💸 Is Big Tech Burning Cash?

AI is already changing our world.

But that doesn’t mean the companies building it will make you money.

I’ve been thinking a lot about how big tech’s spending on AI is changing their business models, and what the implications could be.

The Mag 7 were wonderful businesses

Many of the businesses in the Magnificent 7 have been historically wonderful businesses.

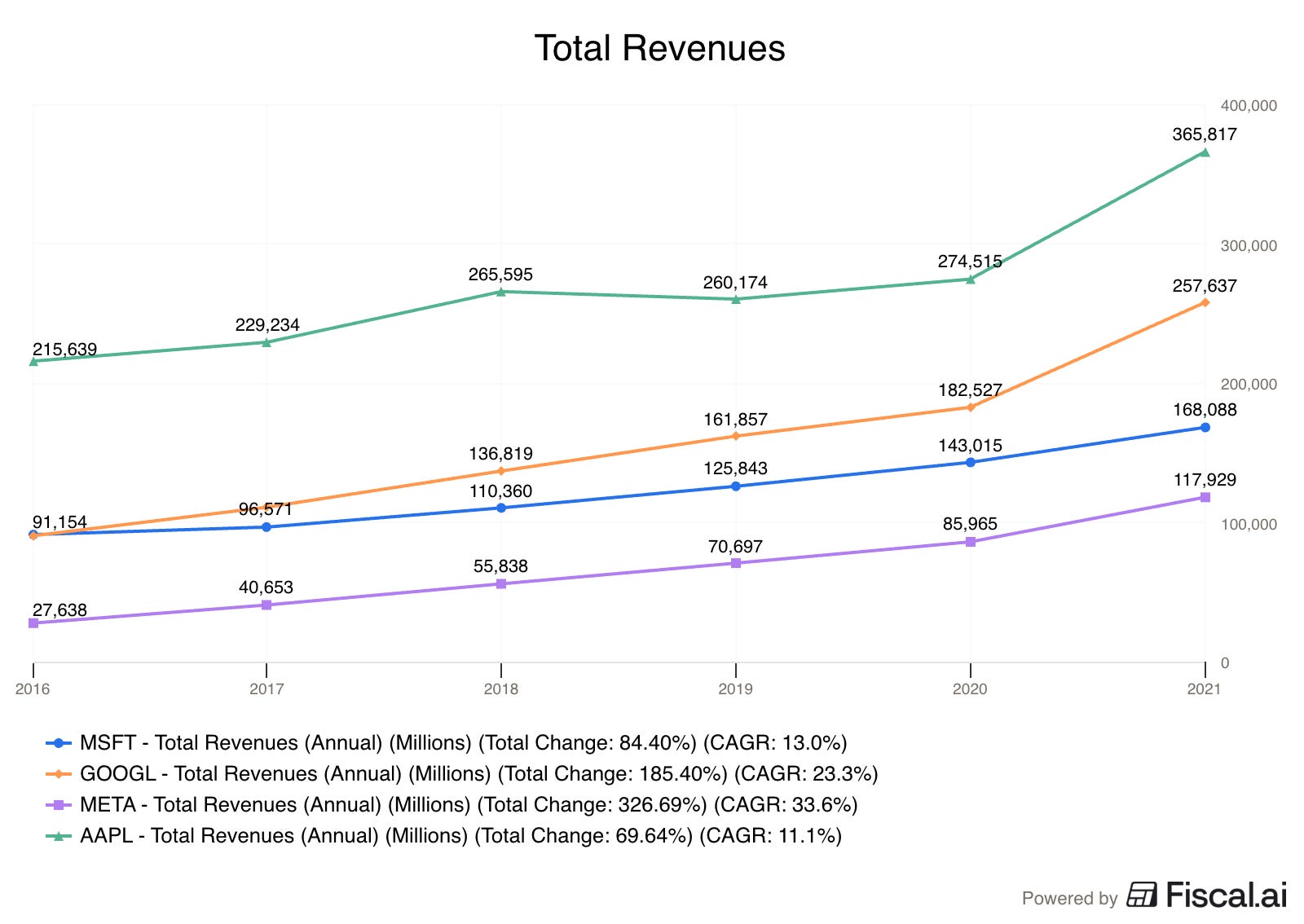

They’ve steadily grown revenue at very attractive rates:

Meta is the fastest here with a 33% CAGR

Apple is the laggard at a still attractive 11%

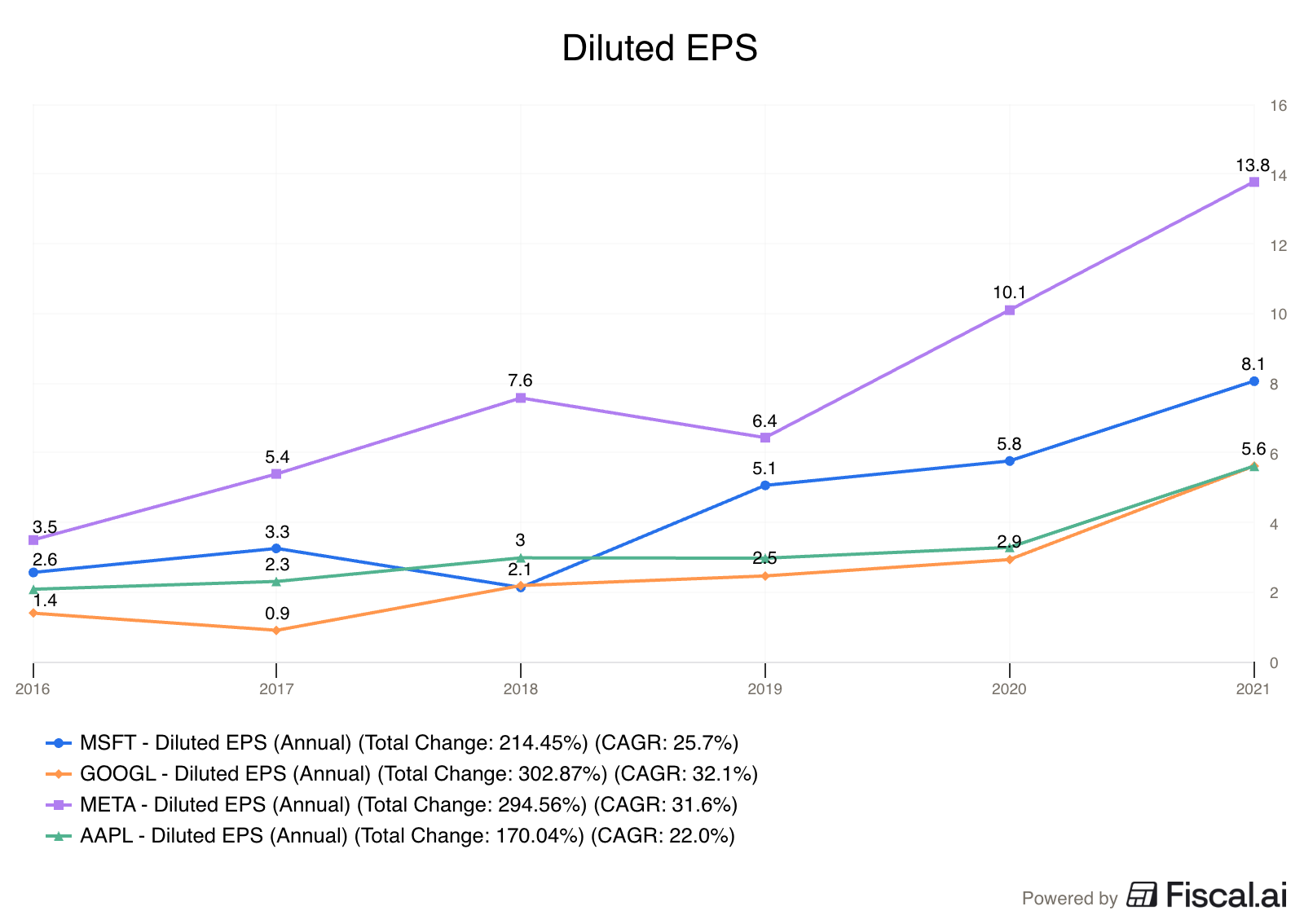

They’ve grown their profits just as fast.

