HCA Healthcare is a serious cannibal stock.

They reduced their share count by 5% per year over the past decade.

The stock is currently down 20% from its peak in October.

Does this hospital operator have a minor cold, or is something more serious going on?

Let’s take a Not So Deep Dive into the company to find out!

Source: Finchat

1. Do I understand the business model?

Remember, we want a simple and attractive business model.

HCA is the largest operator of acute care hospitals in the United States.

They also have a large network of outpatient, ambulatory and other services.

As of their Q3 call, HCA had more than 2,600 sites of care.

The majority of HCA’s revenue comes from US government programs.

50% of volume comes from Medicare

17% comes from Medicaid

HCA’s Advantages

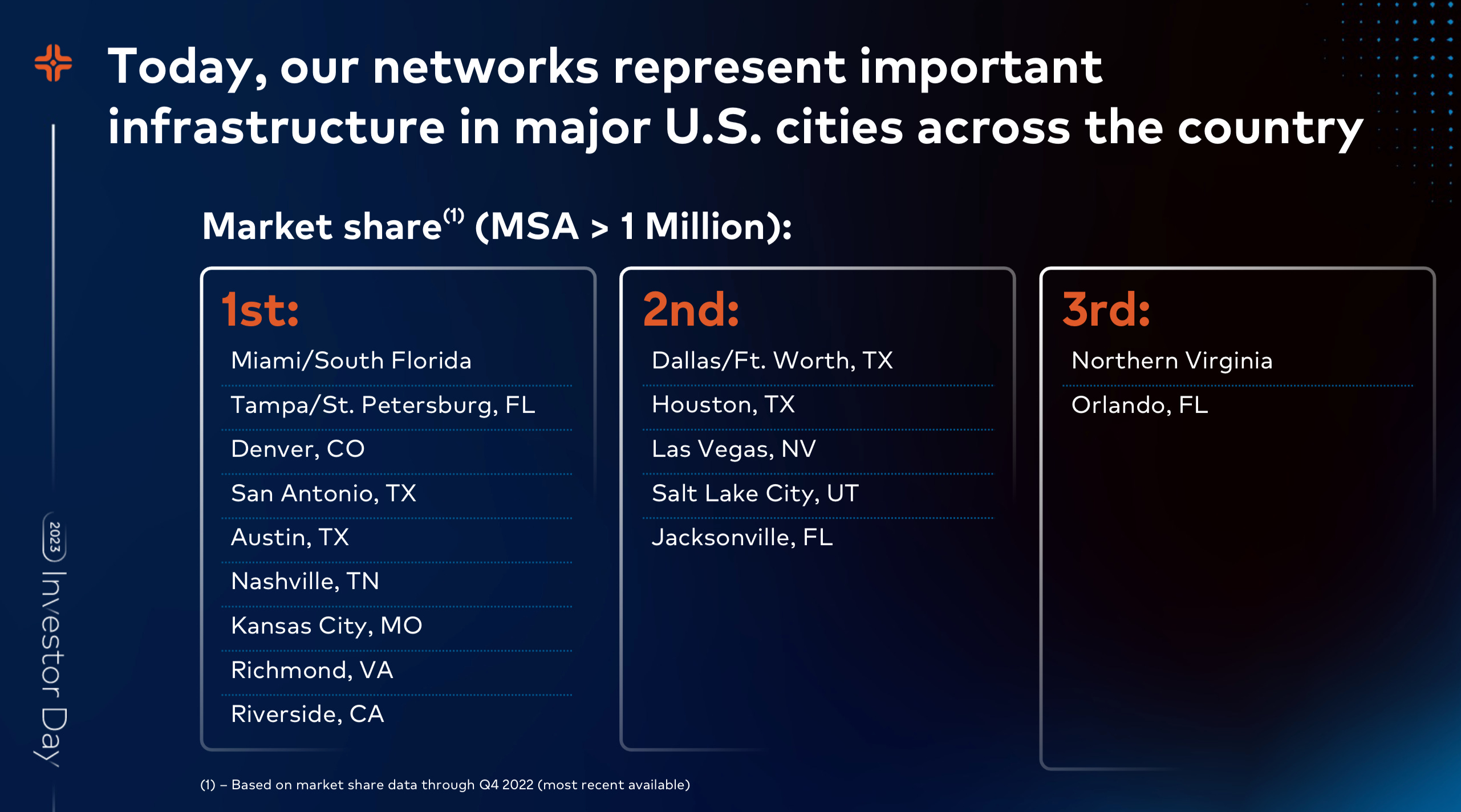

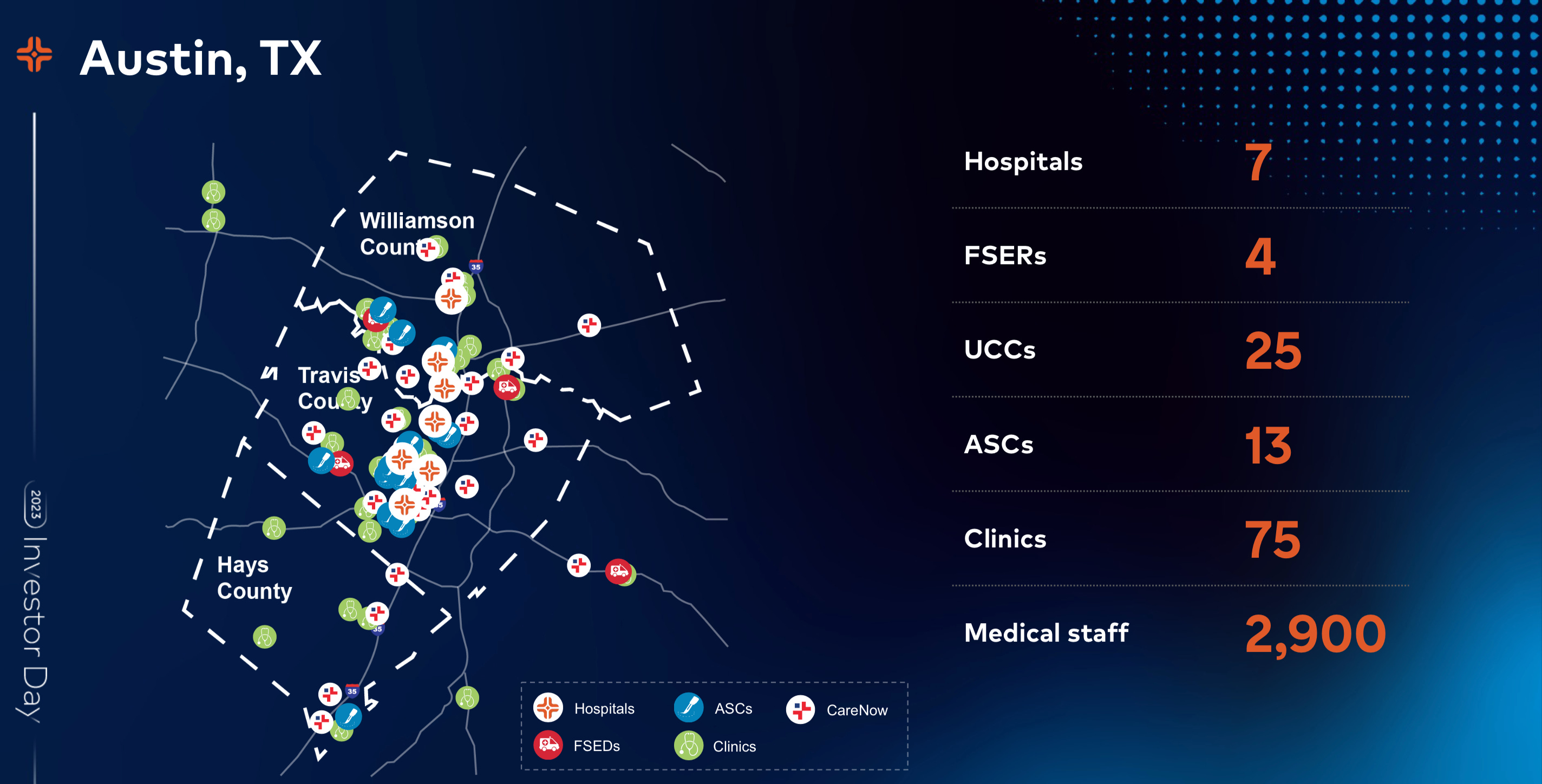

HCA creates local monopolies in healthcare and services.

50% of HCA hospitals are in Texas & Florida.

