Best Buys June 2026

Something special is happening on June 23rd that you won’t want to miss.

If you want behind-the-scenes updates and early access to our upcoming high-yield reports, join the High-Yield VIP List, and you’ll get the following immediately when you join for free:

My high-yield stock watchlist

A Checklist of Dividend Investing Mistakes

The Highest Yielding Dividend Aristocrats

Get on the list by leaving your email here.

A new month, a new Best Buys List.

Each month, I’ll give an overview of my favorite stocks of the month.

Let’s dive into this update and show you some of my favorite stocks.

May 2026

The S&P 500 rose +4.97% in May.

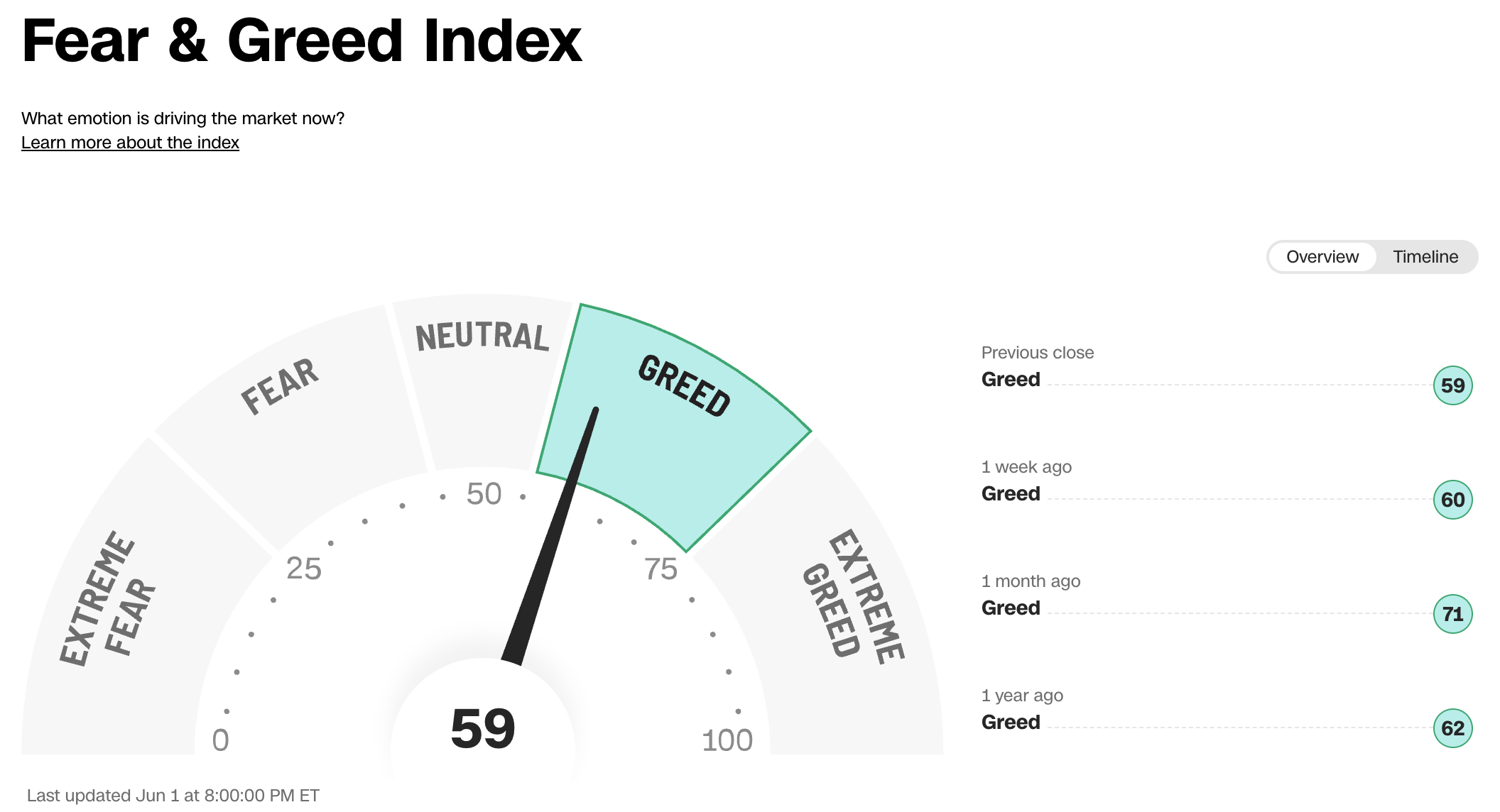

Investors are greedy today according to the Fear & Greed Index:

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

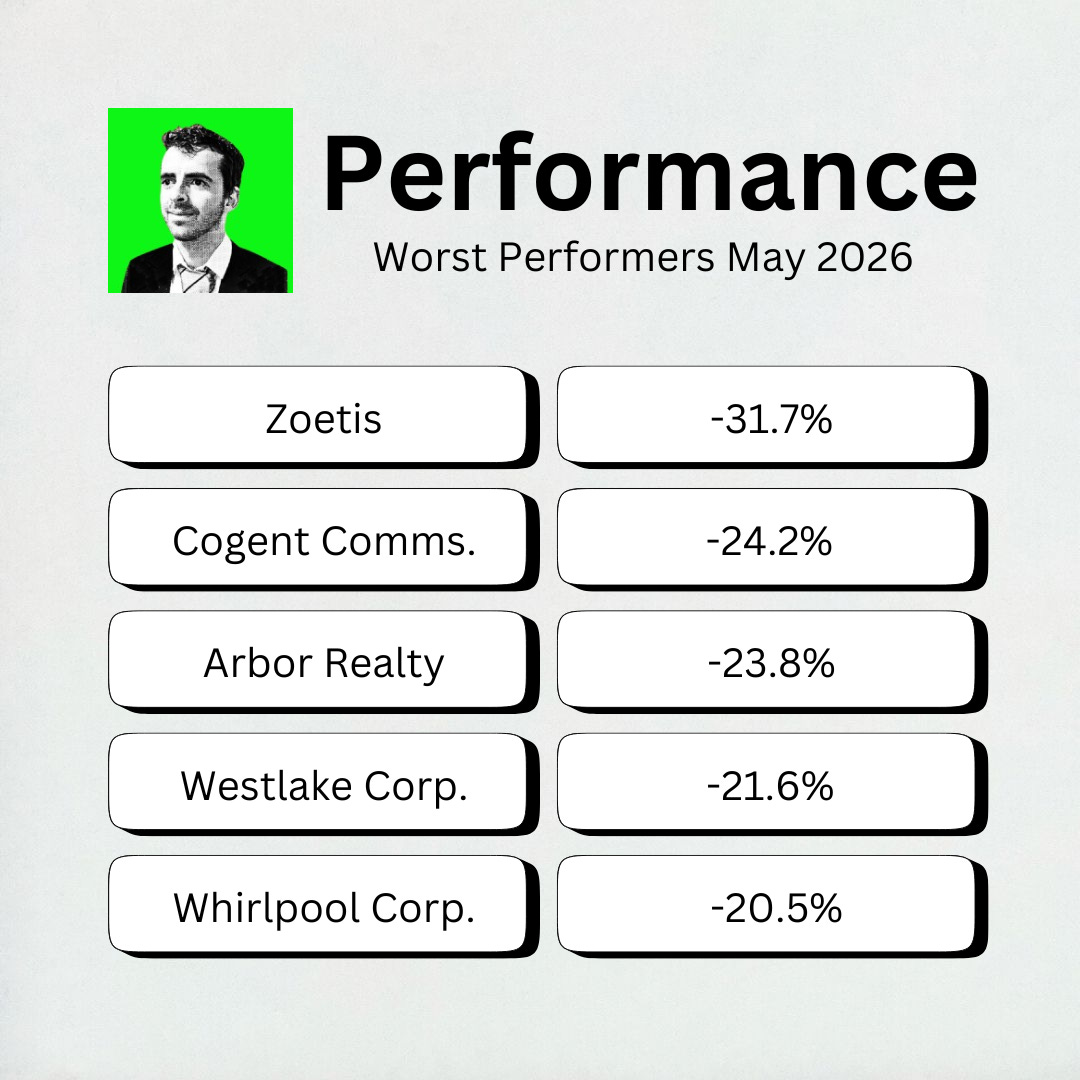

Worst performers

The cheaper we can buy great companies, the better.

The biggest decliner this month? Zoetis, losing 32%.

Zoetis is a leading animal health company that develops and provides medicines, vaccines, and diagnostic products for pets and livestock.

Zoetis fell this month due to weakening pet care demand and intensified competition:

U.S. Companion Animal Weakness: The company reported an 11% decline in U.S. companion-animal sales during the first quarter

Earnings Miss and Guidance Cut: The company earned $1.53 per share, missing the $1.61 analysts had expected, and management lowered 2026 guidance

Intensifying Competition: Competitors have introduced new drugs in Zoetis’ categories and are using aggressive pricing and incentives

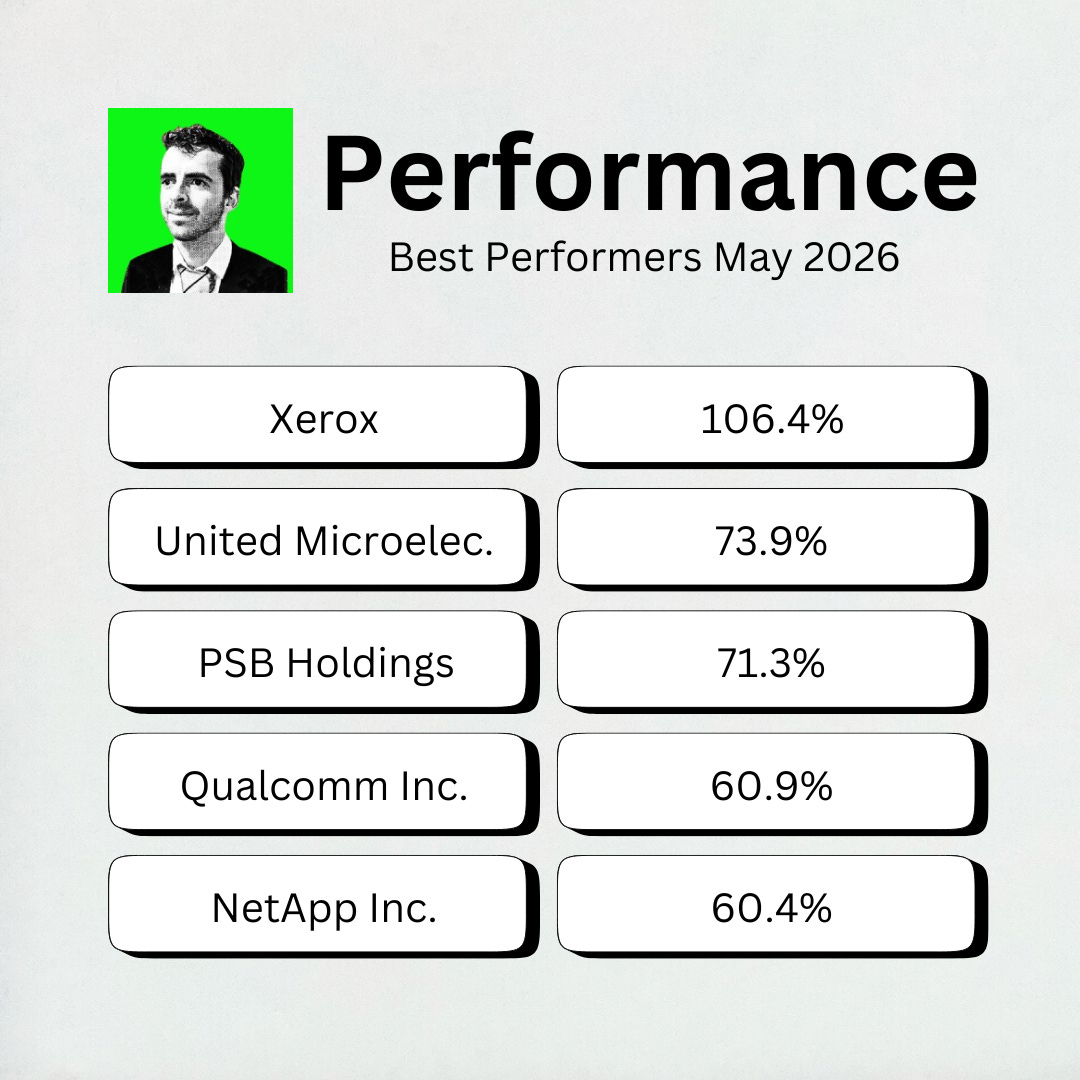

Best Performers

Xerox Holdings was this month’s best performer, more than doubling!

f you want proof that AI hype is driving the market, look no further than this month’s best performers.

Three of our top five gainers shot up for AI-related reasons.

Qualcomm: Known for smartphone chips, Qualcomm shifted its narrative overnight by securing a major hyperscaler customer for its custom data center processors

NetApp ($NTAP): NetApp had record revenue in its flash storage and cloud segments due to customers trying to clean up and organize unstructured data for AI training

United Microelectronics Corp. ($UMC): Had strong monthly sales and progress on its joint 12nm chip program with Intel

But not winner was fueled by artificial intelligence.

Xerox ($XRX) grew revenue by 27% after integrating its Lexmark acquisition.

Michael Burry summed up what happened here well: “My strategy isn’t very complex. I try to buy shares of unpopular companies when they look like road kill, and sell them when they’ve been polished up a bit”.

Expectations for Xerox went from absolute roadkill to “not so bad,” shooting the stock price up very quickly.

Finally, PSB Holdings went up because it is getting acquired by Bank First.

