Quick Pitch: AH Realty Trust

👋 Howdy Partner,

Today we’re looking at a AH Realty Trust, a company undergoing a massive change.

For years, this REIT built buildings, financed other people’s projects, managed apartments, and owned offices.

It’s become much simpler recently, but is it an interesting company?

AH Realty Trust is the new name for Armada Hoffler Properties.

Armada Hoffler ran differently from most other REITs.

It used a development-first model, building high-quality mixed-use, multifamily, office, and retail assets, then selectively keeping only the best properties long-term.

That made it difficult to figure out.

And complex companies often trade at a discount.

That was part of the problem for Armada Hoffler Properties.

The other part?

The market hated the lumpy earnings from the property development business.

Shawn Tibbetts took over as CEO last year, and after a review of the company, decided to simplify it.

Want to see the new look?

Keep reading.

Company Overview

Armada Hoffler officially became AH Realty Trust on March 2, 2026.

The new name is align with the new strategy to:

Move away from unpredictable construction income

Focus on steady, reliable income from high quality properties

Reduce debt and secure stronger financing

Own fewer, higher-quality properties instead of growing for the sake of growth

If they pull it off, we’re looking at a simplified, focused REIT that strictly owns high-quality Retail and Office assets.

By the time the dust settles, they will have exited the multifamily (apartment) sector, shuttered their construction business, and wound down their real estate financing arm.