They have the #1 or #2 position for market share in many large urban areas.

Their sites operate as a network, with the hospital as a hub.

The other sites like outpatient centers, urgent care centers, and physician offices are the spokes - reaching further out.

2. Is management capable?

You want to invest in companies led by great managers.

Sam Hazen is Chief Executive Officer of HCA Healthcare.

He’s been in that role since 2019, and with the company for 38 years including roles as COO, President of Operations, and CFO of several hospitals.

Mr. Hazen owns more than $470 million in HCA stock.

More than 50% of employees approve of the job he’s doing and HCA is rated at 3.3 stars.

That’s comparable to other large hospital operators, here are the next 3 largest by size:

Encompass Health – 143 hospitals - 3.6 stars

Ascension Health - 143 hospitals - 3.6 stars

CommonSpirit Health - 140 hospitals - 3.4 stars

HCA has maintained an ROIC of more than 10% for years.

Source: Finchat

3. Has the company grown its dividend attractively?

You want to invest in companies with a history of growing their dividends.

The higher the dividend growth, the better.

Look for 2 things in the company’s dividend history:

At least 10 years of dividend growth

A 5-year record of growing dividends by 5% or more

HCA does not meet these criteria.

That’s because HCA is a Cannibal Company - returning capital through buybacks instead of dividends.

Source: Finchat

HCA has reduced the share count by about 5% each year.

Source: Finchat.

4. Is the company active in an attractive end market?

You want to invest in companies that are in a stable or growing market.

Here are a few characteristics we look for:

The company sells a necessary product

Recurring sales

A secular tailwind

HCA has all of these characteristics:

Healthcare is necessary, tends to be recurring and the aging of the population means that there is a secular tailwind behind it.

