Guide to Closed End Funds

Simplifying CEFs

Something special is happening on June 23rd.

If you want behind-the-scenes updates and early access to our upcoming high-yield reports, join the High-Yield VIP List by leaving your email here.

Closed end funds are interesting because of their high yields and because they often let you buy a basket of stocks or bonds at a discount to their true value.

But what exactly is a closed end fund, and how do you pick the right ones?

Let’s teach you everything you need to know.

What is a Closed End Fund?

A closed end fund is similar to a mutual fund.

A mutual fund is a pool of money where many investors put money together, and the fund manager invests it in things like stocks or bonds

A closed-end fund works similarly because it also owns a collection of investments, such as bonds, dividend-paying stocks, or other assets

But there’s one big difference.

A mutual fund keeps creating new units when people invest and removes units when people withdraw money.

Each unit gets priced at the end of the day, based on the value of the assets within the mutual fund.

A closed-end fund does not do that.

It creates a fixed number of shares at the beginning through an IPO (Initial Public Offering).

After that, those shares trade on the stock market like regular stocks.

So when you buy a closed-end fund, you are buying shares from another investor, not directly from the fund itself.

Because of this, the share price moves based on supply and demand, which means it can trade above or below the actual value of the investments inside the fund.

How Do Closed End Funds Make Money?

A closed-end fund does not make money like a normal company that sells products or services.

Instead, investors earn returns in three main ways.

1. Income From Investments

The fund owns investments like bonds and dividend-paying stocks.

These investments generate income through:

Interest from bonds

Dividends from stocks

After expenses are paid, the fund distributes this income to shareholders.

2. Capital Gains

If the fund buys an investment at a lower price and later sells it at a higher price, the profit is called a capital gain.

Some of these profits may also be paid out to investors.

3. Discount Narrowing

This is one of the most unique features of closed-end funds.

Sometimes the fund’s shares trade below the value of the investments it owns.

For example:

Imagine the fund owns $1 worth of assets

But the market price is only 90 cents

That means you are buying $1 of assets for 90 cents.

If the discount later becomes smaller, your investment gains extra value even if the underlying investments do not change.

Why Investors Like Closed End Funds

Investors tend to like Closed End Funds due to the following reasons:

