Buffett's top-tier income generators

Warren Buffett set the bar very high.

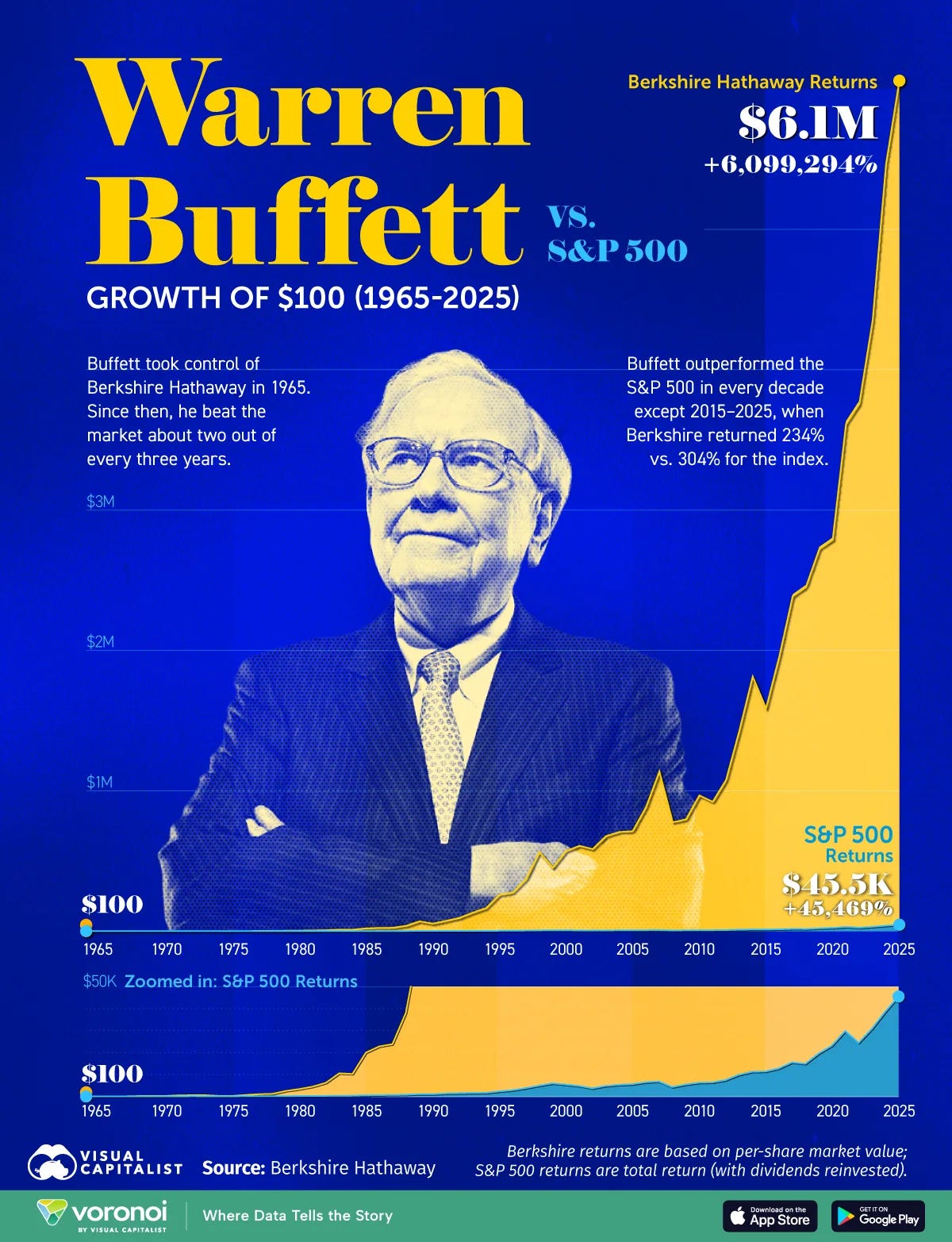

It would be hard for anyone to deliver a 5,000,000% return in 60 years.

That’s an average return of 20% (!) per year for 60 years.

That’s nearly double the returns you get from the S&P 500.

And did you know?

91% of fund managers fail to beat the Index.

No wonder Berkshire CEO, Greg Abel, said, Buffett is a tough act to follow.

I’ve been thinking about this since I returned from the 2026 Berkshire AGM.

Just look at the numbers in the chart below.

It shows your returns if you had invested $100 in Berkshire 60 years ago.

Indeed, in his prime, the Oracle was one tough customer.

Institutional investors found it nearly impossible to match his performance.

However, there’s one area where you could easily emulate Buffett.

I’m talking about collecting a steady income from Dividend Growth Companies.

The irony is that Buffett’s company, Berkshire, maintains a no-dividends policy.

However, a significant portion of his wealth is driven by dividend payouts.

If you start with his favorite sectors, you could enjoy reliable cash flows for decades.

