Best Buys July 2026

A new month, a new Best Buys List.

Each month, I’ll give an overview of my favorite stocks of the month.

Let’s dive into this update and show you some of my favorite stocks.

June 2026

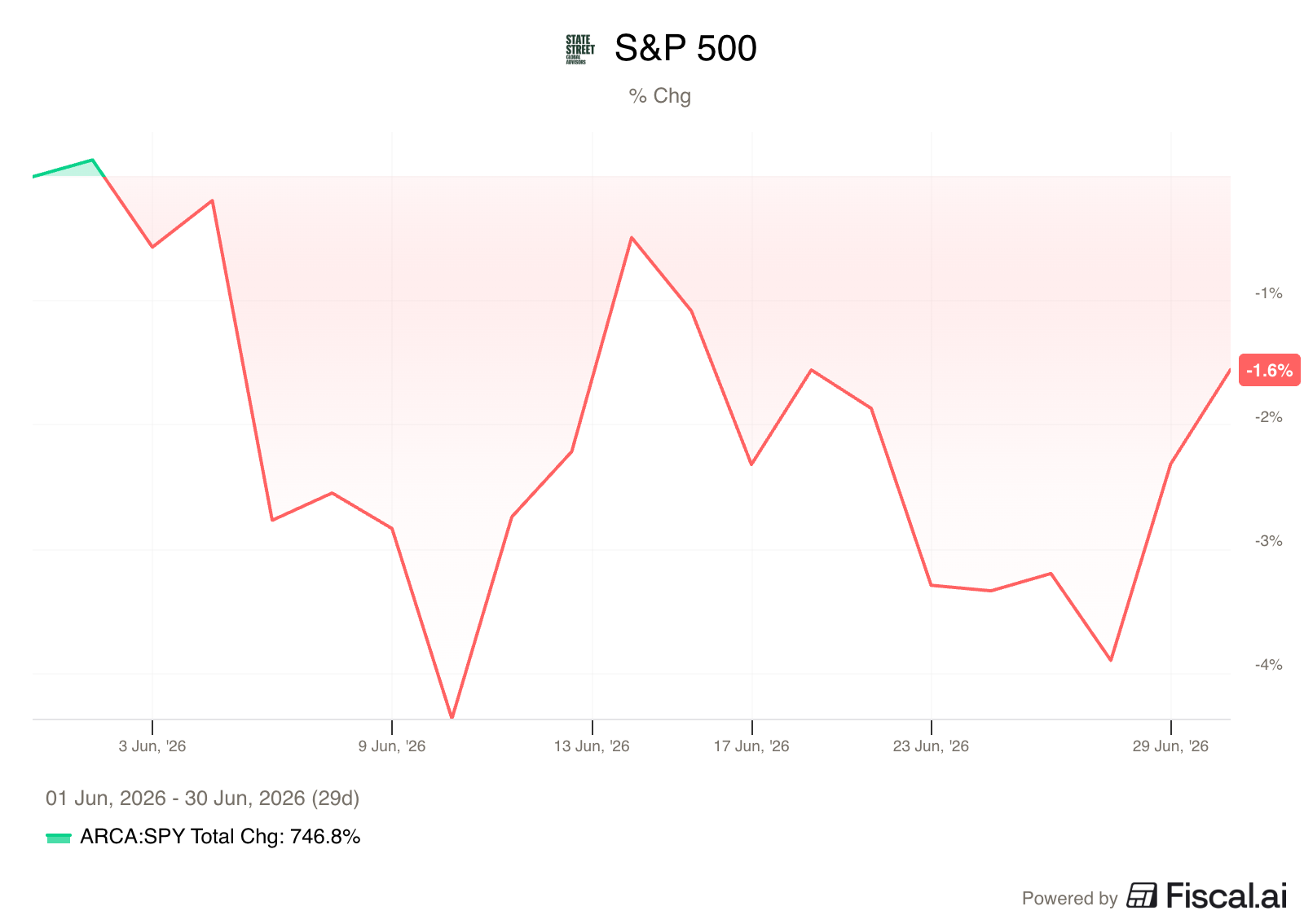

The S&P 500 fell -1.6% in June.

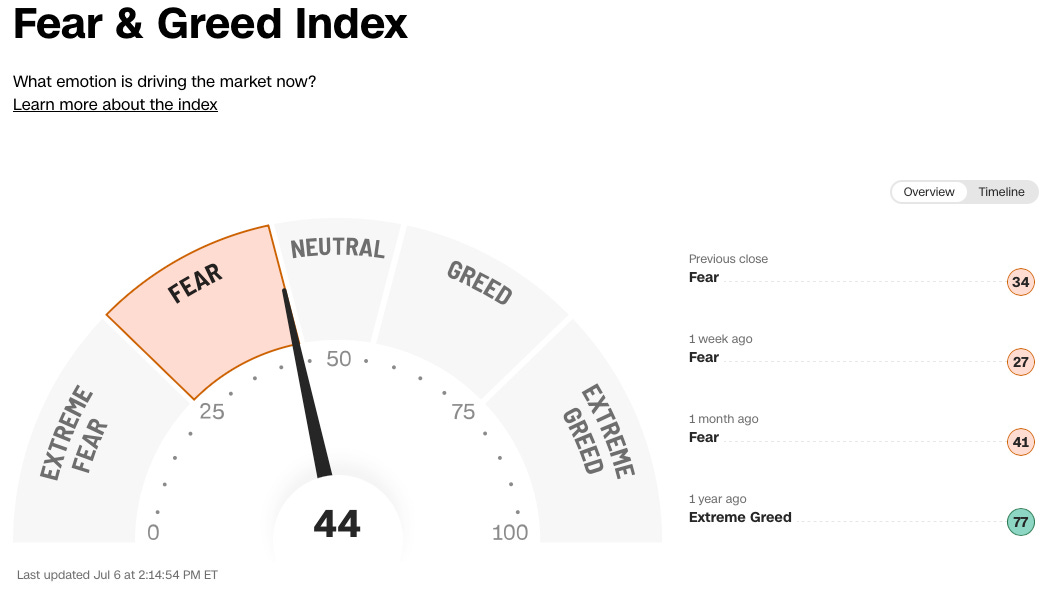

Investors are fearful today according to the Fear & Greed Index:

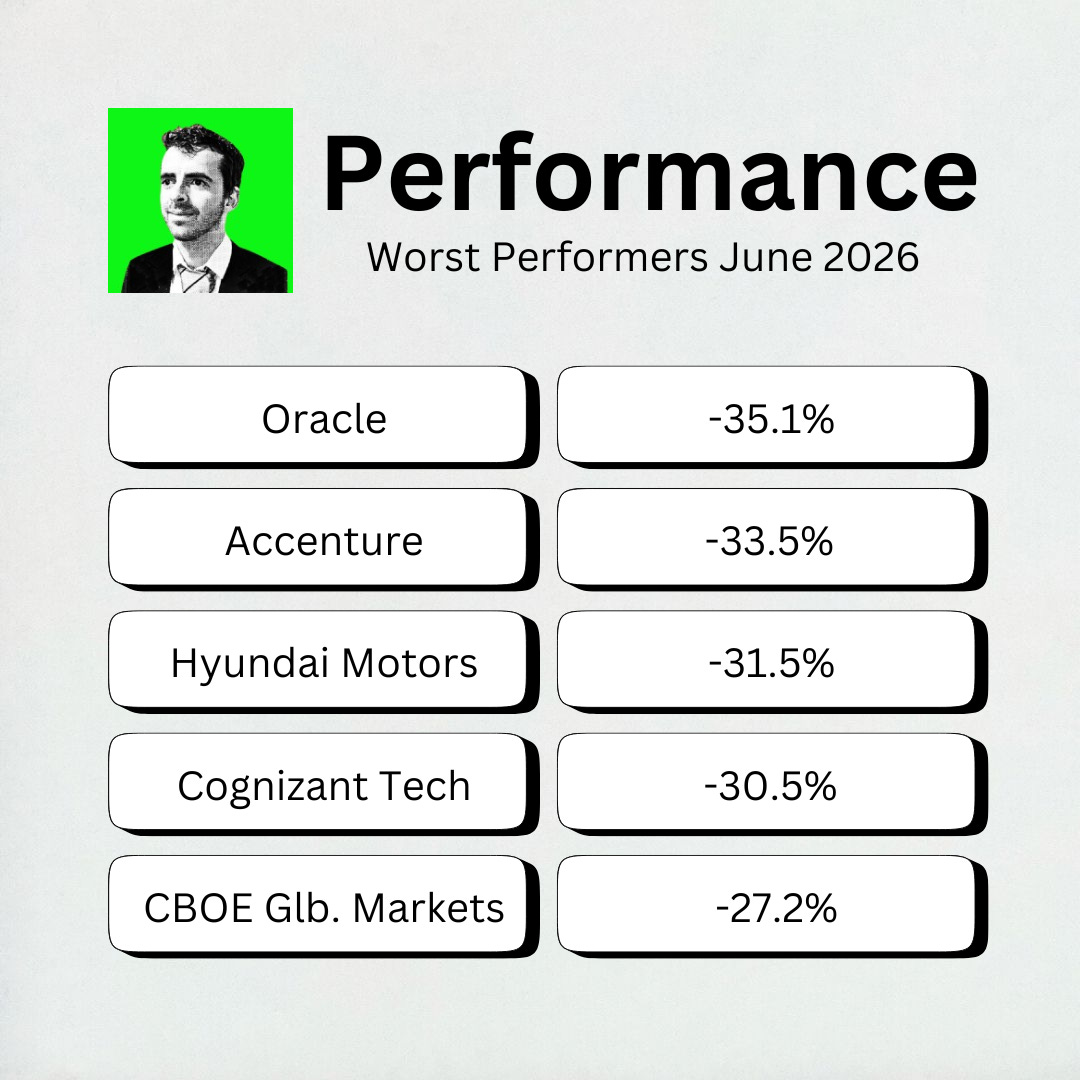

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

Worst performers

The cheaper we can buy great companies, the better.

The biggest decliner this month? Oracle, losing 35%.

Oracle provides enterprise software, cloud infrastructure, and database management systems.

It’s been seen as a beneficiary of the AI buildout, with the stock up 70% from April to the start of June.

But Oracle fell hard last month because of rising debt levels and continued spending.

Massive Spending: Management announced plans to raise another $40 billion through a mix of debt and equity to aggressively build out its AI cloud infrastructure

Debt Concerns: Oracle already has more than $130 billion in net debt, so investors are worried that the hyperscaler buildout will slow down before the debt is paid off

Dilution: Investors didn’t like the planned $20 billion equity issuance that will dilute existing shareholders

Best Performers

Newell Brands was this month’s best performer, increasing by 80%!

Newell Brands is a consumer goods company with a portfolio of well-known household brands, including Rubbermaid, Sharpie, Coleman, and Yankee Candle.

This month a combination of improving consumer demand, automation investments, and a guidance raise caused a short squeeze.