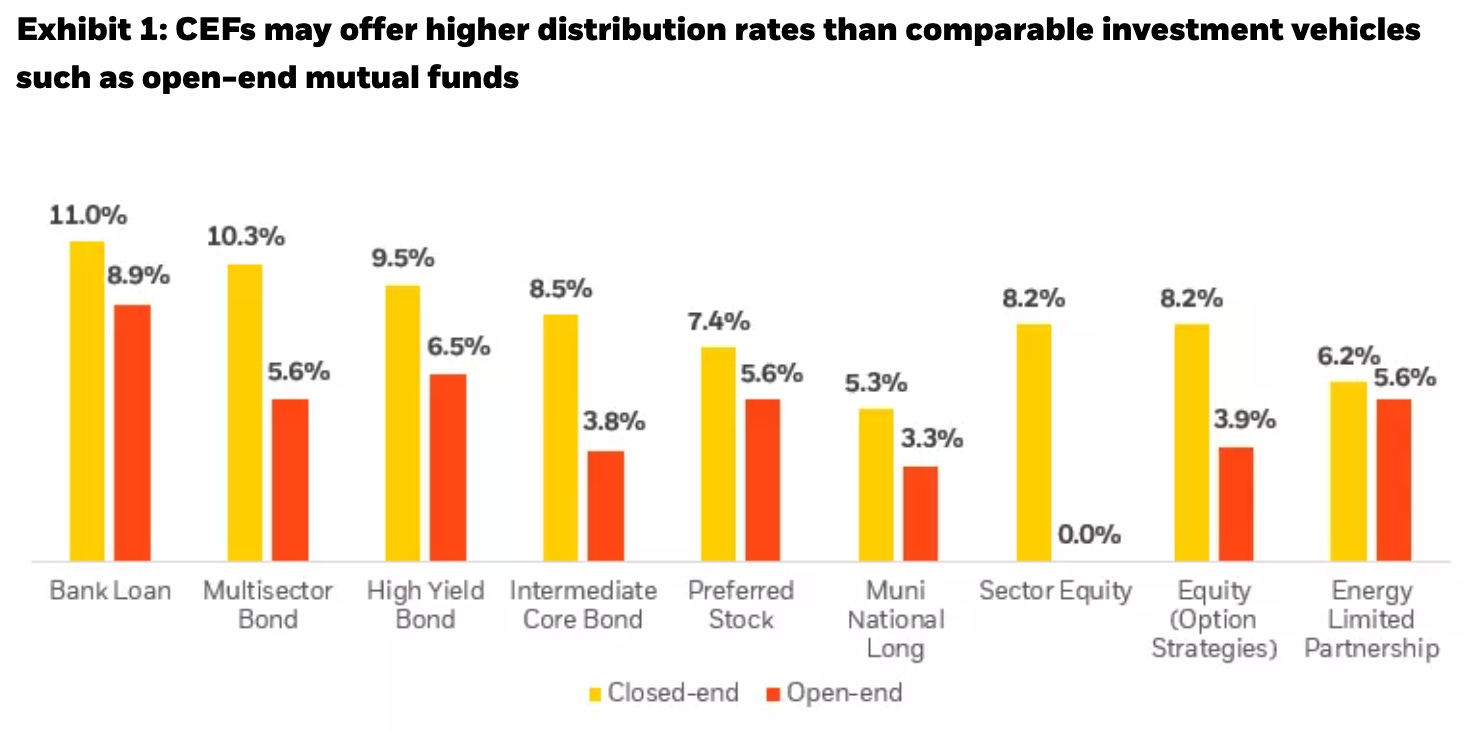

High distribution yields

Because closed end funds can use borrowed money and buy higher yielding assets, their payouts are often much larger than ordinary mutual funds.

Discount to net asset value

You can sometimes buy 1 dollar of assets for 90 or 85 cents. That gives you a margin of safety.

Leverage

When borrowing costs are low, a fund can borrow cheap money and buy bonds that pay a higher yield. The extra income goes to shareholders.

No forced selling

Mutual funds must hold cash to meet redemptions. Closed end funds do not. Their managers can stay fully invested, even in less liquid assets that offer higher returns.

Intra day liquidity

Unlike a mutual fund, you can sell your shares at any time during market hours.

Types of Assets Closed End Funds Hold

What a closed-end fund owns plays a big role in determining its risk and potential returns.

Different funds invest in different types of assets:

Taxable Bond Funds – Invest in corporate bonds, high-yield bonds, and bank loans. These usually focus on generating income.

Municipal Bond Funds – Invest in state and local government debt. The income from these funds is often tax-free.

Equity Funds – Hold investments such as dividend-paying stocks, preferred shares, REITs, and utility companies.

Multi-Asset Funds – Own a mix of stocks, bonds, and sometimes options to create a more balanced portfolio.

One important concept to understand is leverage.

Leverage means the fund borrows extra money to buy more investments.

This can increase returns, but it also increases risk.

If the investments rise in value, a leveraged fund can gain more than a regular fund.

But if the investments fall, losses can also become larger.

For example, the BlackRock Enhanced Equity Dividend Fund holds:

Around 60% large-cap U.S. dividend stocks

Around 20% international stocks

Around 10% preferred shares

Around 10% convertible bonds

Uses roughly 22% leverage

This shows how a closed-end fund can combine different investments while using leverage to potentially boost returns.

Analyzing a Closed End Fund

Closed-end funds are analyzed a little differently from regular stocks.

Here are the key things to understand.

1. Net Asset Value (NAV)

NAV stands for Net Asset Value. It represents the actual value of everything the fund owns after subtracting its debts.

