Best Buys March 2026

A new month, a new Best Buys List.

Each month, I’ll give an overview of my favorite stocks of the month.

Let’s dive into this update and show you some of my favorite stocks.

February 2026

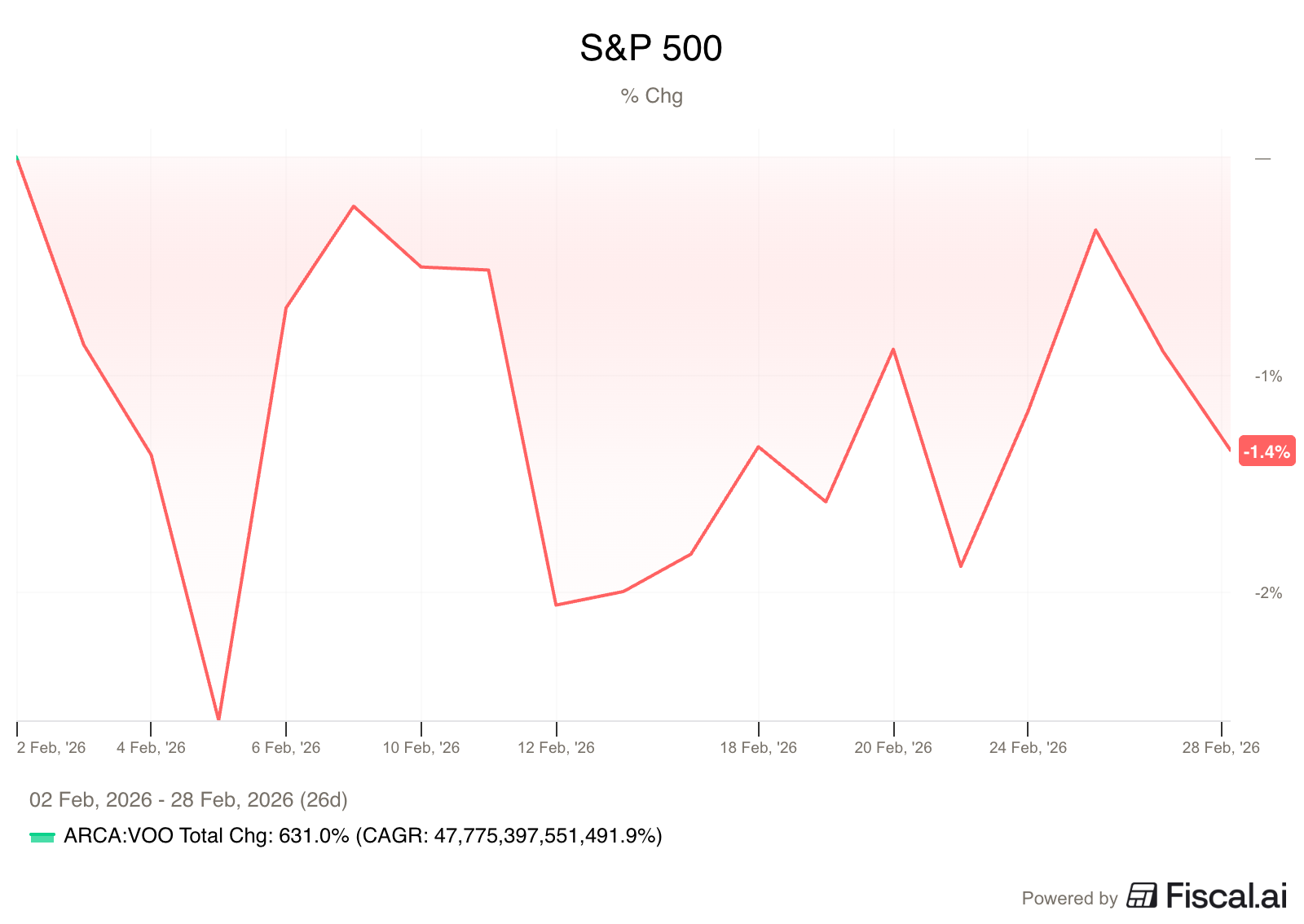

The S&P 500 was down 1.4% in February

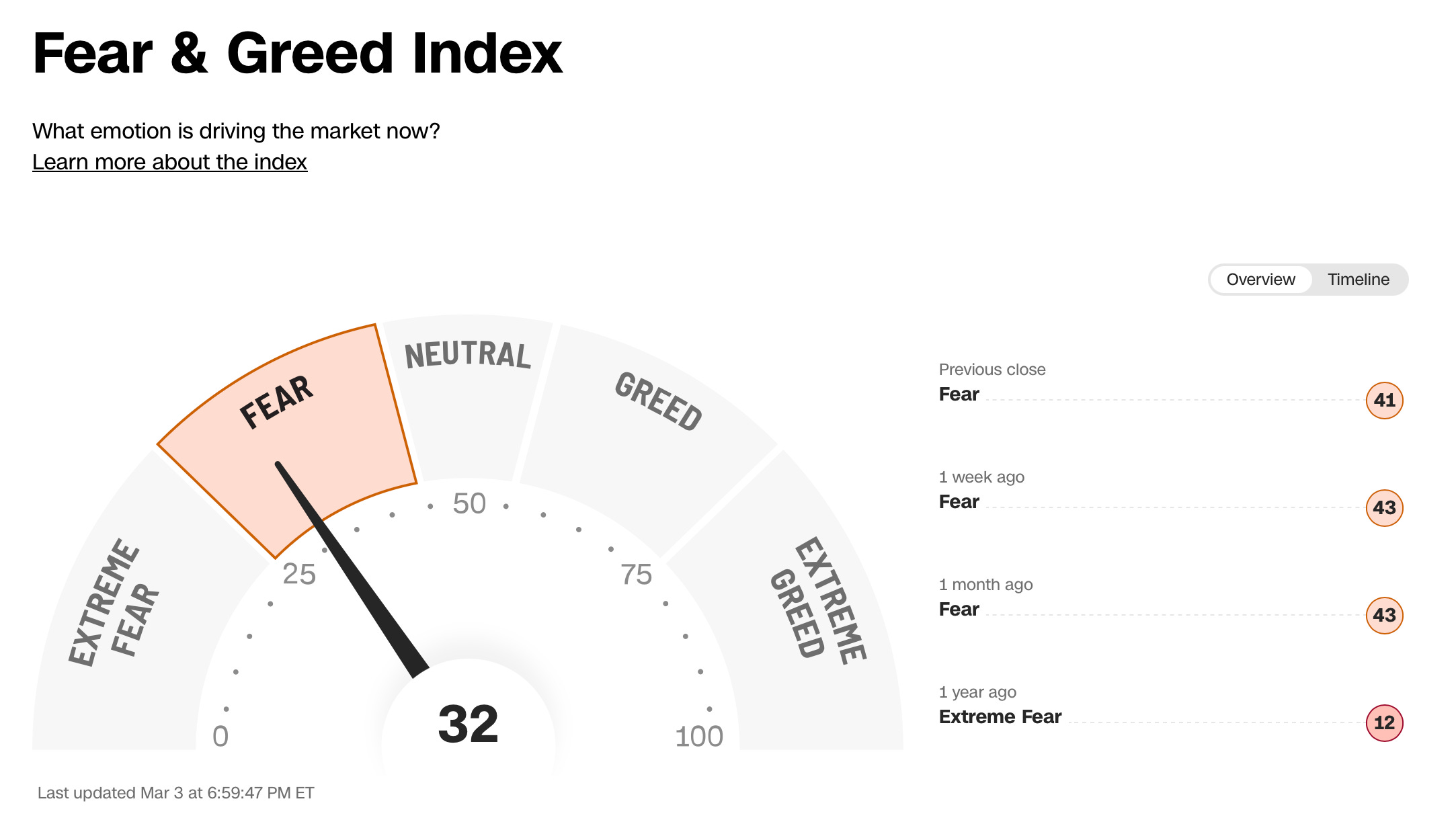

