🔥 Stock Idea: Americold Realty Trust

Americold is the second-largest owner of cold storage warehouses in the world, a critical part of the global food supply chain.

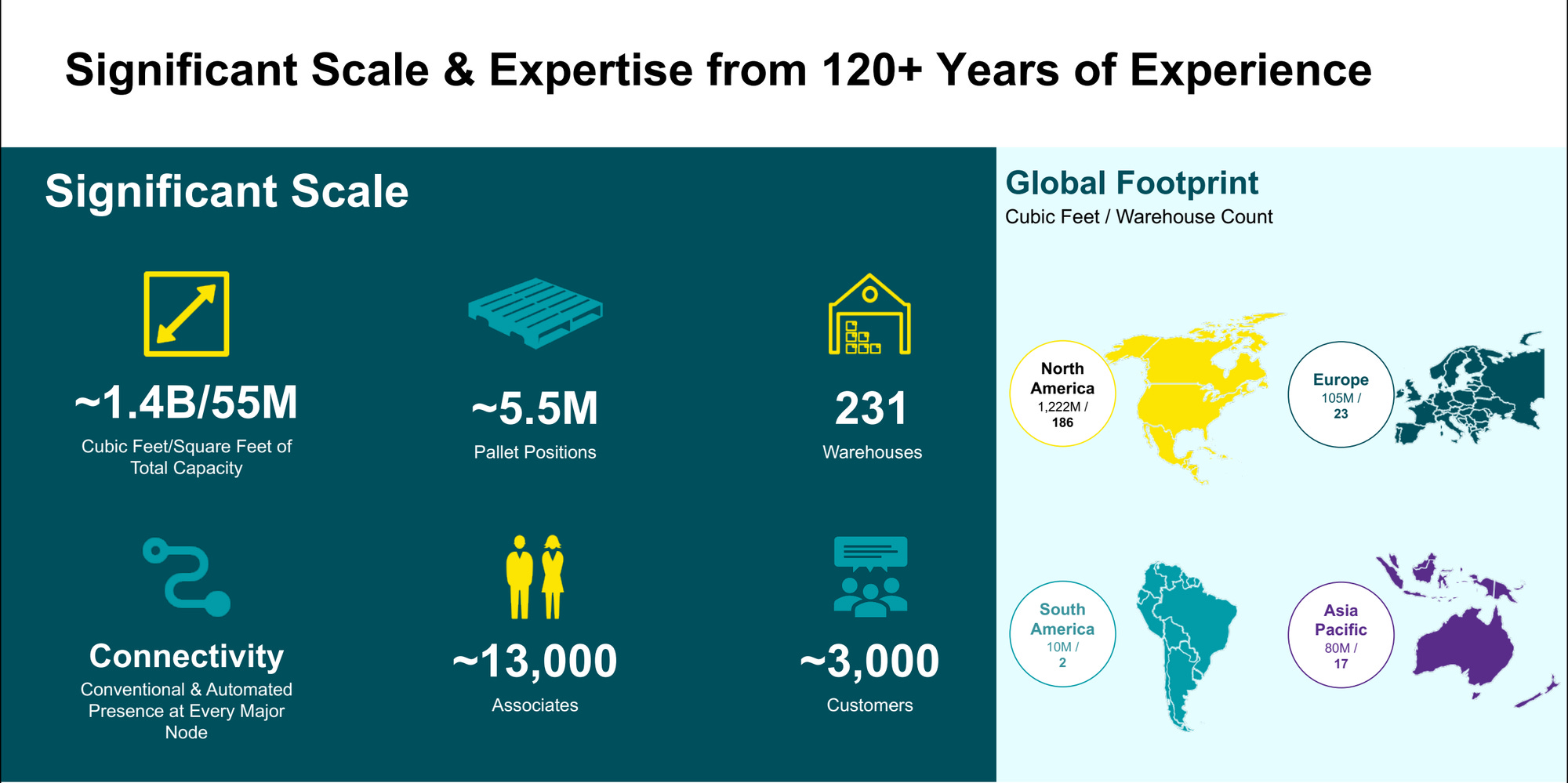

It operates a massive network of over 230 facilities, serving thousands of food producers and retailers.

Despite being an industry leader, it’s facing a perfect storm:

Oversupply: Competitors built too many warehouses recently (estimated at 15% of capacity over the last five years, compared to demand growth of 5%), driving down prices.

