📈 Quick Pitch: Comcast

👋 Howdy Partner,

Today we’re looking at another company that’s about to go through a big change.

It’s Comcast ($CMCSA).

For years, Comcast has said that the combination of the media and connectivity (broadband) businesses has advantages.

But now they’re planning on separating them.

Let’s look at if this could be an interesting opportunity.

Company Overview

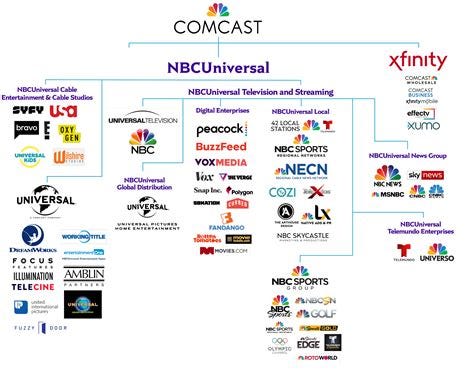

Today, Comcast is huge.

They own:

Xfinity, the nation’s largest broadband network

NBCUniversal

The NBCUniversal theme parks

Sky

The Peacock streaming platform

Movie and TV studios like DreamWorks, Illumination, and Sky Studios

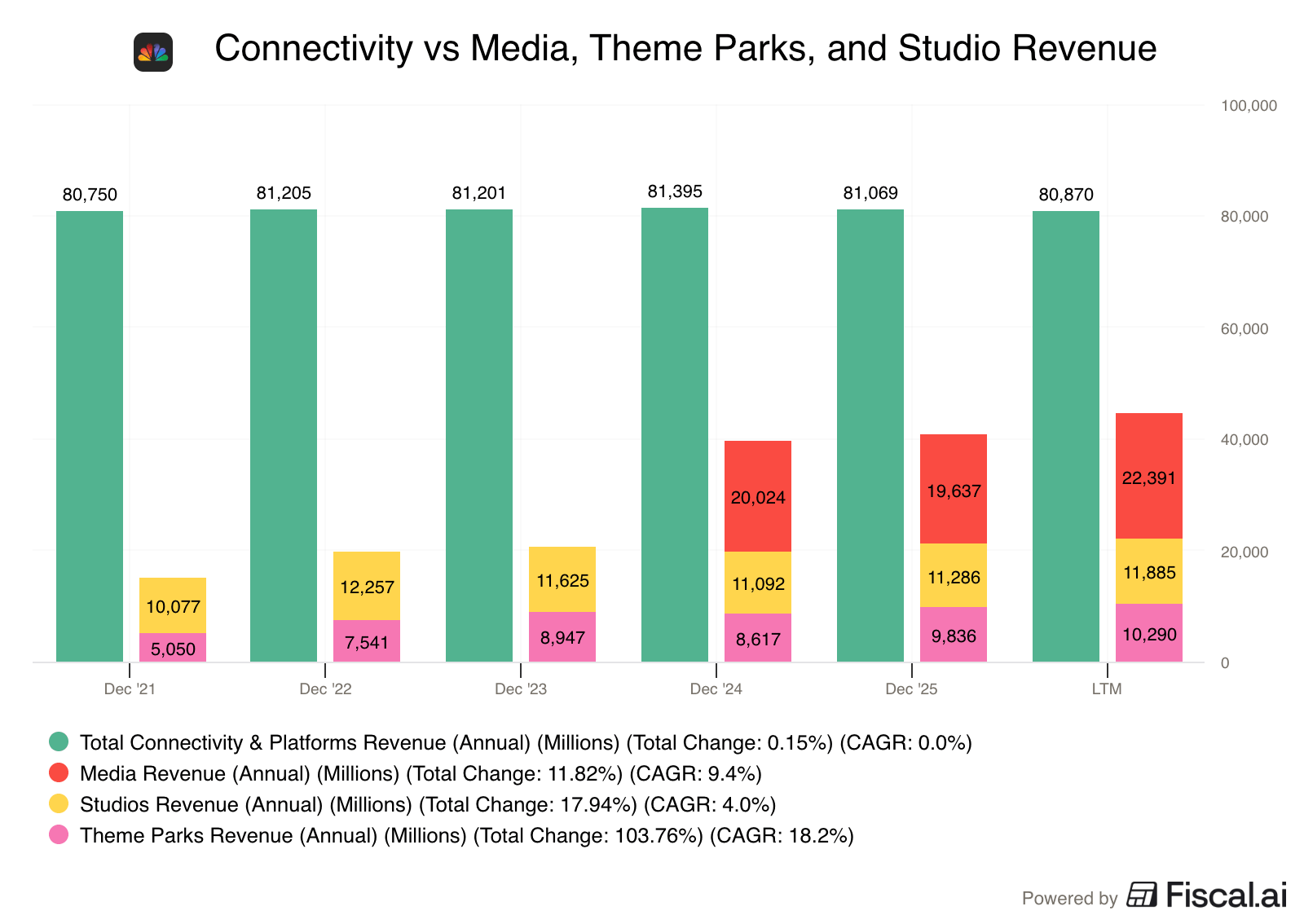

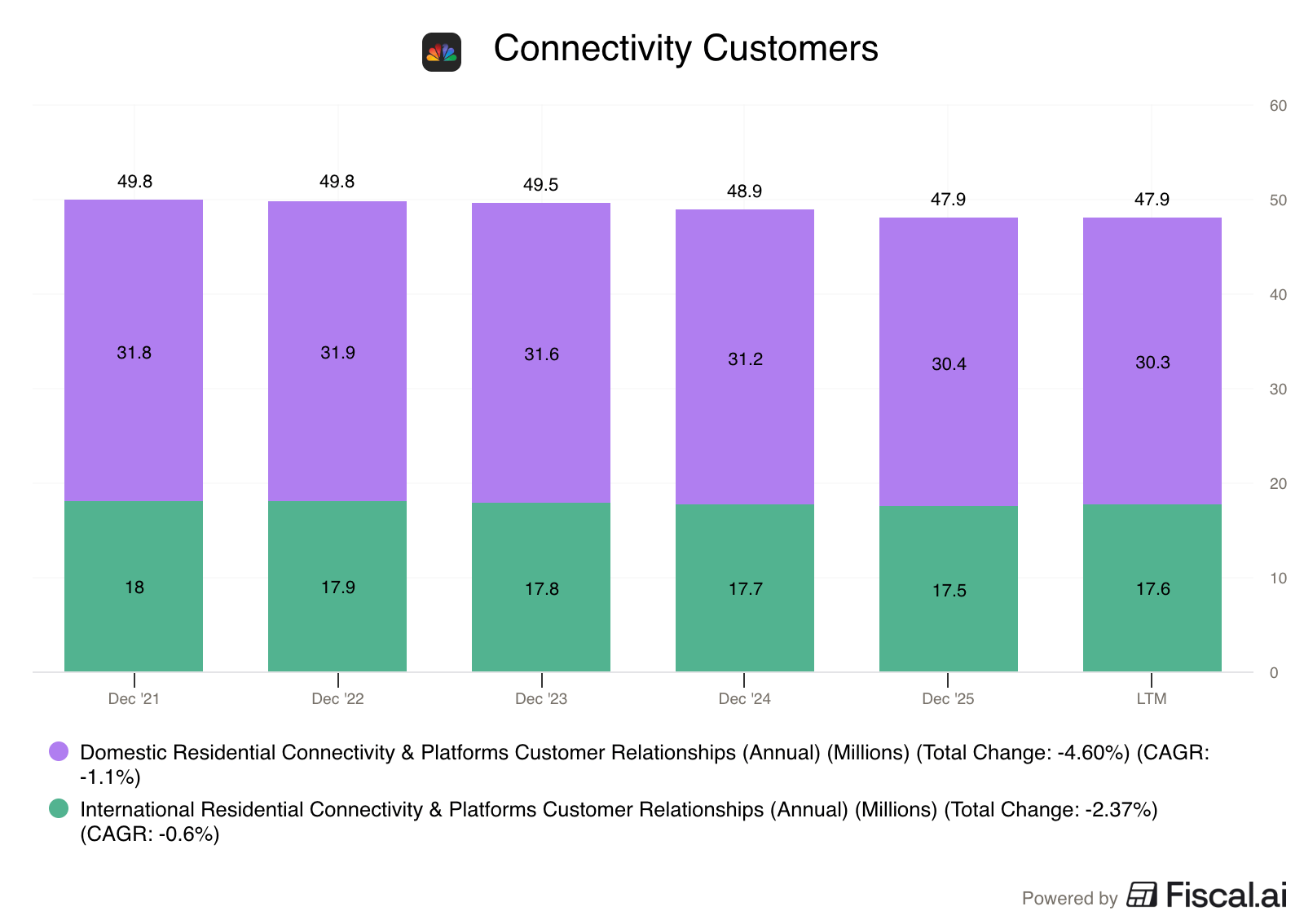

The connectivity business includes broadband for homes and businesses.

This is almost like a utility business, with very steady revenue

The media, studio, and theme park businesses aren’t as stable as broadband.

The theme parks are growing quickest

Studio revenue has been steady

Media doesn’t have a lot of data (yet)

