Dividends, Buybacks, and the Truth About Capital Allocation

The Iran war seems to be at a stalemate.

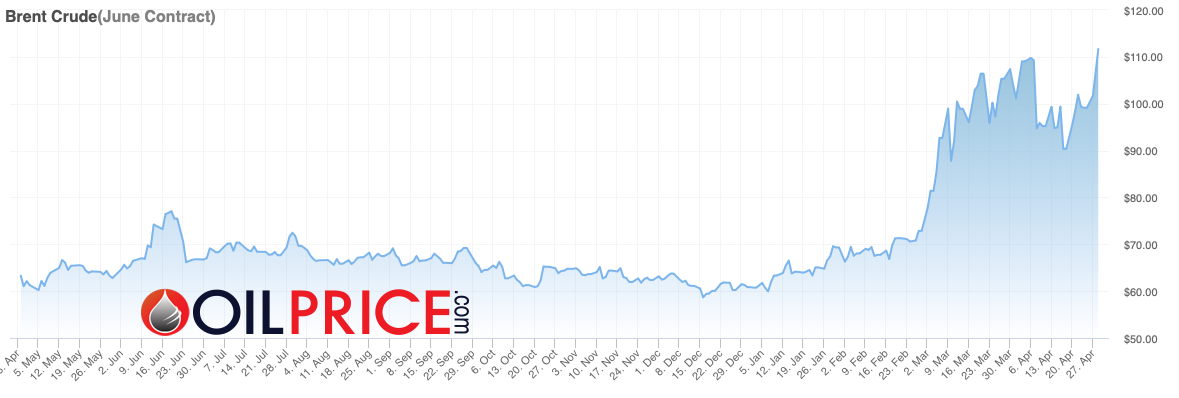

Oil prices are up around 50% compared to a year ago.

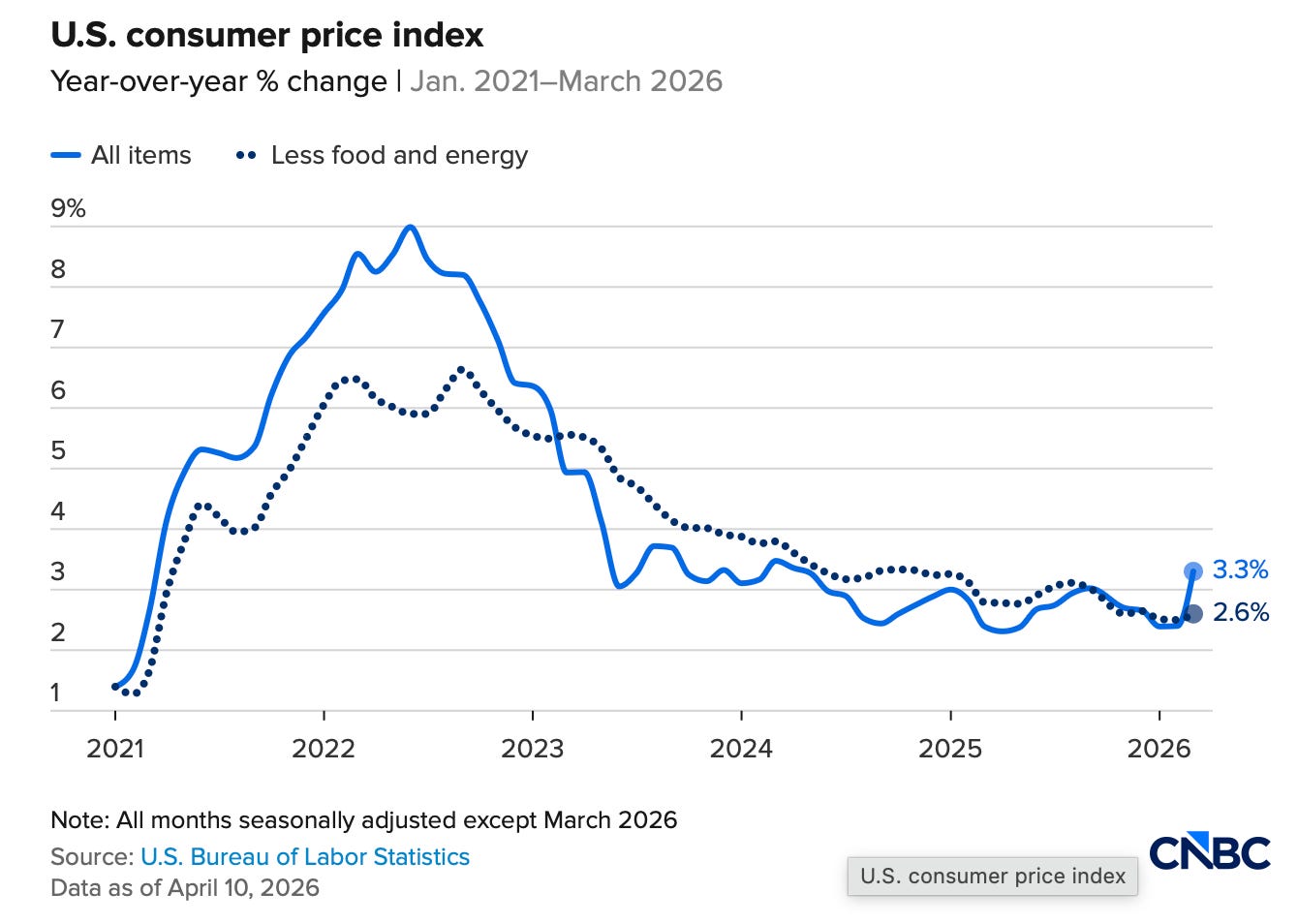

Inflation was up 3.3% in March.