Google leads here at 32% (!) per year

Apple is again the slowest at 22% per year

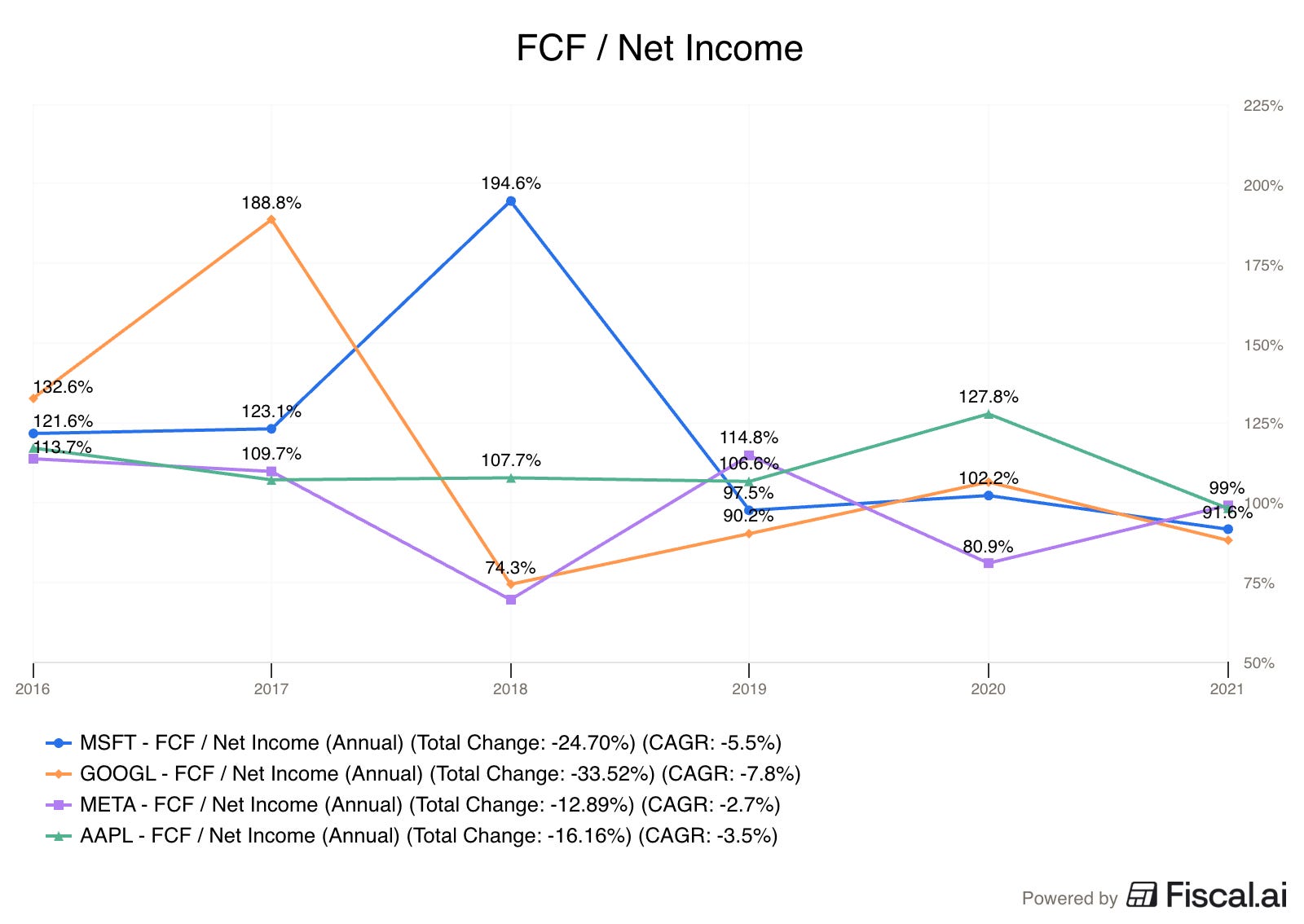

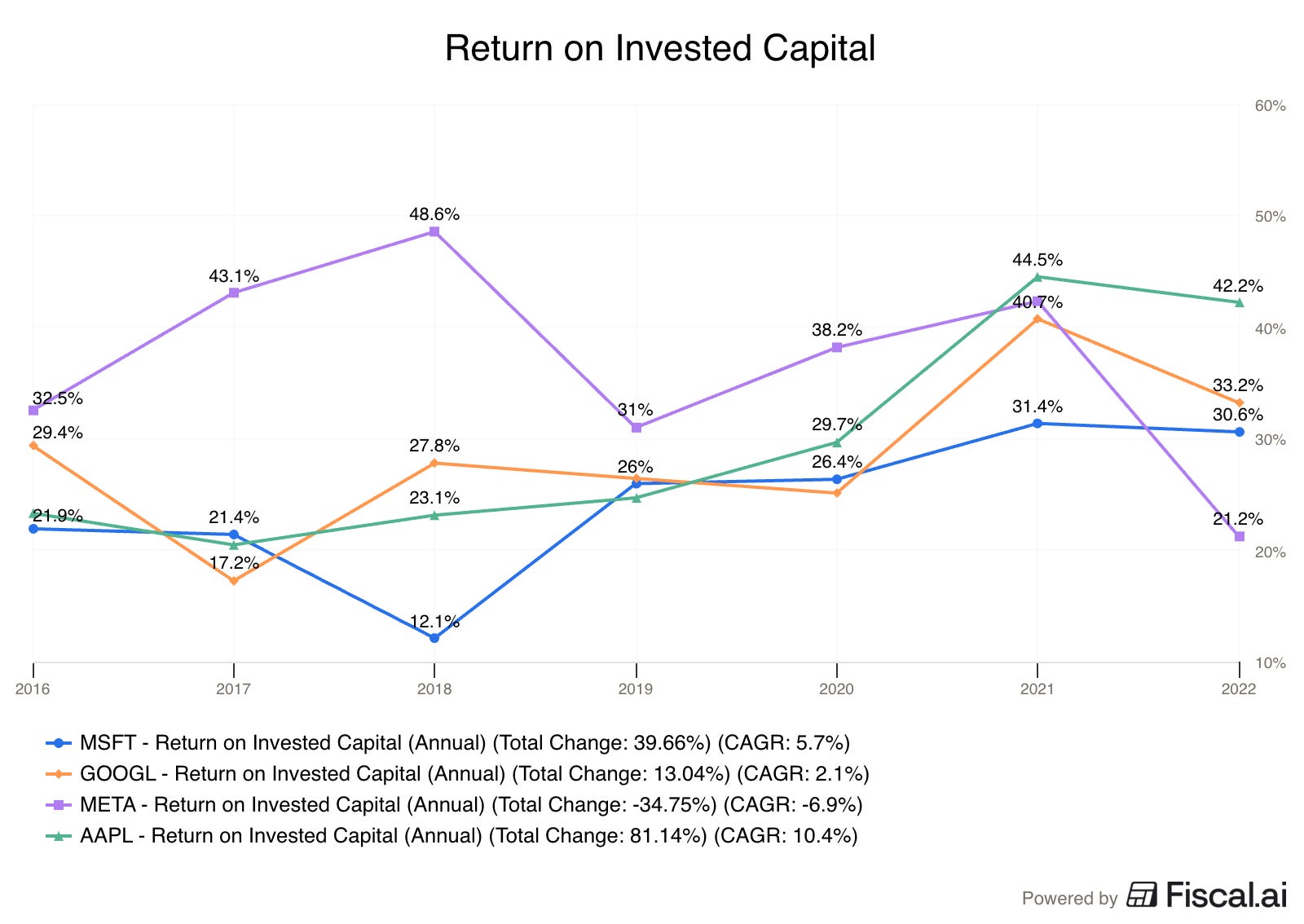

Nearly all of that profit has historically been turned into cash.

They’ve been capital light businesses.

That management has been able to reinvest in at high rates of return.

It’s no wonder they became called Magnificent.

It’s a much better name than the old one - remember FAANG?

They Rewarded Shareholders

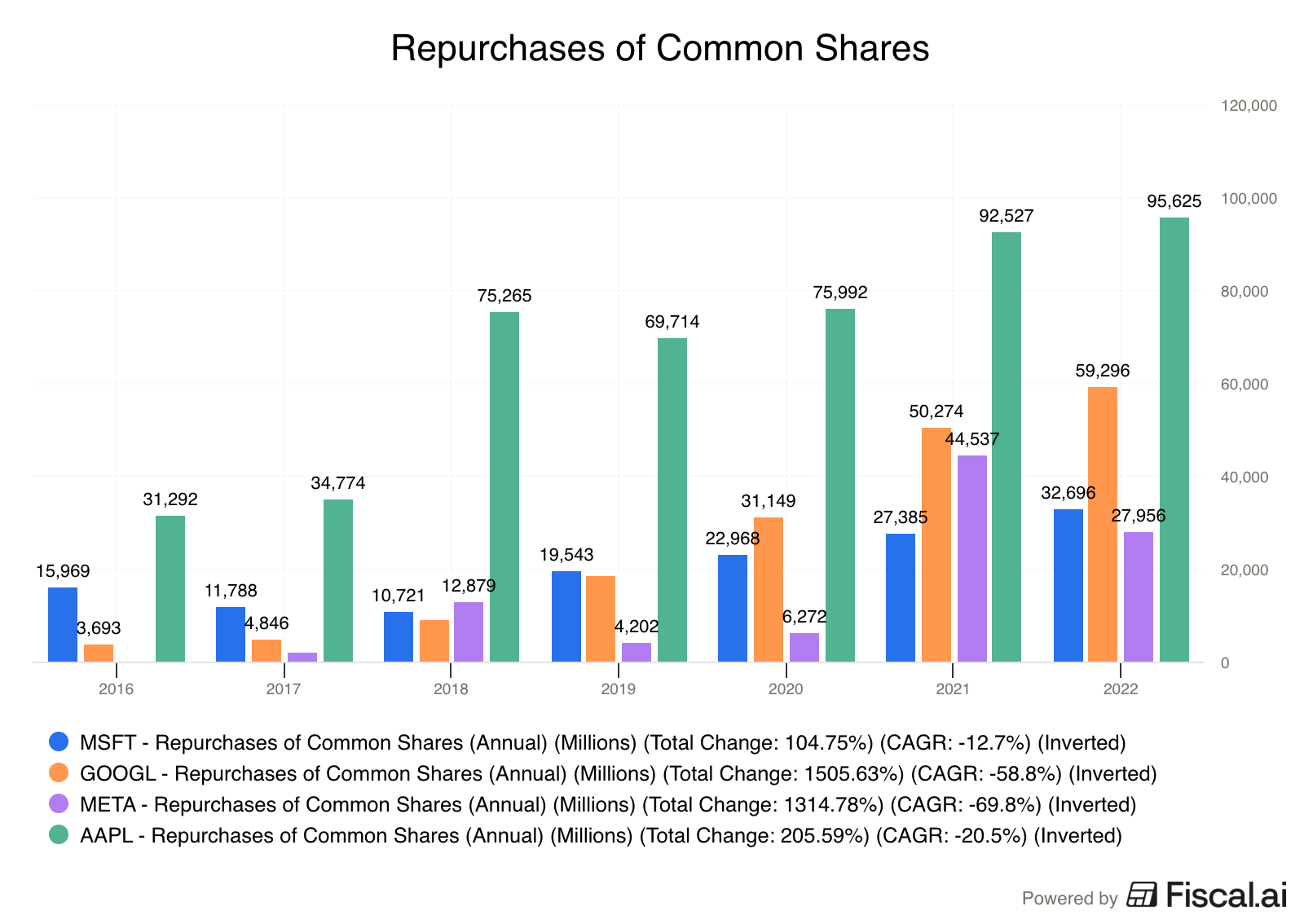

Because they made so much cash, and didn’t need much to run the business, management bought back more and more stock every single year.