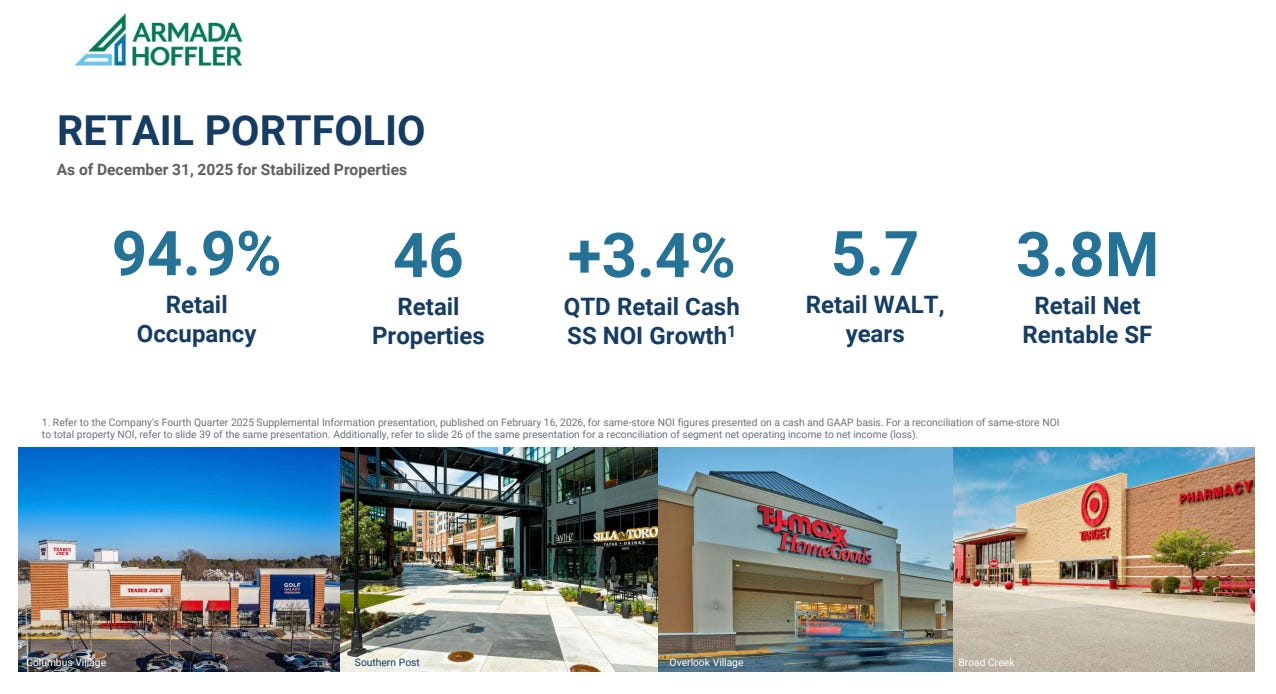

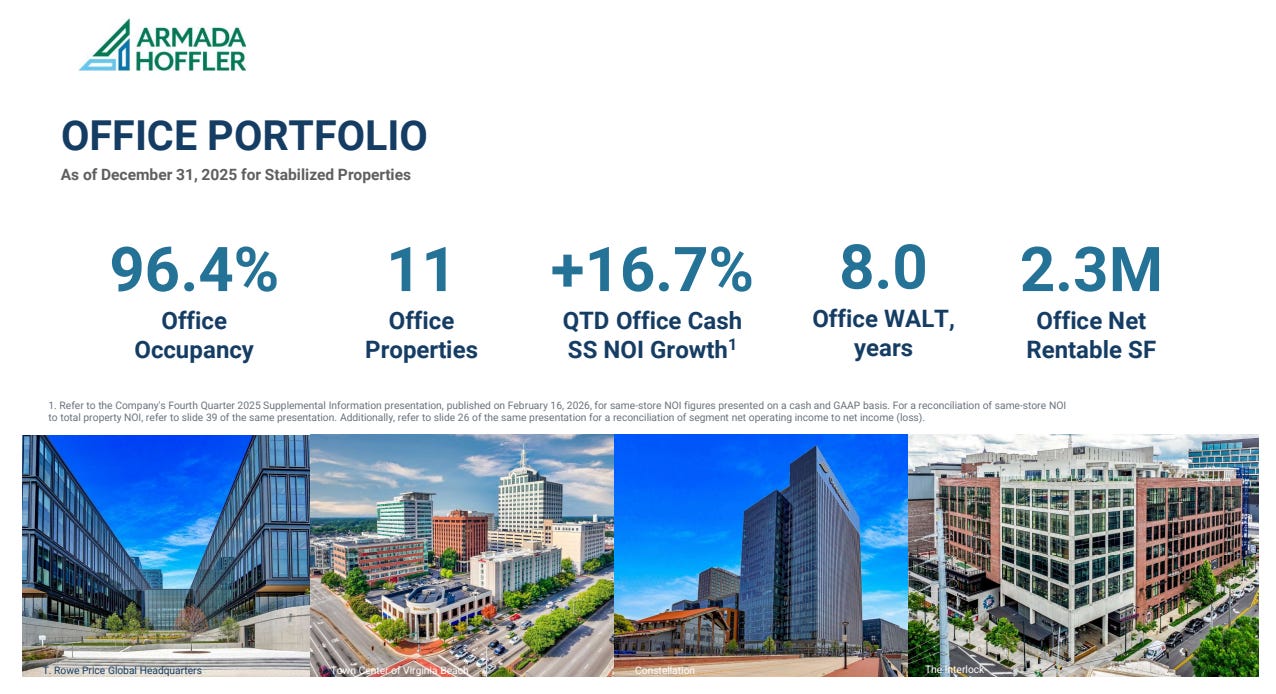

The Portfolio

AH Realty Trust will own retail buildings:

And office properties:

94% of their Net Operating Income (NOI) comes from mixed-use communities like the Town Center of Virginia Beach and Baltimore’s Harbor Point.