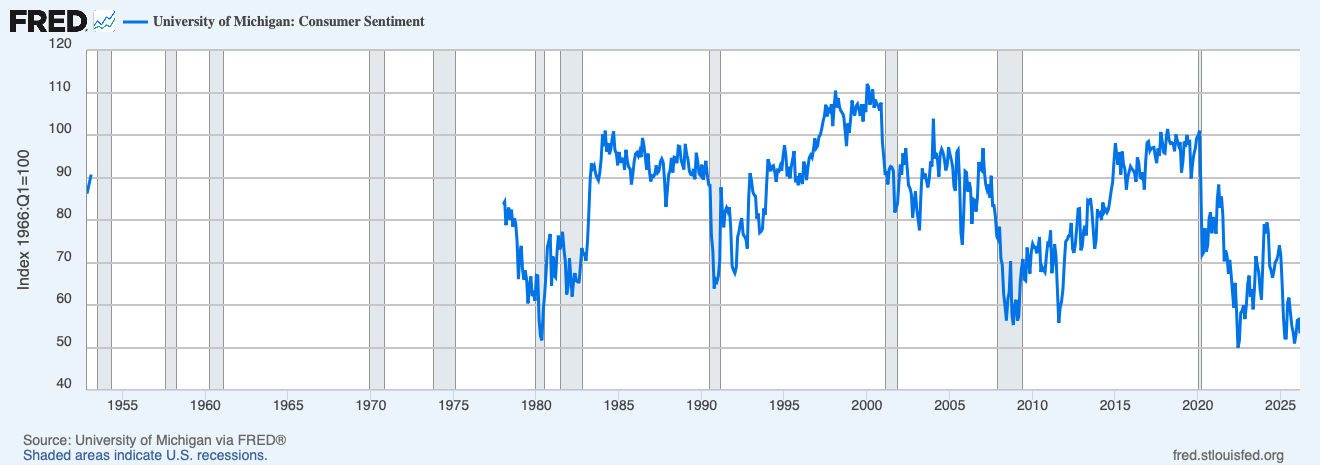

Consumer sentiment is at all time lows.

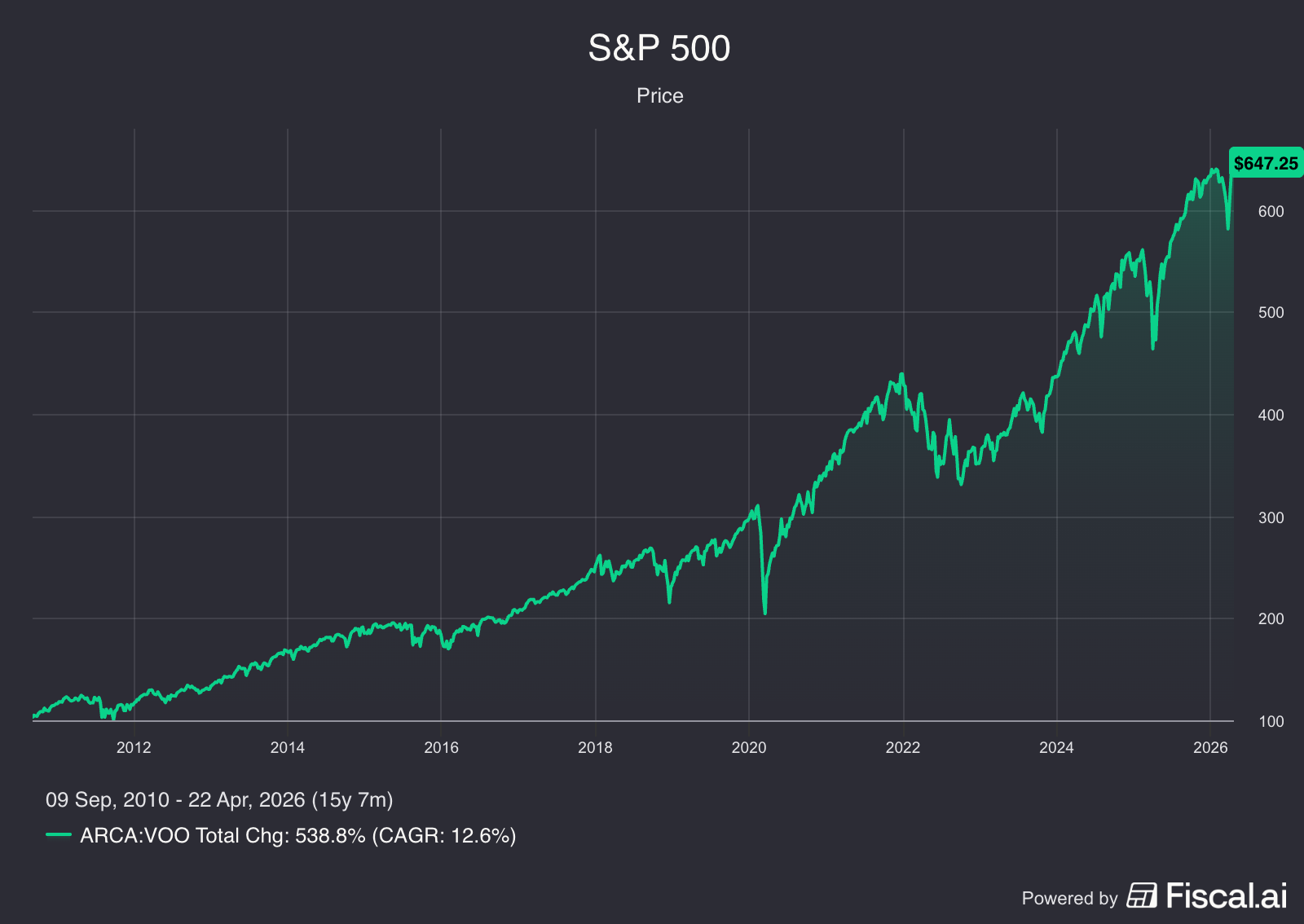

And yet, the S&P 500 is near all time highs.

How can this be?

It seems investors believe that nothing can hurt the mighty U.S. stock market.

And why wouldn’t they?