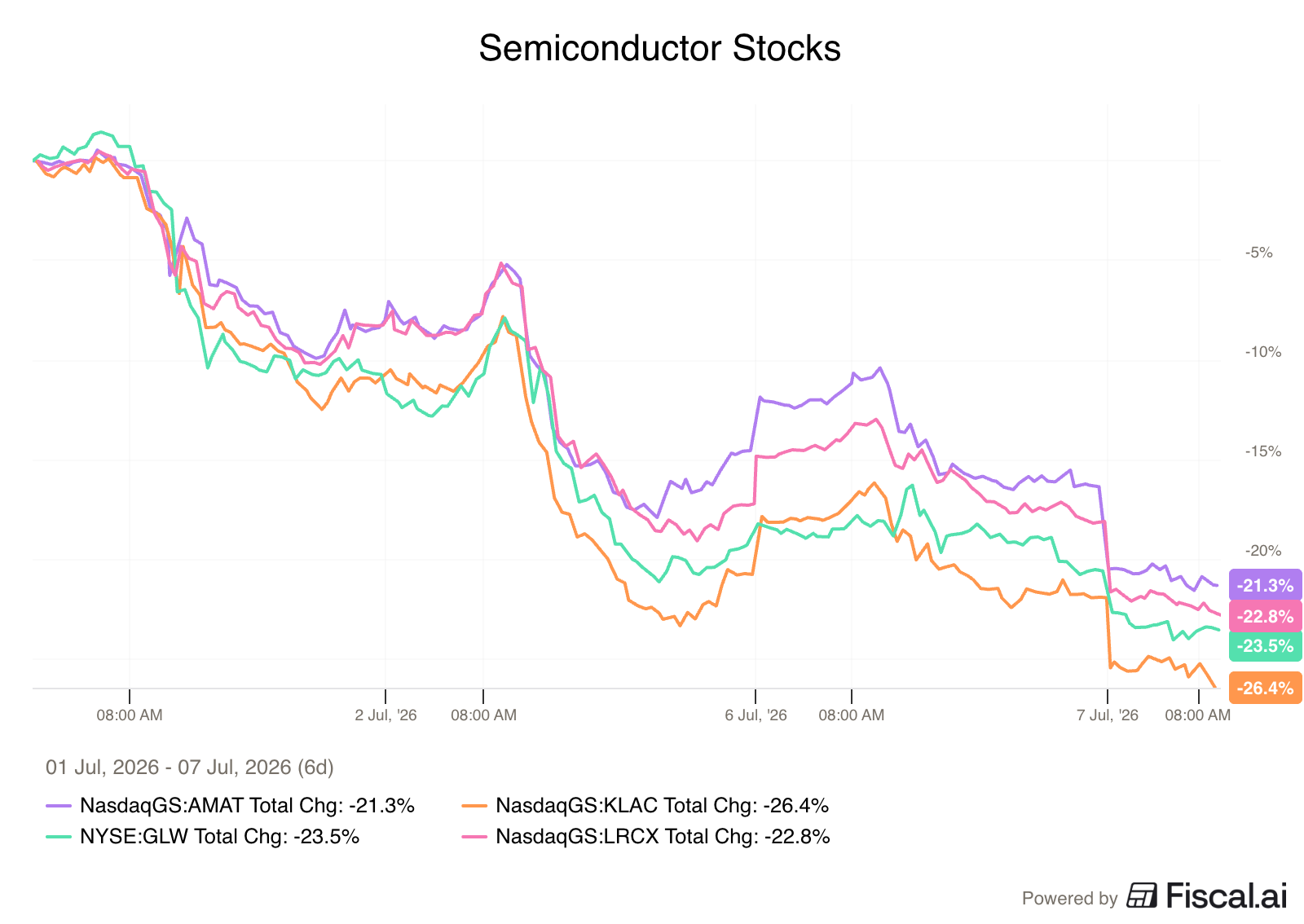

Semiconductors

Perhaps more interesting are the other 4 stocks on the list.

They’re all related to semiconductors, which are the new hot stocks in the AI hype.

Applied Materials (AMAT): Makes the machines that add microscopic layers of materials onto silicon wafers to build the chips.

Lam Research (LRCX): Makes the machines that carve out (etch) those layers to create the tiny circuits.

KLA Corporation (KLAC): Makes the inspection tools that check for defects to ensure the chips actually work.

Corning (GLW): Supplies the ultra-pure, specialized glass used for lenses and mirrors inside chip-making equipment.

So far after the big run up in June, all 4 have fallen at least 20%.

Spotlight: Cboe Global Markets ($CBOE)

Cboe Global Markets runs options exchanges across multiple asset classes.

It was trading as high as $366 per share in May, but has quickly dropped by 33%, putting it at the number 5 spot on our Worst Performers in June.

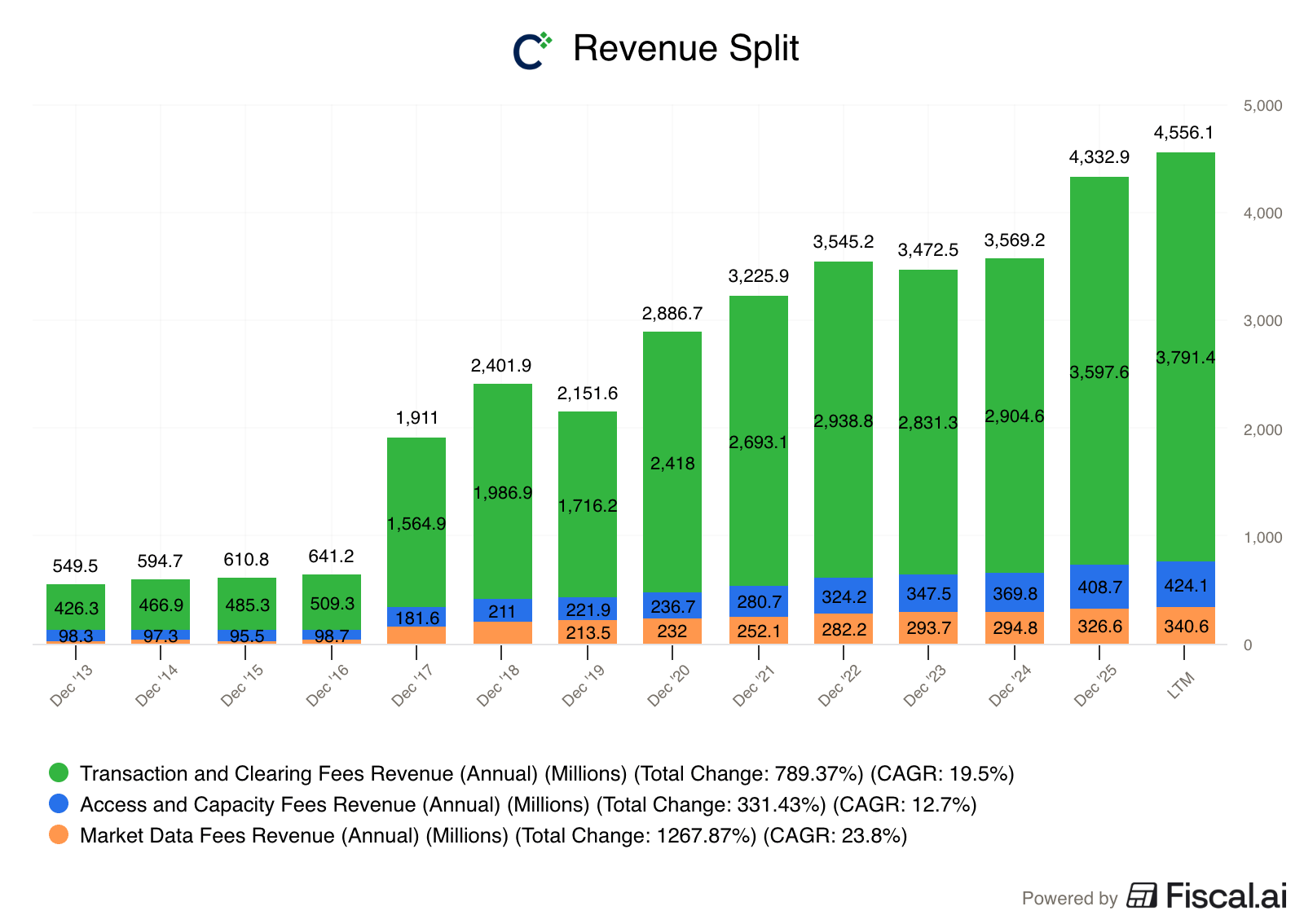

How Cboe Makes Money

Cboe makes money in three main ways:

Transaction Fees: Fees on every contract traded across its options, futures, equities, and FX platforms.

Proprietary Products: Holds exclusive rights to institutional hedging staples like S&P 500 Index (SPX) options and the Cboe Volatility Index (VIX)

Data & Access Fees: Recurring revenue from charging institutional firms for real-time market data feeds and low-latency system connectivity

Why Cboe deserves to be in the spotlight:

Strong Network Effects: Institutional traders need liquid markets. They’ll go where the most trading is already happening. For a lot of products, that’s Cboe. This self-reinforcing loop makes it difficult for competitors to steal volume from its core index products, keeping operating margins high.

