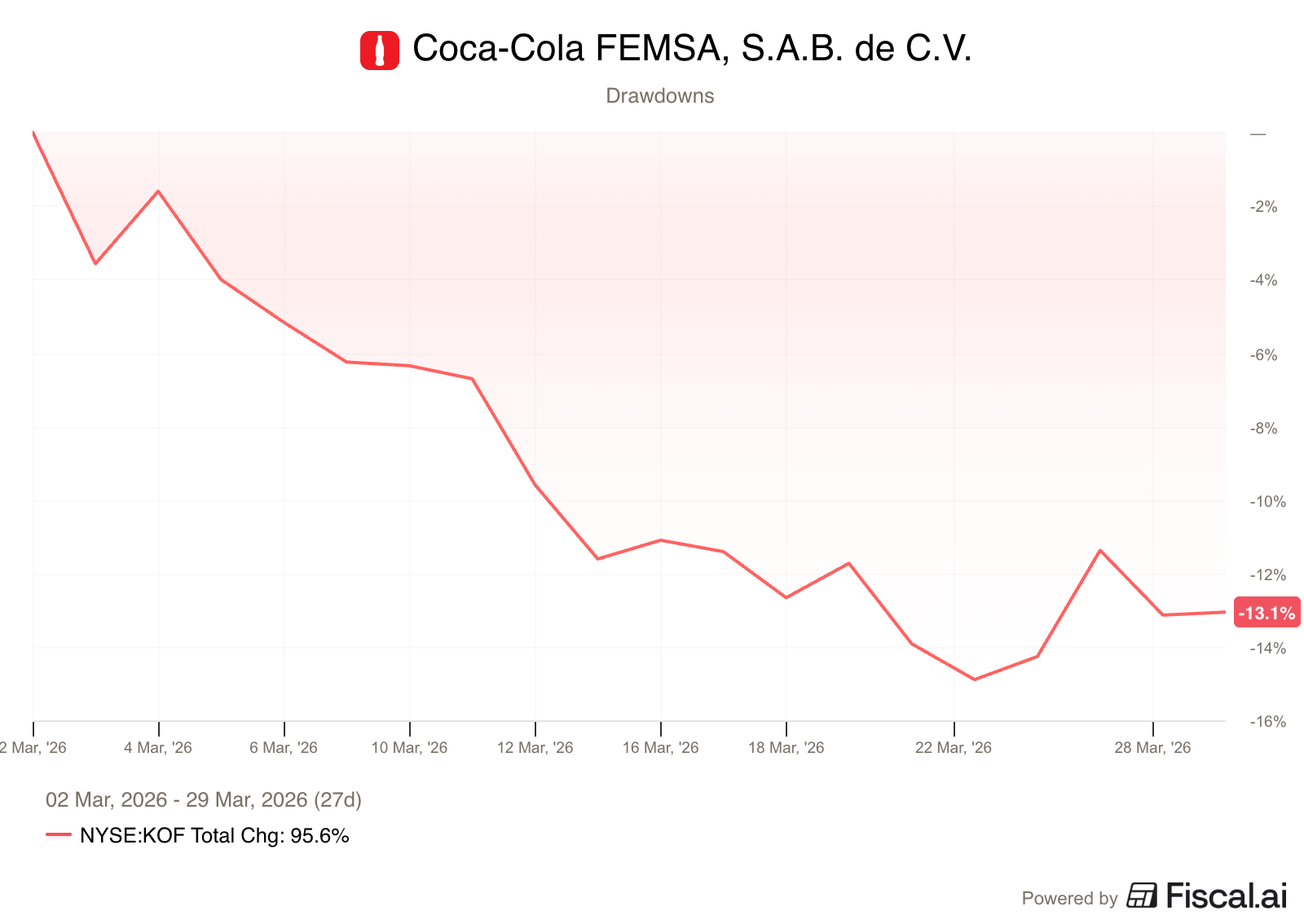

Why is the stock cheap?

The stock has fallen about 13% in the past month.

Earnings Miss: Coca-Cola FEMSA missed both revenue and profit targets from Wall Street.

Rising Costs: Geopolitical tensions and high oil prices made it more expensive to make bottles and ship products.

New Taxes: Investors are worried about a new excise tax in Mexico.