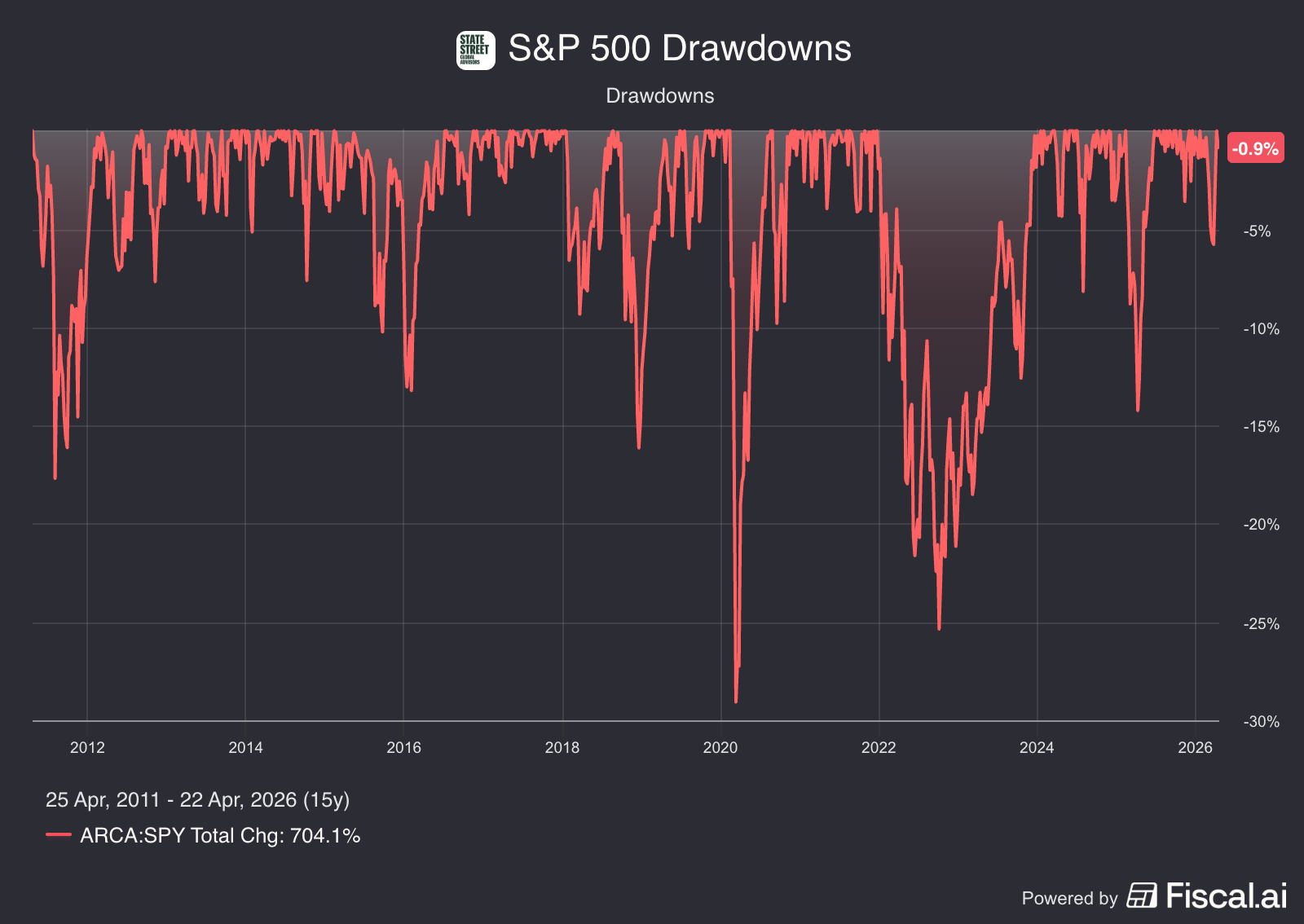

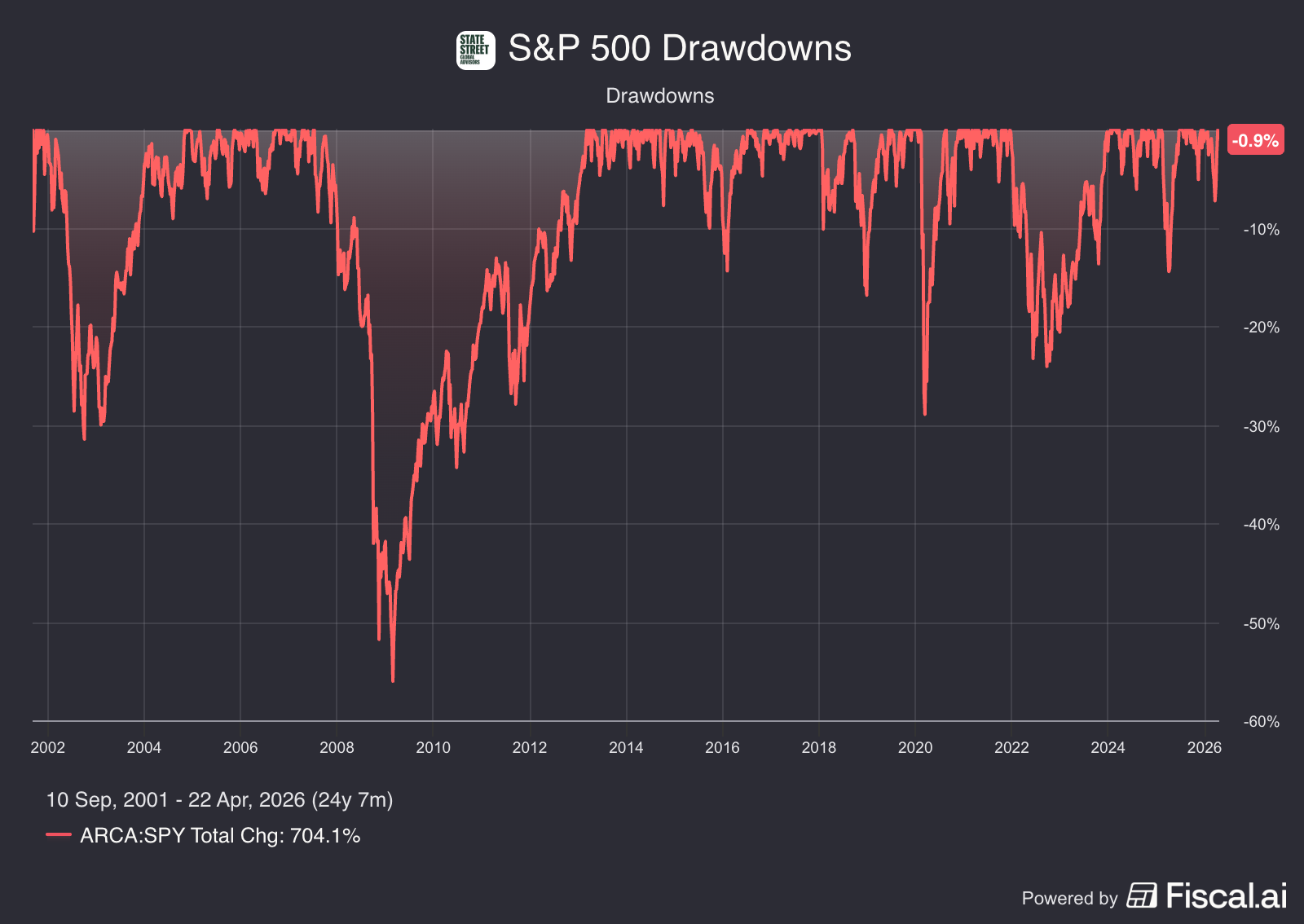

In the last 15 years, the deepest drawdown investors have seen was the Covid crash of 2020.