Weak Demand: Consumers are buying less food due to inflation and the reduction of government benefits (like SNAP), so companies are storing less.

Labor & Power Costs: It takes a lot of people and energy to run these freezers. Wages and electricity prices have gone up.

Debt: As a REIT, it relies on debt, and interest rates have hurt.

All of this means the stock has crashed, pushing the dividend yield to over 7%.

Is this a value trap or a generational buying opportunity in a critical asset class?

Let’s find out!

Americold Realty Trust

Company name: Americold Realty Trust

✍️ ISIN: US03064D1081

🔎 Ticker: $COLD

📚 Type: High Yield Stock

📈 Stock Price: $12.10

💵 Market cap: $3.49 billion

📊 Average daily volume: $69 million

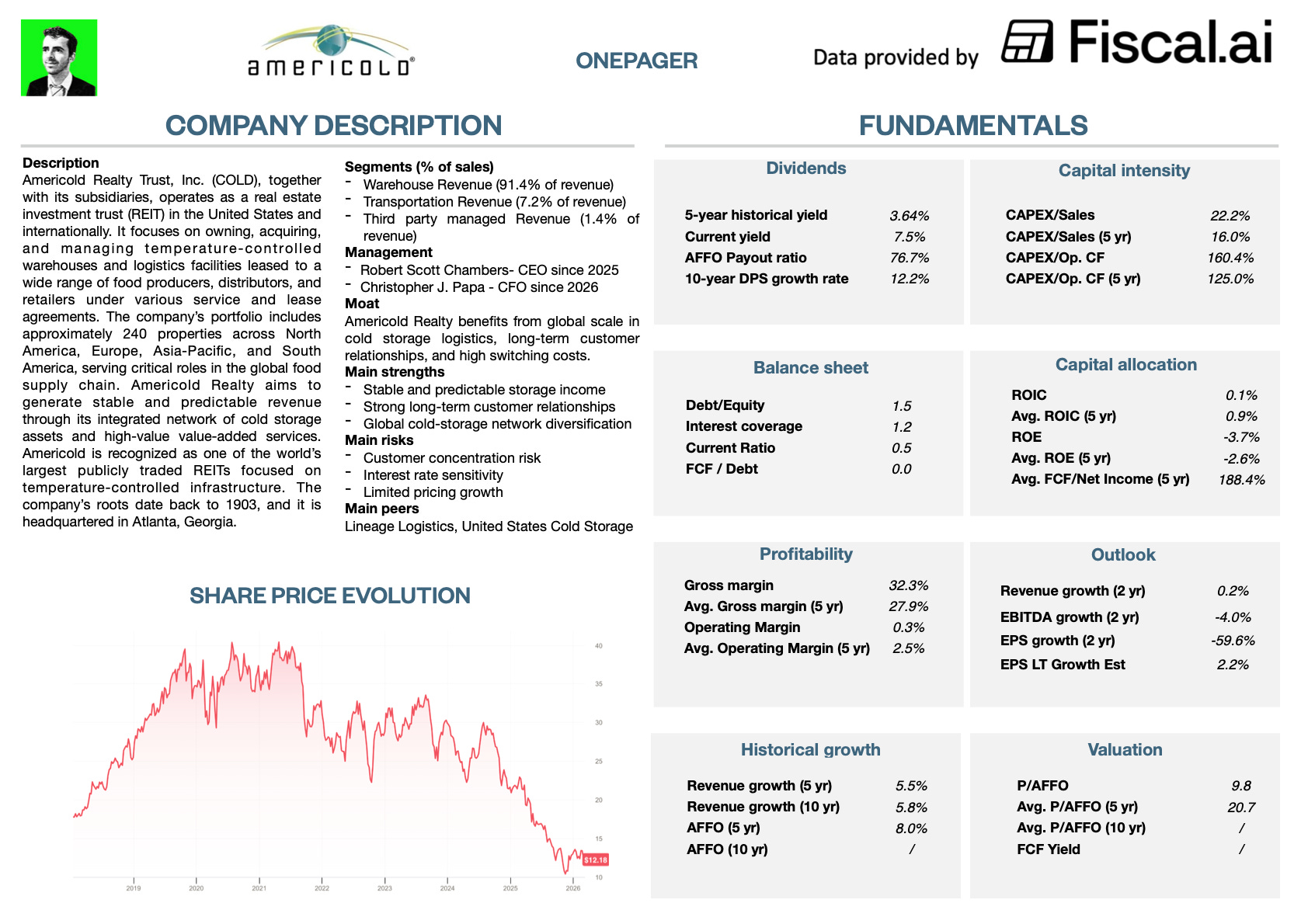

Onepager

Don’t know Americold Realty Trust?