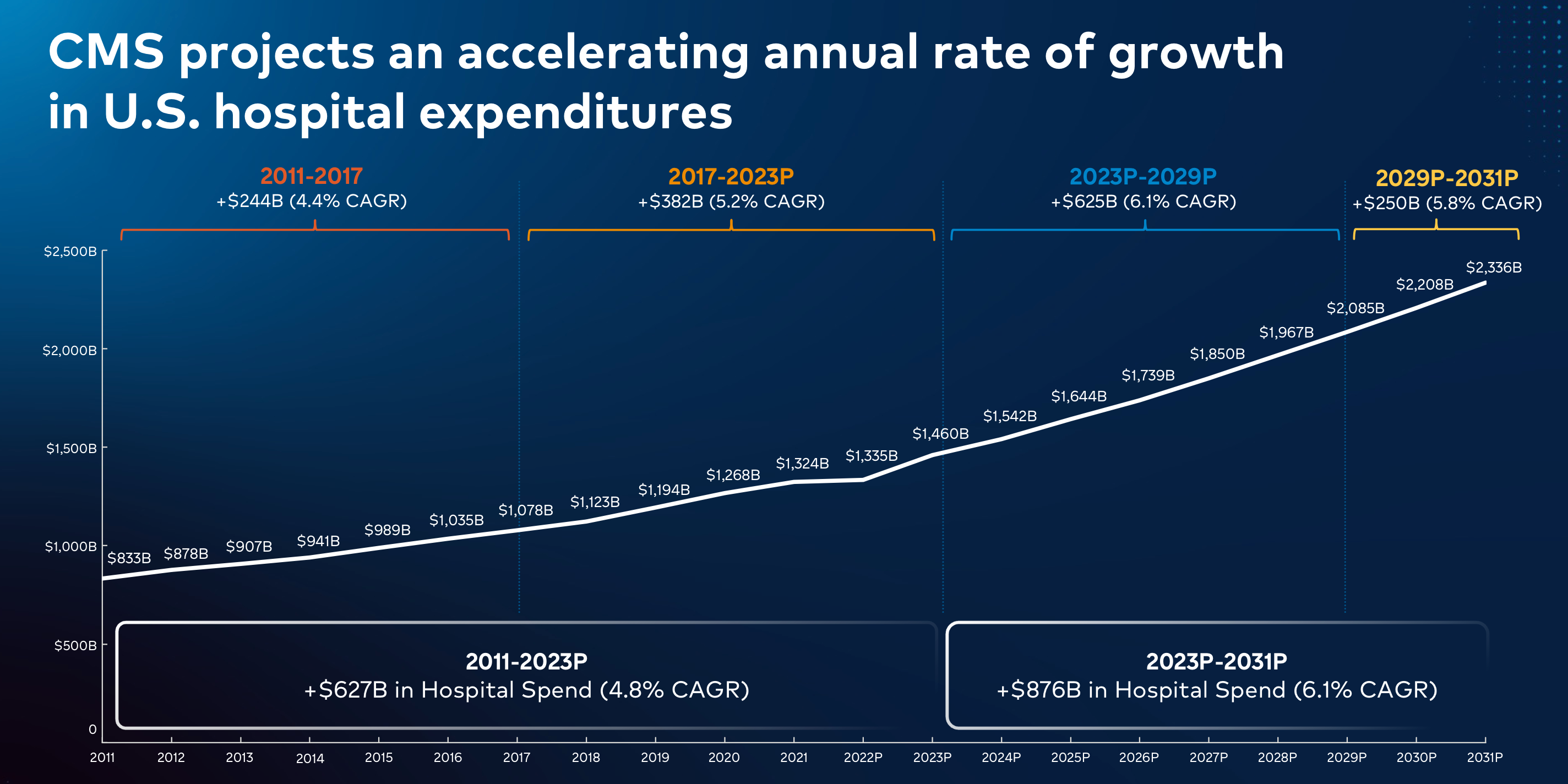

CMS is the government agency in charge of Medicare and Medicaid.

Here are their projections for hospital spending.

5. What are the main risks for the company?

Disruption is the worst enemy for every long-term investor.

When you invest in a company that is losing its moat, you’ll end up with horrible investment results.

Let’s talk about HCA’s largest risks

Political Risk

Republicans are now in control of the US government and want to make changes to healthcare.

8-10% of HCA’s payments come from plans bought on insurance exchanges

These are the 2nd best payers behind commercial insurances

Republicans have said they want to repeal “Obamacare” which created these insurance exchanges

50% of HCA’s payments come from Medicare, another government program

They would be affected by any changes or cuts to payments from that program as well

Medicaid is 17% of HCA’s payment volume, which is also a government program

Labor

There have been shortages in nurses, physicians, and other staff.

HCA is well staffed today, but the shortages raised labor costs significantly from COVID in 2020 to today.

At the peak, up to 10% of labor costs were contract and travel employees

These are much more expensive

That has been reduced to 4.6% in Q3 2024

HCA has been investing to develop their own workforce

They bought the majority of the Galen School for Nursing in 2020

Have been expanding, with target of 30 capuses by 2028

Debt

HCA carries more than $40 billion in Net Debt.

HCA has a Debt/Equity ratio over 50

Their cash flow/debt ratio is around 12%, meaning it would take more than 8 years to pay off the debt from cash flow.

Now let’s dive into more into the balance sheet and other Fundamentals.