That lasted a little over a month, then turned into a bull market.

The longest drawdown was 2022, but by the end of 2023, the S&P was back to all-time highs.

But if you’re an older investor, you might remember that the 2007 crash took until 2013 to recover.

The point I’m making isn’t that a big market crash is coming.

(One is, we just have no idea when it’ll happen or what will cause it)

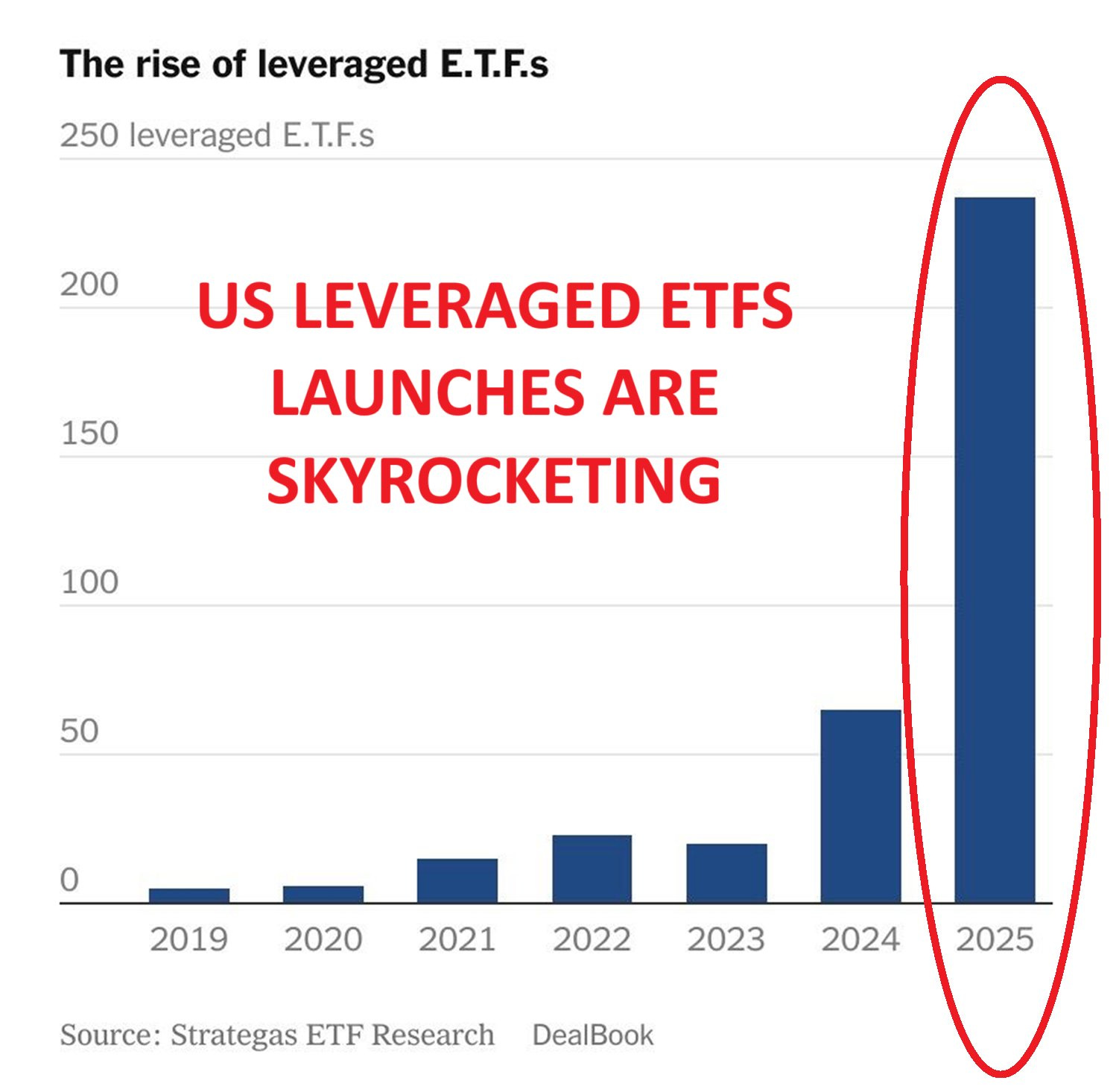

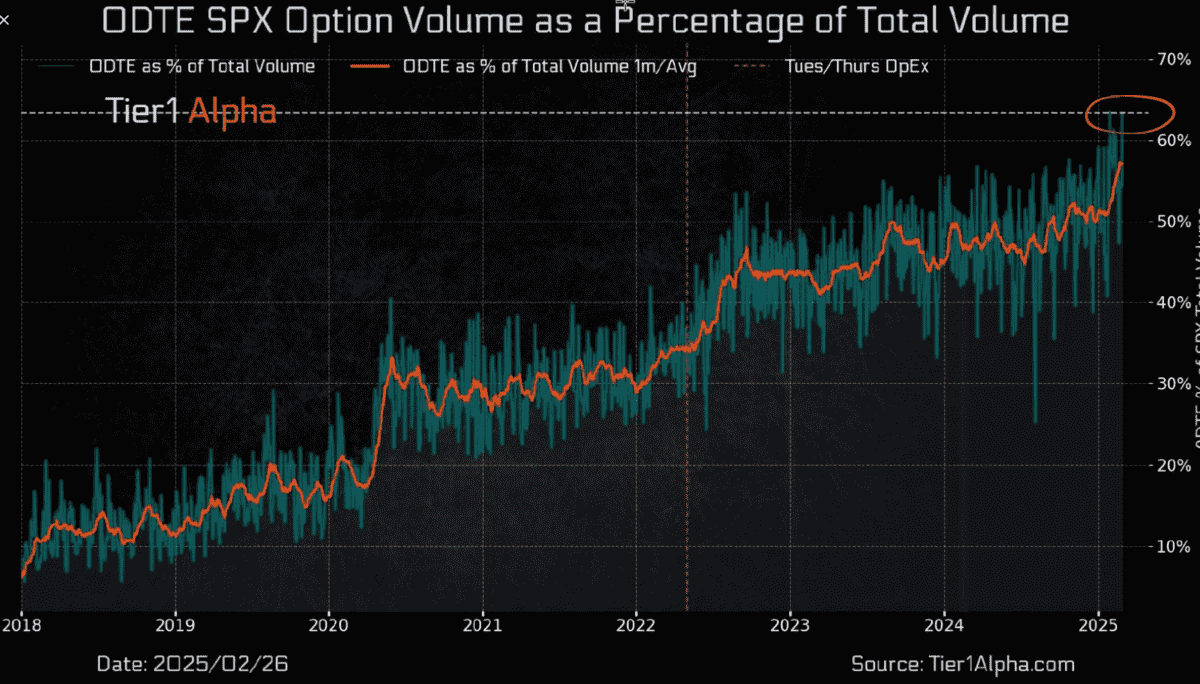

The point is that investors seem more and more willing to take risk.

That’s backed up by some data points like the record number of leveraged ETFs launched in 2025.

The continual rise of 0DTE options contracts.

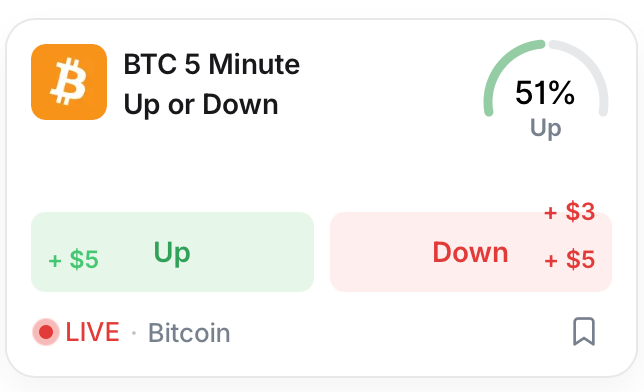

And the ability to bet on if Bitcoin prices will be higher or lower in the next 5 minutes.

In this kind of environment, it’s easy to accidentally slide from investing to gambling.

That means we stop looking at businesses, and start looking at tickers and prices.

So it’s probably a good idea to take a minute to remember what investing is.

Here’s how Warren Buffett described investing in his 2022 letter:

“To make meaningful investments in businesses with both long-lasting favorable economic characteristics and trustworthy managers.”

The emphasis on businesses in the quote above is Buffett’s, not mine.

The best way to buy a stock is the same way you’d buy a local business.

Choose a business that’s been successful and grown in the past

Make sure it’s going to continue growing long into the future

Hire a good manager to handle daily operations

Pay a price based on the cash that you’ll be able to take out of the business over time

I want to spend some time focusing on point #4.

Frozen Corp.

It’s not enough to buy a profitable business.

You need a business that will actually produce some cash for you.

Benjamin Graham used to illustrate this in his class at Columbia by asking the students to value ‘Frozen Corporation’.