Investors are in ‘Fear’ today according to the Fear & Greed Index:

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

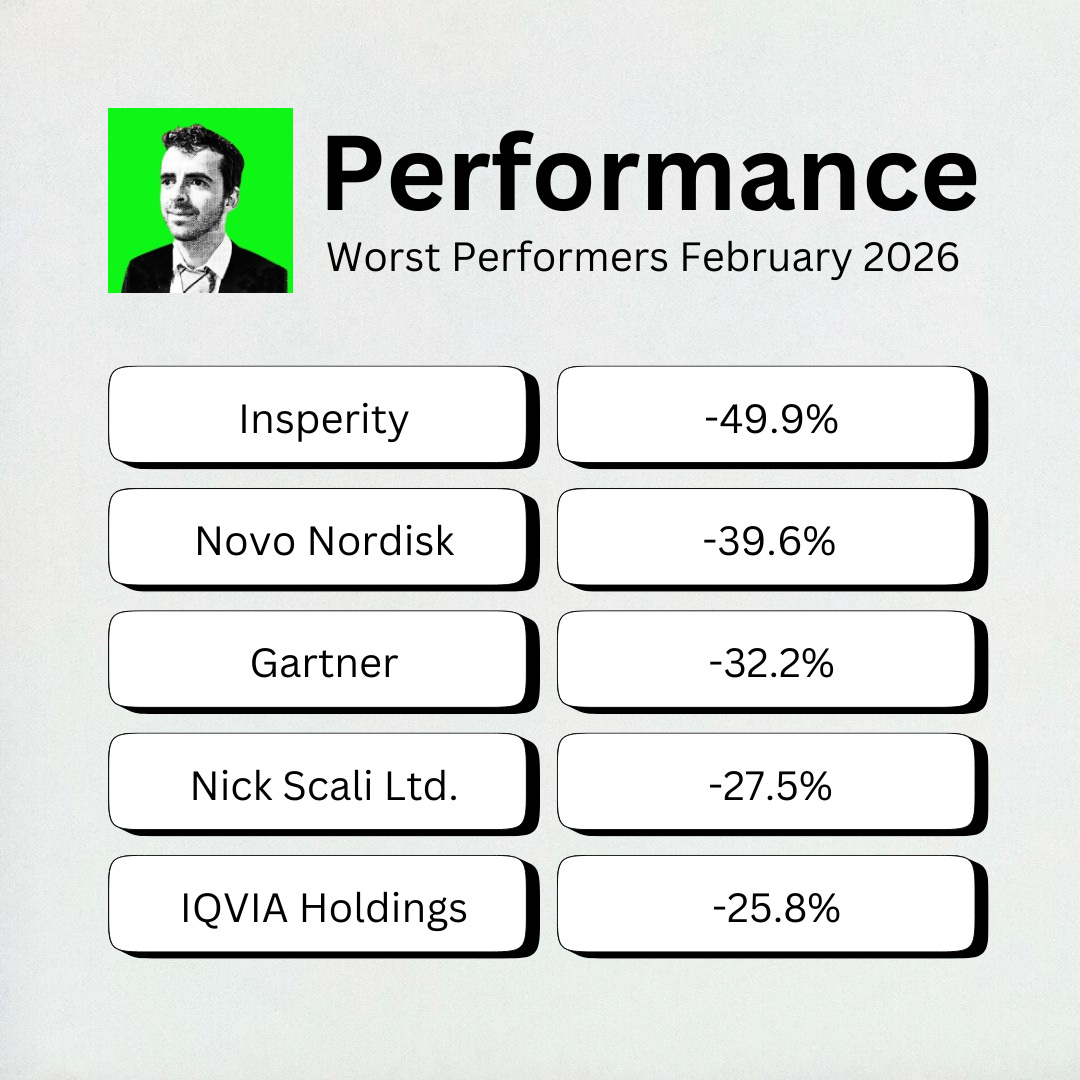

Worst performers

The cheaper we can buy great companies, the better.

The biggest decliner this month? Insperity, losing nearly half of its value.