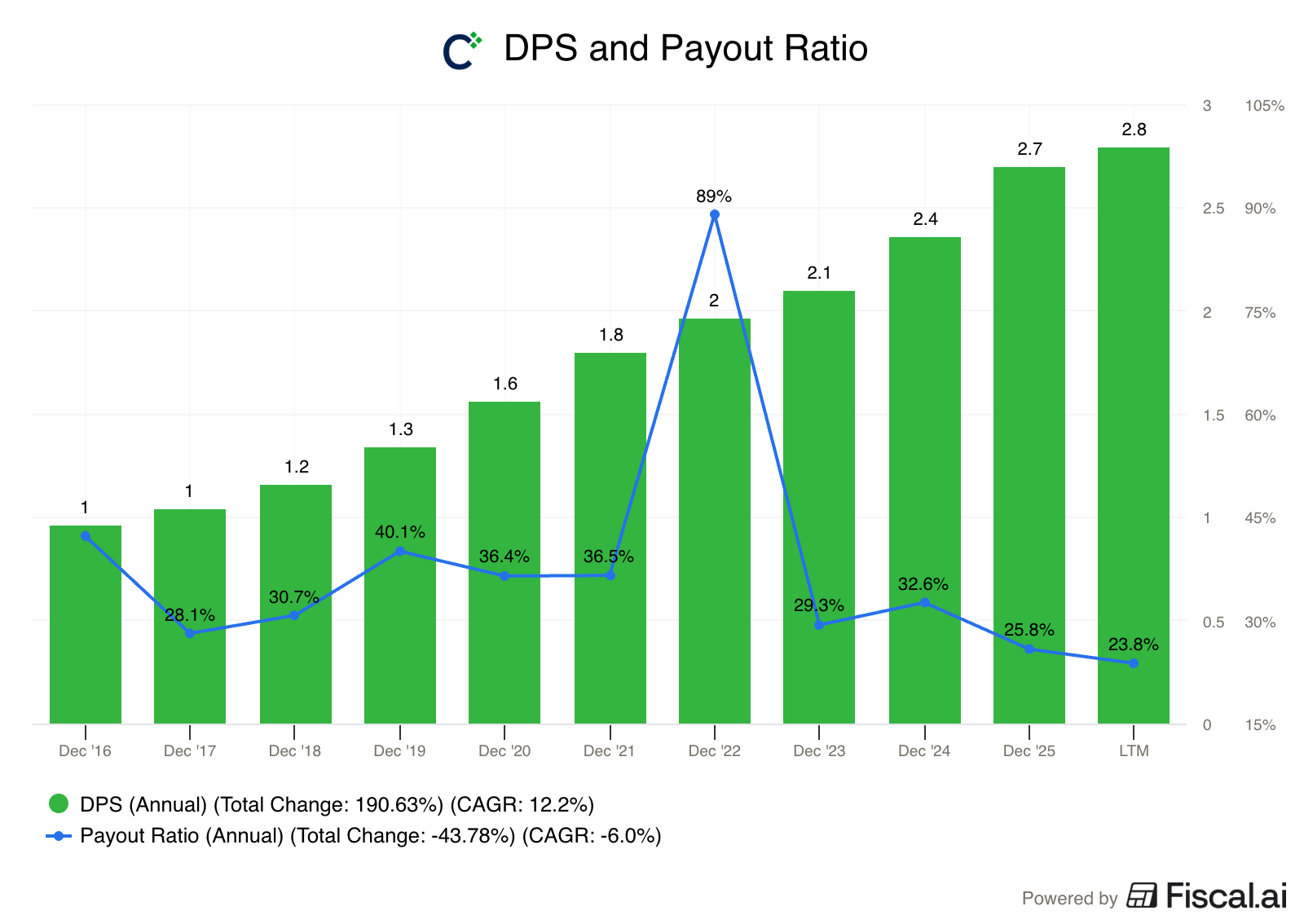

Strong Dividend Growth: Cboe has gown its dividend by 12% per year over the past decade, and generally maintains a low payout ratio.

An Interesting Portfolio Hedge: When markets drop, most stocks drop right along with them. Cboe sees higher trading volumes and higher fee income during times of more volatility.

Why the stock got knocked down

The recent drawdown was triggered by two main issues.

Crypto Perpetual Futures Approval: The CFTC approved crypto perpetual futures trading on Kalshi at the end of May. Investors are nervous that these could expand beyond crypto and structurally threaten or erode Cboe’s monopoly over traditional proprietary options and futures.

Declining Revenue Per Contract (RPC): Cboe logged record-breaking volumes in June (averaging 23 million contracts per day), but its preliminary Q2 guidance showed more activity in lower-margin, multi-listed options, which diluted total options RPC down to $0.317 (from $0.343 in March) causing investors to be concerned that this number will keep declining.