It was a company whose charter prohibited it from ever paying anything to its owners, ever being liquidated, or ever being sold.

If a business doesn’t ever produce any cash for its owners, it’s not worth anything.

Which is of course why we focus on the cash a business returns to its shareholders.

It’s generally accepted that a business can do this in two ways.

Pay dividends

Buy back shares

Dividends are pretty straightforward - the company makes profits, and pays you in cash.

It can be argued whether that dollar could have been used better elsewhere - reinvested in the company, used in an acquisition, or paying down debt.

What can’t be argued is that if the dividend is $1, you get $1.

Buybacks are simple to understand in theory - the company spends money to reduce the shares outstanding.

That means that each remaining share represents a larger portion of the company and should be worth more.

But in practice, they’re more complicated.

If a company spends $1 on a buyback, how much value did you get?

That depends on a few things.

Was the stock undervalued?

Did the buyback reduce share count, or just clean up stock based compensation?

And of course, we still have that opportunity cost problem, where the money may have been better spent elsewhere.

So it’s entirely possible for a company to spend money on buybacks and have no value actually accrue to the shareholders.

Not All Buybacks Are Good Buybacks

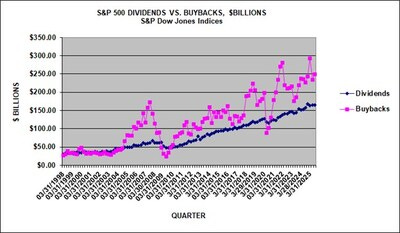

As it’s the case that since 2010 or so, companies have been spending more and more on buybacks, we should look deeper into whether all that money has been put to good use.

Unfortunately, the track record here is pretty terrible.

Christopher Bloomstran from Semper Augustus Capital wrote about buybacks in his letter to shareholders this year.

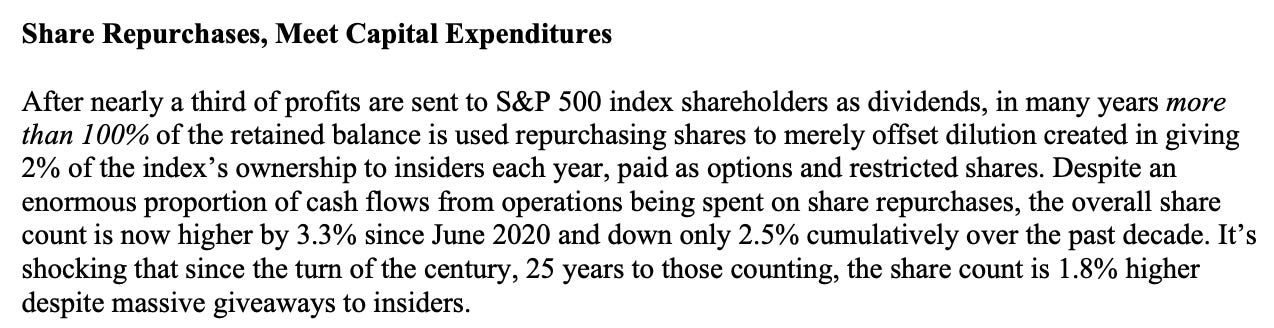

That’s right, despite massive amounts of capital being spent on buybacks, the companies that make up the S&P 500 index have more shares outstanding today than they did 25 years ago.