Insperity is a professional employer organization (PEO) that provides human resources, payroll, and benefits administration services to help small and medium-sized businesses manage their workforce.

Insperity fell so much due to a major earnings miss and rising costs:

They reported a surprise loss of $0.60 per share, which was worse than the already low expectations.

This was mainly due to healthcare claims for the employees they manage being much higher than expected.

Their guidance also came in below analyst estimates.

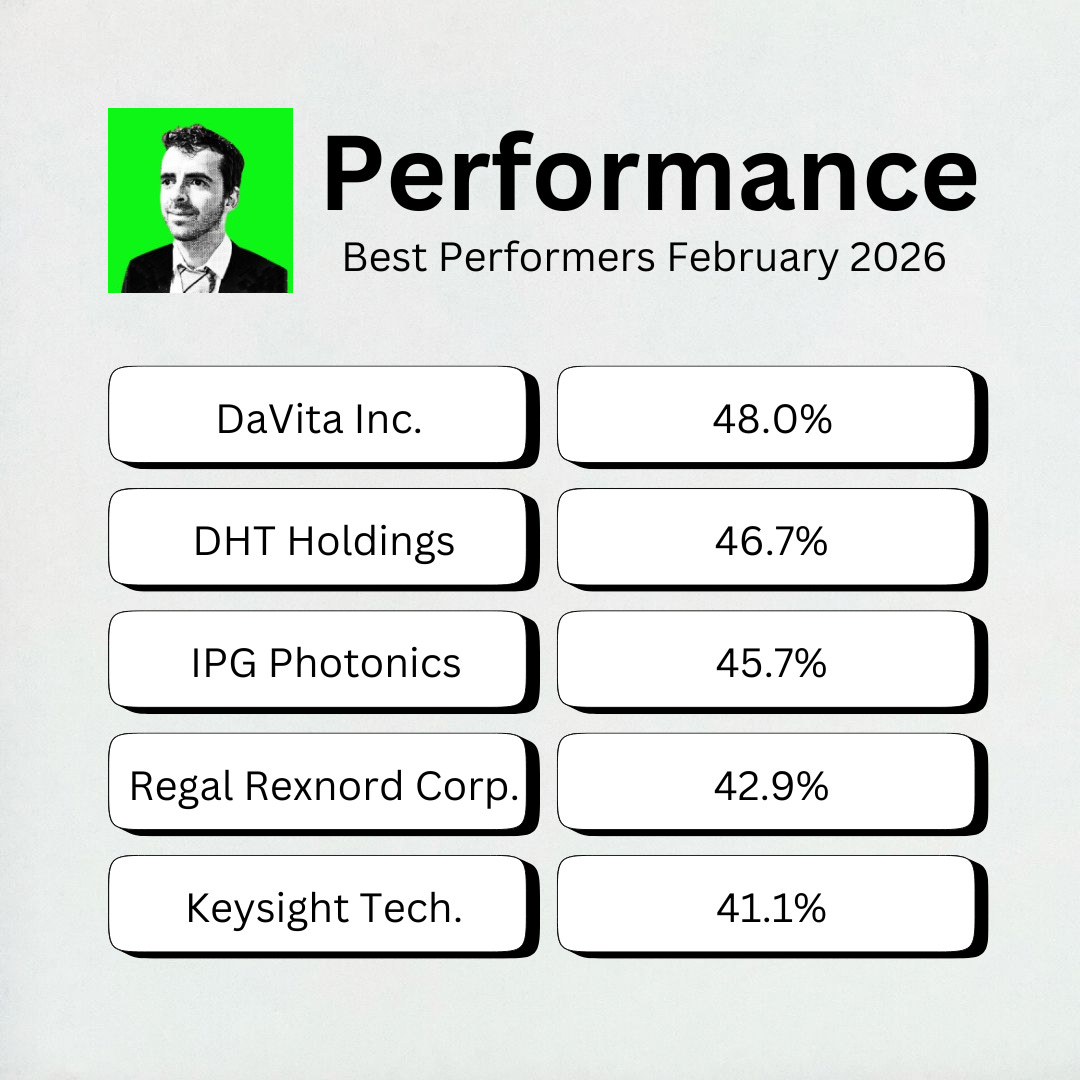

Best Performers

DaVita was this month’s best performer, rising 48%!

DaVita provides kidney dialysis services and comprehensive care to patients with chronic kidney failure through a global network of outpatient centers.

Its stock jumped so much because their Q4 results were significantly above what Wall Street expected for both revenue and profit.

On top of that, they issued guidance that was much higher than analysts anticipated.