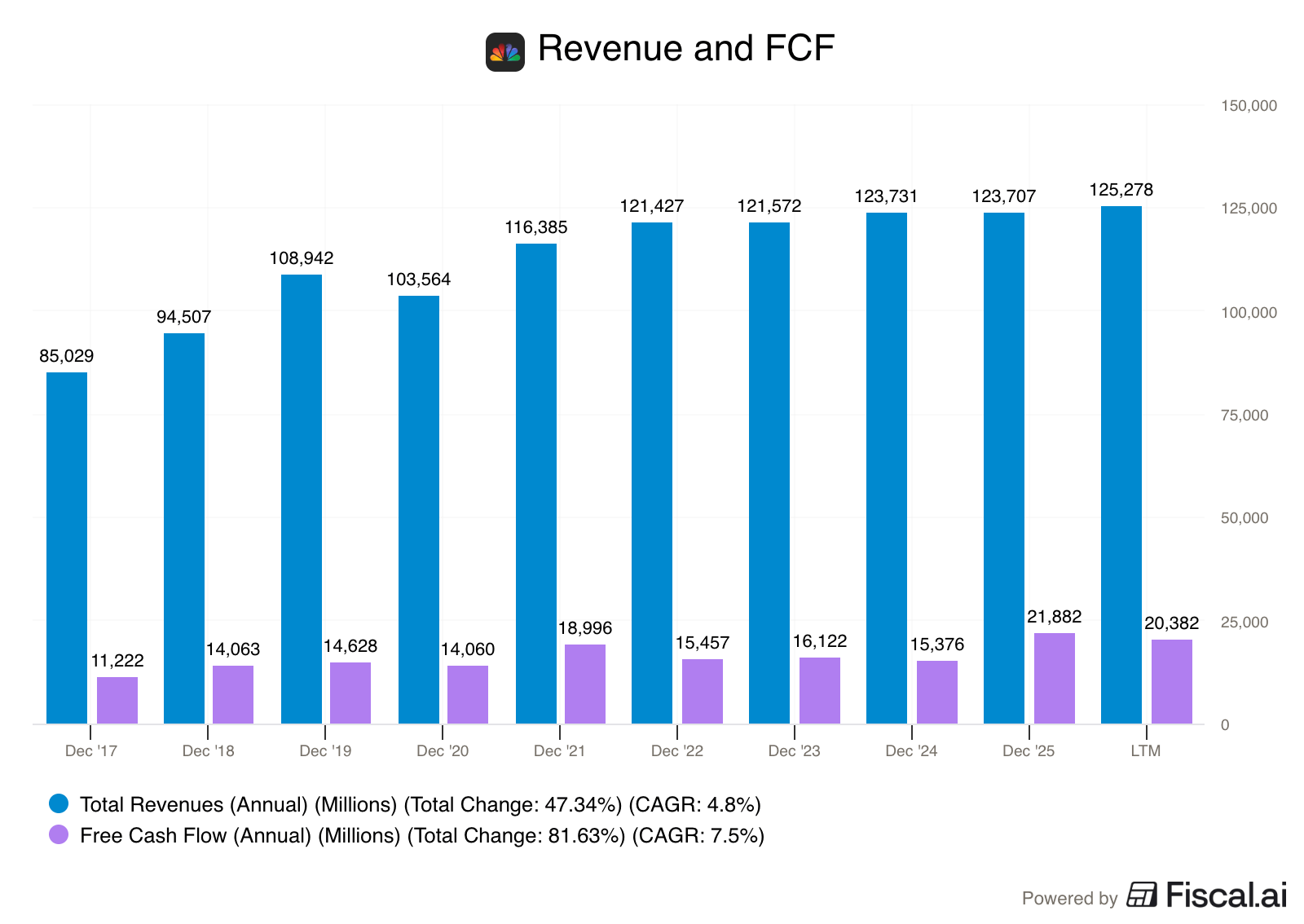

Overall, the business shows slow, steady revenue growth and a lot of FCF.