The Bottom Line

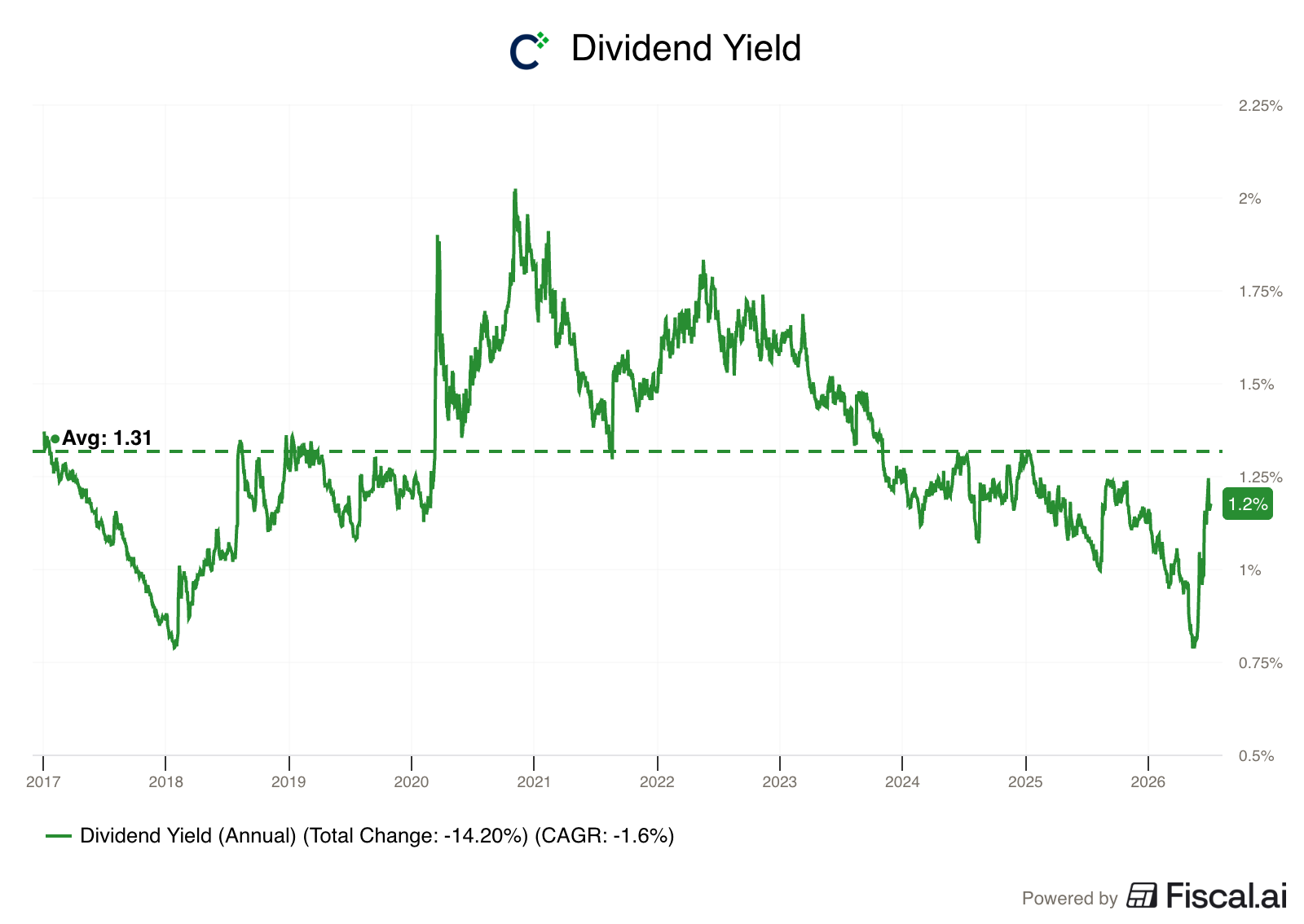

Cboe is a high quality business that’s starting to look more reasonably valued again.

The dividend yield is heading back up to the long term average after more than a year below it.

Uncertainty may keep pushing the price down, making Cboe a stock that dividend growth investors might want to keep their eye on.

July Best Buys

I scanned our Buy-Hold-Sell List for great quality compounders and dependable dividend payers trading at attractive discounts.

Let’s dive into 5 of our favorite income ideas for this month!

5. Sage Group ($SGE.L)

How does Sage make money? Sage Group provides back-office software (like accounting, payroll, and human resources) for small and medium-sized businesses globally.

Sage has very high switching costs. Once a business integrates its accounting software and builds workflows around it, switching providers becomes a nightmare. It carries massive risks of data corruption and operational downtime.

The cost for Sage’s software and services is also a very small portion of a business’s total revenue.

That means it’s not worth the risks that come with switching just to save a few pennies if the product works.

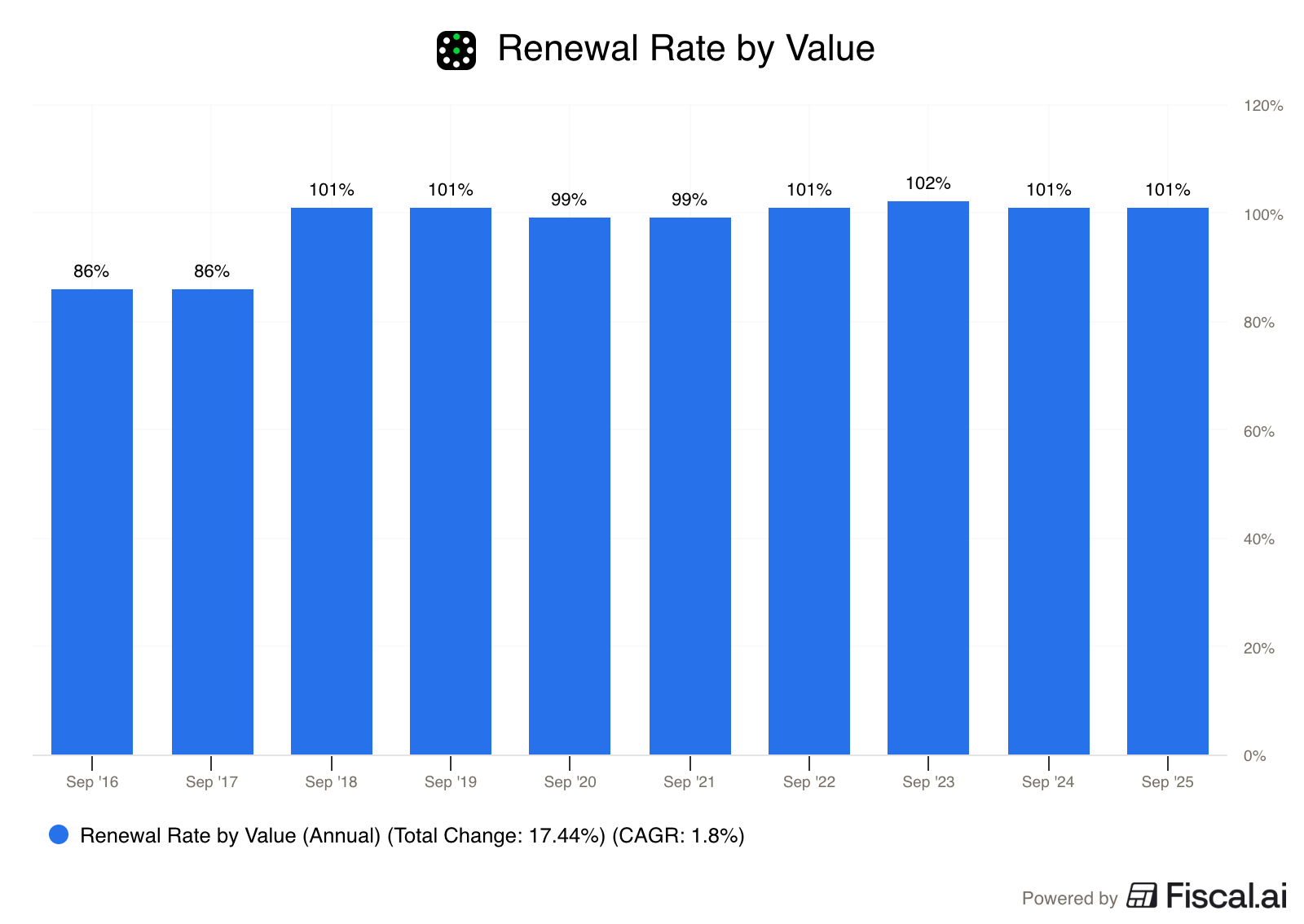

You can see this in the very high Renewal Rate by Value.

This measures renewal by existing customers only, and shows that they tend to spend more with Sage as time goes on.