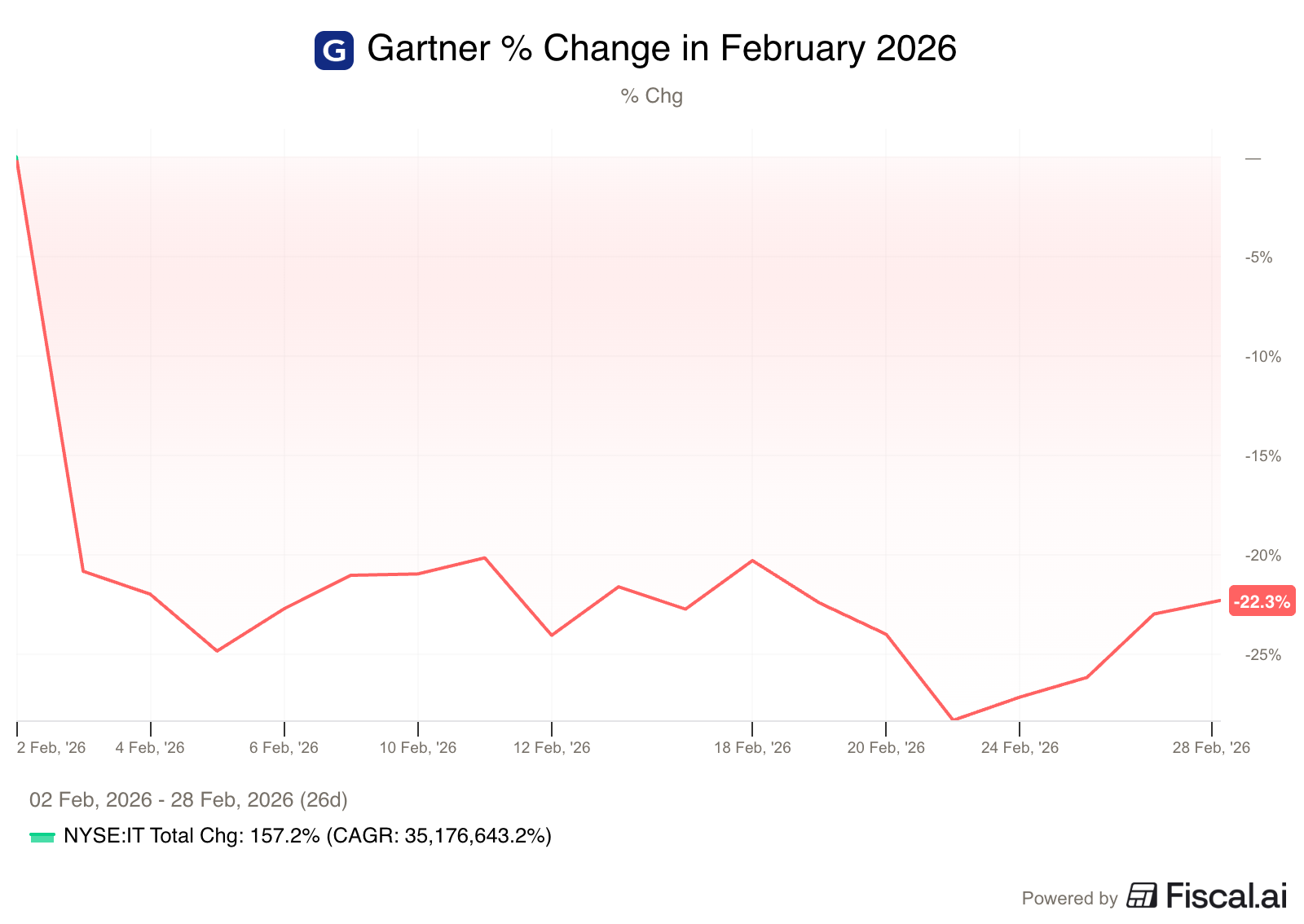

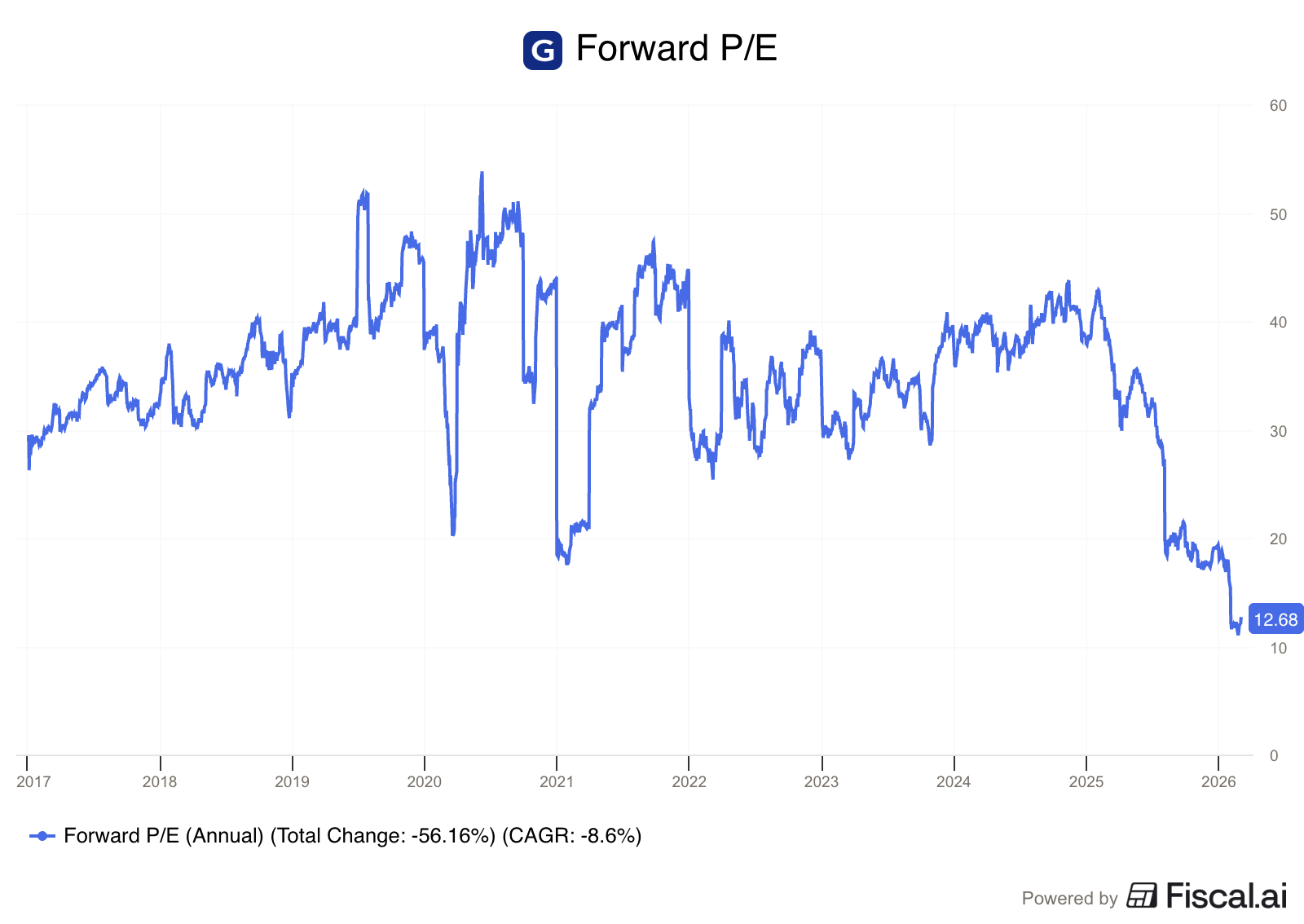

Spotlight: Gartner ($IT)

Gartner was one of the worst performers in February, with shares dropping 21% in a single day.