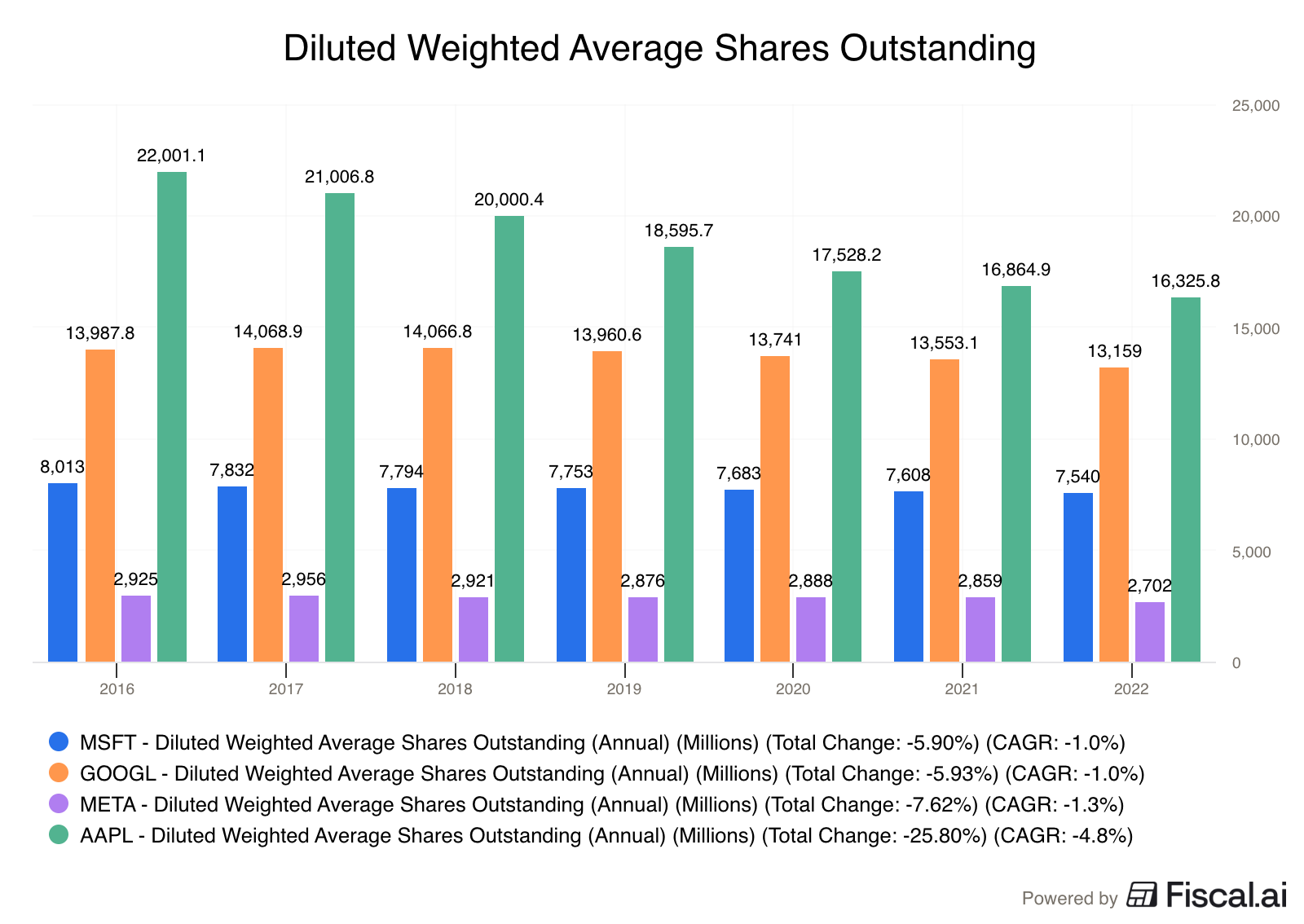

A lot of the businesses did issue a lot of share based compensation, but the diluted shares outstanding shrunk by about 1% per year for most of them.

Apple was the execution, buying back about 5% of its shares outstanding every year.

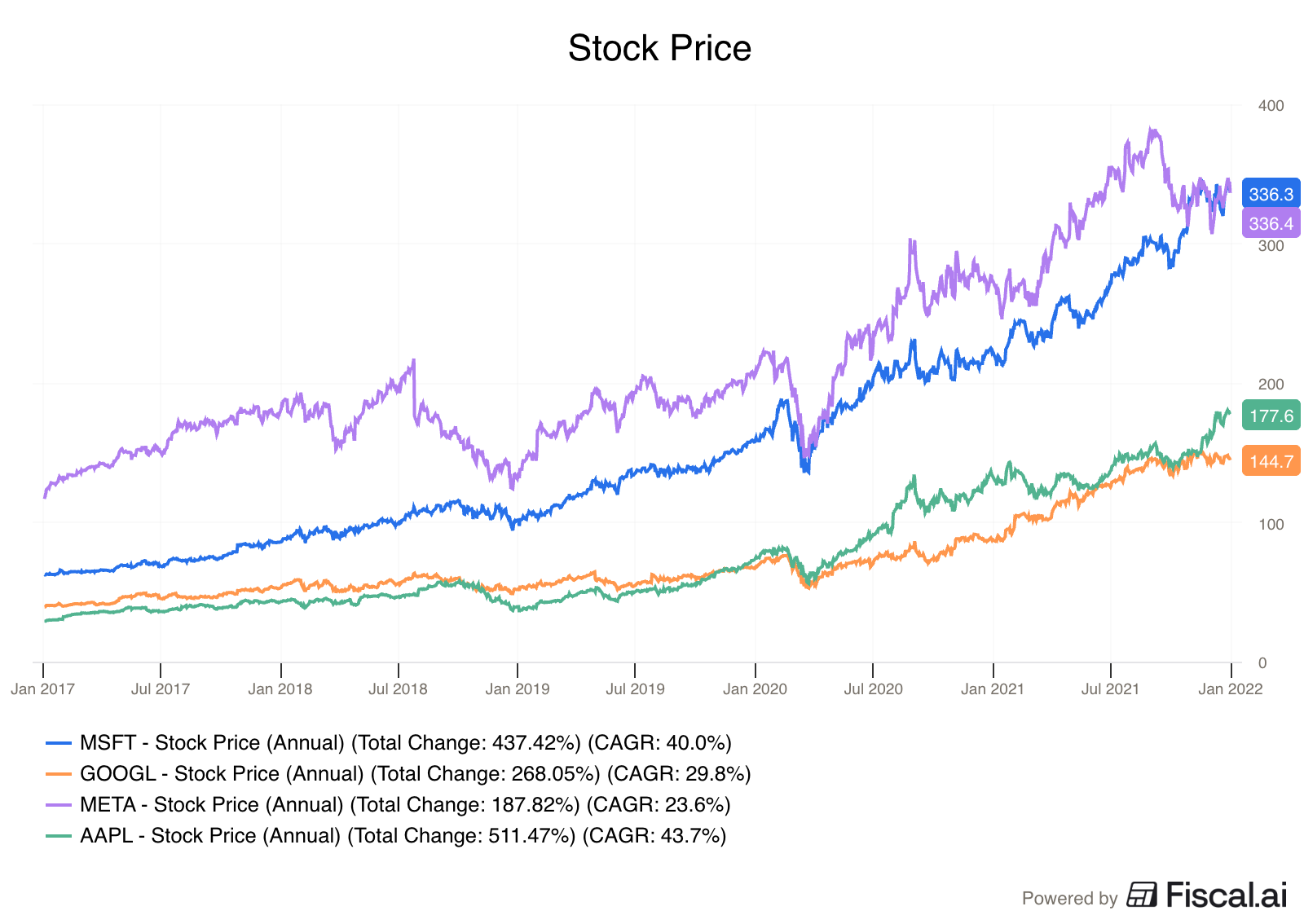

And as the profits rose, and the share count shrunk, the stocks went up.