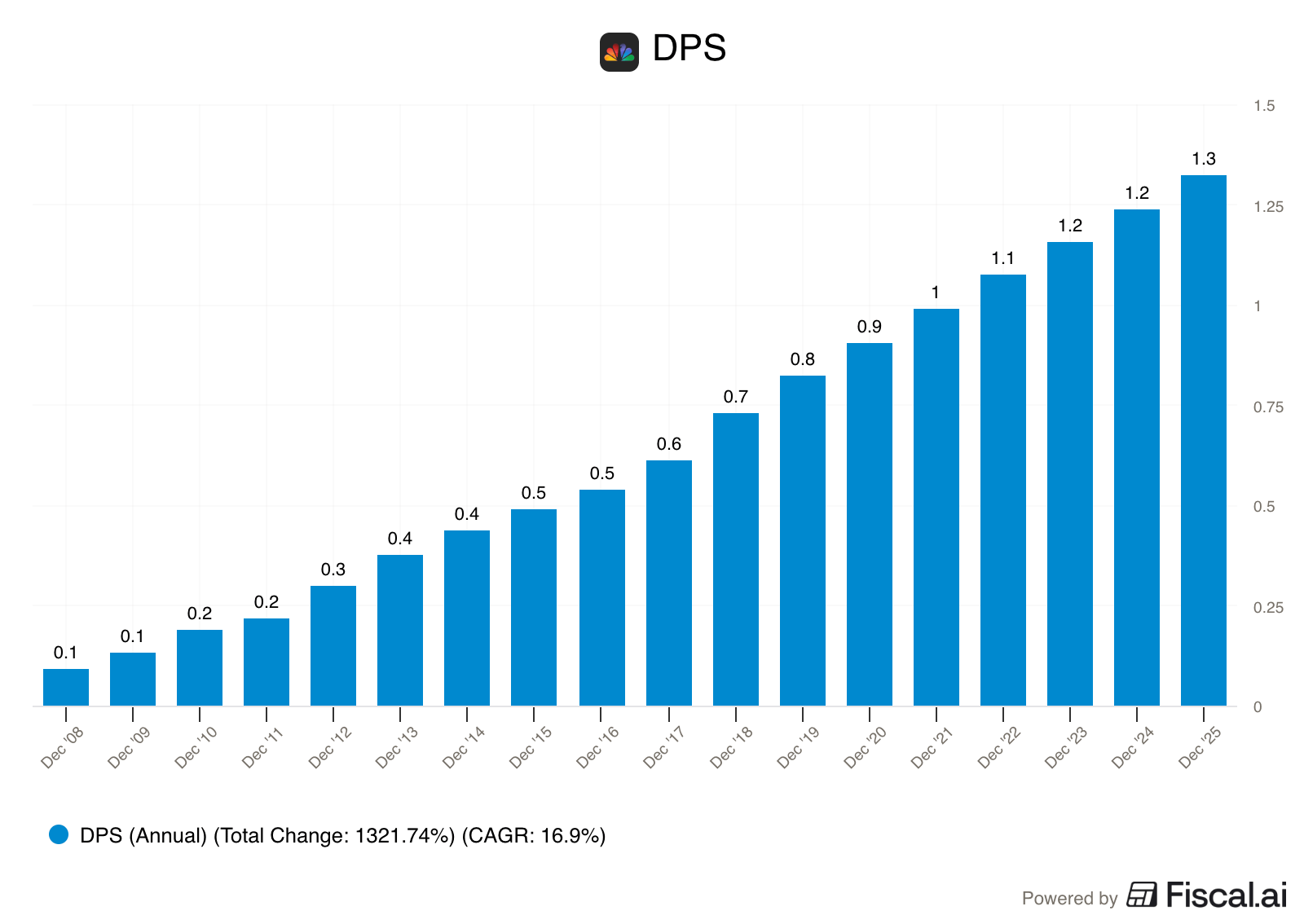

That's allowed Comcast to pay a growing dividend for 18 years now.

Comcast’s Problems

The company wouldn’t be splitting itself up if things were going well.

Let’s talk about the main issues with Comcast.

