Best Buys May 2026

A new month, a new Best Buys List.

Each month, I’ll give an overview of my favorite stocks of the month.

Let’s dive into this update and show you some of my favorite stocks.

April 2026

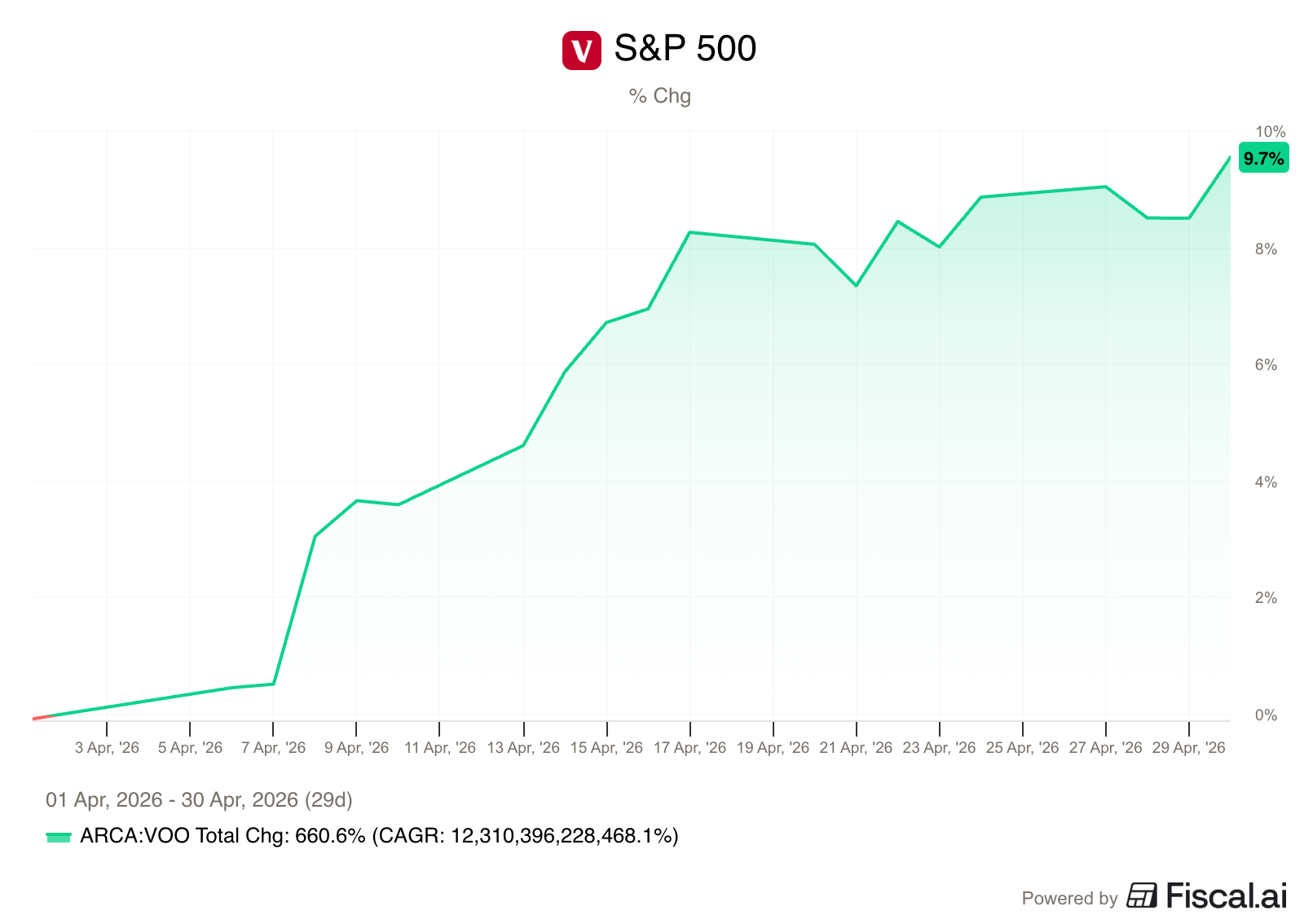

The S&P 500 increased by 9.7% in April.

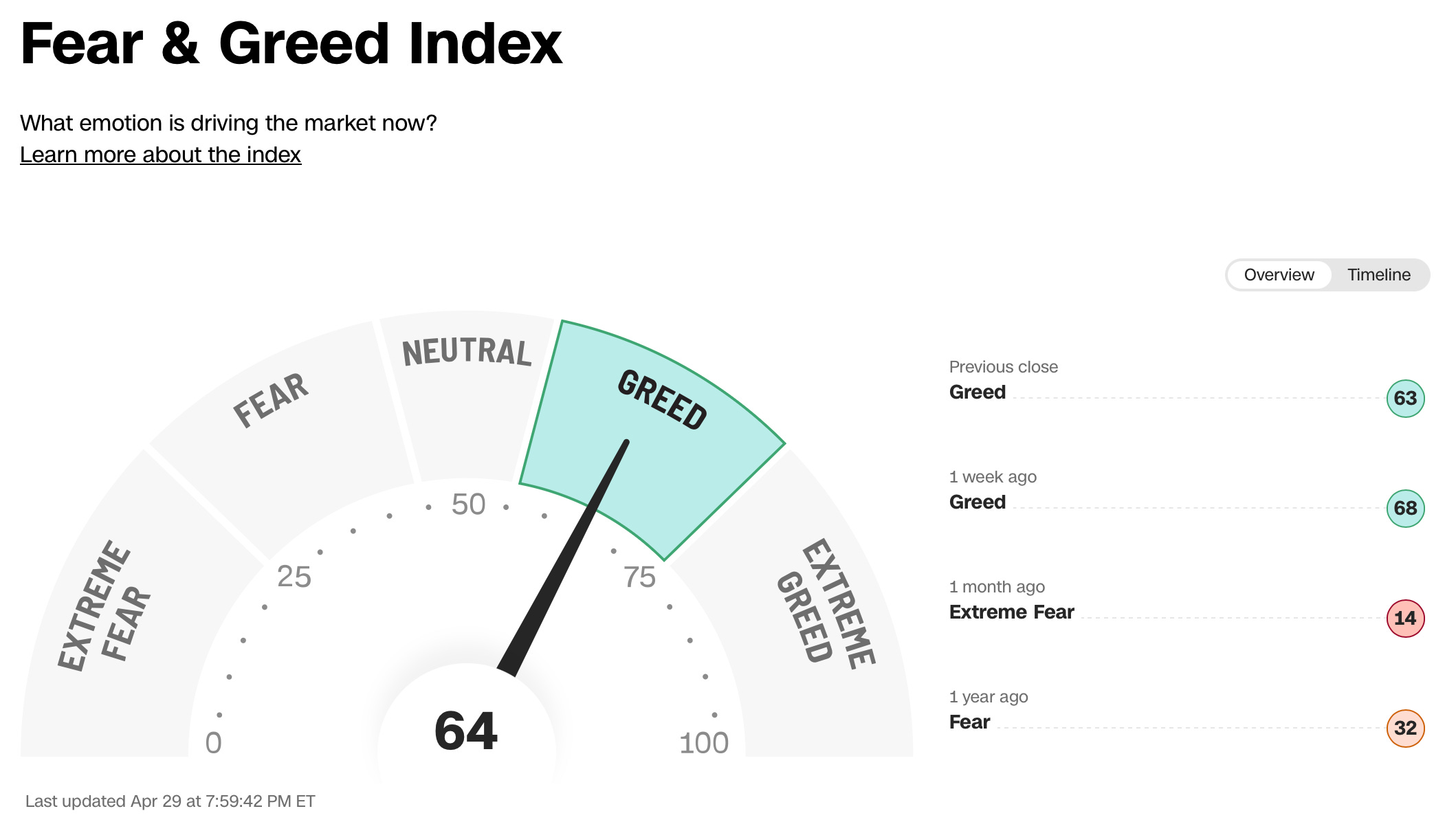

Investors are in Greed today according to the Fear & Greed Index:

Best & Worst Performers

This overview shows you the best and worst performers in our investable universe.