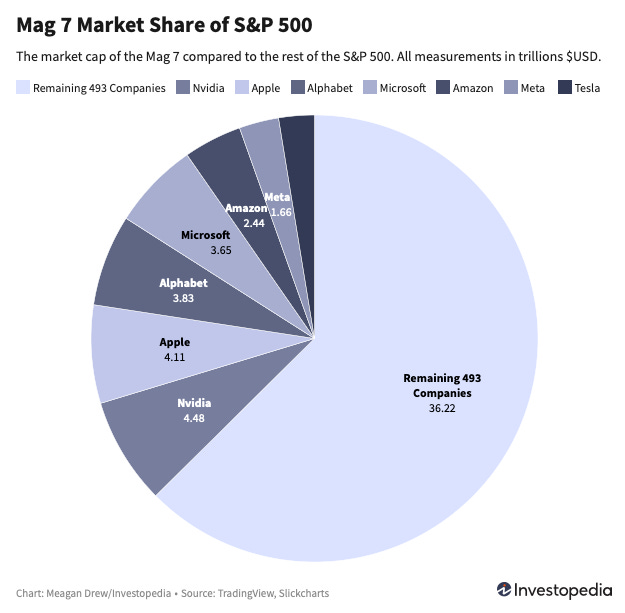

Concentration

Now they make up a huge part of index.

It used to be they were somewhat diversified:

Meta mainly sold ads, ands was tied to consumers

Google ran a diversified business, with ads, cloud computing, YouTube, etc.

Microsoft was very tied to corporate spending, selling office subscriptions and cloud services to businesses

Amazon was also diversified, with AWS, e-commerce, logistics, revenue from Prime subscriptions, etc.

Then OpenAI released ChatGPT.

And things changed quickly.