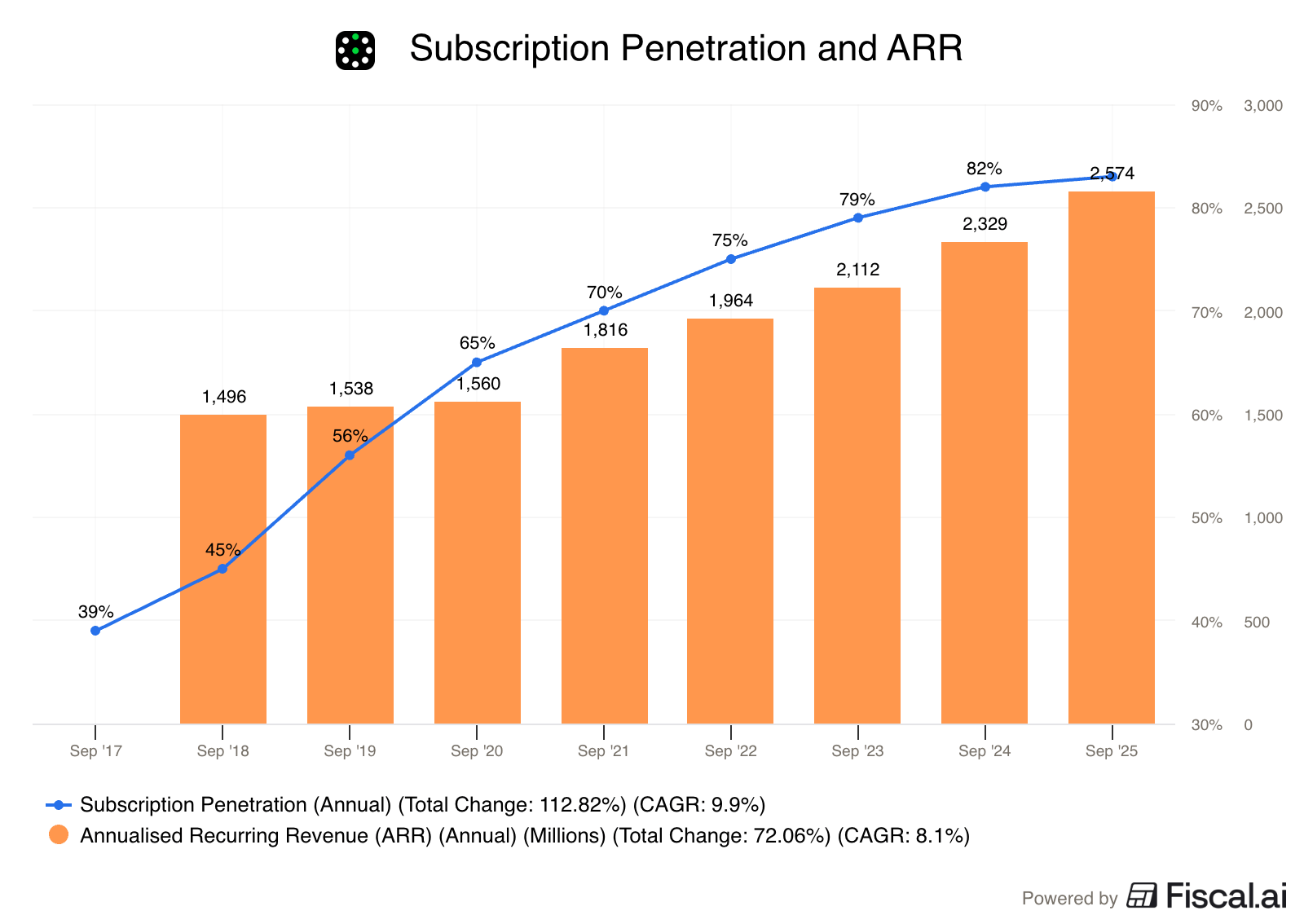

The company has successfully shifted to a subscription-based cloud SaaS model.

The vast majority of their revenue now comes from subscriptions, and their Annual Recurring Revenue grows every year.

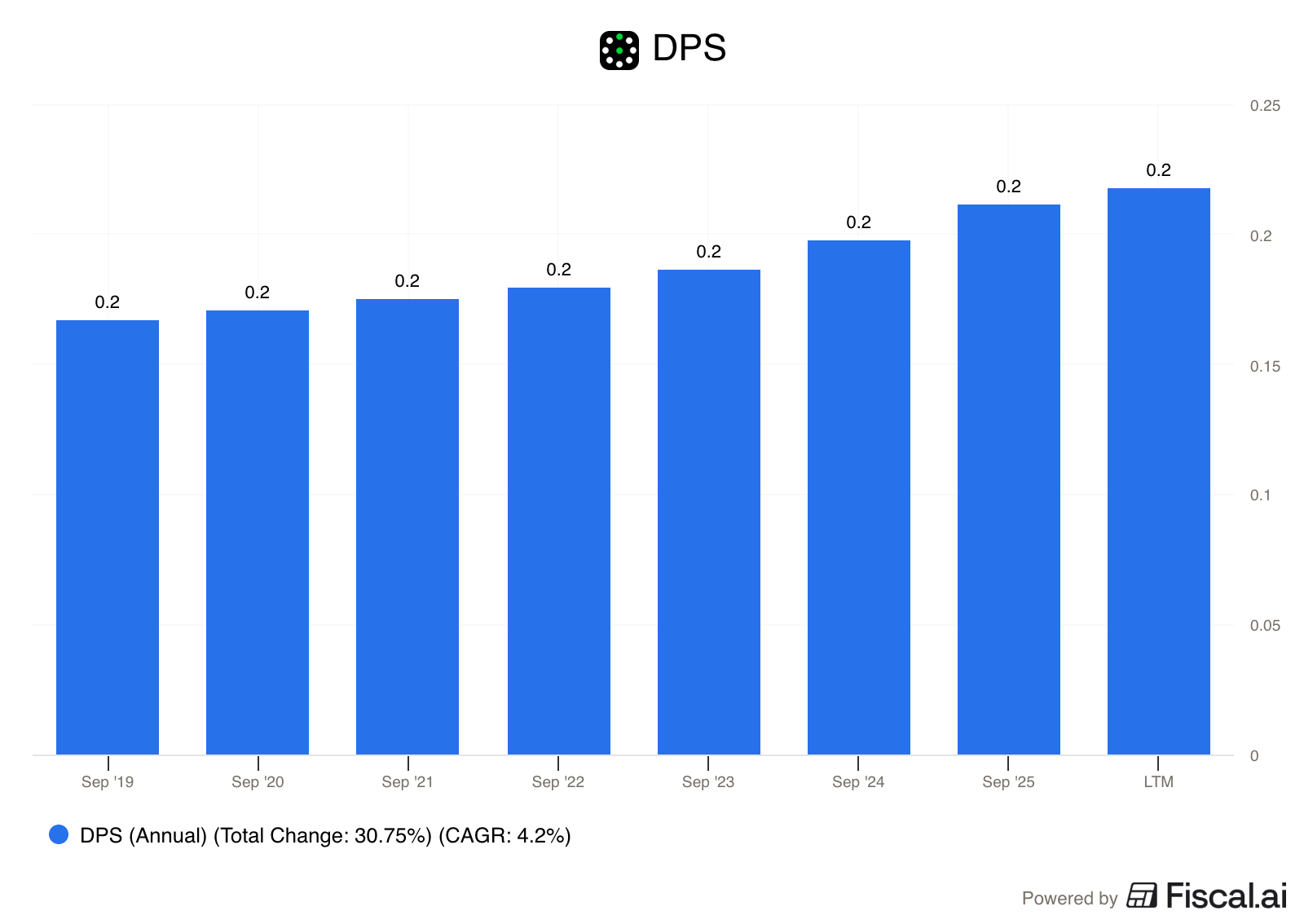

That stability and recurring revenue has allowed Sage Group to become a reliable, slow dividend grower.