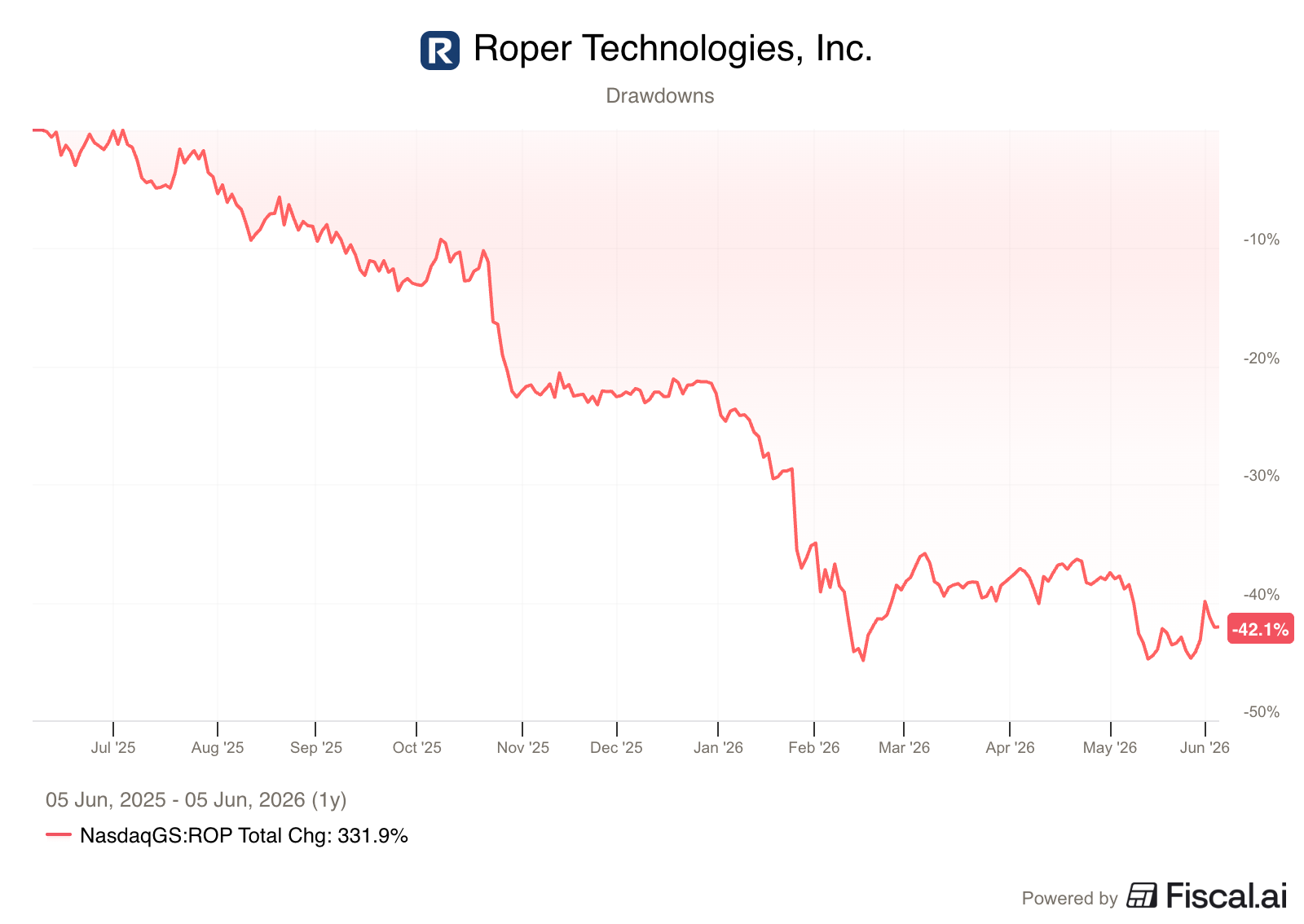

Spotlight: Roper Technologies ($ROP)

Roper Technologies is a Dividend Aristocrat that has historically been valued at a premium by the market.

But the company got sold off in the ‘Saaspocalypse’.

How does Roper make money?

Roper acquires, develops, and manages technology and software businesses.

They operate a decentralized model, allowing each company to run independently, but all excess free cash flow goes back to the parent company to fund more acquisitions.

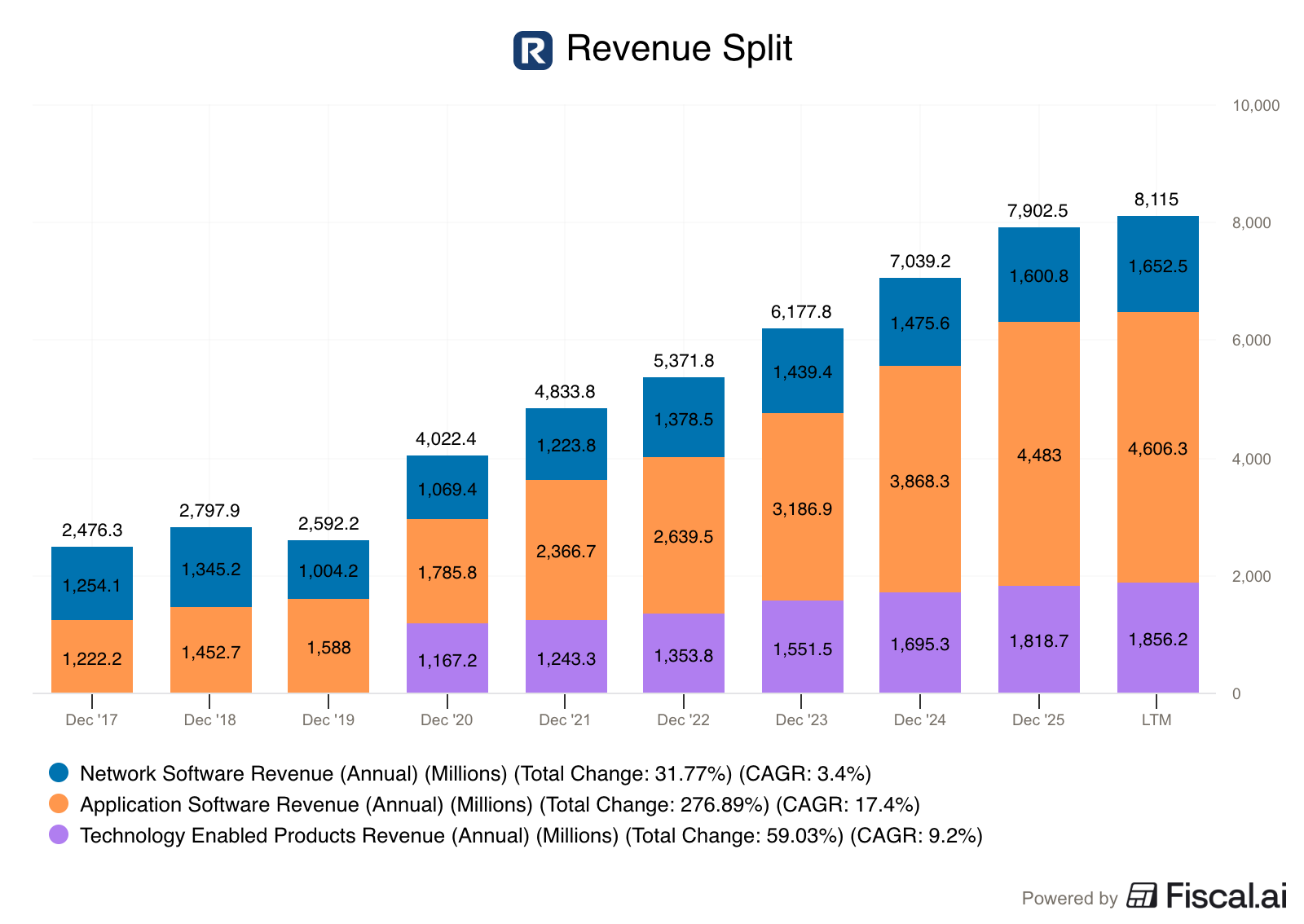

Roper splits their business into three segments:

Application Software: This includes critical, niche platforms like Deltek (government contracting software) and Aderant (legal software) and makes up more than 50% of Roper’s total revenue

Network Software: This segment includes industry-standard marketplace platforms, like DAT Freight & Analytics. DAT matches truckload carriers with brokers and shippers in North America.