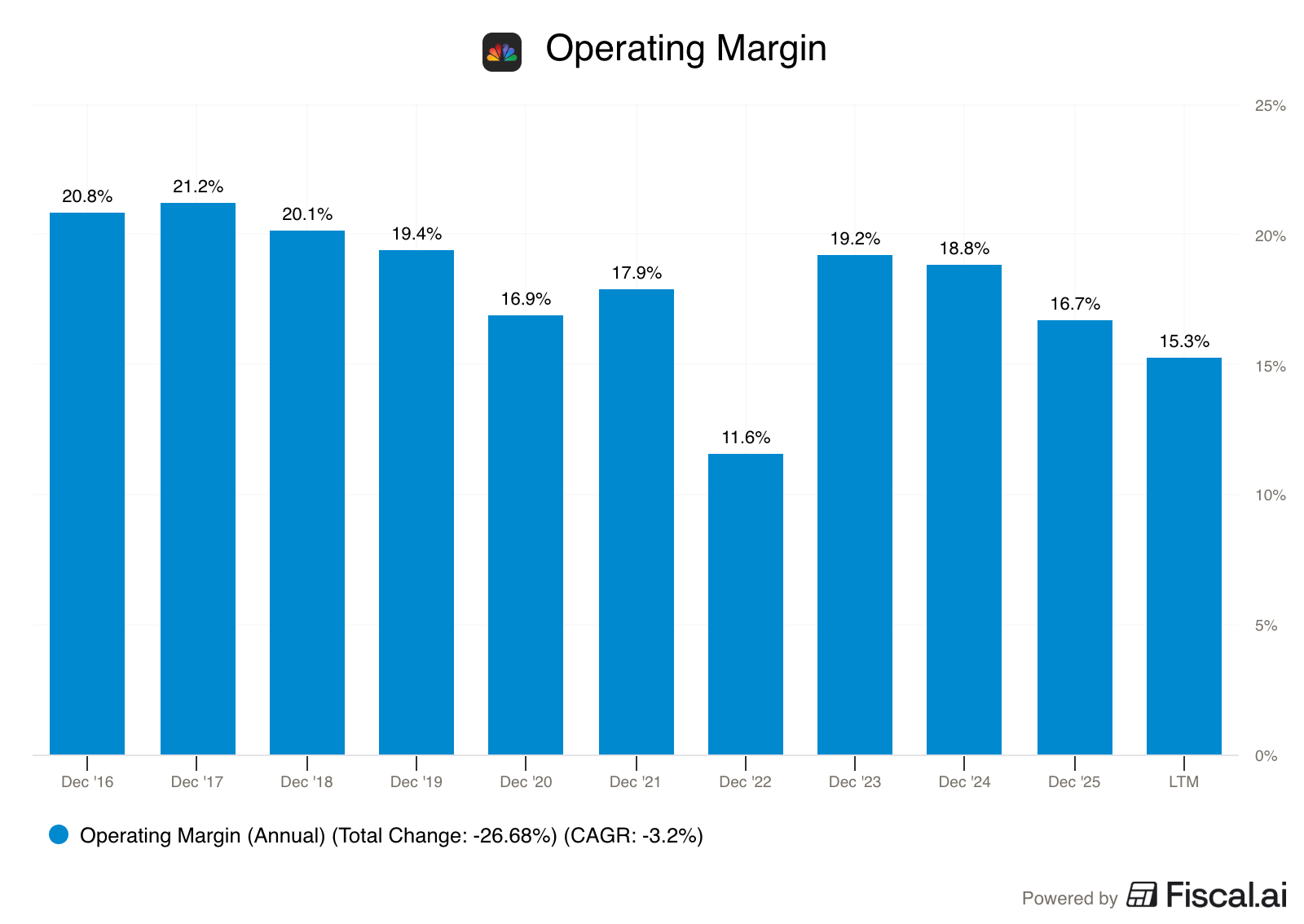

1. Broadband

The broadband network is the main cash generator.

But it’s losing customers to aggressively expanding fiber networks (like AT&T) and 5G fixed-wireless options (like T-Mobile and Verizon).

The competition has forced Comcast to compete on price, and incentives like giving away a year of free wireless to keep accounts.

This is hurting their profit margins.

2. Streaming

Streaming is taking traditional cable TV subscribers.

To fight back, Comcast is burning massive amounts of cash on the Peacock streaming service and expensive sports rights (like the NBA).

Peacock is still losing money, and is small compared to most competitors.

Investors aren’t happy that Comcast keeps pouring broadband cash into a streaming war that Comcast isn’t winning.