How does the company make money?

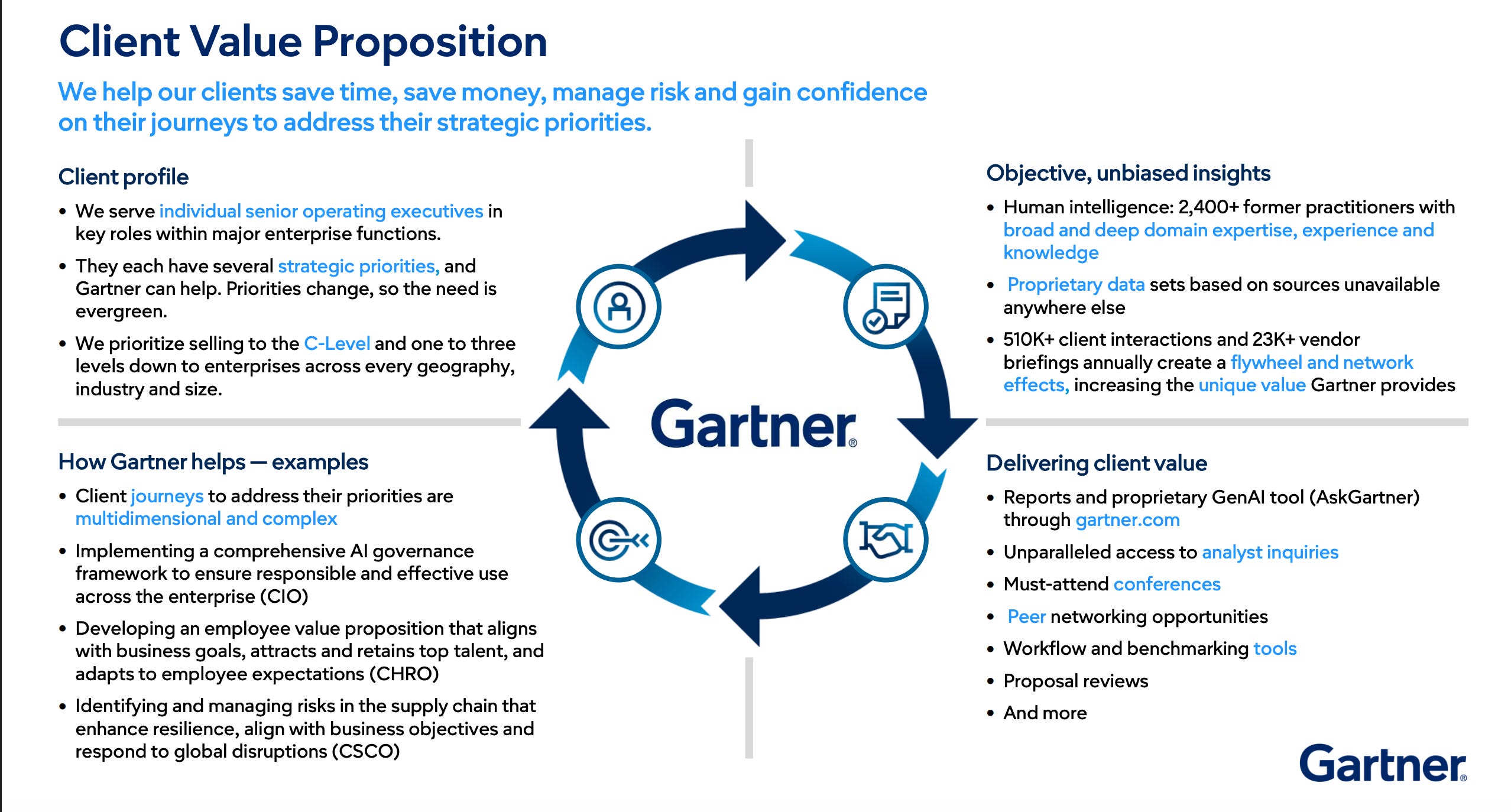

Gartner provides business and technology insights to help executives make decisions. They operate through three primary segments:

Insights: The company’s core business, providing research, expert briefings, and consultations.

Conferences: High-profile industry events, such as the IT Symposium/Xpo, where IT leaders network and share best practices.

Consulting: Strategic advice for technology initiatives.

Gartner makes about 80% of total revenue through upfront, noncancelable subscriptions for its research.

Why is it interesting?

Gartner has long been considered the gold standard for IT research.

Scale: With over 2,400 experts and 13,000 customers, Gartner is significantly larger than its direct competitors.

The Magic Quadrant: For many software vendors, being featured in Gartner’s research is required to be considered by large enterprise customers.

Operating Leverage: The marginal cost of delivering an extra research report to a new client is near zero, allowing for attractive profit potential as the customer base grows.