4. SBA Communications ($SBAC)

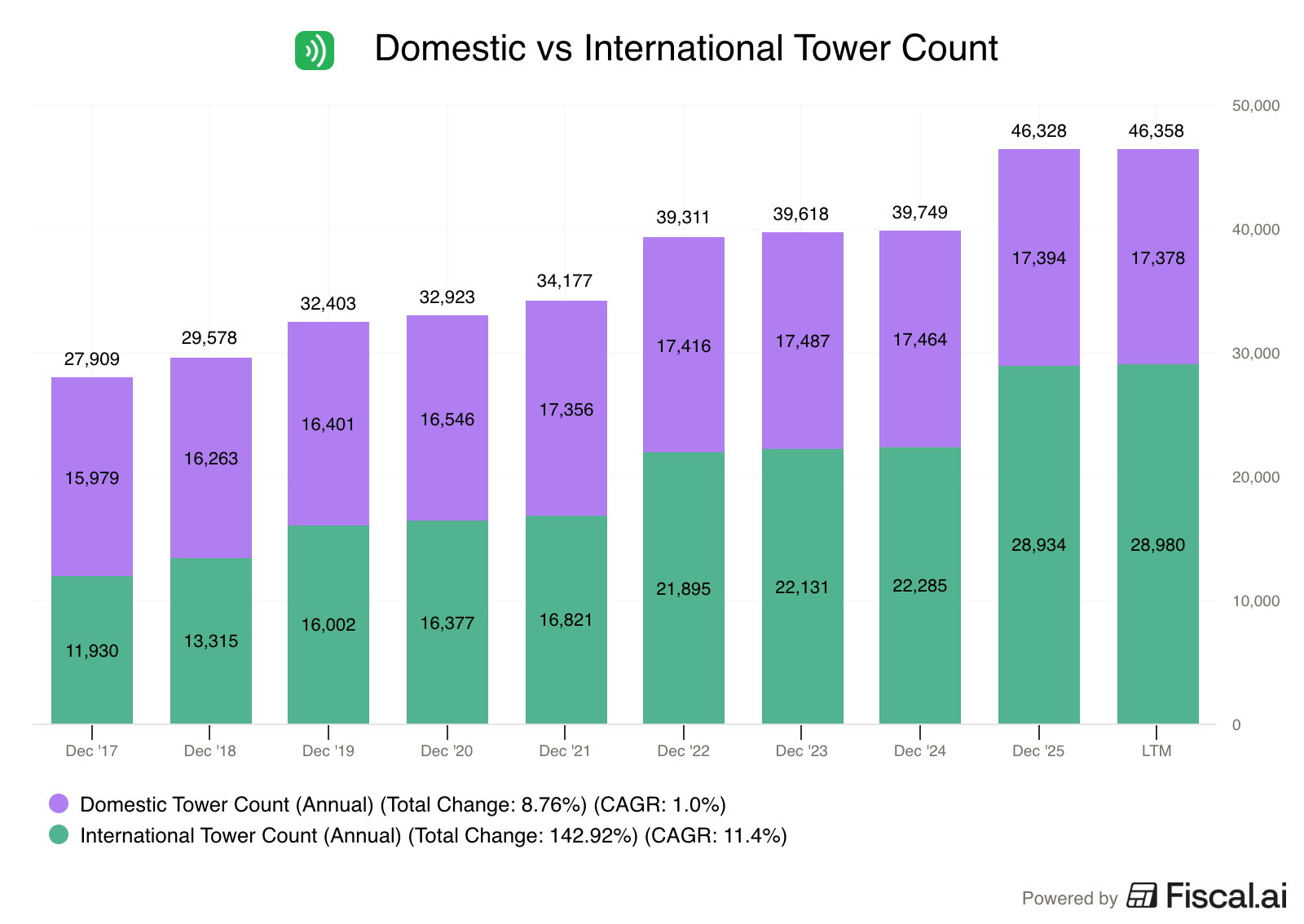

How does SBA make money? SBA operates as a real estate investment trust (REIT) that owns a massive portfolio of roughly 46,000 wireless cell towers across North America, South America, and Africa. They lease antenna space out to top mobile carriers like T-Mobile, Verizon, and AT&T.