Here are the basics (click on the picture to expand):

Now let’s dive into the full investment case!

1. Do I understand the business model?

Americold owns and operates temperature-controlled warehouses full of giant freezers and refrigerators that are critical to the food supply chain.

They store food for producers (like Conagra or Kraft Heinz) before it goes to grocery stores (like Kroger or Walmart) or restaurants.

In addition to renting them the space, Americold also provide services like freezing, packing, and transporting goods.

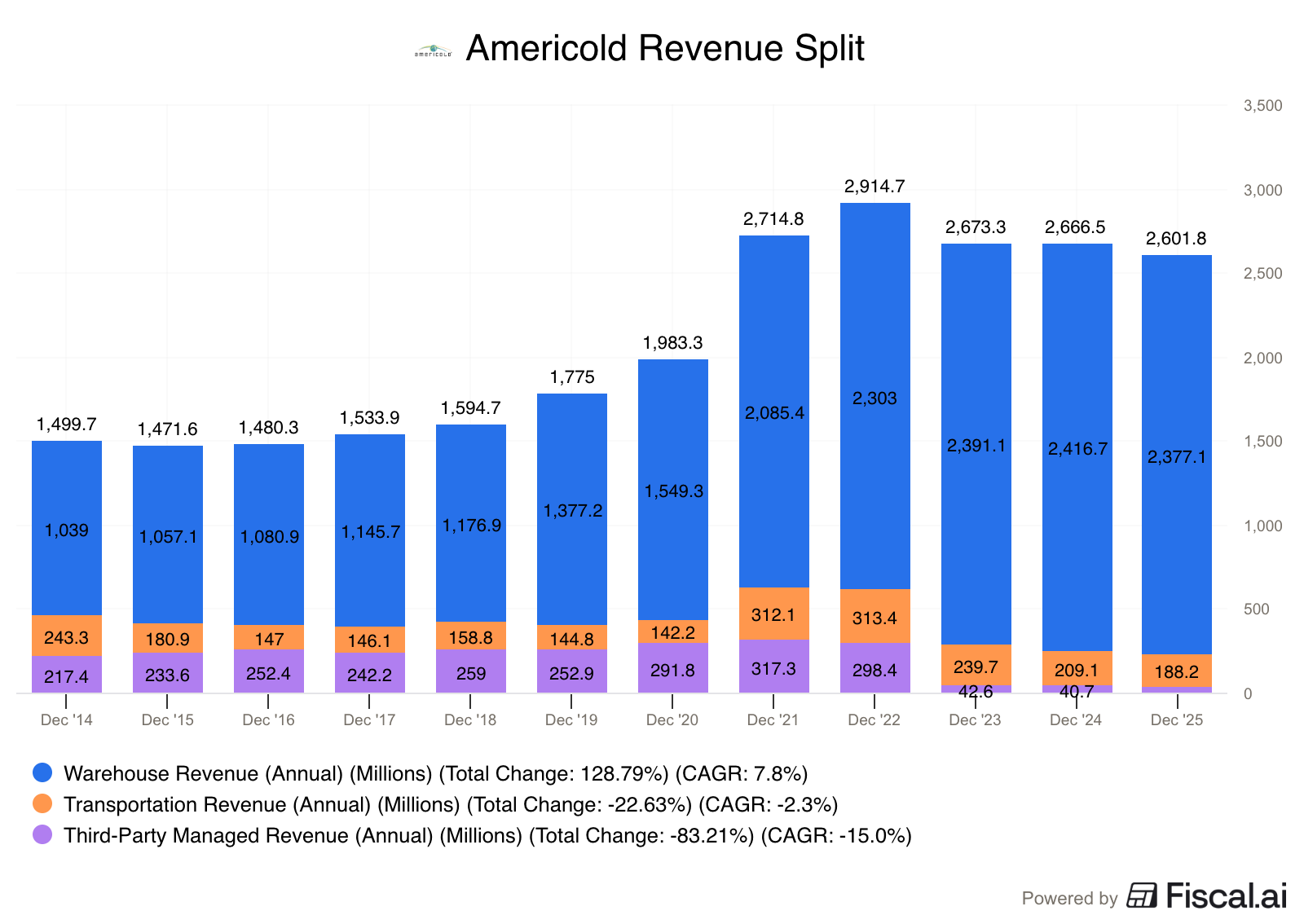

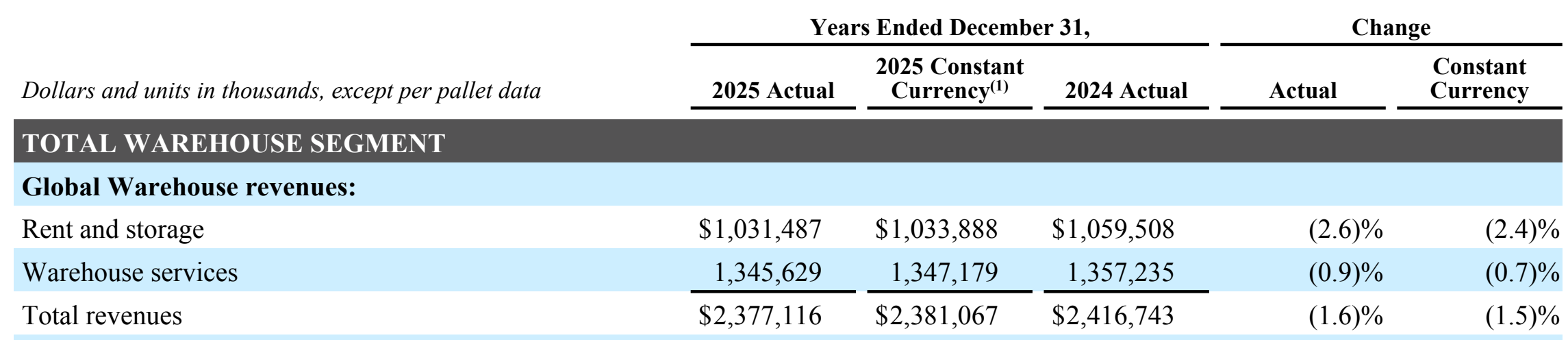

Revenue Split

Most of the revenue comes from renting out cold storage space and the services provided within those warehouses.

Here’s how the revenue breaks down:

Warehouse Rent, Storage & Services: $2.38B (91.4%)

Transportation: $188M (7.2%)

Third-party Managed: $36.5M (1.4%)