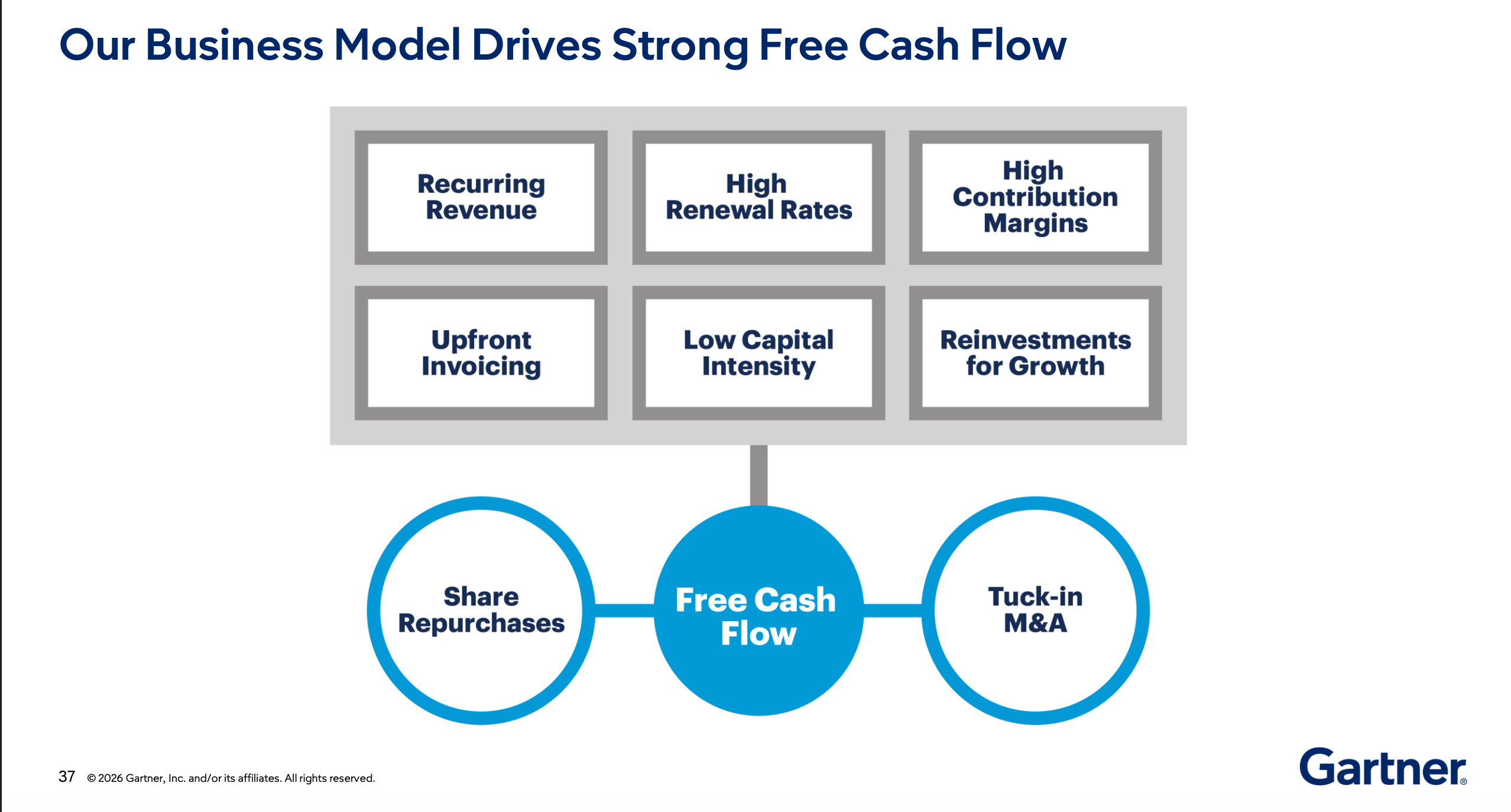

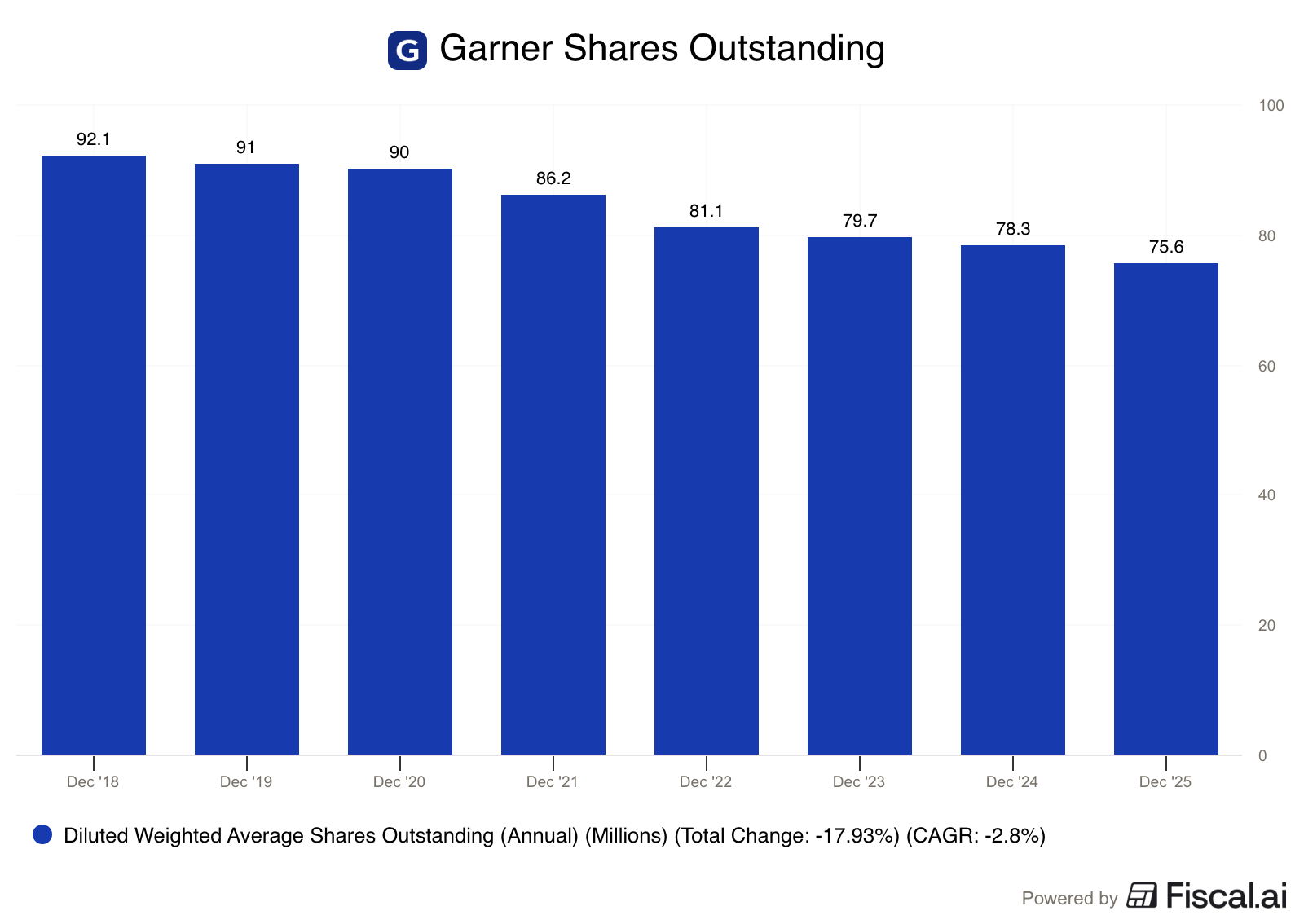

Gartner generates a lot of Free Cash Flow

Which they use to consistently buy back their own shares.