In simple words, NAV tells you the fund’s true value per share.

NAV is usually calculated once every day after the market closes.

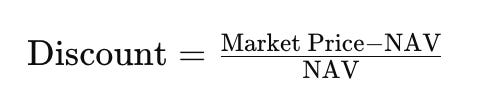

2. Market Price vs NAV

The market price is the price investors actually pay to buy shares on the stock exchange.

This price can be different from NAV.

The difference between the two is called a discount or a premium.

A negative number = discount

A positive number = premium

Example:

NAV = $20

Market price = $18

The fund is trading at a 10% discount.

This means you are buying $20 worth of assets for only $18.

Buying at a discount is often attractive because you are paying less than the value of the assets.

Buying at a premium can be riskier because that premium can disappear quickly if investor sentiment changes.

3. Distribution Yield vs NAV Yield

Closed-end funds have two important yield measures.

Market Yield

This shows what you actually earn based on the price you paid.

NAV Yield

This shows the yield based on the value of the underlying assets.

Imagine a fund has:

Market yield = 9%

NAV yield = 7%

This means that the fund is trading at a discount to NAV, meaning you can buy a larger income stream.

Where Do Distributions Come From?

This is one of the most misunderstood parts of closed-end fund investing.

When a fund pays a distribution, the money can come from three different sources:

1. Net Investment Income

This comes from the income generated by the fund’s investments.

Examples include:

Interest from bonds

Dividends from stocks

This is usually the most reliable and sustainable source of distributions.

2. Capital Gains

This comes from profits made when the fund sells investments at a higher price than it originally paid.

This can support distributions, but it may not happen consistently because market conditions change.

3. Return of Capital

This happens when the fund gives investors back part of their own money.

This can be a warning sign, especially if it happens repeatedly.

If a fund keeps paying return of capital while its NAV keeps falling, it may be slowly shrinking or “paying itself away.”

But not all Return of Capital (ROC) is bad.

It can be a very clever tax-saving strategy.

Funds buy and sell hundreds of assets.

Smart fund managers will purposefully sell certain assets at a loss to offset their winning trades.

By doing this aggressively, they can legally reclassify the cash they pay you from Capital Gains into Return of Capital.

Here’s how:

Imagine a Closed-End Fund (CEF) needs to pay out a $2 million distribution to its shareholders. The fund’s portfolio has a mix of winners and losers:

ABC: Sitting on massive profits.

DEF: Sitting on smaller profits.

XYZ & GHI: Currently sitting at a loss, but the fund managers still believe in their future potential.

If the fund simply sells its winning ABC stock to pay the $2 million dividend, that triggers a taxable capital gain.

To prevent that, the fund manager uses a combination of trades to zero out the tax liability.

Take the profit: The manager sells a portion of ABC stock, raising $8 million in cash. This sale realizes a $3 million profit.

Harvest the loss: To offset that profit, the manager sells some XYZ stock, raising $5 million in cash and intentionally realizing a $3 million loss.

Reallocate: The manager immediately takes $2 million of that cash and invests it into DEF and GHI to capitalize on their growth potential.

Because the fund perfectly offset its $3 million profit with a $3 million loss, it has zero net capital gains on paper.

This is known as Tax Loss Harvesting.

When the fund distributes the $2 million to you, the IRS considers it a Return of Capital rather than a taxable profit.

You get your dividend without the immediate tax bill.

How to Check if a Distribution Is Safe

Not every high distribution is a good distribution.

A fund may offer an attractive yield, but the important question is:

Can it keep paying it?

Here are a few things to look for in a healthy closed-end fund:

Net investment income + capital gains should cover the distribution.

Ideally, the fund should generate more money than it pays out.Coverage above 100% is a good sign

If there’s return of capital, ask why?

If the fund is just handing you back your own cash, that’s a warning sign. If it’s a tax strategy like we talked about above, it might be ok.NAV should be stable or growing over time.