AI spending

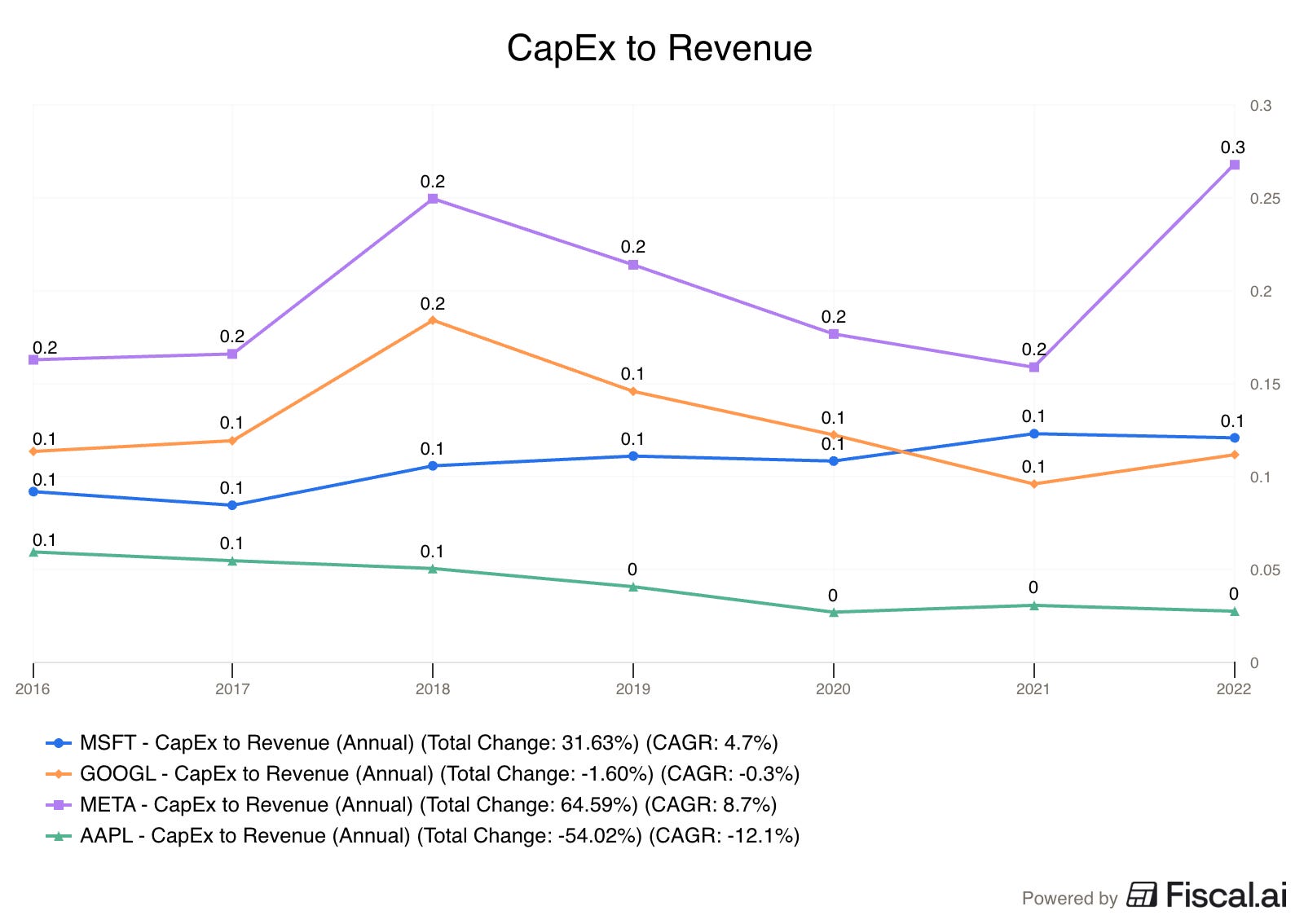

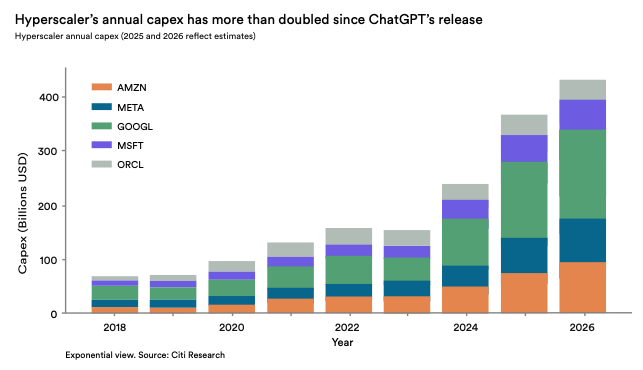

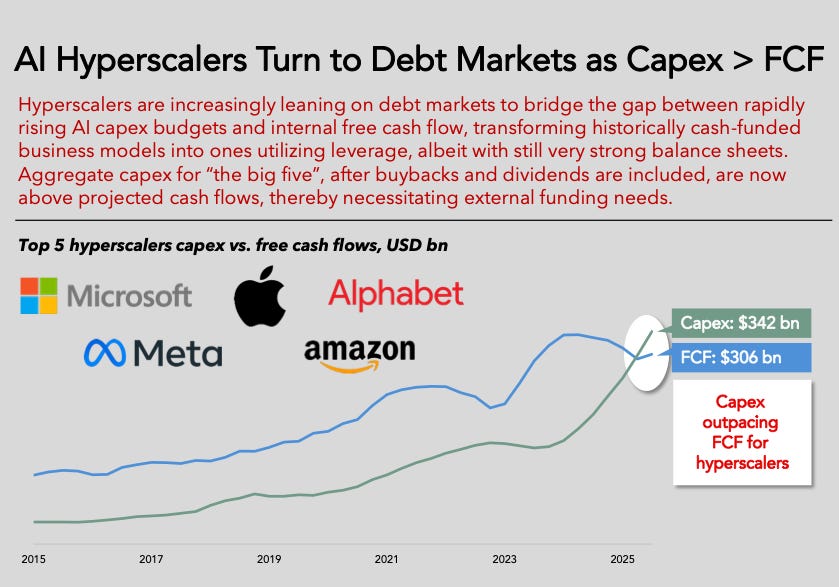

These companies went from capital light cash machines to CapEx heavy companies building data centers and all of the infrastructure to go with their transition into AI.

The amounts of money being spent are enormous.

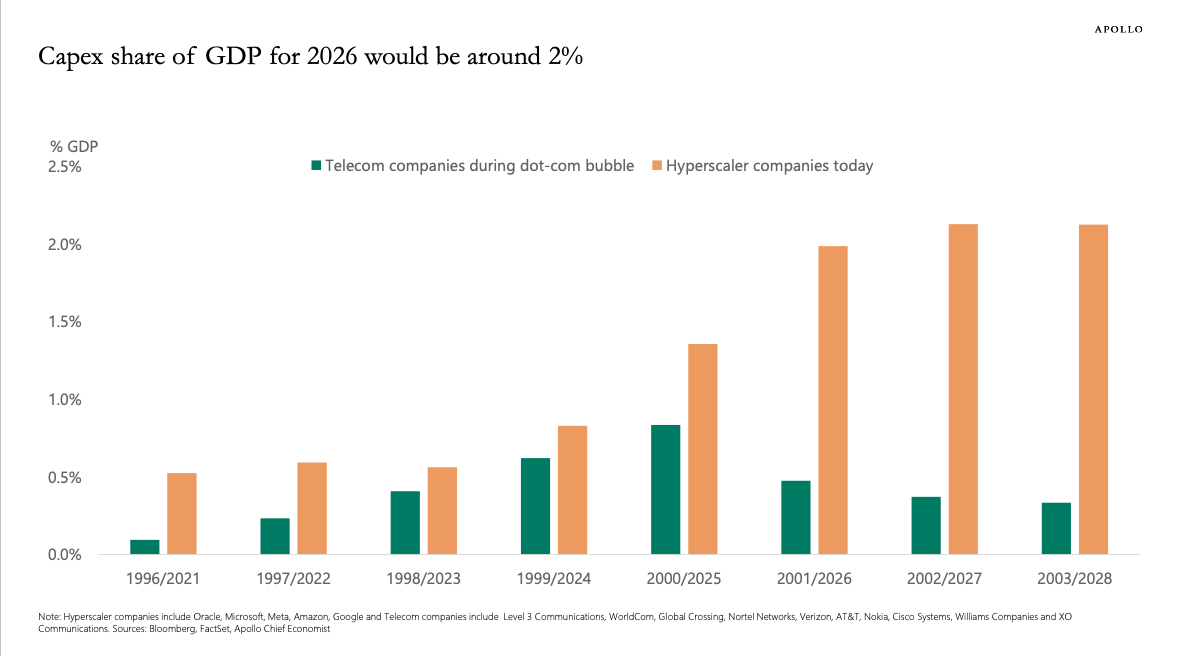

To put it into perspective, the hyperscalers are projected to spend 2% of U.S. GDP on AI CapEx in 2026.

At the peak of the 2000 dot-com bubble, CapEx spend was only about 1%.

Even though these businesses are incredibly profitable, they’re outspending what they earn, and are increasingly turning to debt to finance the AI buildout.

This increases risk, and it means that all the buybacks we talked about earlier either go away, or are financed with more debt.

Required Returns

These companies are all terrified of being left out of the AI revolution, and that fear is fueling the spending.

But I’m also going to assume that they’d like to make a return on their CapEx.

This year, Microsoft, Meta, Alphabet, and Amazon are projected to spend about $400 billion on AI.

These companies are used to making a 20% to 30% return on capital.

That’s probably not going to happen with AI, so let’s say they’d like to make 15%.

If that’s the case, you’ll need $60 billion in net income.

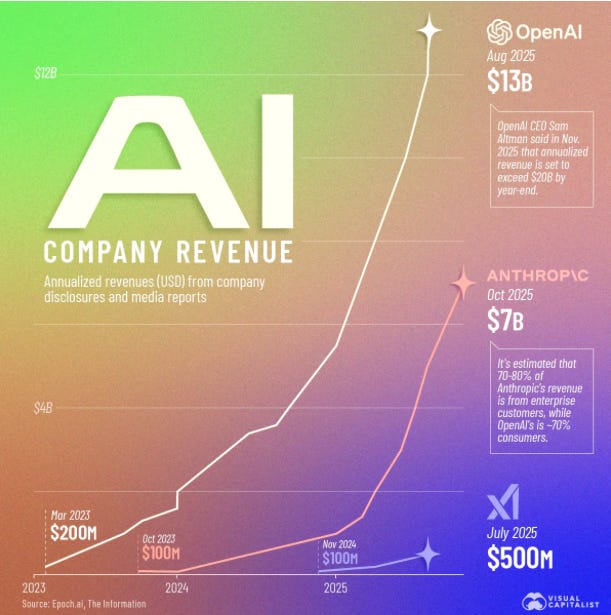

Last year, if we’re generous and include China, AI revenue was only $110 billion.

But there’s a problem - those chips and data centers don’t last forever.

There’s a debate as to whether the right depreciation schedule is 4 years, 6 years, or more.

Let’s be generous and use a straight-line 10-year depreciation schedule on them.

At $400 billion of CapEx, you’ve got $40 billion in depreciation.

So after accounting for depreciation, you need $100 billion in profit from about $110 billion in revenue.