To add insult to injury, as more and more was spent on buybacks, the cash was buying increasingly expensive stock.

So on average, buybacks were done at high prices and didn’t reduce share count.

As a shareholder, did they create any value?

Or did you simply buy a slice of the ‘Frozen Corporation’.

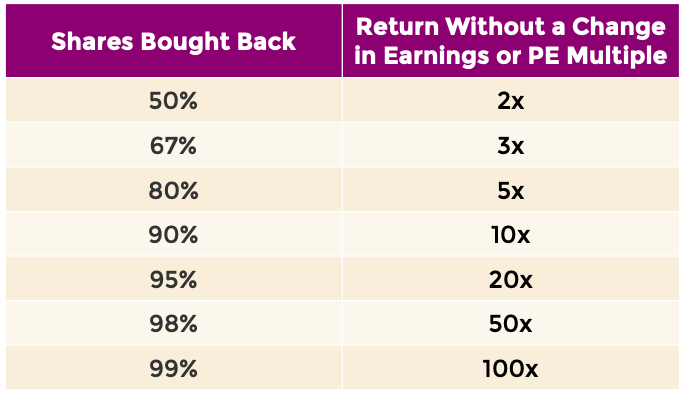

Don’t get me wrong, buybacks can be an amazing capital allocation tool.

But for buybacks to work, they have to:

Be done at valuations below intrinsic value

Meaningfully reduce the share count

When used correctly, here’s the kind of returns buybacks can achieve:

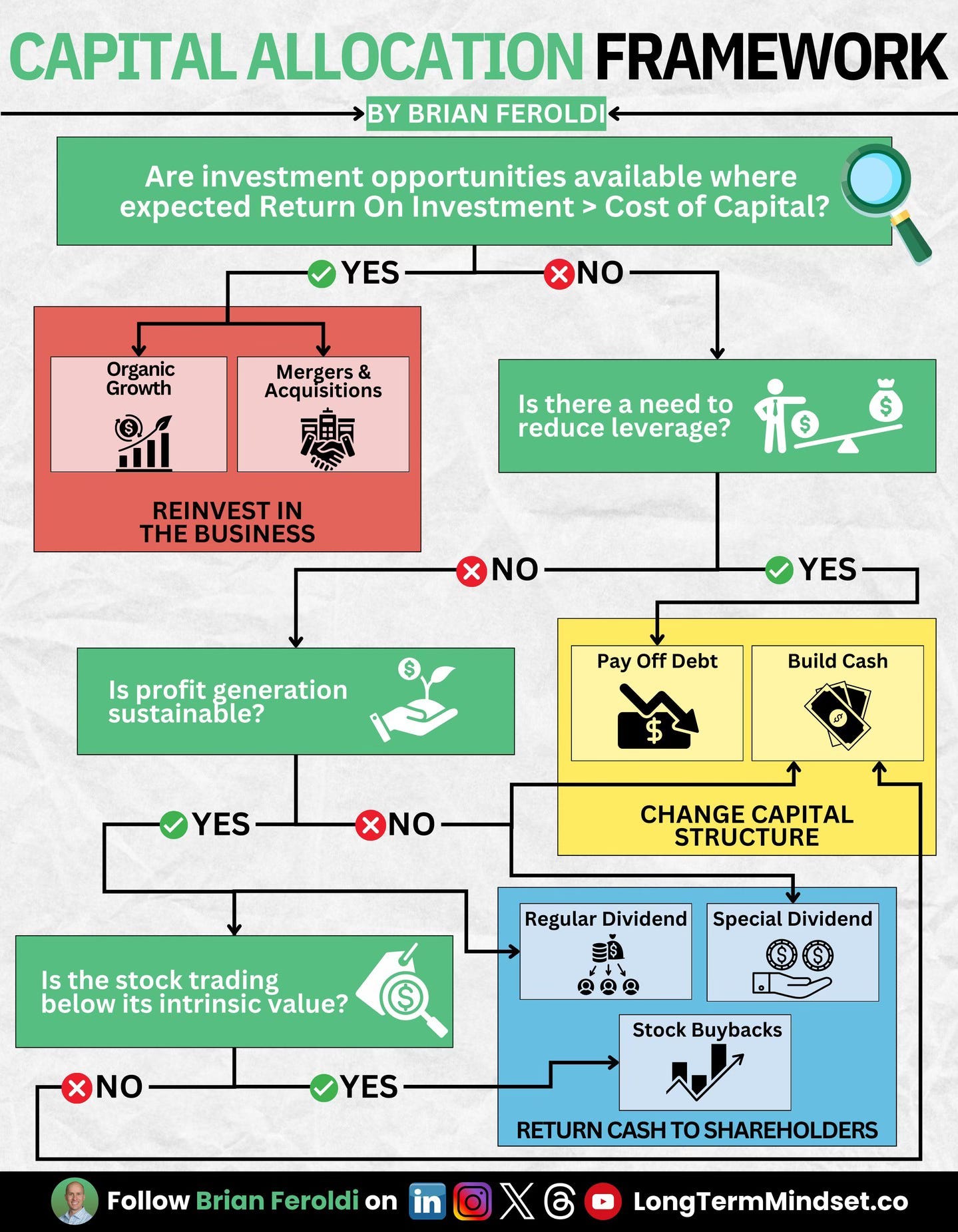

That’s why it’s important to do your research, understand the business you’re buying and understand how the management team thinks about capital allocation.

This great visual by Brian Feroldi shows how a good management team thinks about it.