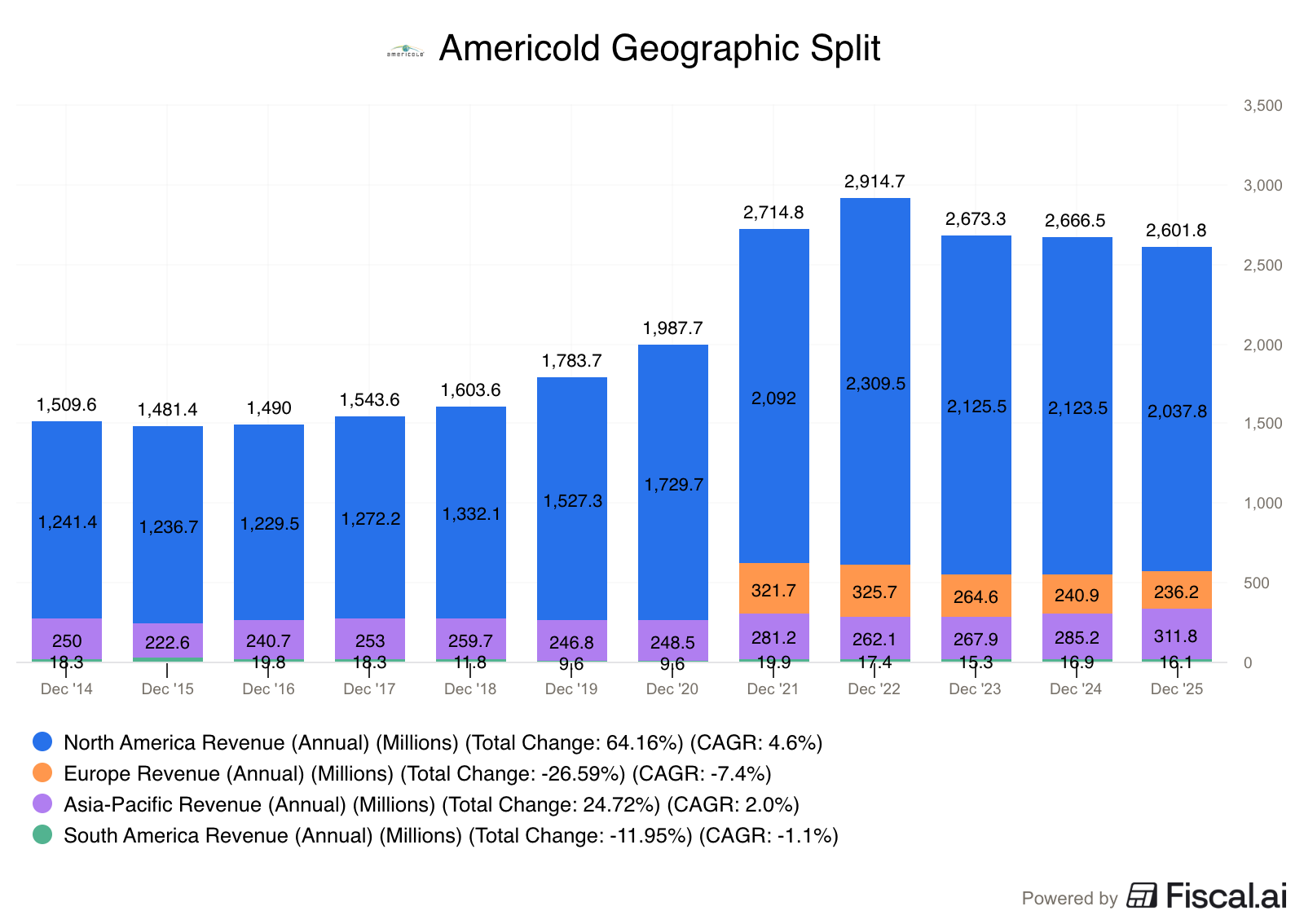

Geographic Split

While they are a global company, the vast majority of their business is in North America.

North America: 78% of revenue ($2.04B)

Asia-Pacific: 12% of revenue ($312M)

Europe: 9% of revenue ($236M)

South America: 1% of revenue ($16M)

Who are the customers?

Americold serves approximately 3,200 customers involved in the food industry. This includes:

Food Producers: Companies that make frozen and perishable foods (fruits, vegetables, meats, dairy).

Retailers & Distributors: Grocery store chains, food distributors, and e-commerce companies.

The top 25 customers account for more than 50% of warehouse revenue, and these relationships are very sticky, averaging 39 years.