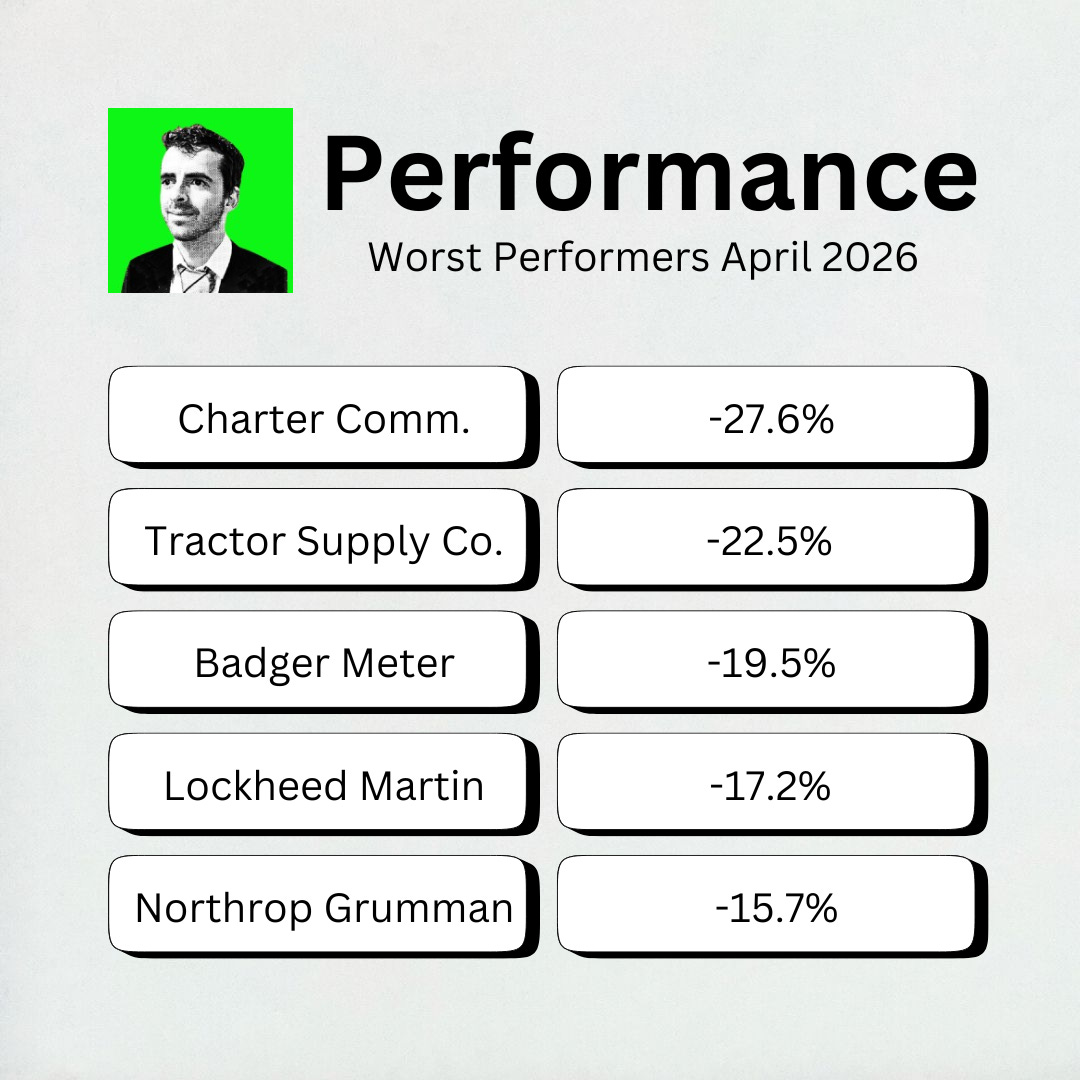

Worst performers

The cheaper we can buy great companies, the better.

The biggest decliner this month? Charter Communications, losing 27%.

Charter Communications is a broadband and cable operator that provides internet, TV, and mobile services to over 30 million customers under the Spectrum brand.

Charter fell this month due to shrinking subscriber numbers and high infrastructure costs:

Broadband Losses: The company reported a loss of 120,000 internet subscribers in the first quarter

Earnings Miss: They earned $9.17 per share, missing the $10.08 analysts expected, as revenue from traditional cable TV packages continued to slide.

Spending: Management is spending billions ($2.9 billion this quarter alone) on network evolution and rural expansion, which is eating into cash flow at a time when competition is very high