Here are some examples to begin with (payout profiles included).

A Consumer Staple.

Buffett began buying Coca-Cola (KO) stock in 1988.

He accumulated 400 million shares at a total cost of $1.3 billion.

This gave the Oracle a cost basis of roughly $3.25 per share.

At the time, Coca-Cola offered a standard market yield of approximately 3.0%.

If you bought the stock today, you would get a similar yield.

However, Buffett locked in his low purchase price decades ago.

As of 2026, the beverage giant has increased its dividend for 64 consecutive years.

These continuous hikes have driven Buffett’s yield on cost to over 65% annually.

The KO payouts now generate over $800 million in annual dividends for Buffett’s company.

Moral of the story?

You do not need a high starting yield to build lasting wealth.

Instead, just focus on high-quality companies capable of growing their payout year after year.

These are sound companies that tend to do well even during economic downturns.

Their ability to consistently increase payouts is driven by solid business fundamentals.

Some of these are industry dominance, low costs and high profitability.

And while a 3% starting yield may seem small to most investors…

It’s usually a different story when it comes from a world-class Dividend Grower.

Why?

Because over time…

The steady increase in payouts compounds your wealth significantly.

Let me show you another example from Buffett’s portfolio.

Tech Royalties.

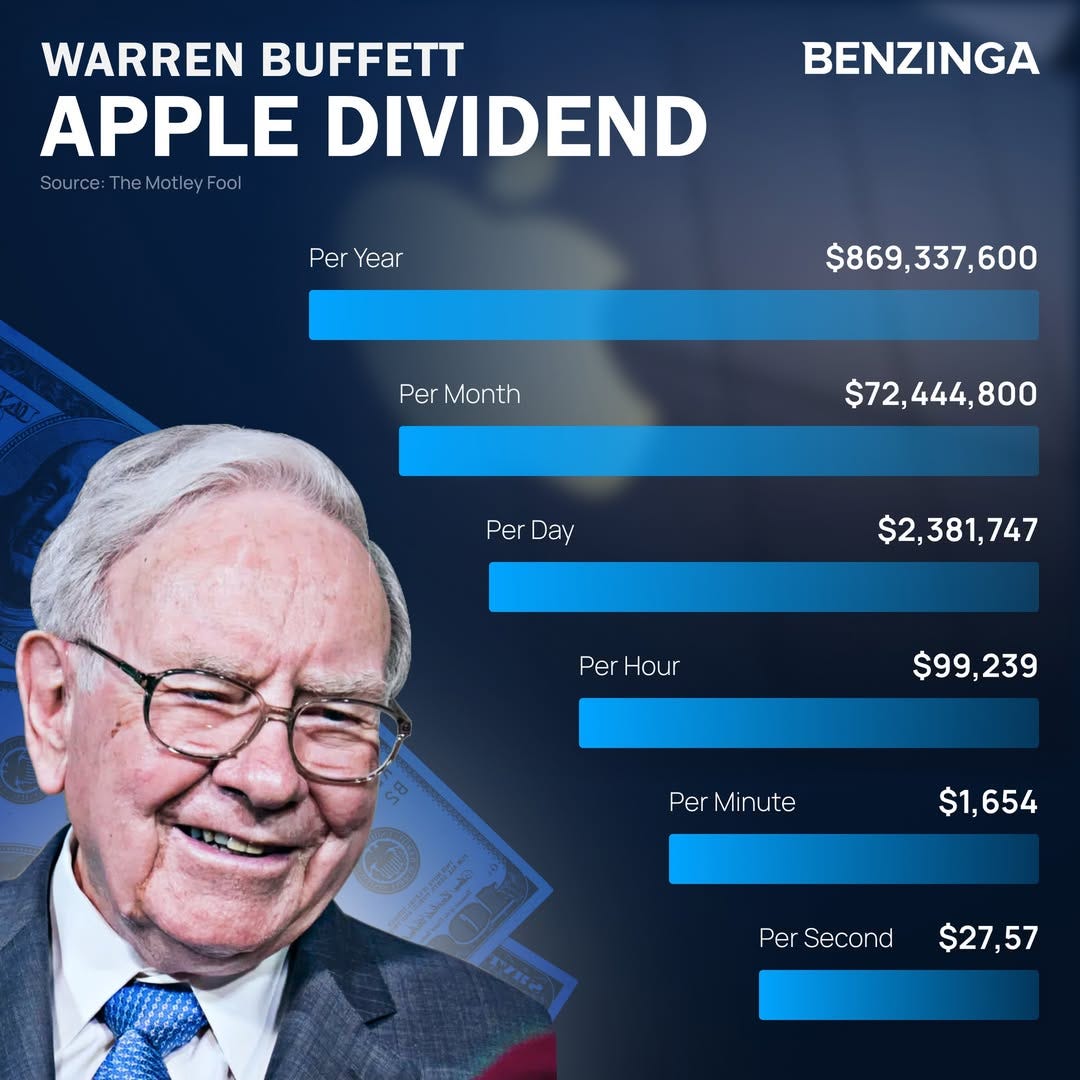

Yahoo Finance published an article with this headline:

You Won’t Believe How Much Money Berkshire Hathaway Gets From Apple Dividends

Let’s look at the numbers.