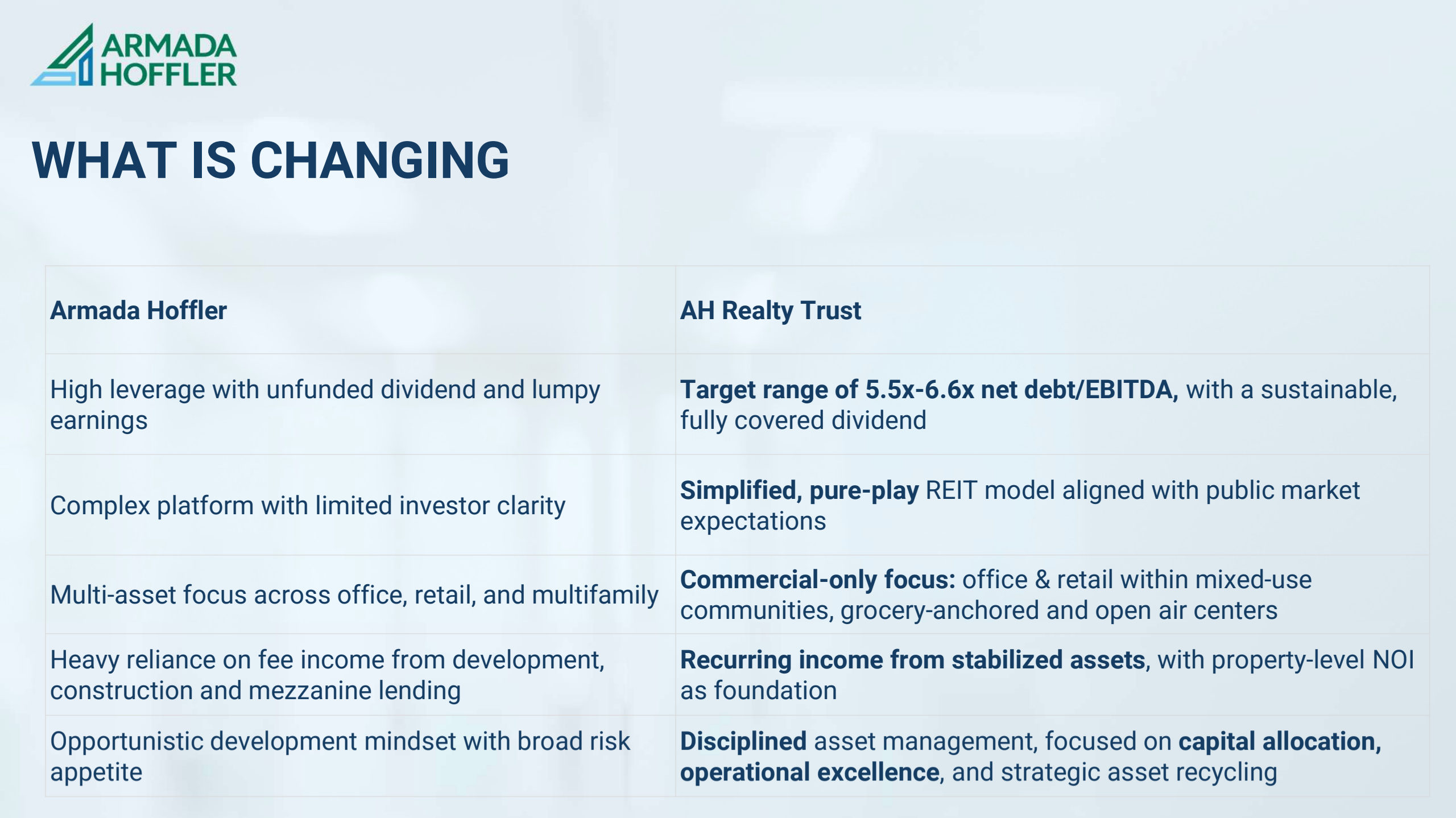

The Transformation: What’s Changing?

The goal here is simple: predictability.

Management is trading lumpy fee income for recurring, contractual rent checks.

They’re also planning on reducing debt.

“The days of being a sprawling, complex octopus are behind us.” — Shawn Tibbetts, CEO