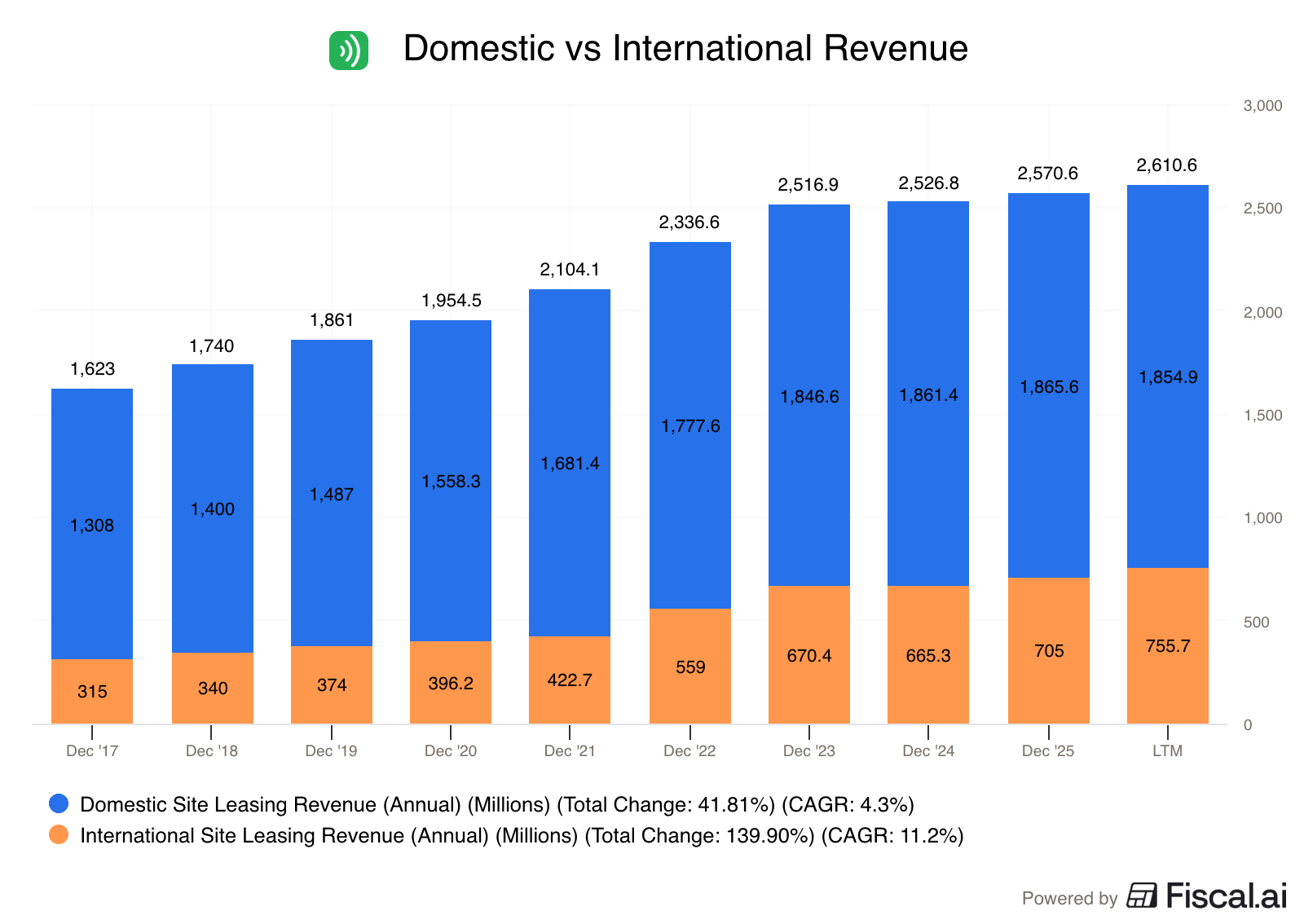

The majority of SBA’s leasing revenue comes from North America.

That’s despite SBA having more towers internationally.

The U.S. business is more profitable and more stable, but the international business has more potential for growth.

Both businesses have strong moats.

Moving equipment off of SBA’s towers risks network disruptions and dropped calls for the wireless carriers that lease them.

It’s also expensive and difficult to move wireless equipment from one tower to another.

That means that wireless companies leave their equipment right where it is.

Another great thing?

Operating leverage.

The cost to run a cell tower is almost entirely fixed.

Once it’s built, adding a second or third carrier costs SBA virtually nothing, so that new lease revenue is nearly all profit.

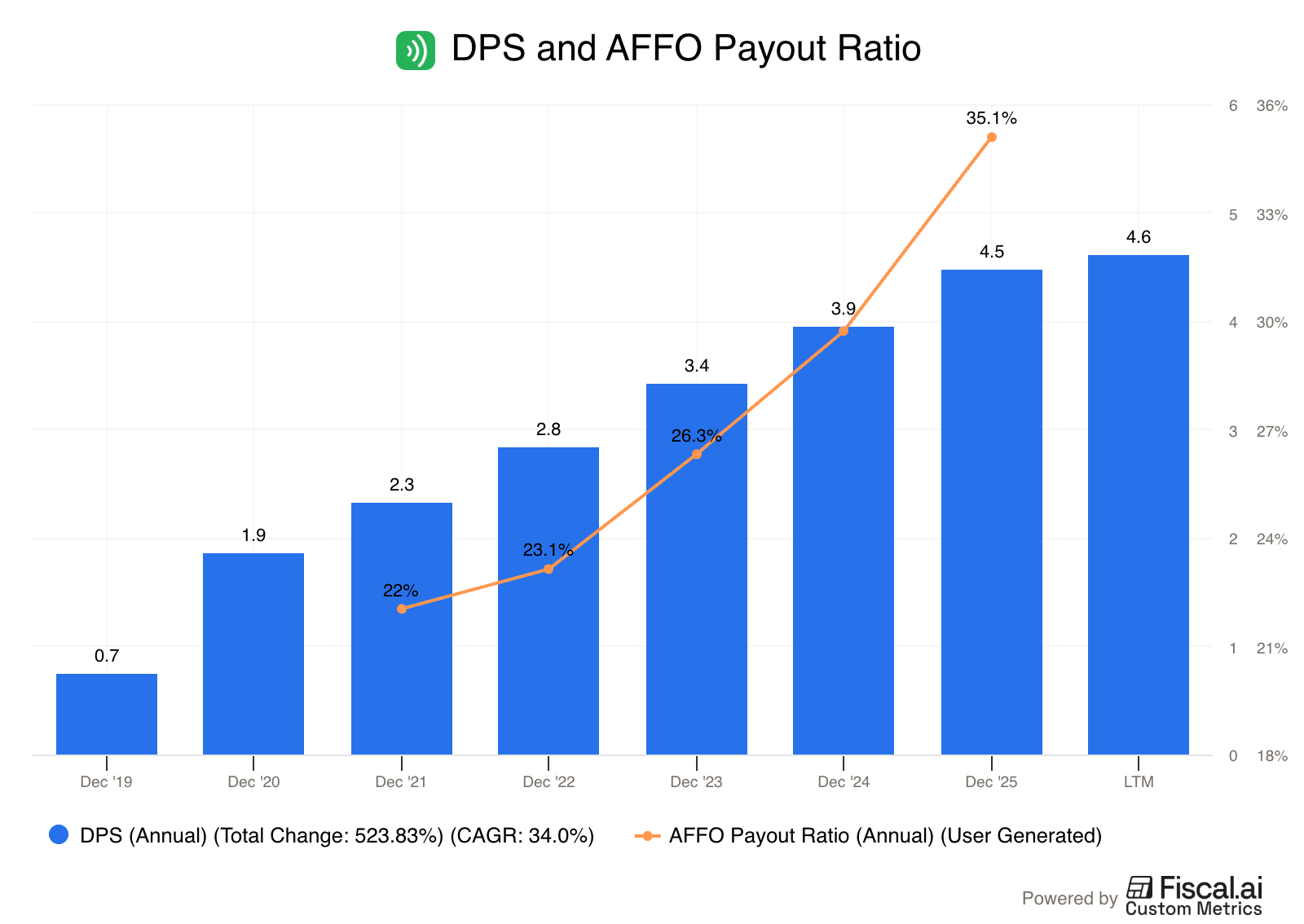

That’s how SBA has been able to grow its dividend by more than 30% (!) per year, while keeping a conservative AFFO Payout Ratio.

Want to see the top 3 Best Buys?

Our #3 pick is a retailer with a 40-million-member loyalty program, protection from e-commerce competition, and the stock recently dipped by more than 50%.

Our #2 pick is a healthcare duopoly that looks to be on sale.

Our #1 pick is a software provider with virtually impenetrable switching costs, and rising revenue.

Upgrade your subscription to read the full analysis on our top 3 Best Buys for July, and get full access to the complete every single month!

Upgrade your subscription here 👇

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.