Buffett initiated Berkshire’s position in Apple in early 2016.

Since then, Apple has consistently increased its payout, resulting in significant dividend growth.

Now, Apple’s current dividend yield is low.

It is around 0.4%–0.5% at current market prices.

However, the yield on Berkshire’s cost basis is much higher.

Berkshire’s average purchase price is around $36 to $40 (split-adjusted).

Apple’s current annual dividend payout is over $1 per share.

So the yield on cost for Buffett and Berkshire is over 2.5%.

The result?

Despite selling a large portion of the stake…

Berkshire still collected roughly $280 million in dividends from Apple in 2025 alone.

Bottomline:

Apple’s yield may seem unimpressive compared to the broader market.

However, two powerful forces make it a top-tier income generator for Berkshire.

Steady dividend growth paired with astronomical capital appreciation.

In addition, Apple aggressively buys back its own stock.

As such, Berkshire’s stake, and its share of the payout, grows automatically.

As an income investor, you should look for smaller, cash-rich companies on a similar trajectory.

A High-Yield Energy Play.

In late 2020, Berkshire began building a major stake in Chevron.

Around this time, the company was navigating the COVID meltdown.

However, its dividend yield was also approaching 8%.

Since then, it has consistently compounded…

Rewarding shareholders with high-yielding income.

In early 2026, the oil and gas giant marked its 36th year of raising dividends.

That’s partly due to two benefits from its acquisition of Hess Corp.

It caused an increase in production and significant cash flow growth.

These factors strengthen the company’s ability to raise dividends.

Further, it continues to maintain a low break-even price of around $50 per barrel.

This allows it to buy back shares aggressively, boosting total value for shareholders.

Over the past five years, Chevron has increased its dividend by 5%–6% per year.

And like Coca-Cola, it remains a key high-yield component of Berkshire’s portfolio.

Now, of course, Coca-Cola, Apple, and Chevron are high-quality stocks.

However, they have drawbacks for income-focused investors.

Coca-Cola has limited growth potential

Apple offers a low dividend yield (often below 0.5%)

And Chevron relies on oil price fluctuations

This can affect its ability to grow its dividend steadily for decades.

A trillion-dollar company like Berkshire Hathaway can afford to wait.

But if you’re an individual investor, there are better opportunities to consider.

My suggestion?

Start with less popular Dividend Growth companies.

Not all of them are as big as Coca-Cola.

But these are sound companies that consistently raise their dividends.

They operate in sectors that outperform during recessions or high inflation.

A good example is a Consumer Discretionary Company we bought in November 2024.

The company has increased its payout for 14 consecutive years.

In the past decade, it has maintained a compound annual growth rate (CAGR) of over 15%.

The 2026 dividend hike also reflects strong free cash flow and attractive shareholder returns.

That’s a good example of a dividend growth company you could rely on.

There are many more like this in our portfolio.

Right now, we own 18 Dividend Growth Companies.

The cash flow has been very steady since we bought them.

And we’re confident they’ll continue to increase dividends over the long term.

If you’d like to see our positions, it’s easy.

Start with a risk-free trial of Compounding Dividends.

The regular subscription fee is $499 for a full year.

But if you act now?

You can get a $100 discount.

This means you pay only $399 annually.

On top of that, your subscription is covered by our money-back guarantee.

Here’s how it works.

If you’re not happy after 90 days, just let me know.

You’ll get a full refund.

That’s how confident I am in Compounding Dividends.

Here’s a summary of what you get when you join us today.

📈 Full access to our Portfolio of Dividend Stocks.

📚 Access to our entire library of data-driven articles.

🔎 New investment cases about interesting Dividend Growers.

As Buffett said, Dividends can make you rich.

But to make it happen, you need to own high-quality dividend stocks.

Our primary objective is to help you find the best of the best.

We’re confident you’ll love our research in Compounding Dividends.

That’s why we’re offering you a 90-day money-back guarantee.

You’ll also get these Exclusive Bonuses.

📘 E-book with one-pagers of all our stocks

📊 Spreadsheet with the dividend growth of the portfolio

🎥 Video course: How to find great dividend stocks

🛒 Report: 3 Dividend Stocks to Buy

⭐ Report: Pieter’s 3 Favorite Stocks

🔍 Report: How to find 100-baggers

💵 10 Dividend Stocks to Own Forever

🏗️ Masterclass: Build Your Dividend Machine

But please note:

This offer expires shortly.

So if you’re interested, don’t wait until it’s too late.

Click here to get started.

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data