Why’s the stock down?

Gartner’s stock is down due to a combination of disappointing recent performance and future uncertainty:

Guidance: Management guided for revenue and earnings to decline in 2026

Federal Spending Cuts: The US federal government renewed less than half of their contracts in 2025.

AI Disruption: There is a growing fear that AI makes it easier for companies to gather IT information themselves, undercutting the value of Gartner’s research.

Low Retention: Client retention recently declined to 84%

Investor Takeaway

Gartner is having a hard time right now.

Management has introduced a transformation plan in response to falling revenue and the threat of AI, focusing on four areas: impact, volume, timeliness, and user experience.

Here’s a summary of their plan:

AskGartner: An AI chatbot designed to make their research easier to access.

Human Connection: Shifting toward hands-on, expert-led services that AI cannot easily replicate.

Flexible Terms: They’re considering moving away from rigid, multi-year, upfront payments to prevent customer churn.

Operational Fixes: Potential workforce restructuring or product overhauls.

Gartner has gone from an industry leader to a turnaround story.

If you believe the company can transition to continue to lead in the age of AI, it’s currently trading at one of the lowest valuation we’ve seen in quite a long time.

March Best Buys

February continued to be a month where individual stocks had big moves in price.

I scanned the Buy-Hold-Sell List for great dividend payers at attractive prices to highlight for you this month.

Let’s dive into 5 of the most interesting ones I found!

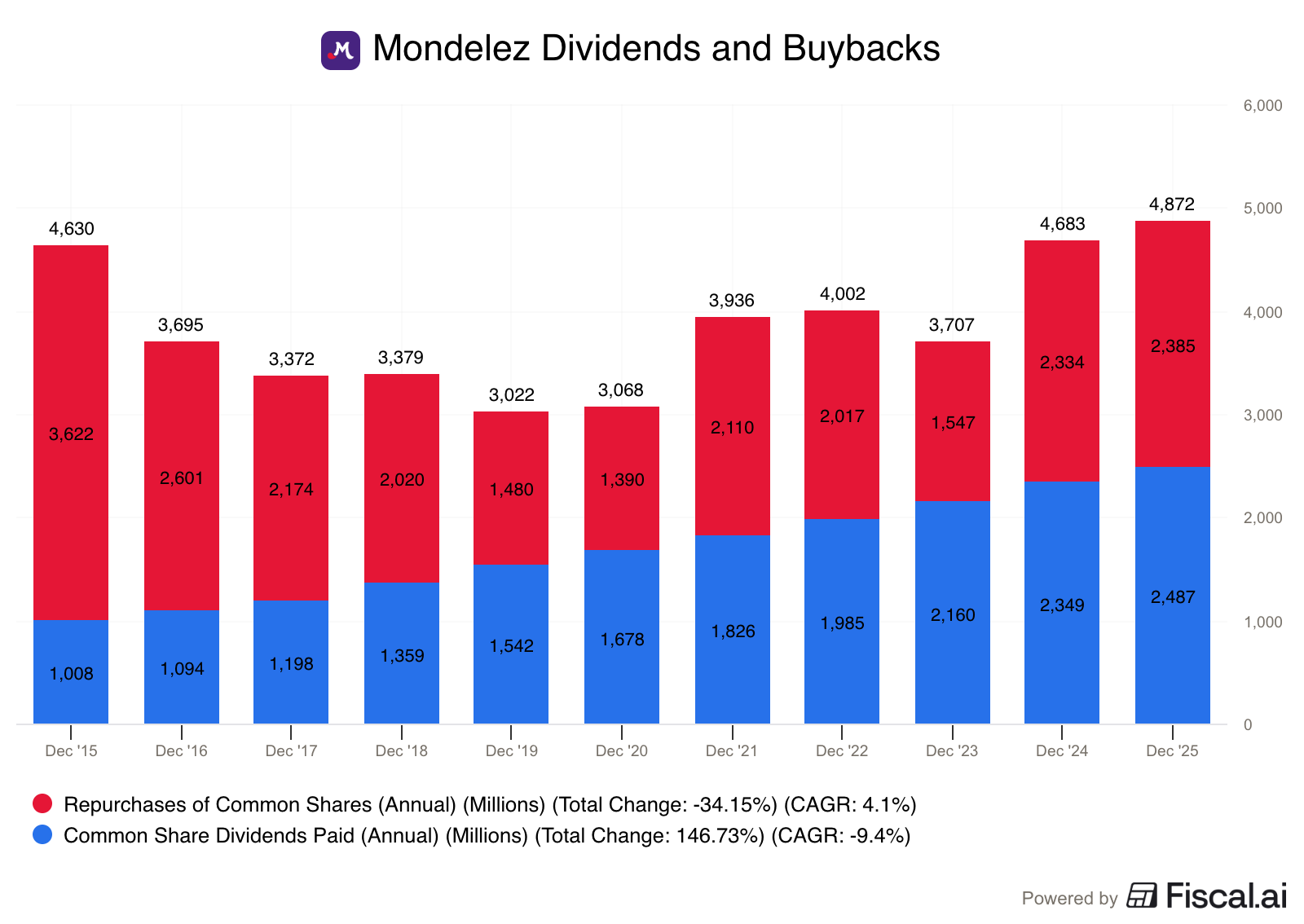

5. Mondelez (MDLZ)

How do they make money?