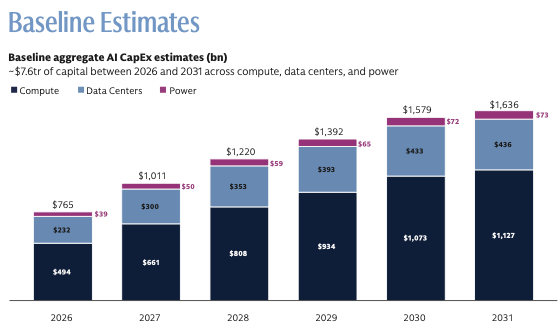

So far, we’ve spent somewhere around $1.3 trillion in AI CapEx.

There are projections now that we could spend $7.6 billion on AI between now and 2031.

I won’t do all the math, but you can see that the revenue required to justify this kind of spending is enormous.

Revenue Growth

The argument of course, is that AI revenue is growing very quickly, and that’s true.

And that’s what they want you to focus on, because most of these companies aren’t yet profitable.

We know xAI is losing massive amounts of money from the SpaceX S-1.

Open AI is projected to lose $17 billion in 2026 on $20 billion in revenue.

Anthropic did make an operating profit in Q2 of this year, but it may not remain profitable for the year.

The reported operating profit number also excludes stock based compensation, which I would expect to be high.

Expectations vs Reality

The expectation is that revenue will keep growing at triple digit rates, spending will slow down, and eventually all of these companies will make massive profits.

But this is all set against the backdrop of companies starting to slow down their AI spending.

Like the company that accidentally spent $500,000,000 on Claude in one month.

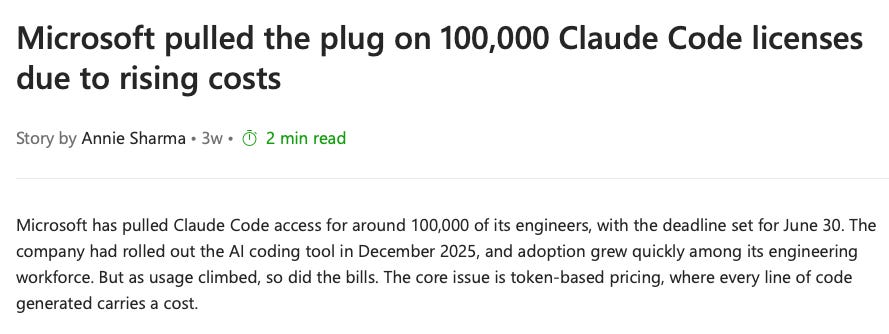

Or Microsoft who cancelled 100,000 Claude licenses because of the cost.

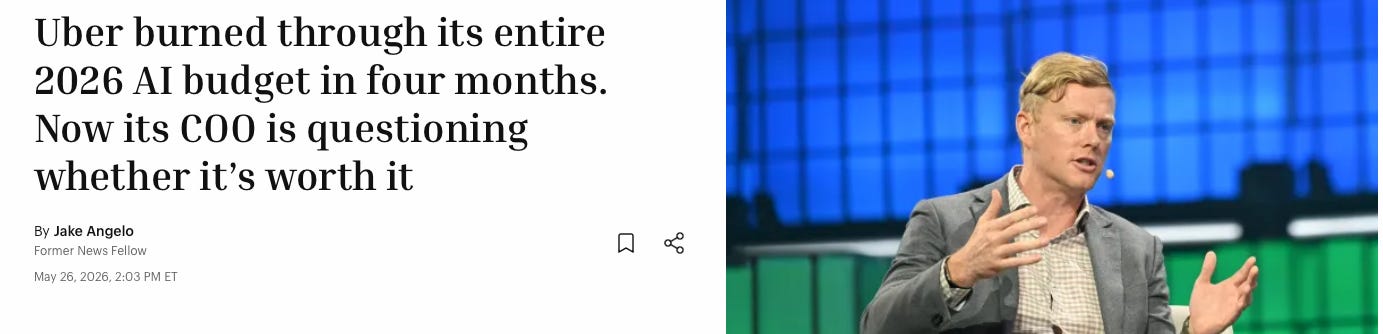

Or Uber, who spent the entire 2026 AI budget in 4 months, and isn’t sure it was worth it.

At the same time, competition is rising.

OpenAI is reportedly considering cutting the price to compete with Anthropic.

That would of course further hurt profitability, and make it even harder to get a return on trillions of dollars of CapEx.

And it’s not just the models where competition is increasing.

Google and Amazon are both considering selling their own custom AI chips to outside firms.

That threatens Nvidia’s margins and profitability.

And Nvidia is actually helping finance the massive buildout that requires its chips.

Bringing It Together

I’ll be very clear here.

This looks very much like the internet bubble to me.

Back then we spent 1% of GDP on fiber.

By 2021, only 4% of the fiber we put in the ground was being used.

The companies who laid the fiber couldn’t support their debt, and they went bankrupt.

If we didn’t lay all that fiber you wouldn’t have Youtube and you probably wouldn’t be reading this article right now.

It went great for consumers. It went terrible for the businesses.

AI is a world alternating technology.

That doesn’t mean that the companies who build it will do well, and it certainly doesn’t mean their investors will make money.