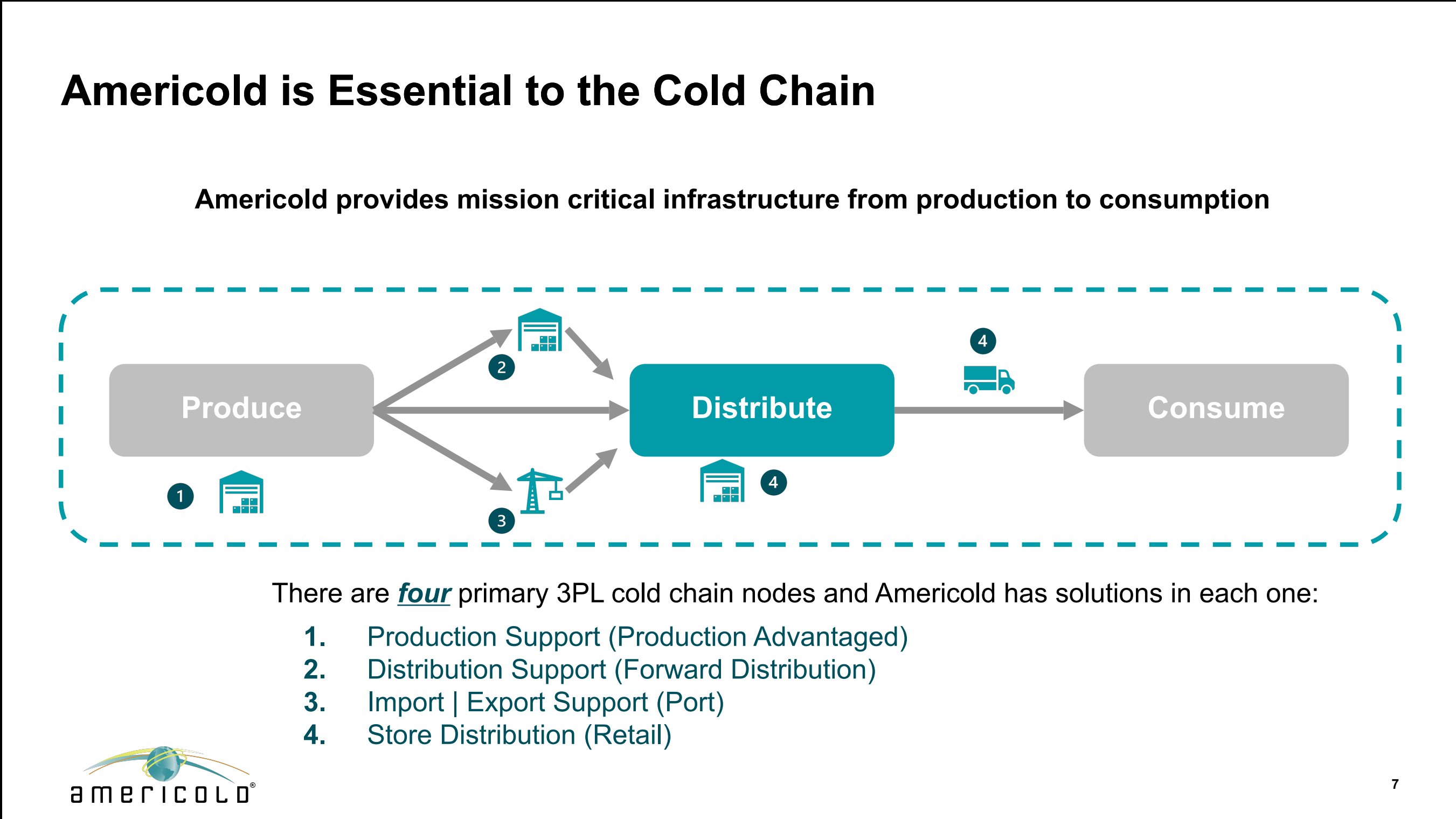

What’s the moat?

Americold’s moat comes from its scale and integration.

In the cold storage business, location and network density matter.

Americold has facilities in every key node of the supply chain: right next to food production plants, in major distribution hubs, and at ports.

This creates a few advantages:

High Switching Costs: 26% of their sites are production-advantaged, meaning they are physically connected or right next to a customer’s factory. It is incredibly expensive and logistically difficult for a customer to move to a competitor when the warehouse is literally attached to their building.

Network Density: With 239 facilities, they can offer national/global solutions to massive food companies that smaller regional players can’t match.

Fixed Commitments: To protect against volatility, Americold has successfully shifted 60% of its rent and storage revenue to fixed commitment contracts. This means customers pay for the space whether they use it or not, stabilizing cash flow significantly.

Americold also offers specialized services, that make up more than half of the warehouse revenue.

These are complex handling and repackaging tasks that involve breaking down large shipments into smaller, order-specific units.

Unique Handling Services Include:

Case-Picking and Kitting: Breaking down pallets to select individual cases or assembling specific kits for retail or restaurant delivery.

Protein Boxing and Repackaging: Handling raw or processed proteins and placing them into retail-ready or restaurant-ready packaging.

Produce Grading and Ripening: Using specialized rooms to control the ripening process of fruits (like bananas or avocados) before they are sent to grocery stores.

Blast Freezing: Rapidly lowering the temperature of fresh products to preserve quality for long-term storage or international transit

Customers who take advantage of these services have even higher switching costs.

2. Is management capable?

Robert Chambers - CEO

Mr. Chambers became CEO in 2025 but is a veteran of the company.

He previously served as Chief Commercial Officer and has been with Americold in various leadership roles since 2013.

He has deep experience in the logistics and supply chain industry.

Chris Papa - CFO

Mr. Papa was appointed as CFO in 2026.