Technology-Enabled Products: This division focuses on specialized hardware-software solutions, like Verathon’s medical visualization systems.

Why does it deserve to be in the spotlight?

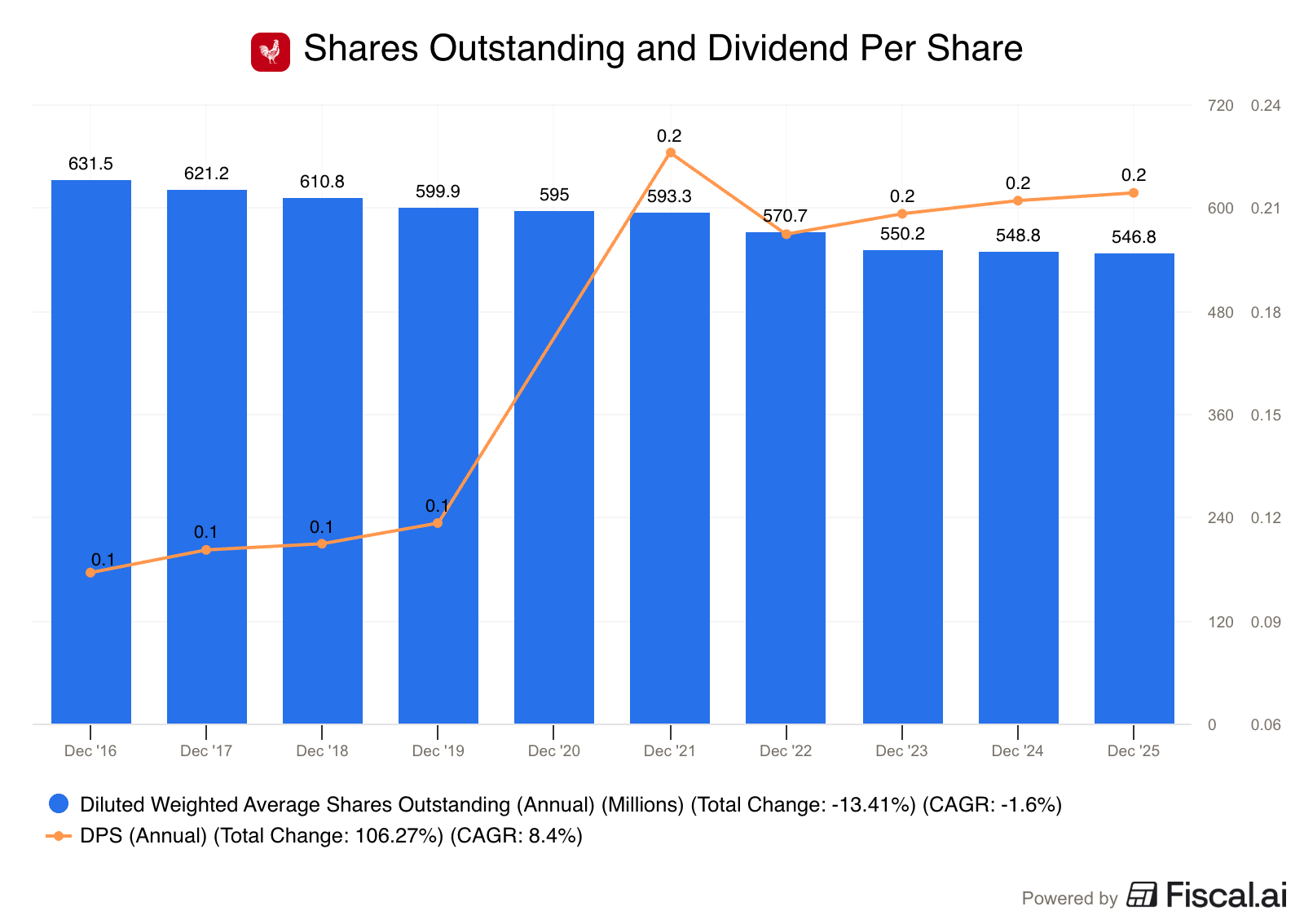

$1.5 Billion in Q1 Repurchases

Roper typically uses excess cash to acquire new businesses.

However, management is incredibly disciplined.

Private market software companies haven’t seen their values collapse the same way public ones have.

At the same time, management views shares of Roper as extremely cheap, so they changed their capital allocation strategy.

Roper spent $1.5 billion on buybacks in Q1 and the board authorized another $3 billion.