Notice that buybacks should only happen when:

Reinvestment opportunities have been taken advantage of

The balance sheet is taken care of

The profits are sustainable

The stock is trading below its intrinsic value

Buybacks Done Right

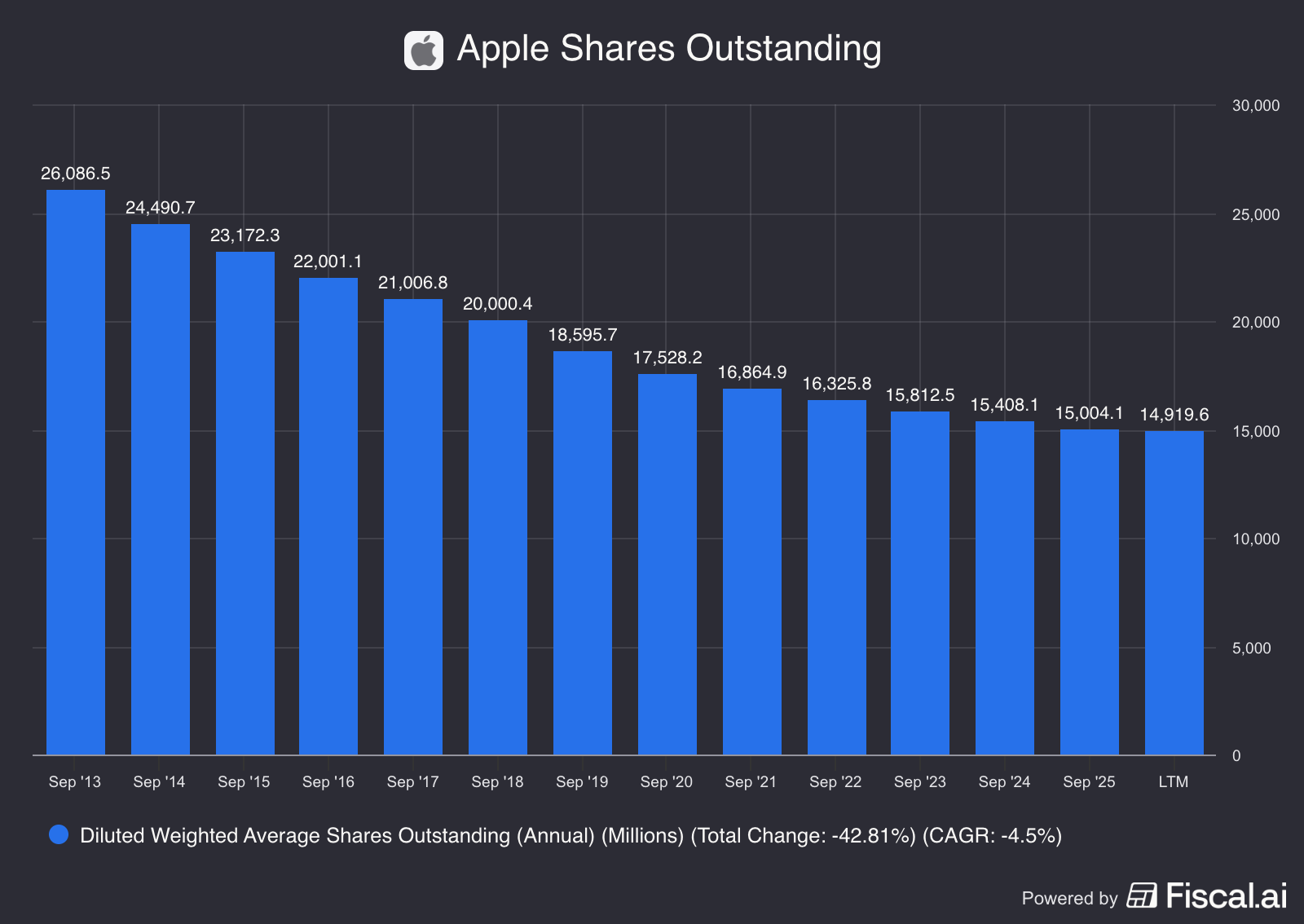

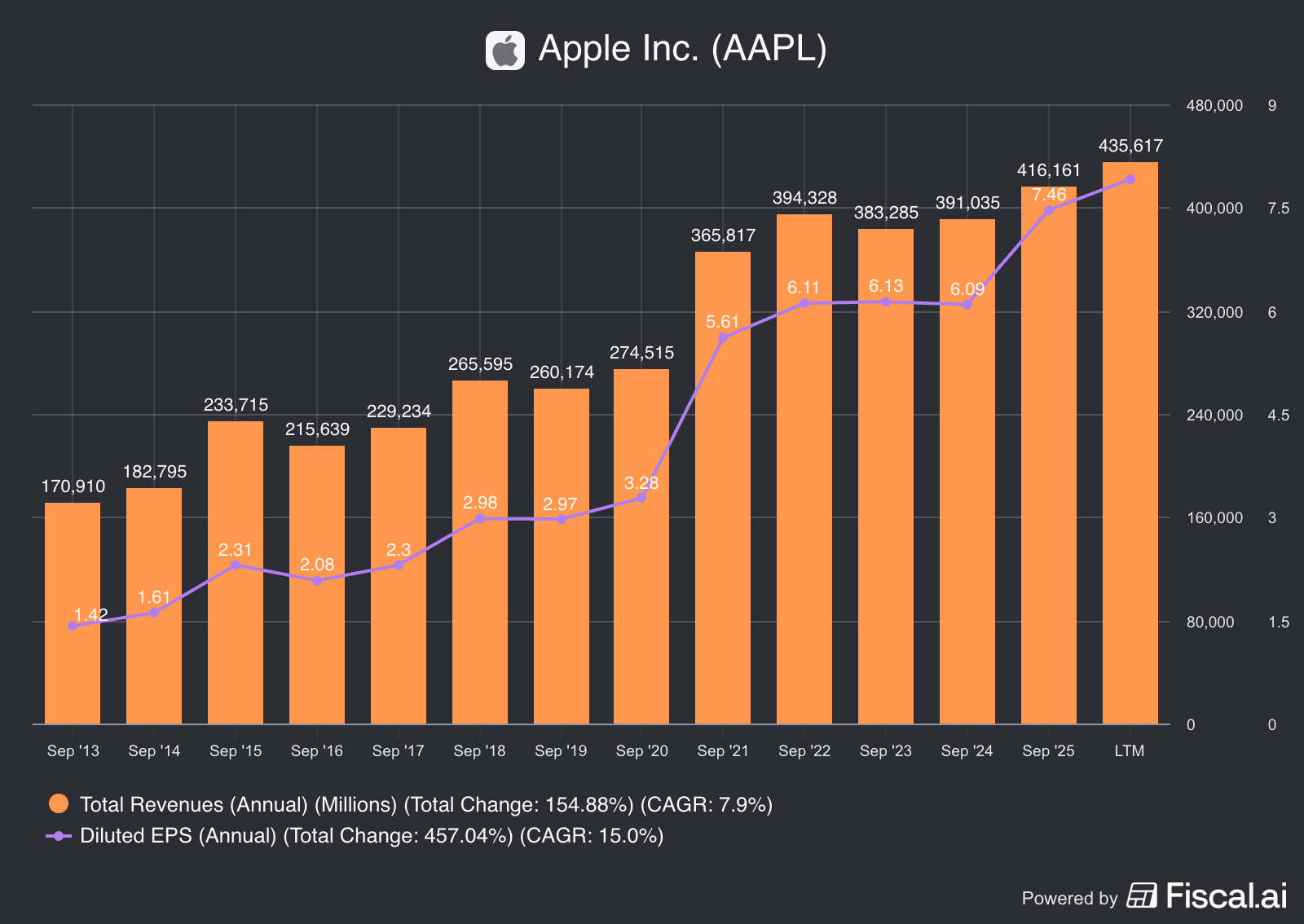

Apple is an example of a company that’s done buybacks well.

Since beginning its buyback program in 2014, Apple has reduced the share count by more than 40%.

That’s how Apple’s EPS has grown nearly 2x as fast as revenue.

Now let’s look at a company that’s ‘returned’ a lot of capital to shareholders through buybacks.