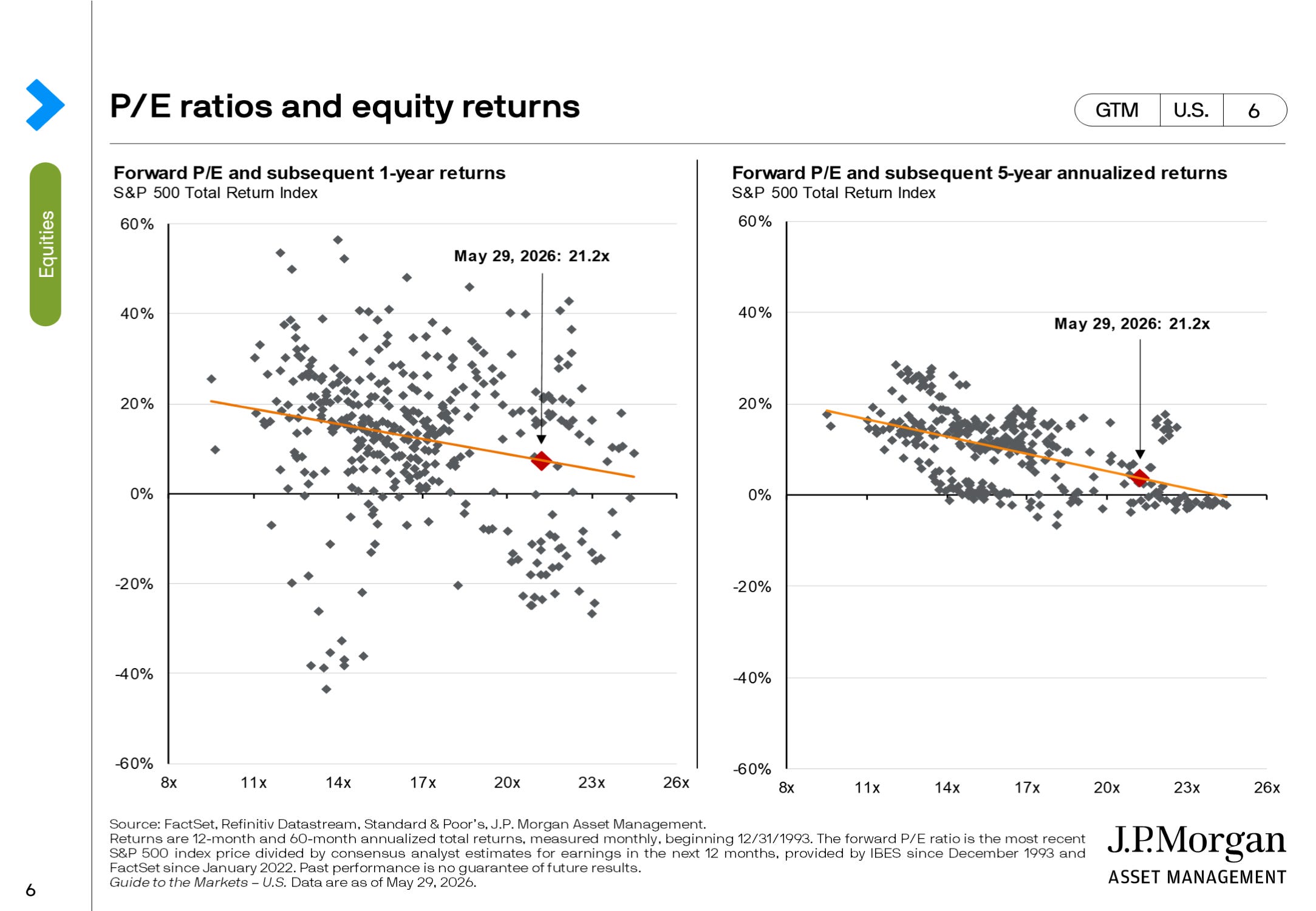

Based on the Forward P/E alone, the 1 and 5 year returns for the S&P 500 look like they’ll be below average.

Even though the long-term track record of the index is impressive, we’ve had decades with no returns.

Once after the dot com bubble burst, and once during the high inflation era of the 70’s.

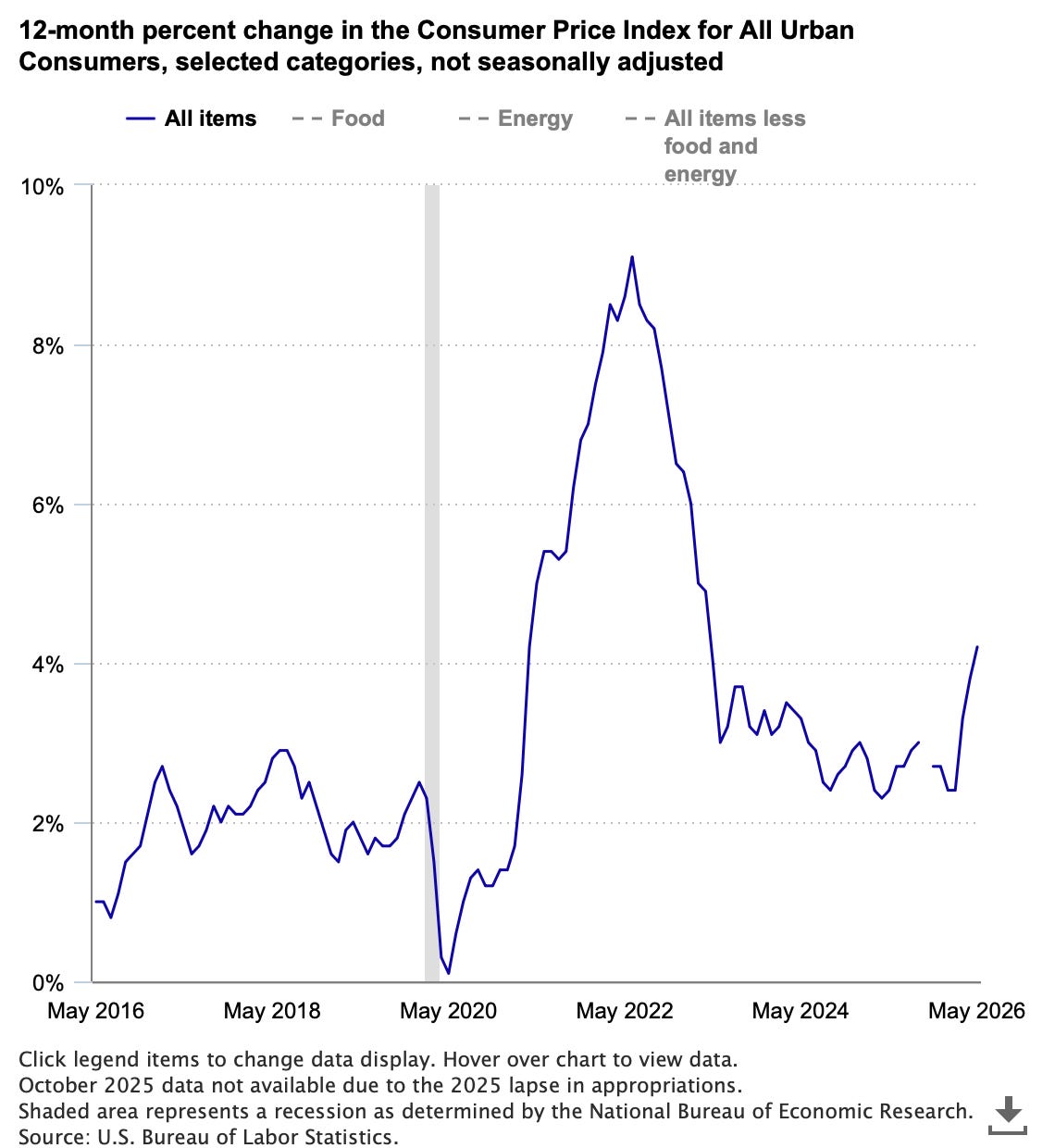

Not only do we have what looks like a massive capital cycle going on with AI, we also have inflation rising back up.

I’m not predicting doom, a crash, or a lost decade.

But, should one happen, having some of your return tied to cash coming directly from businesses in the form of dividends is a great idea.

In the 1970’s, 73% of the index’s total return came from dividends.

During the lost decade of the 2000’s, dividends were the only source of positive returns

If you don’t want to miss out on the special focus on high yield coming, make sure you’re on the VIP list.

We start tomorrow.

You’ll also get the following just for joining the VIP list:

My high-yield stock watchlist

A Checklist of Dividend Investing Mistakes

The Highest Yielding Dividend Aristocrats

One Dividend At A Time

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.

Amazing insights