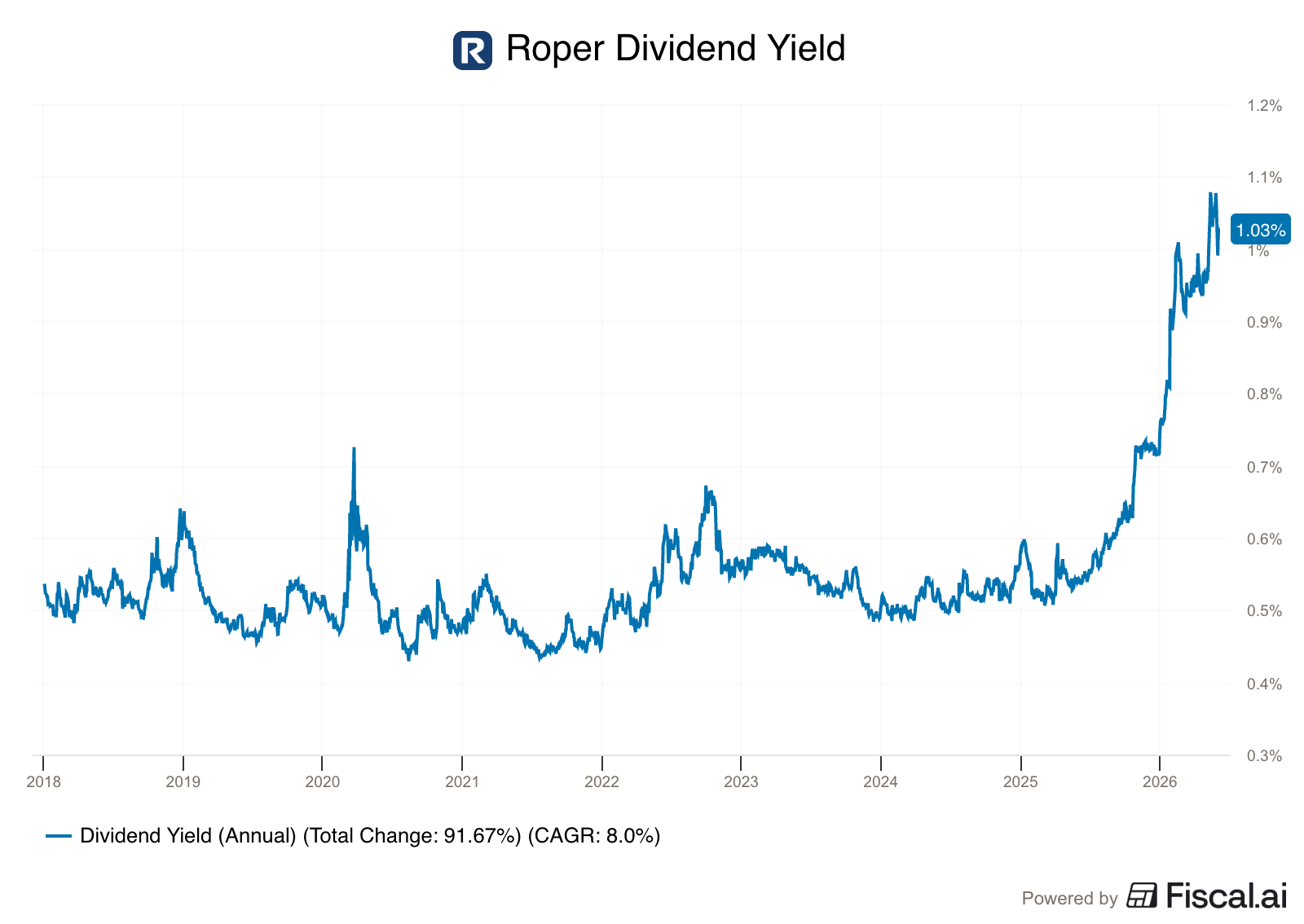

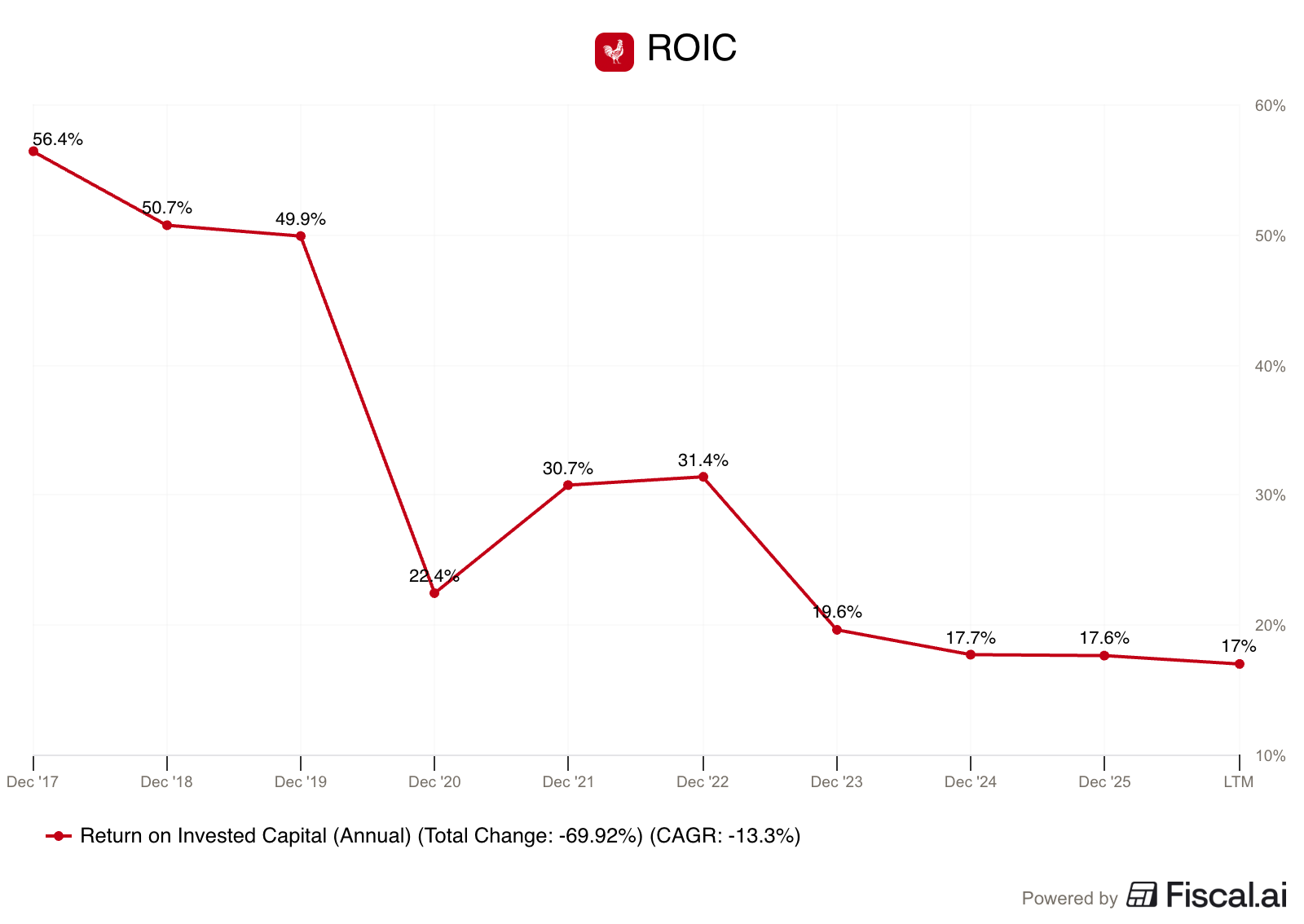

Low Valuation

Between the ‘Saaspocalypse’ and a slowdown at Deltek, Roper is now trading at a much higher dividend than normal (indicating a correspondingly low valuation).

Will AI kill Roper?

The market is afraid that AI will allow clients to build solutions in-house or erode software pricing power.

I think this idea completely misses the structural advantages of Roper’s businesses:

Switching Costs: Roper’s systems handle complex, highly regulated workflows. The operational risk, retraining costs, and disruption required to rip out a system is huge.

Network Effects: Platforms like DAT Freight & Analytics get better as they grow. Shippers go where the carriers are, and carriers go where the shippers are. AI can generate code, but it can’t recreate a marketplace.

AI Integration: Roper is already successfully monetizing AI. Management said that “AI-influenced” features were responsible for 75% of all new business at Central Reach.

The Bottom Line

The market has cut Roper’s stock nearly in half.

Management is telling us very clearly that they think it’s cheap by stopping acquisitions and buying back 5% of the company.

For long-term investors looking for quality at an attractive price, Roper is worth a look.

June Best Buys

I scanned our Buy-Hold-Sell List for great quality compounders and dependable dividend payers trading at attractive discounts.

Let’s dive into 5 of our favorite income ideas for this month!