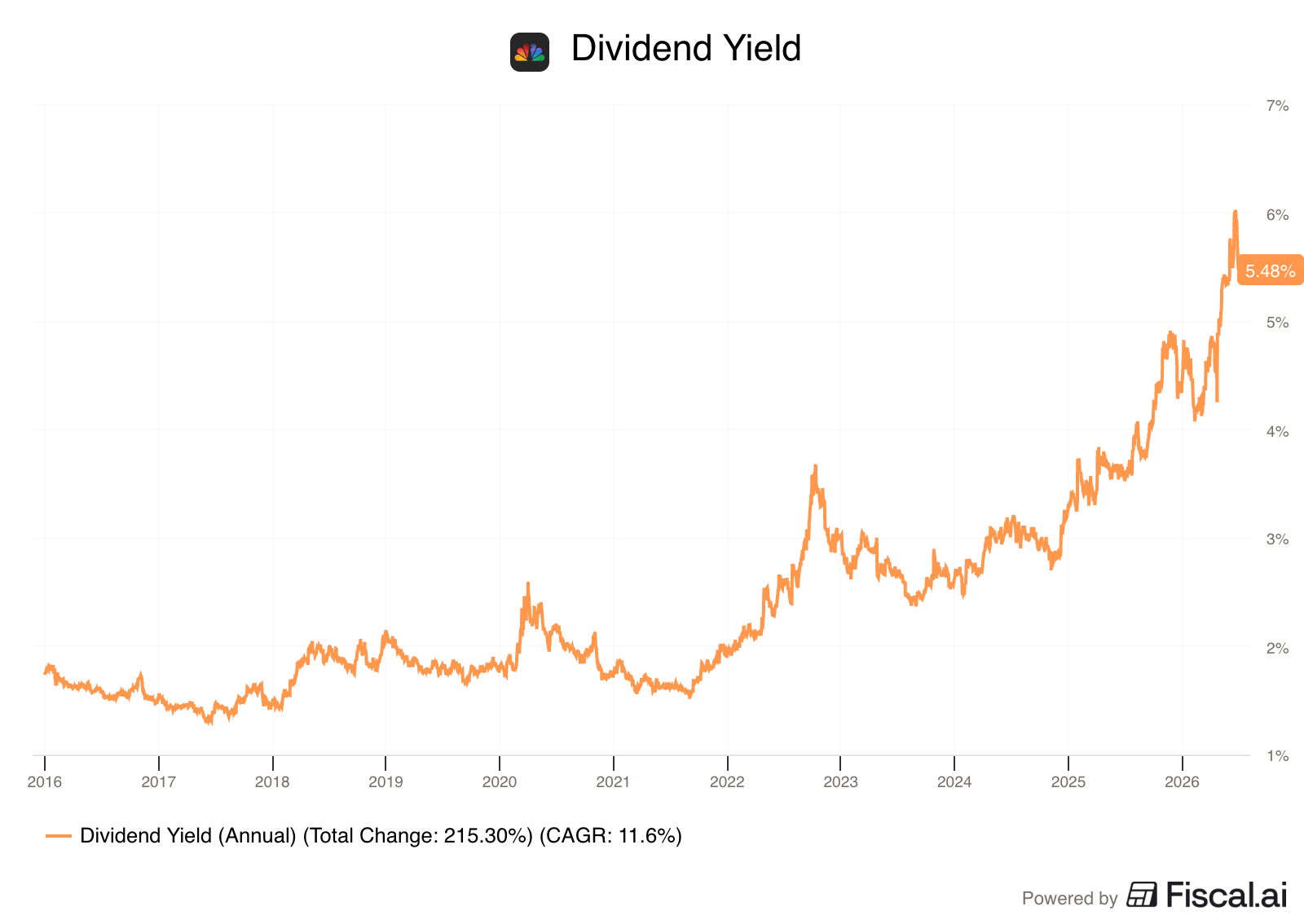

3. The Conglomerate Discount

Investors always have a hard time valuing complex businesses.

Investors have been viewing Comcast as a slow growing broadband business that pours cash into movie and streaming studios.

The stock price started declining in 2021, and hasn’t stopped.

That’s driven Comcast’s dividend yield up to record levels.

Investors seem to be pricing in the worst-case scenario for both halves of the business at the moment.

That’s why management is looking to split the business.