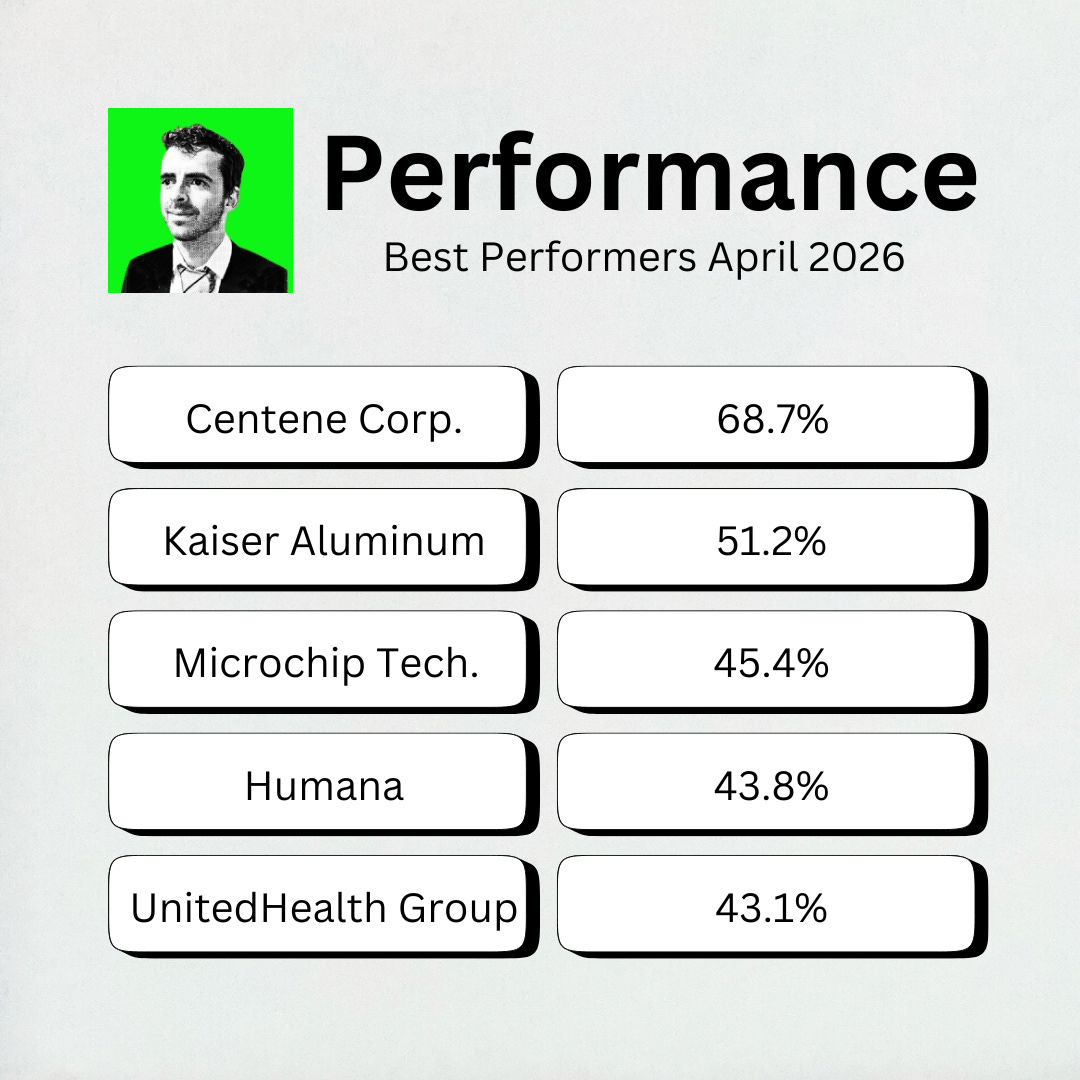

Best Performers

Centene Corporation was this month’s best performer, rising 68%!

Centene Corporation acts as a middleman for Medicaid, Medicare, and the Health Insurance Marketplace.

Centene gained this month because of a massive earnings beat and raising its future outlook:

Earnings Beat: They reported adjusted earnings of $3.37 per share, well above the $2.13 Wall Street predicted due to cost management and lower-than-expected medical claims.

Raised Guidance: Centene raised its profit and revenue forecasts for the entire year, signaling that its margin recovery plan is working ahead of schedule.

Medicare: Other insurers have struggled with rising costs in Medicare Advantage, Centene’s had improved profitability

You’ll notice that Humana and UnitedHealth Group are in our Best Performers list this month as well, showing that the whole health insurance segment did well.

Spotlight: Adobe ($ADBE)

Adobe is currently facing a perfect storm of uncertainty.

Between a CEO transition and AI disruption fears, the stock has gone nowhere but down.

But this could be an opportunity to buy a world-class monopoly at its lowest valuation in a decade.

How does Adobe make money?

Adobe is the standard for the creative digital world.

They sell creative software as a service (SaaS) to professional designers, photographers, filmmakers, and digital media companies.

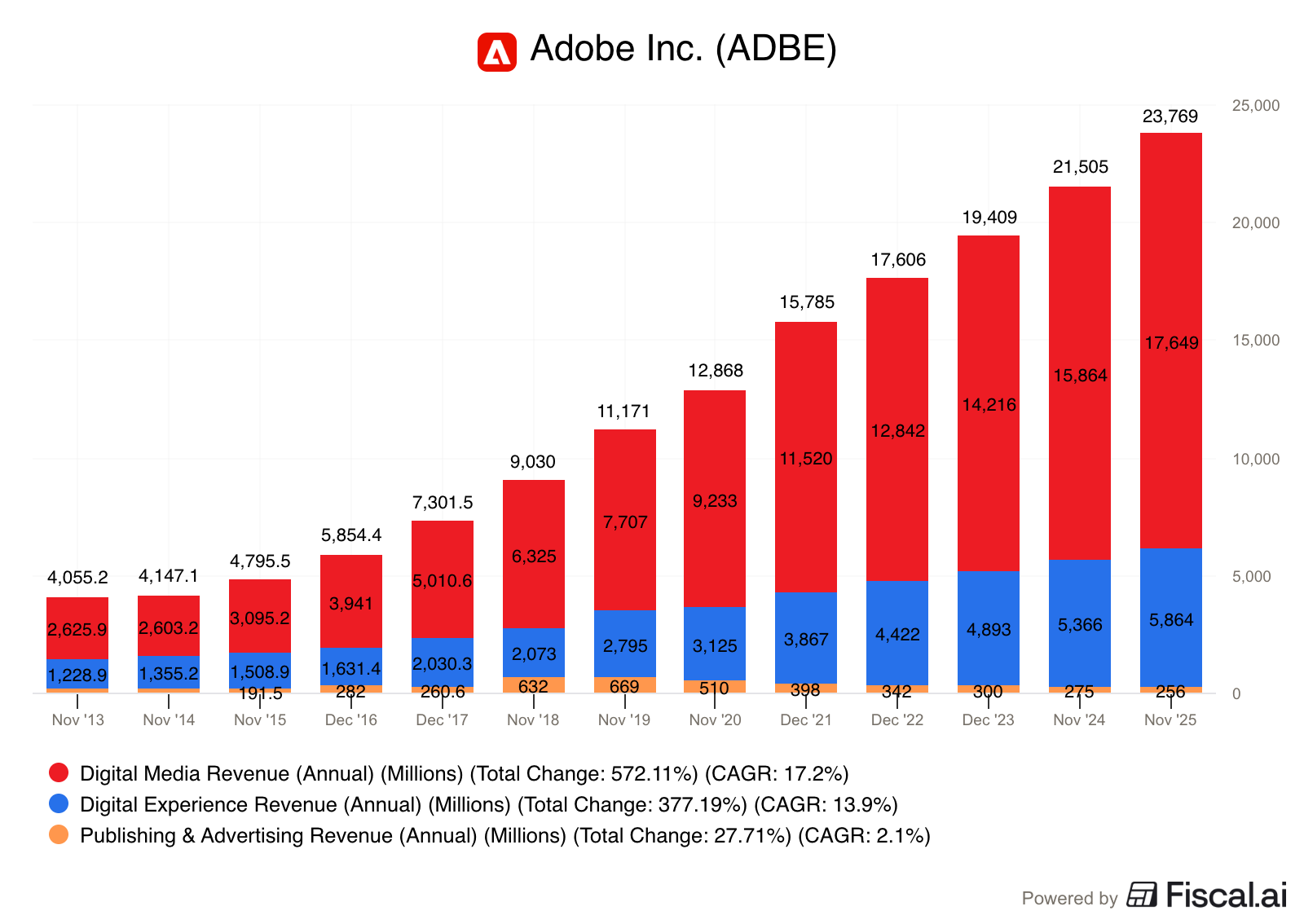

Digital Media (~74% of revenue): This is the core of the company, consisting of Creative Cloud (Photoshop, Illustrator, Premiere Pro) and Document Cloud (Acrobat/PDF).