Check the fund’s NAV over the last 3–5 years.A stable or rising NAV suggests the fund is creating value. A falling NAV may indicate the fund is struggling to support its payouts.

For example, BlackRock Science and Technology Trust reported:

Net investment income + realized gains: $3.10 per share

Distributions paid: $2.80 per share

That means the fund generated more than it paid out.

Coverage was 111%, which suggests the distribution was well supported and safe.

Leverage

More than 70% of closed-end funds use leverage, which simply means borrowing money to buy more investments.

Funds may borrow through loans or issue preferred shares to increase the amount they can invest.

The goal is simple: use extra money to generate higher returns.

But leverage works both ways.

If investments go up, gains become larger.

If investments fall, losses also become larger.

A common measure is the leverage ratio:

For example:

A 30% leverage ratio means for every $1 of investor money, the fund borrows 30 cents and invests $1.30.

What to Check

Borrowing cost

How much interest is the fund paying? Higher interest rates can reduce profits.Type of debt

Fixed-rate borrowing is generally more stable. Variable-rate borrowing can become expensive if rates rise.Asset coverage

This measures whether the fund has enough assets to support its debt. Higher coverage provides a larger safety cushion.

A well-managed fund should keep borrowing costs under control so that most investment income still goes to shareholders.

Fees

Closed-end funds have expenses, and these usually come from two sources:

Management and operating fees

These cover portfolio management and administrative costs.Interest expense

This is the cost of borrowing money for leverage.

Because leveraged funds use debt, their expense ratios can sometimes appear higher than expected.

Do not judge a fund by the number alone.

Always compare it with similar funds in the same category.

Discount History and Z-Score

A fund trading at a discount may look cheap, but not always.

Imagine a fund trades at a 12% discount today.

That sounds attractive.

But if its average discount over the last five years was 14%, the fund is actually trading more expensively than usual.

This is where the Z-score helps.

The Z-score compares today’s discount with the fund’s historical average.

Z-score below -2 → Discount is unusually large and could signal an opportunity.

Z-score above +2 → Discount is unusually small or the fund trades at a premium. This can be a warning sign.

The Z-score helps investors understand whether a fund is cheap or expensive relative to its own history.

Looking at the Capital Structure

Many closed-end funds issue debt or preferred shares.

As a common shareholder, you want to make sure there is enough protection if markets become volatile.

A useful measure is the asset coverage ratio:

Higher asset coverage generally means lower risk.

Conclusion

Investing in closed end funds can seem confusing if you are used to simple ETFs or mutual funds.

But once you understand NAV, discounts, distribution sources, and leverage, a closed end fund becomes just another tool in your income toolbox.

Here is why you may want to consider closed end funds in your portfolio:

High current income – Yields of 6 to 10 percent are common. That is much higher than ordinary bond funds.

Opportunity to buy at a discount – You can buy assets for less than they are worth.

Professional leverage management – Most investors cannot borrow at institutional rates. Closed end funds can.

Access to less liquid assets – Like municipal bonds or middle market loans, without locking up your money for years.

Liquidity – Buy and sell any trading day, unlike private funds.

Just remember that not all closed end funds are the same.

Always check:

Distribution source: Make sure you understand where your distributions come from and if they’re sustainable

Distribution coverage: Look for Net Investment Income and capital gains to be covering the distribution (remember that the capital gains may be classified as ROC if the manager is using Tax Loss Harvesting)

Leverage: Make sure it’s conservative, with low borrowing costs

Portfolio: Look for high-quality, well-diversified holdings

One Dividend At A Time

TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

P.S.

On June 23rd, we are kicking off a series all about high yield investing.

If you want to maximize your portfolio's income without sacrificing business quality, jump on the VIP Waitlist.

You'll get behind-the-scenes updates and the very first invite to download our brand-new high-yield special reports the minute we go live.

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.

Fund management is where strategy meets execution. Thanks for sharing your perspective.

Thanks very much for this. I've been watching ADX and CET (v.s. Berkshire) as my "buy after a crash" stocks.