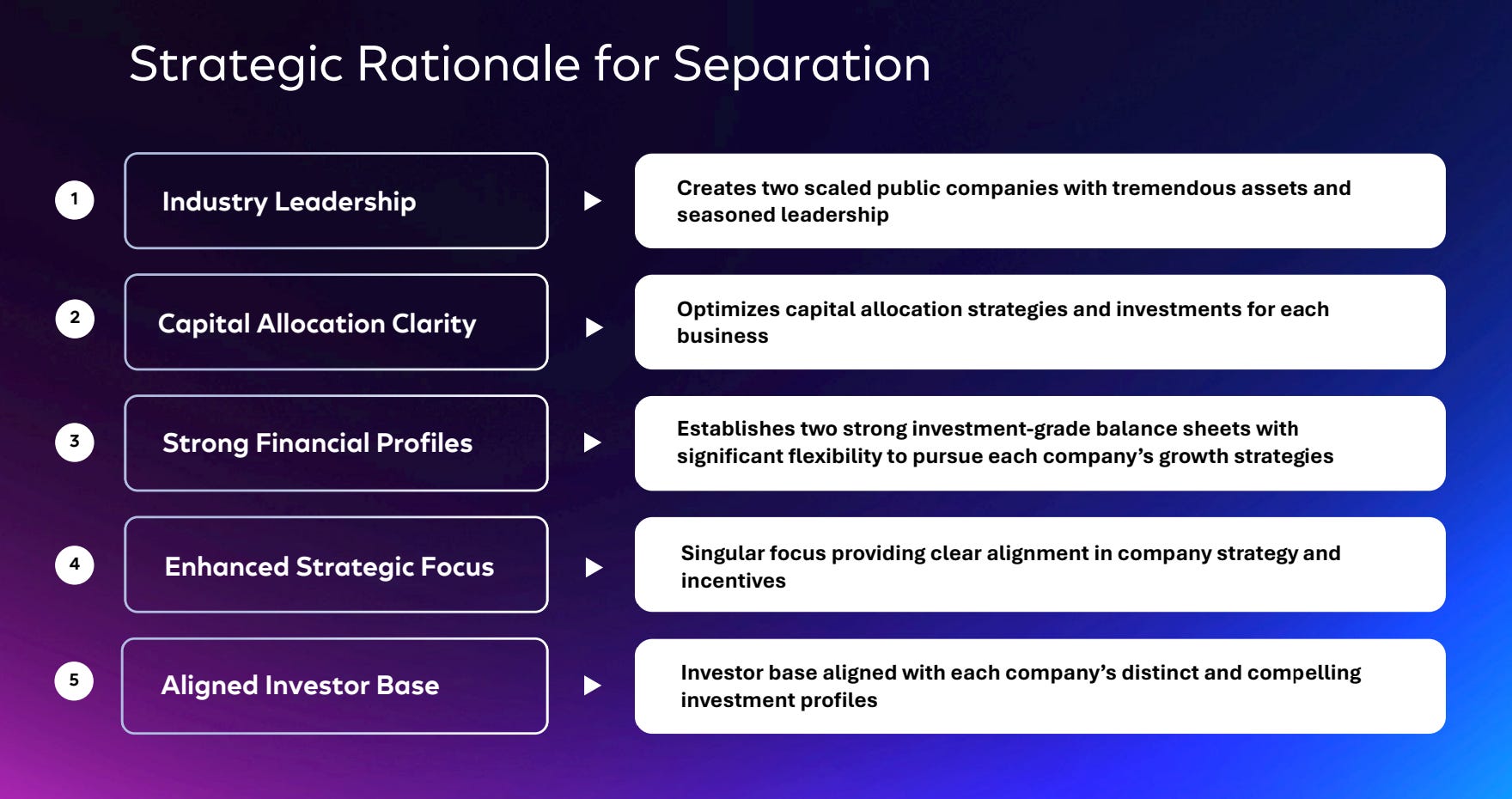

It will let investors value the broadband and media businesses independently.

It will also let the businesses operate independently, which should simplify capital allocation and business strategy.

The Split

Management will use a tax-free spin-off that’s expected to close in about a year to split the businesses.

‘New’ Comcast: will keep the connectivity business, including residential broadband, Xfinity Mobile, and Comcast Business.

NBCUniversal (SpinCo): will take the media assets: the film and TV studios, Universal theme parks, broadcast networks, Peacock, and Sky.

Let’s briefly look at each business.

‘New’ Comcast

The cable and broadband business is what generates most of Comcast’s cash.

It has significant scale advantages over competitors

Even with a slow decline in the number of subscribers, Comcast has been able to maintain stable revenue from this business

This business has been essentially subsidizing the media side’s expansion.

As an independent business, ‘New’ Comcast will be completely focused on returning capital to shareholders and defending its network.

NBCUniversal

The main profit drivers for NBCUniversal will be the theme parks and its iconic intellectual property (like the Jurassic World franchise, The Office, and Minions).

But this business will still continue to consume a lot of capital.

The traditional TV networks are losing subscribers