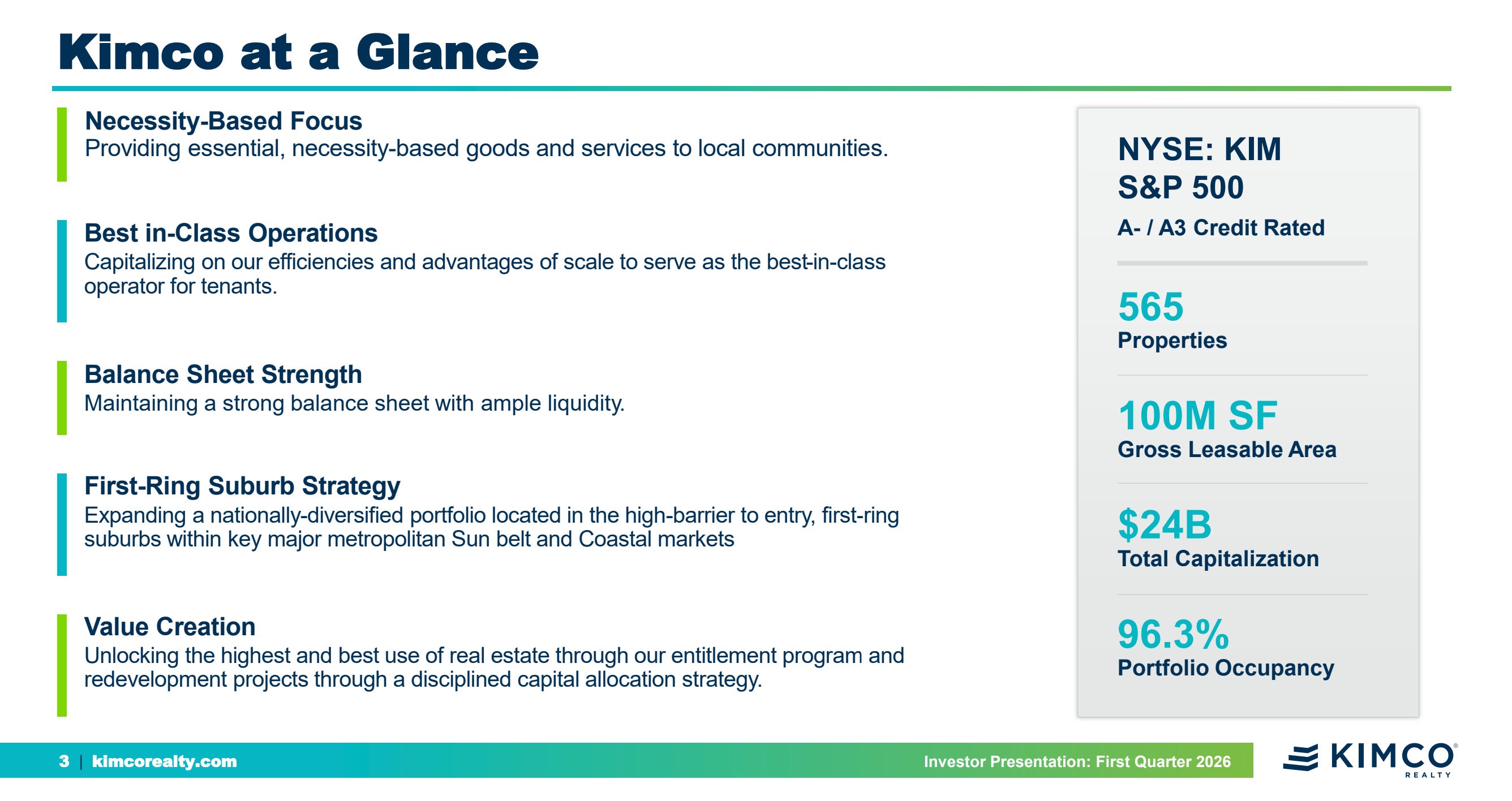

5. Kimco Realty ($KIM)

How does Kimco make money?

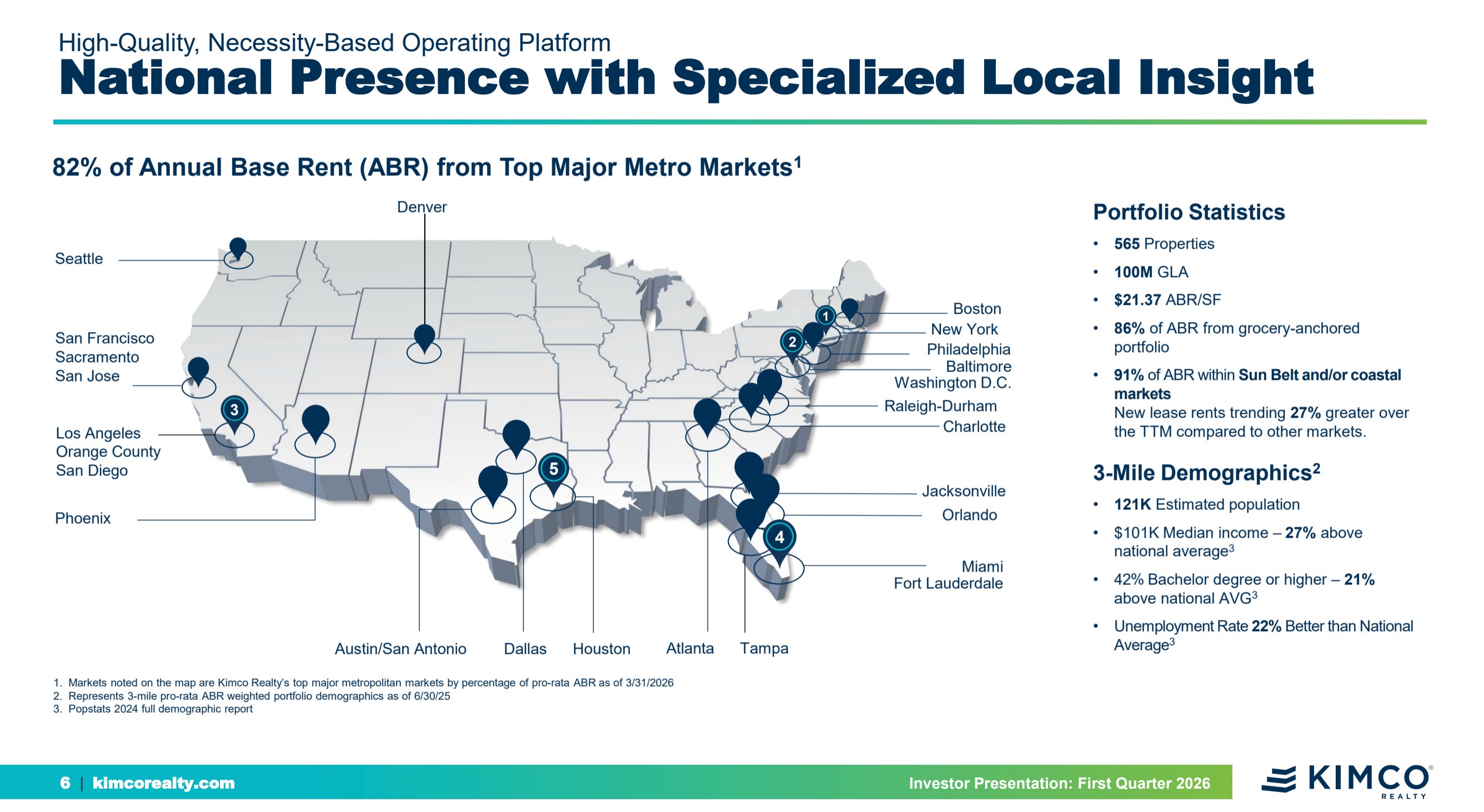

Kimco is a retail REIT and the largest operator of open-air, shopping centers in the United States, managing a portfolio of 565 properties.