Digital Experience (~24% of revenue): A comprehensive suite for marketers and brands to manage customer journeys, analytics, and personalized advertising at scale.

Publishing and Advertising (~2% of revenue): This segment covers legacy products like technical messaging, web conferencing, and high-end printing.

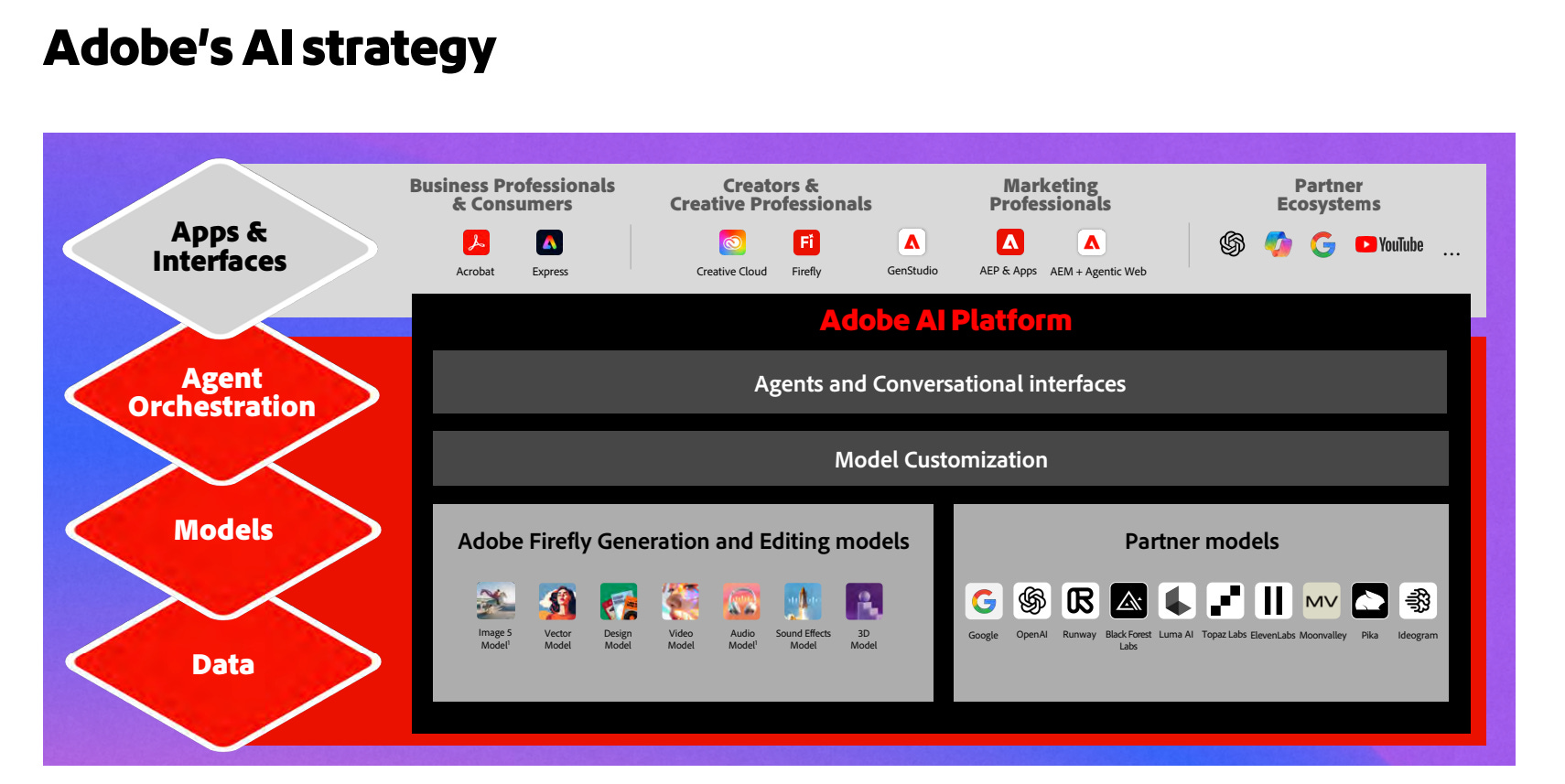

Adobe has incorporated its own Firefly AI model into its apps, along with models from Google, Open AI, and others.

To monetize it, they’re moving to a credits & tokens pricing model.

Instead of just paying for a seat, users pay for usage (Firefly credits).

This allows Adobe to capture more value from high-end professionals without alienating casual users.

Why does it deserve to be in the spotlight?