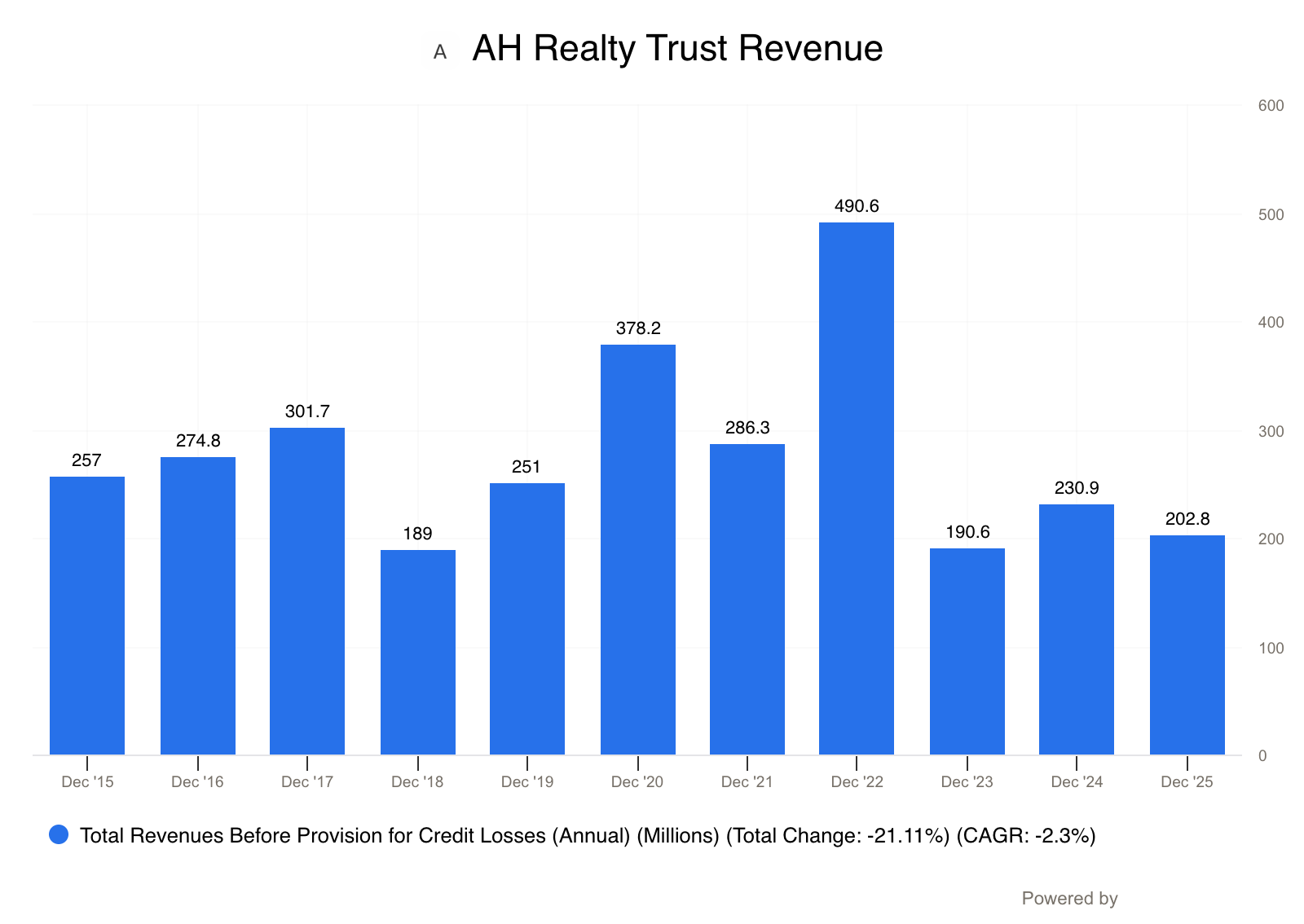

Financial Performance & Outlook

Dividend Reset

In March 2025, the company made the “difficult but necessary” choice to reset the dividend to a sustainable level.

They cut the quarterly dividend from $0.205 to $0.14 per share.

Normally we don’t like to see a dividend cut.

But sometimes it’s the right business decision.

The payout is now fully covered by recurring cash flow.

2026 should have an AFFO payout ratio of approximately 95%.

Management isn’t in a hurry to hike it, they’re focused on deleveraging first.

Ultimately, this should set AH Property Trust up to be a stronger, more stable business.