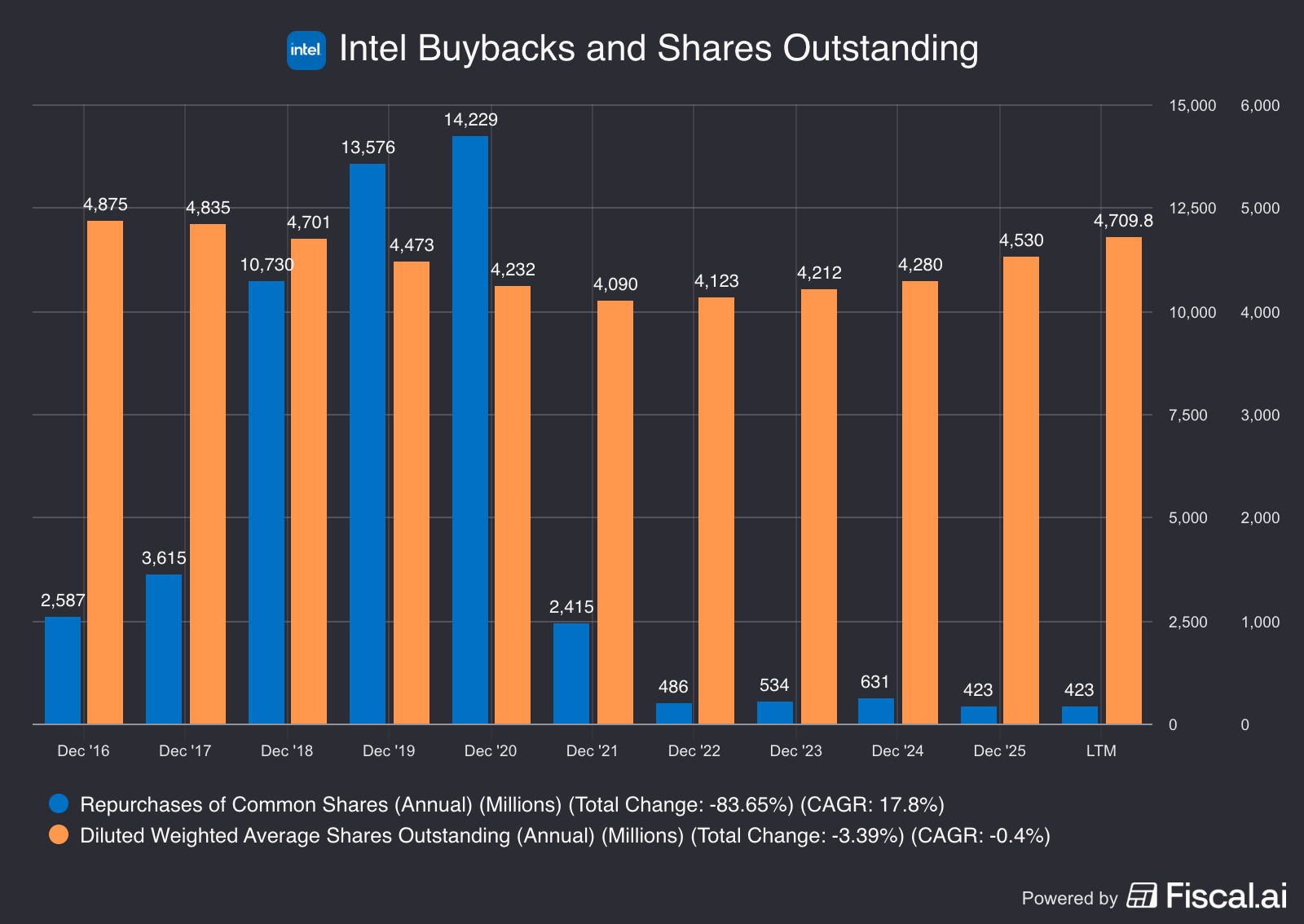

Buybacks Done Wrong

Over the past decade, Intel has spent nearly $35.5 billion on share repurchases.

And for all that money they’ve reduce the share count…

3.4%.

Don’t buy Frozen Corporation.

We’ve got a list of companies that have a history of meaningful share reduction in the cannibal tab on our Buy-Hold-Sell list.

If you’re not yet a Partner, you can join us here and get access:

One Dividend At A Time

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.

Hi TJ. Have you considered PMI for the Compounding Dividends portfolio? Do you perhaps have any information on PMI’s valuation, etc? Regards, Paul