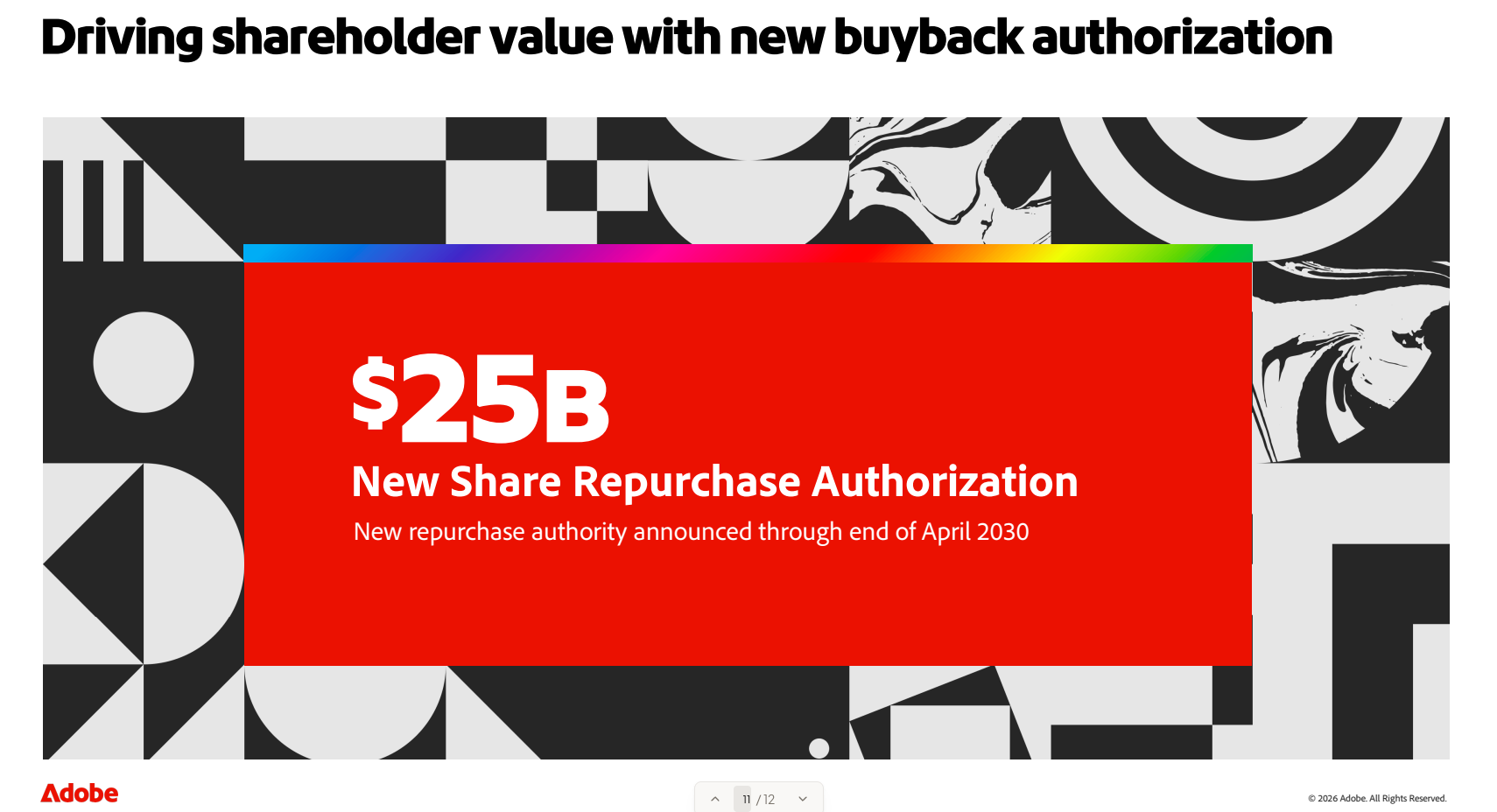

1. $25 Billion in Buybacks

Adobe doesn’t pay a dividend, but they are returning a lot of capital though buybacks.

In April Adobe authorized a massive $25 billion repurchase program through 2030.

At its current market cap of ~$100 billion, Adobe is planning to retire 25% of the entire company.

Existing shareholders should own a significantly larger portion of the company when they’re done.