80%+ of Kimco’s rent comes from major metropolitan sunbelt and coastal growth markets.

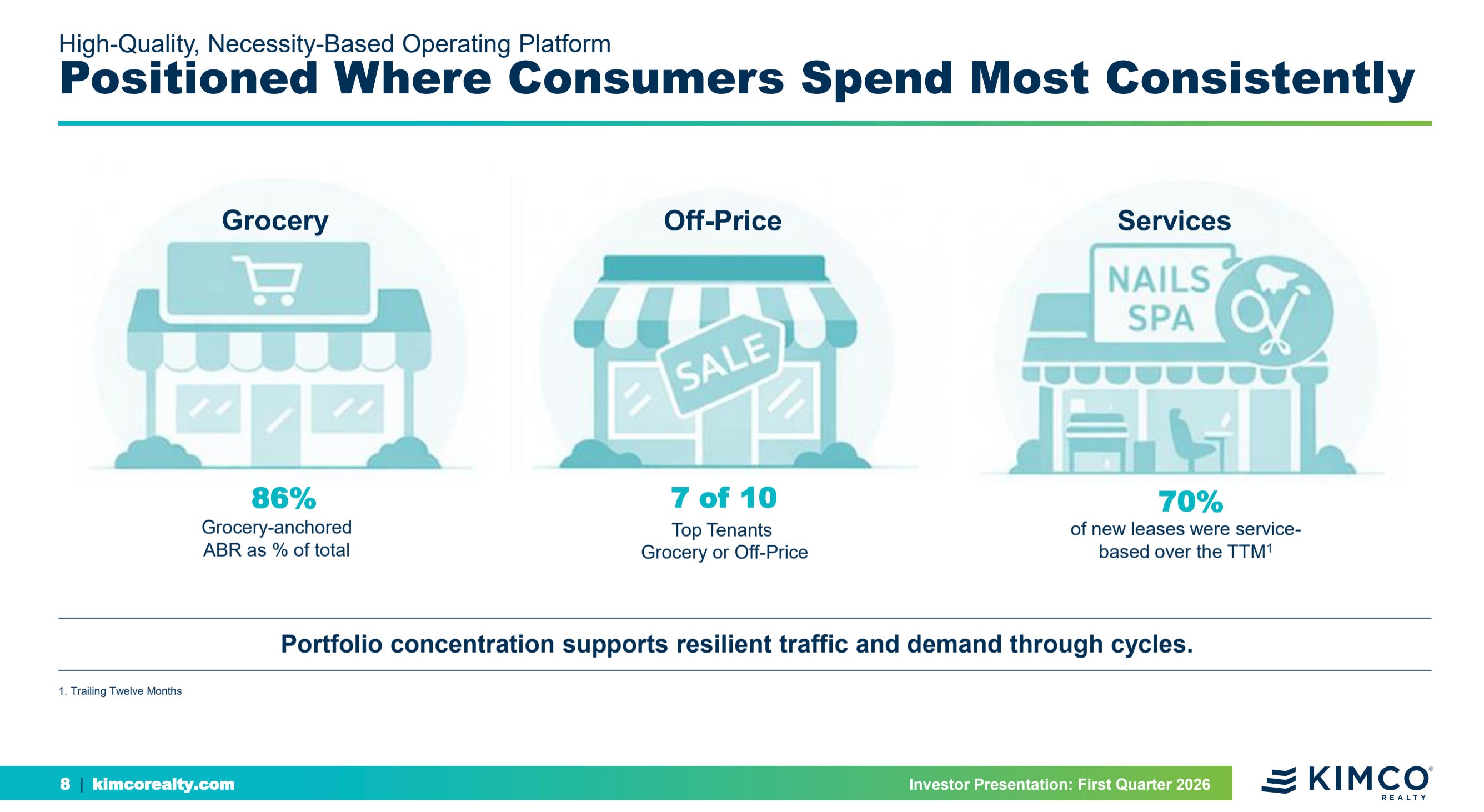

Most of Kimco’s shopping centers are anchored by grocery stores, which creates consistent traffic, and repeat spending.

REITs have been trading at low valuations recently because of high interest rats.

But Kimco’s business is doing just fine.

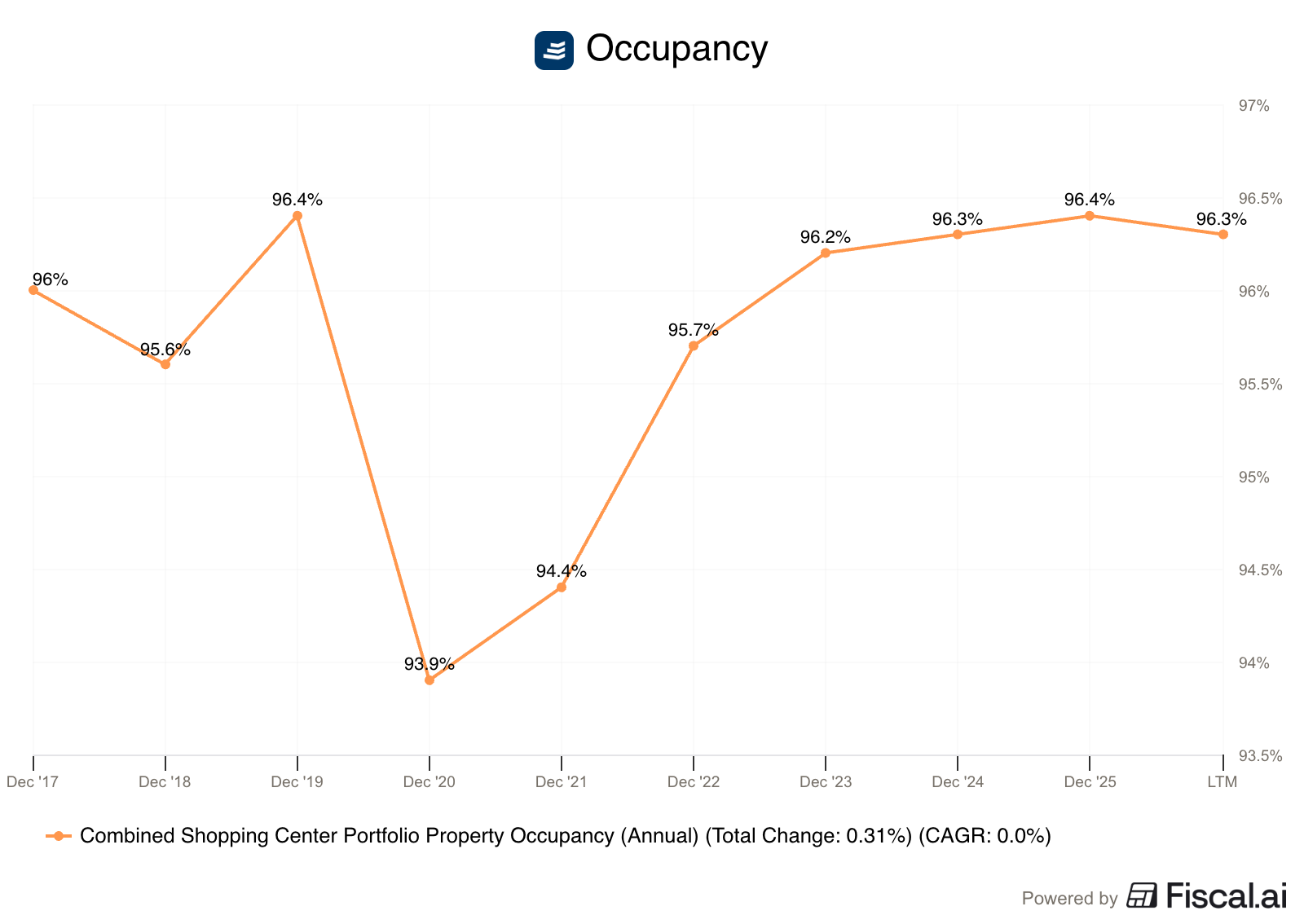

The occupancy rate is over 96%.