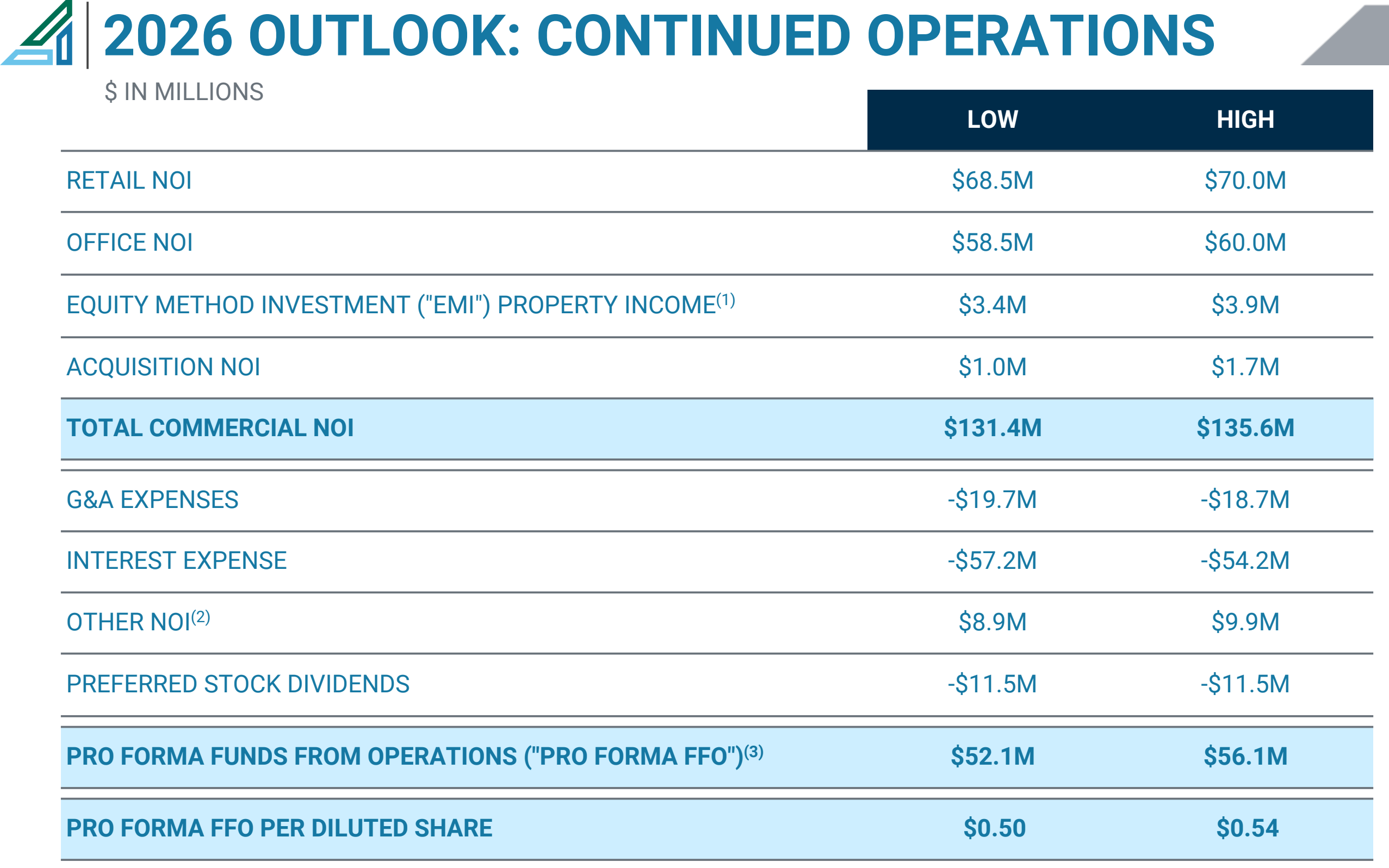

2026 Guidance

2026 is going to look a bit messy on paper because it’s a transition year.

FFO Guidance: Expected between $0.50 and $0.54 per share for 2026.

Debt Reduction: They plan to use proceeds from selling their apartments to pay down roughly $670 million in debt.

Acquisitions: They plan to buy about $50 million in retail properties in the second half of this year