Mondelez owns iconic brands like Oreo, Cadbury, and Ritz. They generate revenue by selling snacks to consumers in over 150 countries through a massive retail distribution network.

Why It’s Interesting

Mondlelez has very strong brands, with pricing power.

Even when prices rise, consumers rarely trade down from an Oreo to a generic cookie.

It’s also a company that returns a lot of cash to shareholders.

In 2025, they returned nearly $5 billion to shareholders, split fairly evenly between dividends and buybacks.

The most interesting thing about Mondelez?

Unlike a lot of it’s competitors, Mondelez has huge exposure to developing markets like India and China, where a rising middle class is consuming more packaged snacks every year.

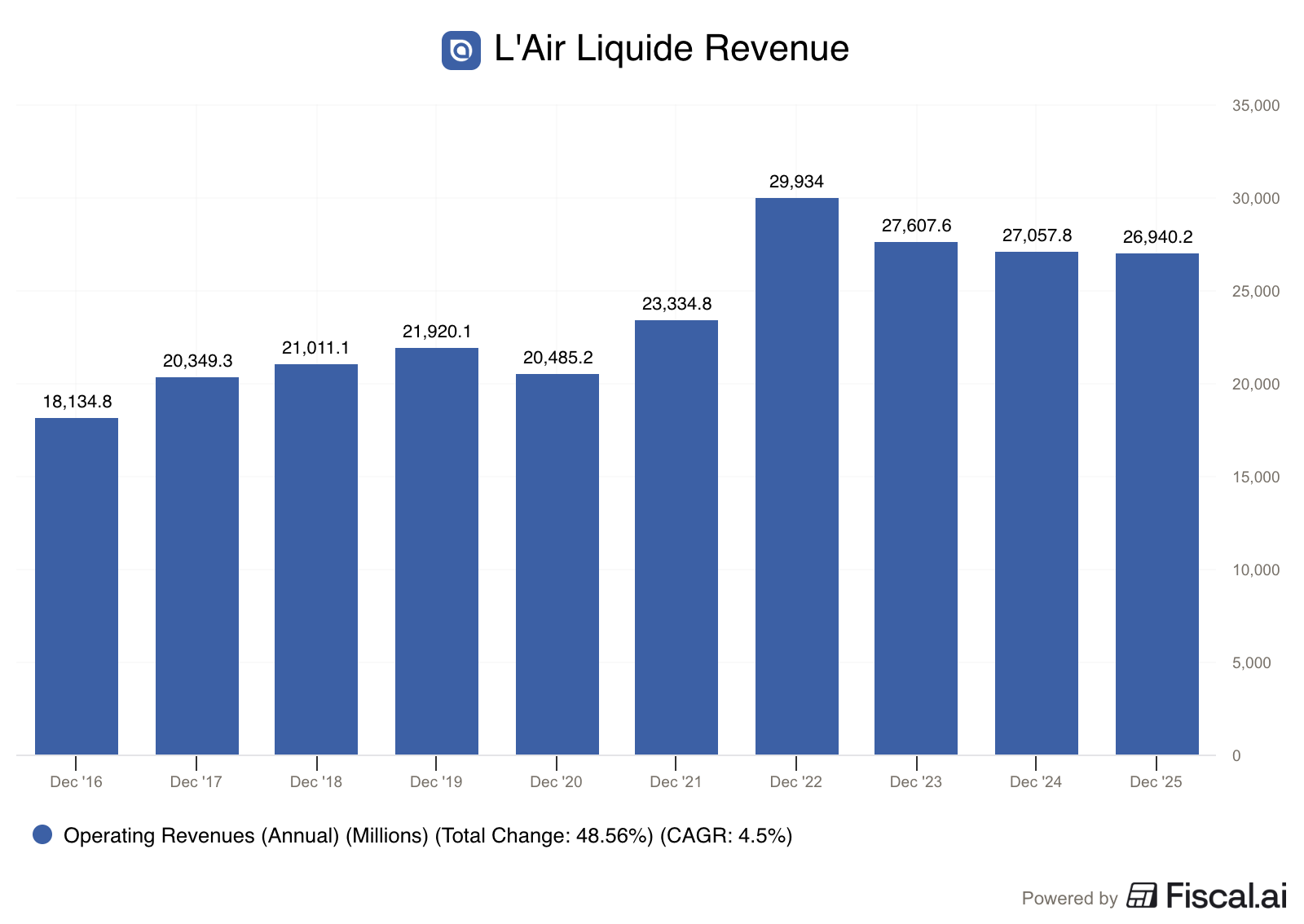

4. L’Air Liquide (AI)

How do they make money?

L’Air Liquide is a world leader in industrial gases, supplying oxygen, nitrogen, and hydrogen to the manufacturing, healthcare, and energy sectors.

Why It’s Interesting

L’Air Liquide usually builds a pipeline directly to it’s customers.

This is very convenient for the customer as they won’t run out of gas, but it also creates a very high switching cost.

Once a pipeline is connected to a factory, it is nearly impossible for a customer to switch suppliers without stopping production, leading to a customer retention rate higher than 95%.

In addition, most revenue comes from take-or-pay contracts lasting 10 to 20 years.

This means they get paid even if the customer uses less gas, providing incredibly stable cash flows.

But L’Air Liquide has room for growth too.

They’re a key player in the semiconductor industry.

Electronics projects, driven by the explosion in Artificial Intelligence now make up 40% of their new business backlog.

They are also investing €8 billion into low-carbon hydrogen over the next 15 years.

Management expects this to triple their revenue from hydrogen.

They have increased their dividend by around 8% each year for the last 20 years.

You’ve just seen two of my favorite stocks for February, but paid Partners get three more.

Whenever you’re ready

Whenever you’re ready, here’s how I can help you:

✍️ Three articles per week (Monday, Wednesday, and Saturday)

📚 Full access to our entire library of data-driven articles

📈 An insight into our Portfolio full of interesting Dividend Stocks

🔎 Full investment cases about interesting companies

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.