High-quality retail real estate is in short supply, giving Kimco pricing power.

Renewing tenants had their rent increased but 12% on average in the first quarter.

And brand-new tenants signed leases with rents 23.8% higher than what the old tenant was paying.

4. Howden’s Joinery ($HWDN.L)

How does Howden’s make money?

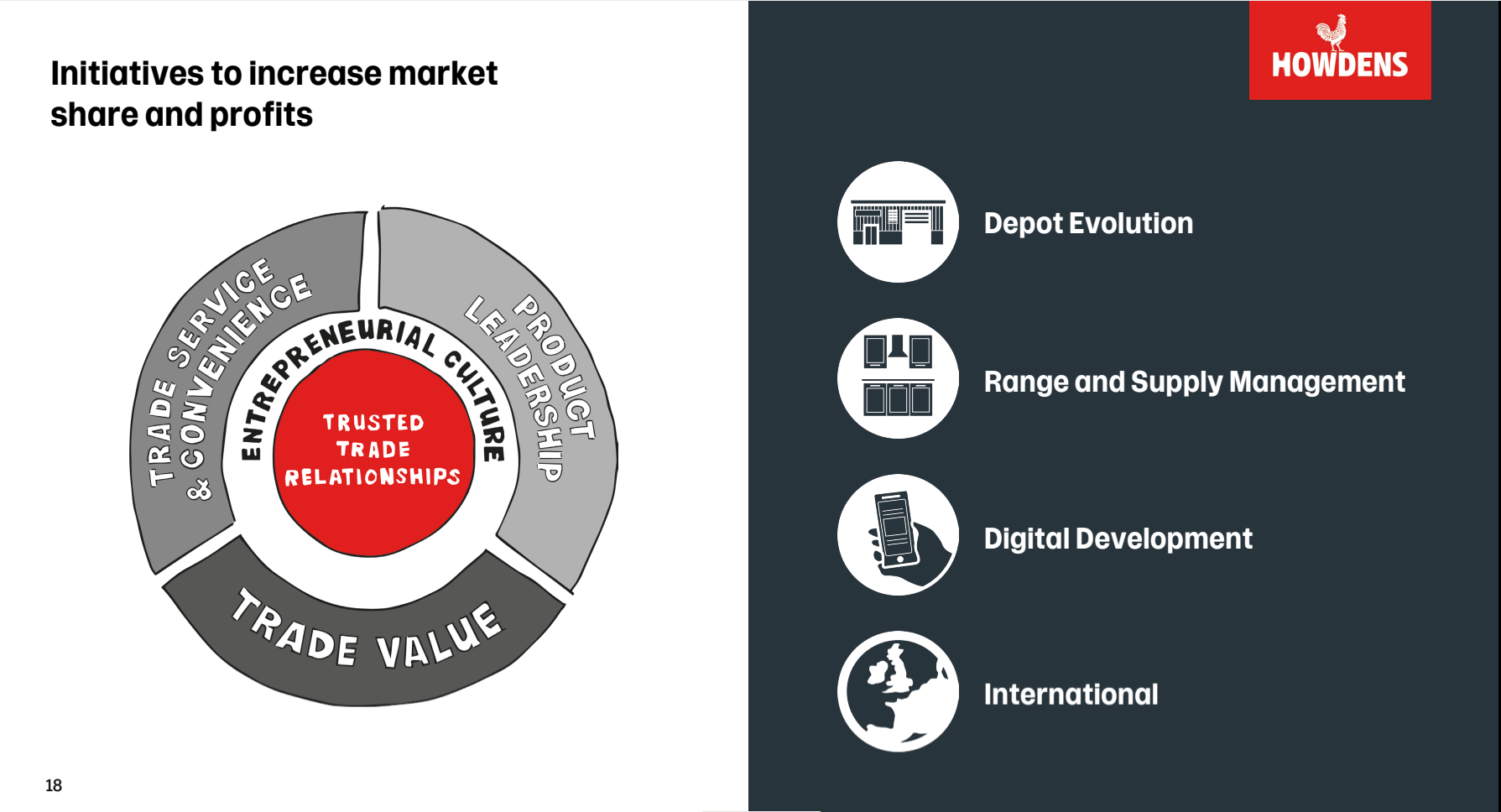

Howden’s Joinery is the dominant supplier of kitchen products like cabinets, sinks, and countertops in the UK market.

Unlike traditional retailers that try to attract fickle retail consumers, Howden’s has a rigid rule: they only sell directly to trade professionals (builders, contractors, and local carpenters).

This is a much better business model.

For a local builder, time is money.

Every project delay because a cabinet door, hinge, or other part is missing hurts their profitability.

Howden’s local depots maintain massive, 100% in-stock inventory availability.

That means builders go to Howden’s first, and trust them to have what they need.

That gives Howden’s a local moat, the majority of the local market share, strong pricing power, and an ability to reinvest in the business at a high Return On Invested Capital.

Howden’s is a very profitable business, so they can’t reinvest all of their excess cash into the business.

Management uses the excess to both buy back shares and pay a rising dividend to shareholders.

Right now, you can collect a 2.8% dividend yield with a conservative 43% payout ratio, leaving the business lots of cash to keep building new depots.

You’ve just seen two of my favorite income stocks for June, but paid Partners get three more.

Our top three picks for June include the leader in a global medical device duopoly trading at a discount because of overblown headline fears, a Wide-Moat financial software leader that is actively winning contracts from its largest competitors, and an iconic restaurant giant trading at a steep discount to its historical valuation.

Don’t Miss Our High Yield Content.

On June 23rd, we are kicking off a series all about high yield investing.

If you want to maximize your portfolio’s income without sacrificing business quality, jump on the VIP Waitlist.

You’ll get behind-the-scenes updates and the very first invite to download our brand-new high-yield special reports the minute we go live.

Don’t forget that you’ll also get the following just for joining the VIP list:

My high-yield stock watchlist

A Checklist of Dividend Investing Mistakes

The Highest Yielding Dividend Aristocrats

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.

the greed reading at the top paired with a best buys list at the bottom is the tension most investors don't notice in their own process. buying when the index says greedy isn't wrong, but it does mean youre paying a sentiment premium on top of whatever the fundamentals justify. and sentiment premiums are the first thing to evaporate in a correction.

the dividend framing helps though. if the income stream is what you're actually buying, the entry price matters less because youre not relying on someone else paying more later. youre relying on the business continuing to pay you. thats a different bet with a different risk profile and honestly its the one I think holds up better in an environment where nobody can agree on whether we're early in a cycle or late in one.