Valuation

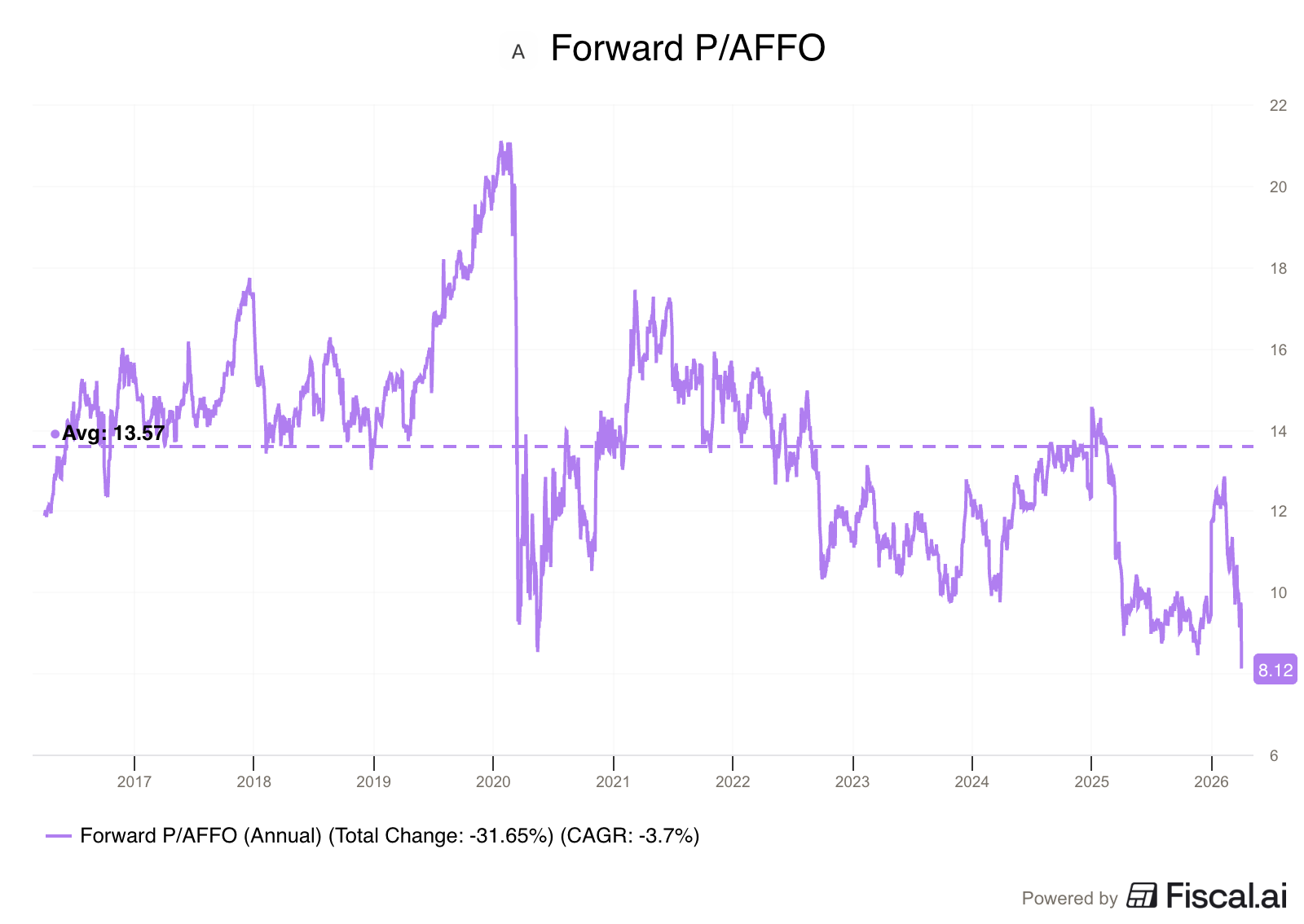

AH Realty Trust has seen the share price drop by more than 50% over the past few years.

That puts it close to a 10% dividend yield, even after the cut.

It also means that it’s trading well below its usual Forward P/AFFO.