Leadership Change: The broader Coca-Cola system is changing CEOs

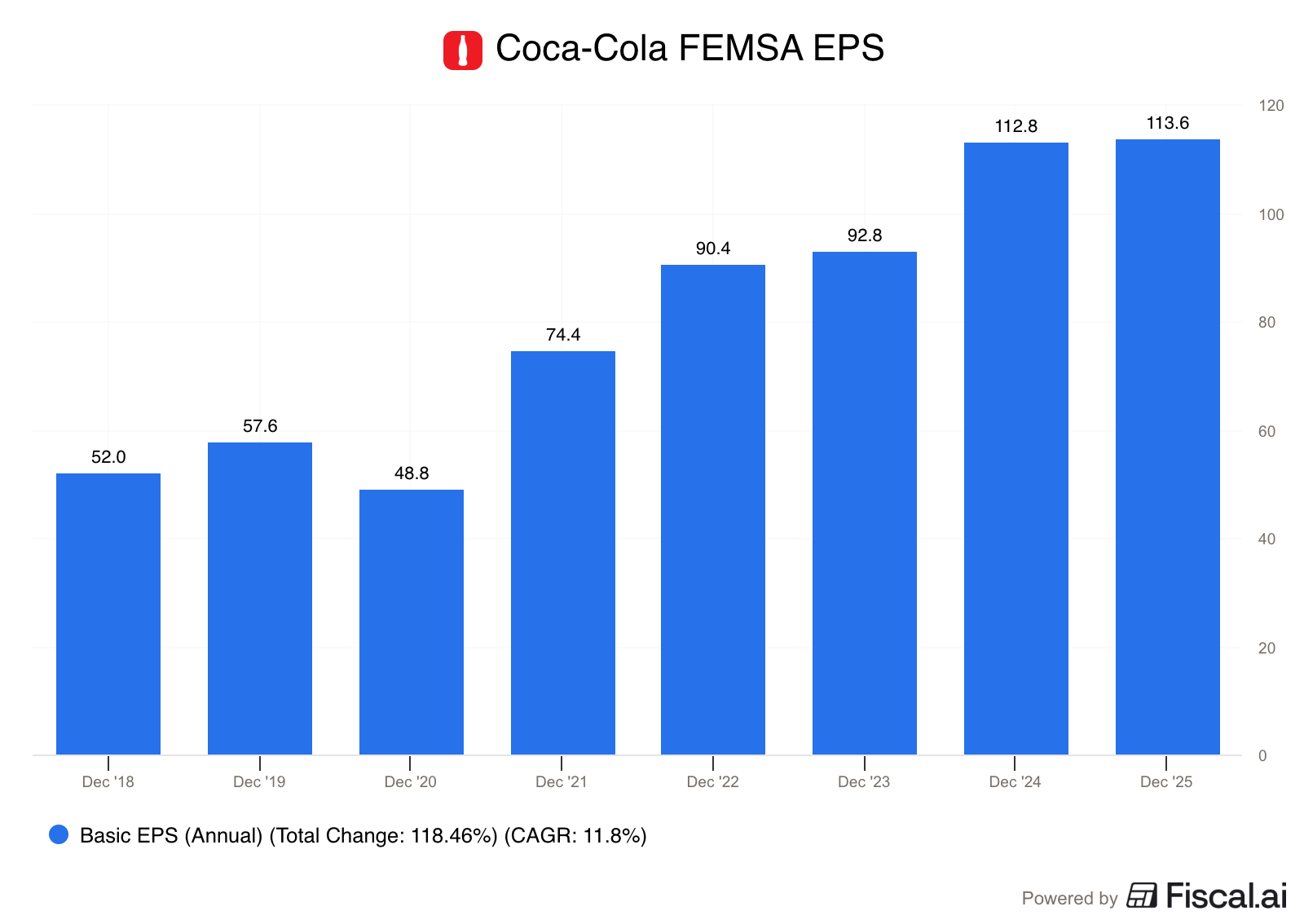

But here’s what matters: the profits are real.

The business hasn’t changed, but the price tag has.

Coca-Cola FEMSA has a 4.3% yield backed by one of the most recognizable brands on Earth.

You’ve just seen two of my favorite stocks for April, but paid Partners get three more.

Whenever you’re ready

Whenever you’re ready, here’s how I can help you:

✍️ Three articles per week (Monday, Wednesday, and Saturday)

📚 Full access to our entire library of data-driven articles

📈 An insight into our Portfolio full of interesting Dividend Stocks

🔎 Full investment cases about interesting companies

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.

There’s always a moment in markets where the language shifts from “what’s the business worth” to “what’s the chart doing,” and that’s usually when the opportunity is already forming beneath the noise.

The owner mindset works—until the tape starts telling a different story. Sometimes price is just noise around a stable business. Other times it’s the first signal that something subtle has changed before the fundamentals catch up. The hard part is knowing which game you’re in.

The best operators I’ve seen aren’t married to either side. They think like owners when things are quiet, and like traders when behavior starts to deviate. Because once the market stops valuing something the way it used to, it doesn’t matter how good the business is in theory—the auction has already begun to move elsewhere.

That’s where most people get trapped, holding something “cheap” while the market quietly reprices what cheap actually means.