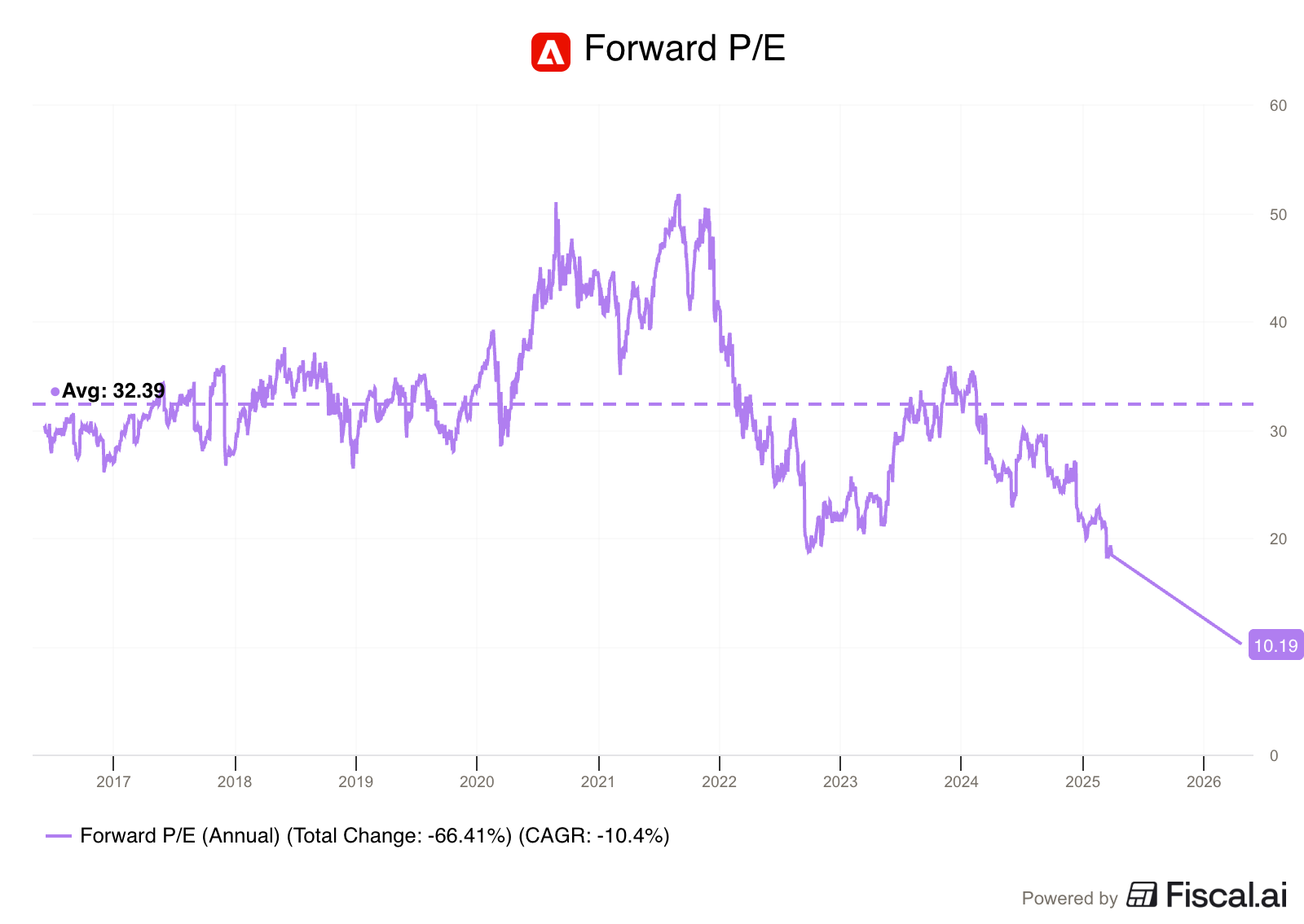

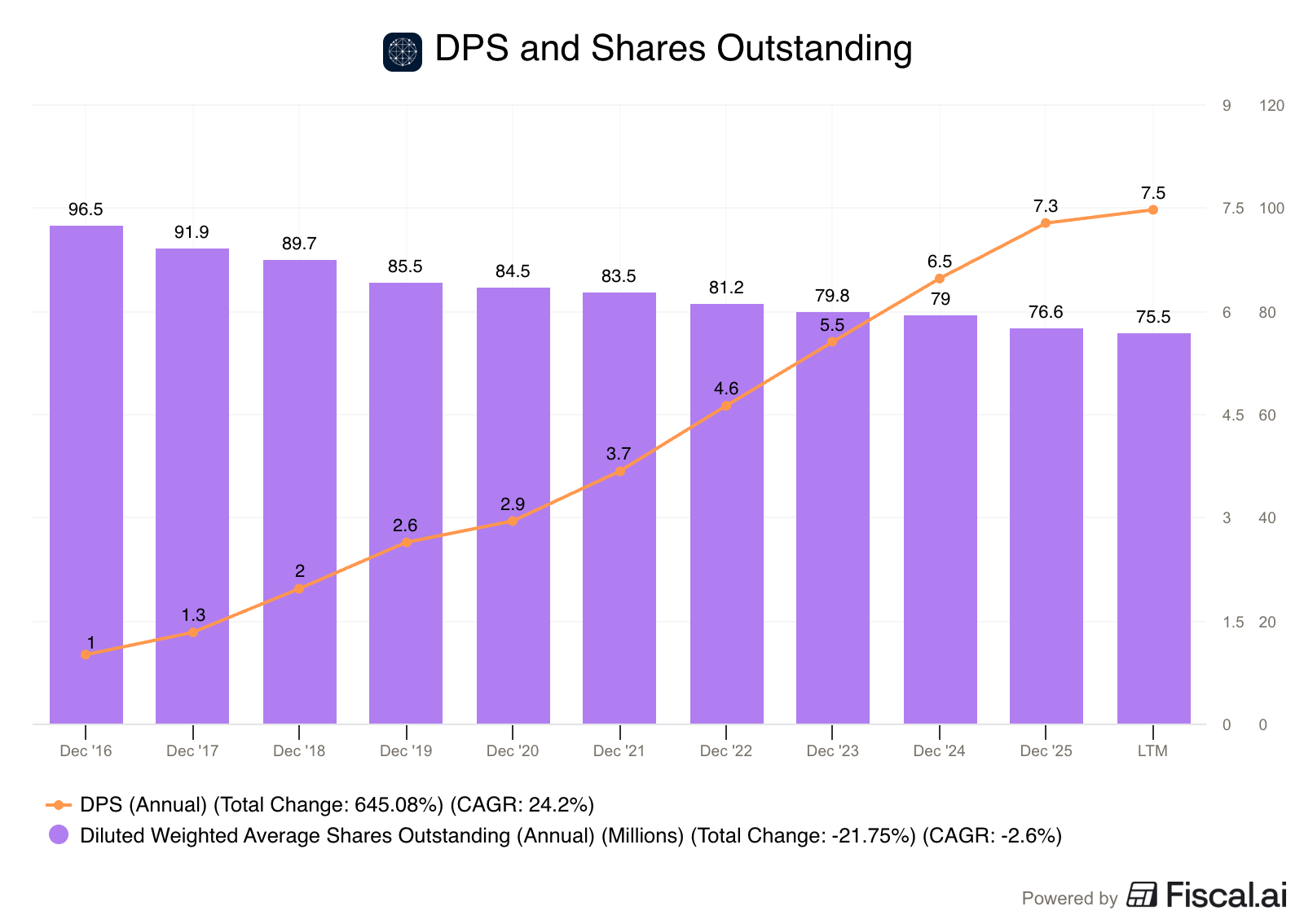

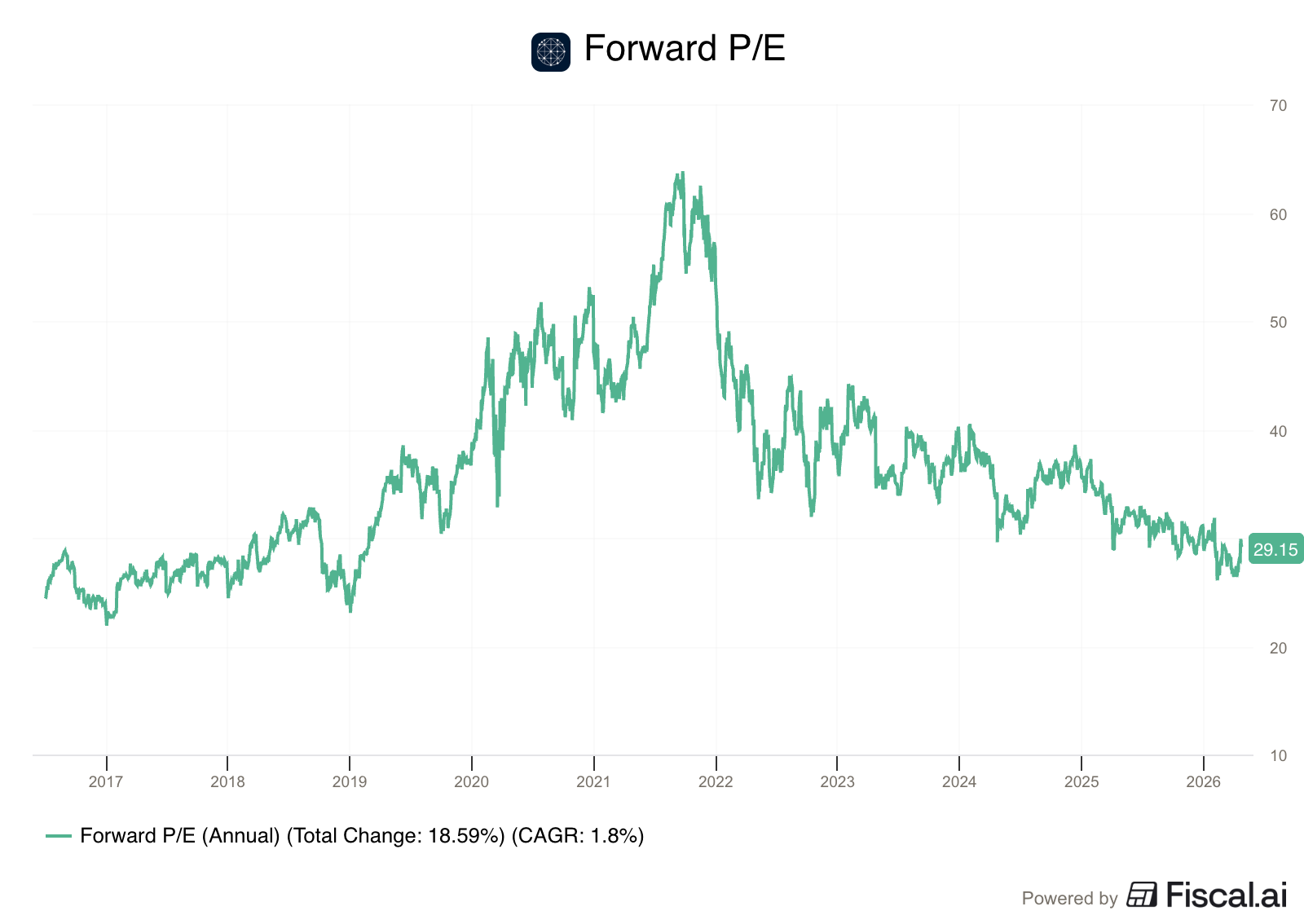

2. Multi-Year Valuation Lows

For most of the last decade, Adobe traded at a P/E above 30x.

Today, it trades at roughly 10x Forward Earnings.

Investors are terrified of AI disruption.

These are risks, but the market is pricing a business with 40% FCF margins at the same multiple as a slow growing, CapEx heavy utility company.

Another reason the market is pricing the business so low?

3. CEO Transition Uncertainty

In March, long-time CEO Shantanu Narayen announced he is stepping down after 18 years.

Narayen was responsible for Adobe’s transition to the Cloud.

His departure has the market nervous as the board searches for a successor during a time of potential disruption.

This is another risk, but Adobe remains the standard for the creative world.

That’s bigger than any one person.

Will AI kill Adobe?

The market thinks AI will kill Adobe.

I’m not so sure, here's why:

Control: Typing a prompt to get a video or image is fun for casual users, but it’s a terrible professional workflow. Professionals need granular control.

Interaction: It’s very hard to prompt an image into exactly what a client wants. Pros need to manually move layers, adjust lighting, and mask edges. Adobe is building AI into the environments that professionals work in.