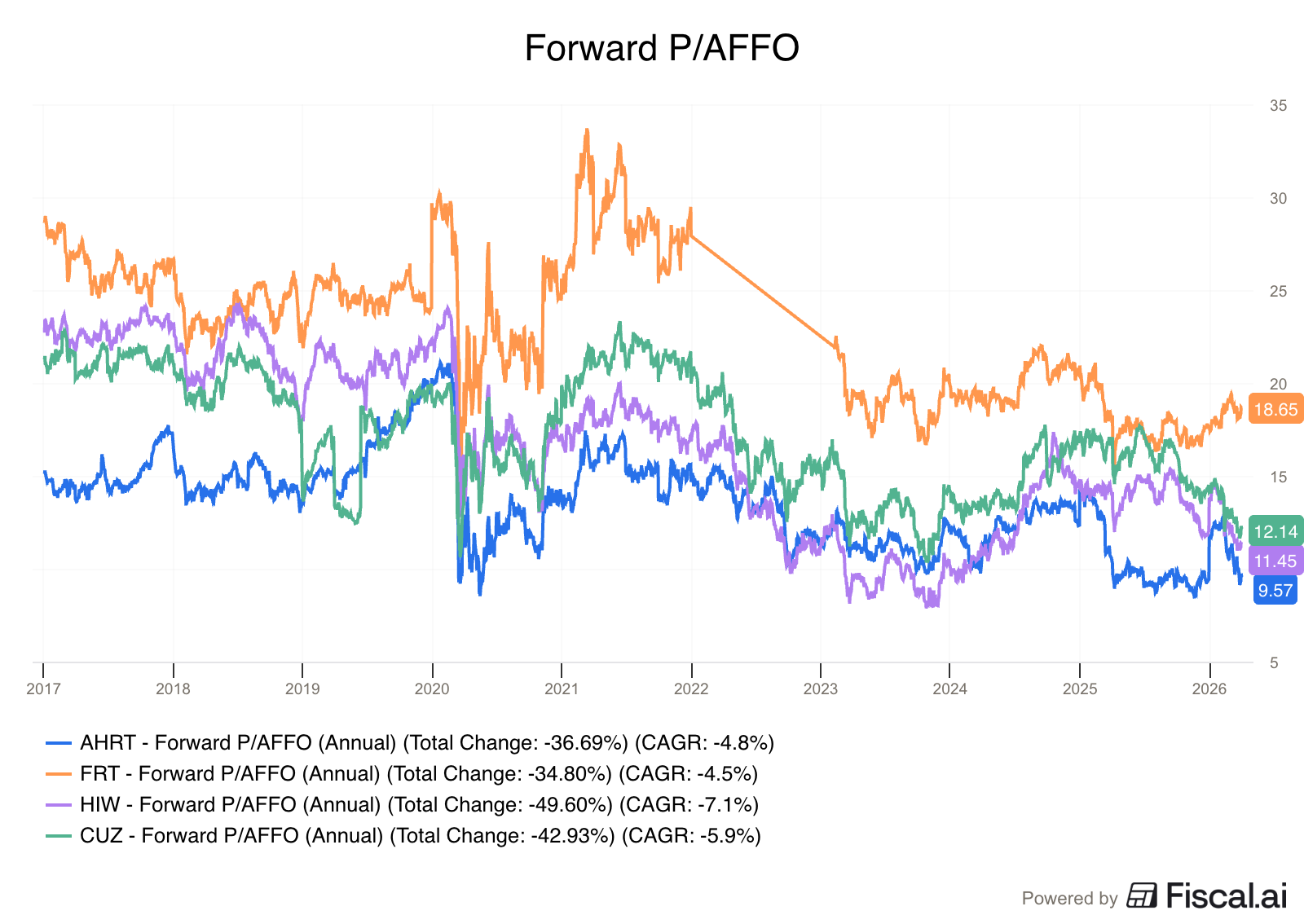

We can also compare the valuation to competitors like:

Federal Realty Trust: Own high-quality, urban mixed-use properties like AH Realty Trust’s Virginia Beach Town Center

Cousins Properties (CUZ): A Sun Belt office REIT that with a very similar strategy to AH

Highwoods Properties (HIW): A direct peer in the office sector that’s active in AH’s high-growth secondary markets

When we do this, we see that AH Realty Trust is at a much lower multiple.

However we choose to look at it, the company looks cheap.

Risks and Considerations

AH Realty Trust is currently in the middle of a serious shift in strategy.

That makes it more risky than some other REITs because of things like:

Execution Risk: They are currently under LOI for 11 of 14 multifamily assets. If these deals fall through or the pricing is worse than what they expect, they may not be able to pay down as much debt as they hope.

Office Headwinds: While their office occupancy is high, they are facing vacancies in Durham and Baltimore that will weigh on growth in the short term.

Dilution: Selling assets to pay down debt is dilutive (meaning lower FFO per share in the short run), but it does seriously de-risk the company.

Final Thoughts

AH Realty Trust was complex company that financed and developed property, owned office buildings, retail centers, and apartments.

By exiting the construction business and the less profitable apartment world, they are betting that investors will reward them with a higher valuation for being a pure-play commercial REIT.

If you believe in the company’s pivot, you’re getting a seat at the table while the stock is in the bargain bin compared to peers like Federal Realty or Cousins Properties.

The bull case is simple: a leaner balance sheet, a fully covered dividend, and high-quality mixed-use assets that are currently 94-96% occupied.

However, the bear case is just as simple.

This transformation is dilutive in the short term, and management still has to finalize the sale of their multifamily portfolio and navigate office vacancies in Durham and Baltimore.

Whether AH Realty Trust is a buy or a wait-and-see depends entirely on your confidence in Shawn Tibbetts and his team’s ability to simplify AH Realty Trust without hurting the core business.

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

There’s always a moment when a sprawling story tries to reinvent itself as something simple. Investors say they want clarity, but when it finally shows up, it usually arrives wearing the scars of everything that had to be cut away to get there.

What stands out here is the trade being made beneath the surface. Chaos for predictability, growth for stability, ambition for discipline. The yield looks generous because the past still lingers in the price, while the future hasn’t earned its credibility yet. That gap is where conviction either compounds or quietly erodes.