And the Peacock streaming service has been operating at a loss (management expects it to hit profitability in the next few years)

There’s probably more growth opportunity here, but there’s also more risk.

As an independent company, NBCUniversal will be able to consider mergers, acquisitions, or partnerships as the media space continues to consolidate.

It would not have the same opportunities if it were still tied to a telecom company.

Could Comcast Be Interesting?

I’ve already showed you that it’s at a very high dividend yield relative to its own history.

From here, the story gets really interesting.

To find out if Comcast is truly a screaming buy or a value trap, we have to run the hard numbers.

In the rest of this deep dive for Premium Partners includes:

The Reverse Dividend Discount Model (DDM): See exactly how low the market’s dividend growth expectations are right now.

The Reverse DCF Model: What kind of FCF growth (or not) the market is currently pricing in.

The Sum-of-the-Parts Valuation: We break down the standalone earnings for both ‘New’ Comcast and NBCUniversal, pick some peer multiples and figure out if you’re really getting a discount today.

📈 Unlock the Full Comcast Valuation Breakdown

Don’t invest blindly on corporate narratives.

Upgrade to Premium to read the full valuation breakdown, and

Get access to all of Our Deep Dives

Our Dividend Growth Portfolio

Our High Yield Portfolio

The Community

And much more!

One Dividend At A Time

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.