Usage Pricing: By moving to token-based pricing, Adobe turns AI from a threat into a new revenue stream. Every time a designer uses AI to save time, Adobe gets paid a fee.

Another thing to consider?

AI compute is limited, and it may become very expensive for heavy users.

That’s why Open AI shut down Sora, it’s video generation app.

The Bottom Line

The market is pricing Adobe like a dying company.

The board and leadership at Adobe don’t seem to think that’s true.

They still have a dominant position in the professional creative workflow.

And they’ve bet $25 billion in buybacks that they’ll remain the industry standard and will integrate AI instead of being replaced by it.

For investors who agree with them and can look past the CEO headlines, this could be a chance to buy a historically dominant business at a historically low multiple.

May Best Buys

I scanned the Buy-Hold-Sell List for great dividend payers at attractive prices to highlight for you this month.

Let’s dive into 5 of the most interesting ones I found!

By monthly tradition, here are our five favorite income stocks for April.

What’s happening in the markets? Where is the income? Let’s get a little bit wiser today.

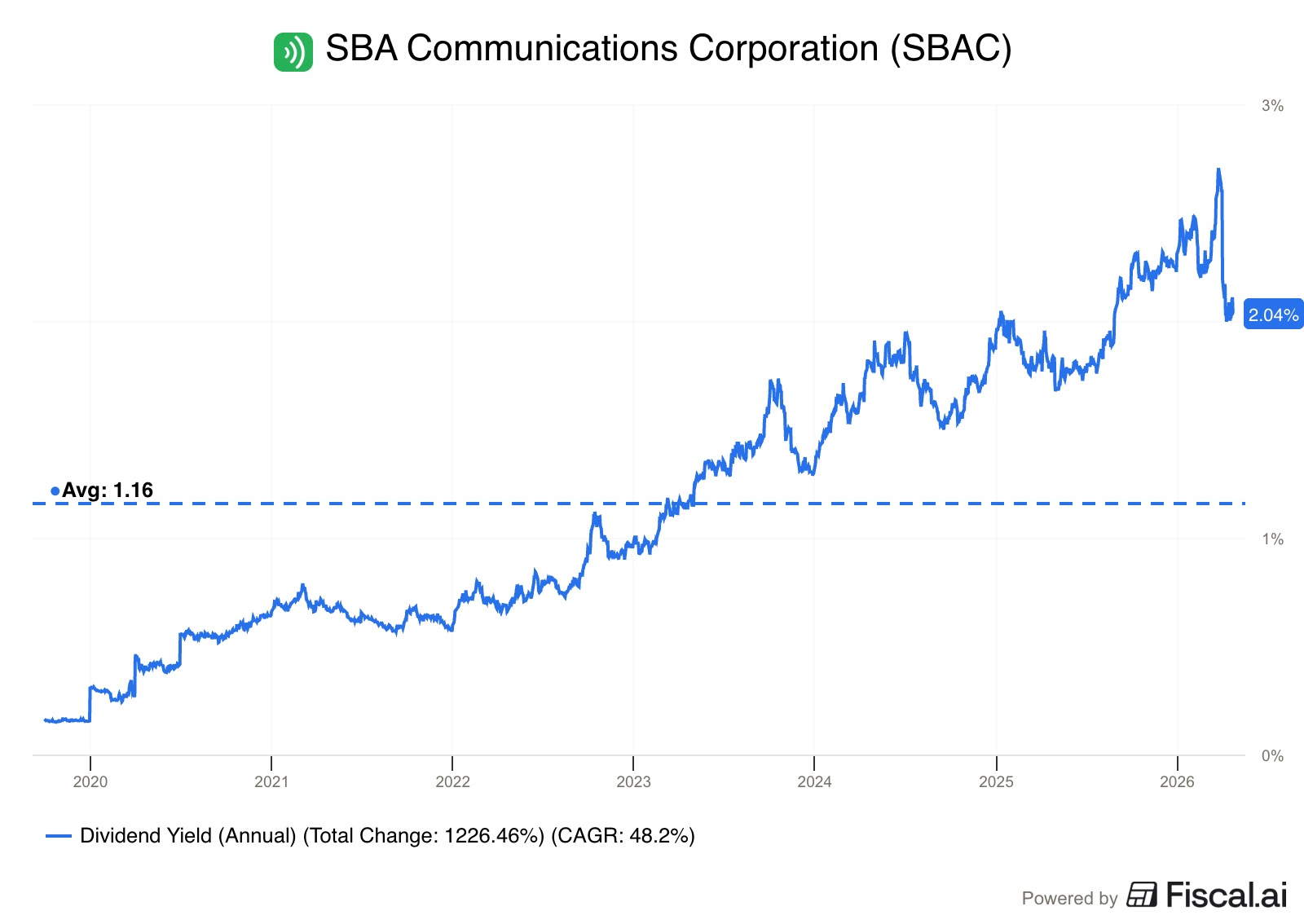

5. SBA Communications ($SBAC)

How does SBA Communications make money?

SBAC is a REIT that owns cell towers across the Americas.

They lease space on those towers to carriers like Verizon, AT&T, and T-Mobile.

The moat here is built on high switching costs. Once a carrier installs its 5G gear on an SBAC tower, they almost never leave.

Moving that equipment is slow, expensive, and breaks the network. So the carriers stay, and the rent keeps coming, often for decades.

Rising interest rates have been a headwind for all REITs over the last two years.

SBAC was sold off with the rest of the pack, regardless of its quality.

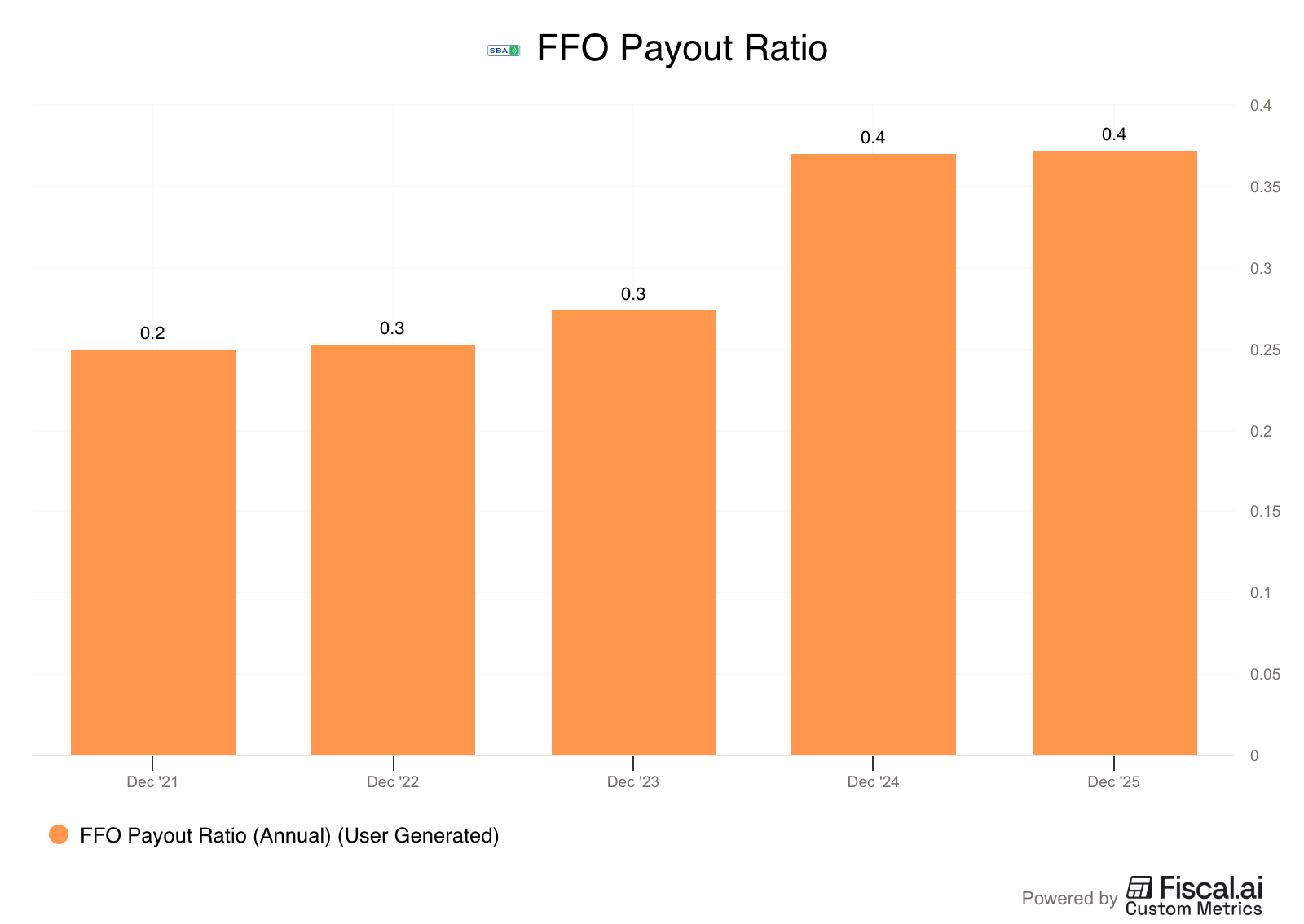

The dividend yield of ~2% is above the historical average.

With a payout ratio below 50% of FFO, there is plenty of room to keep growing the dividend while the carriers continue their 5G rollout.

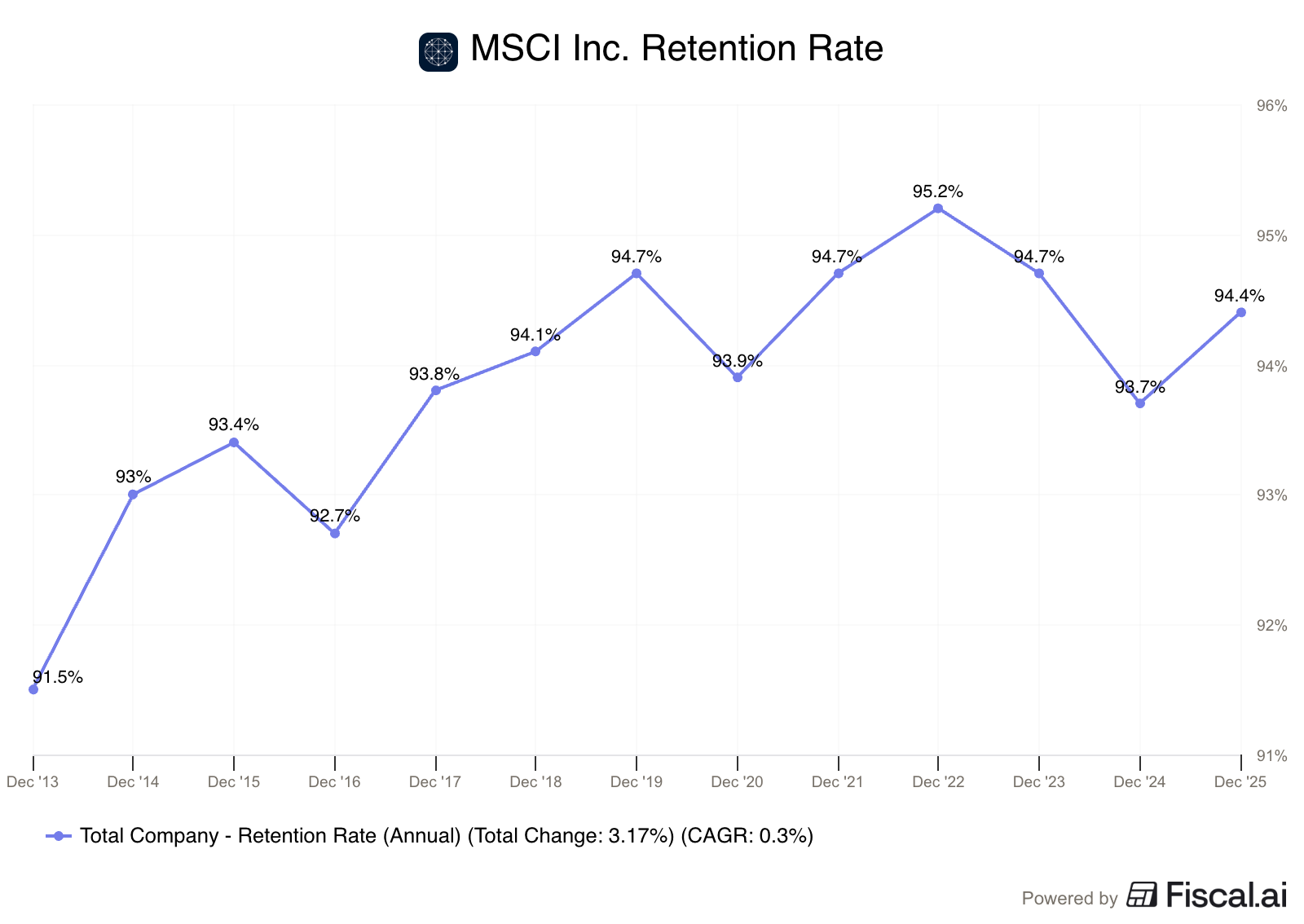

4. MSCI Inc. ($MSCI)

How does MSCI make money?

MSCI is the Gold Standard for financial data.

If a bank wants to launch an ETF or a pension fund wants to track international markets, they use an MSCI index.

As passive investing rises, so do the fees that MSCI earns.

Those fees are also very sticky.

Once a financial institution integrates MSCI’s data into their software and compliance systems, the switching costs are enormous.

This leads to retention rates consistently above 90%.

MSCI does pay a growing dividend, but it’s probably more interesting as a cannibal stock.

They use their high margins to consistently buy back their own shares.

The stock looked quite expensive for several years, but it’s now coming back down to a more reasonable valuation.

It’s a very high quality business that looks to be near a fair price, earning it a spot on this month’s Best Buys list.

You’ve just seen two of my favorite stocks for April, but paid Partners get three more.

Whenever you’re ready

Whenever you’re ready, here’s how I can help you:

✍️ Three articles per week (Monday, Wednesday, and Saturday)

📚 Full access to our entire library of data-driven articles

📈 An insight into our Portfolio full of interesting Dividend Stocks

🔎 Full investment cases about interesting companies

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.