He’s been in real estate and corporate finance for almost 40 years.

Before joining Americold, he was CFO at CenterPoint Properties, Liberty Property Trust, and Post Properties

The management team at Americold has a lot of industry experience.

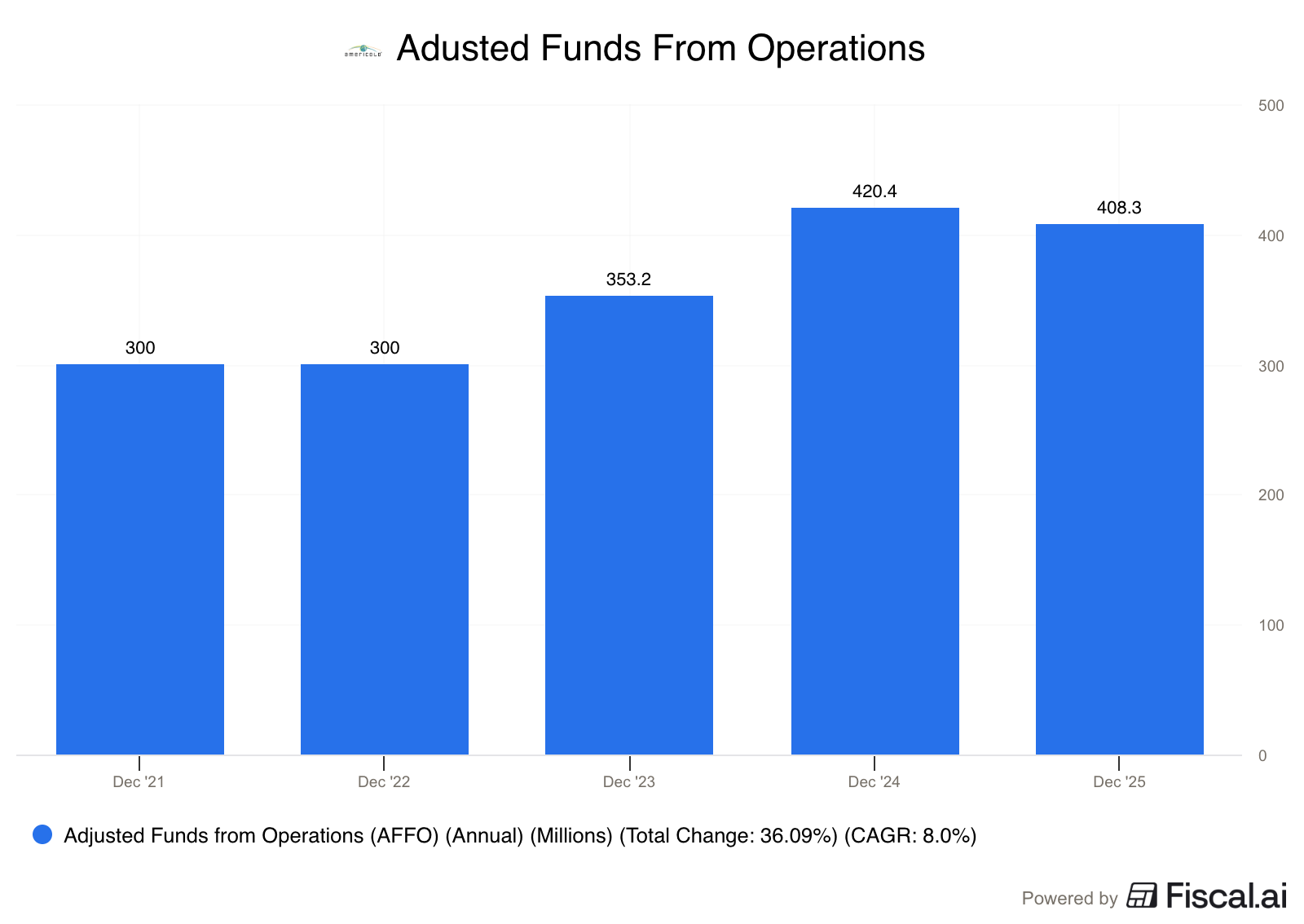

The management at Americold has grown the company’s AFFO at about 8% per year.

3. Has the company grown the dividend attractively?

We look for:

At least 10 years of dividend growth

5-year dividend growth rate of at least 3% (to keep up with inflation).

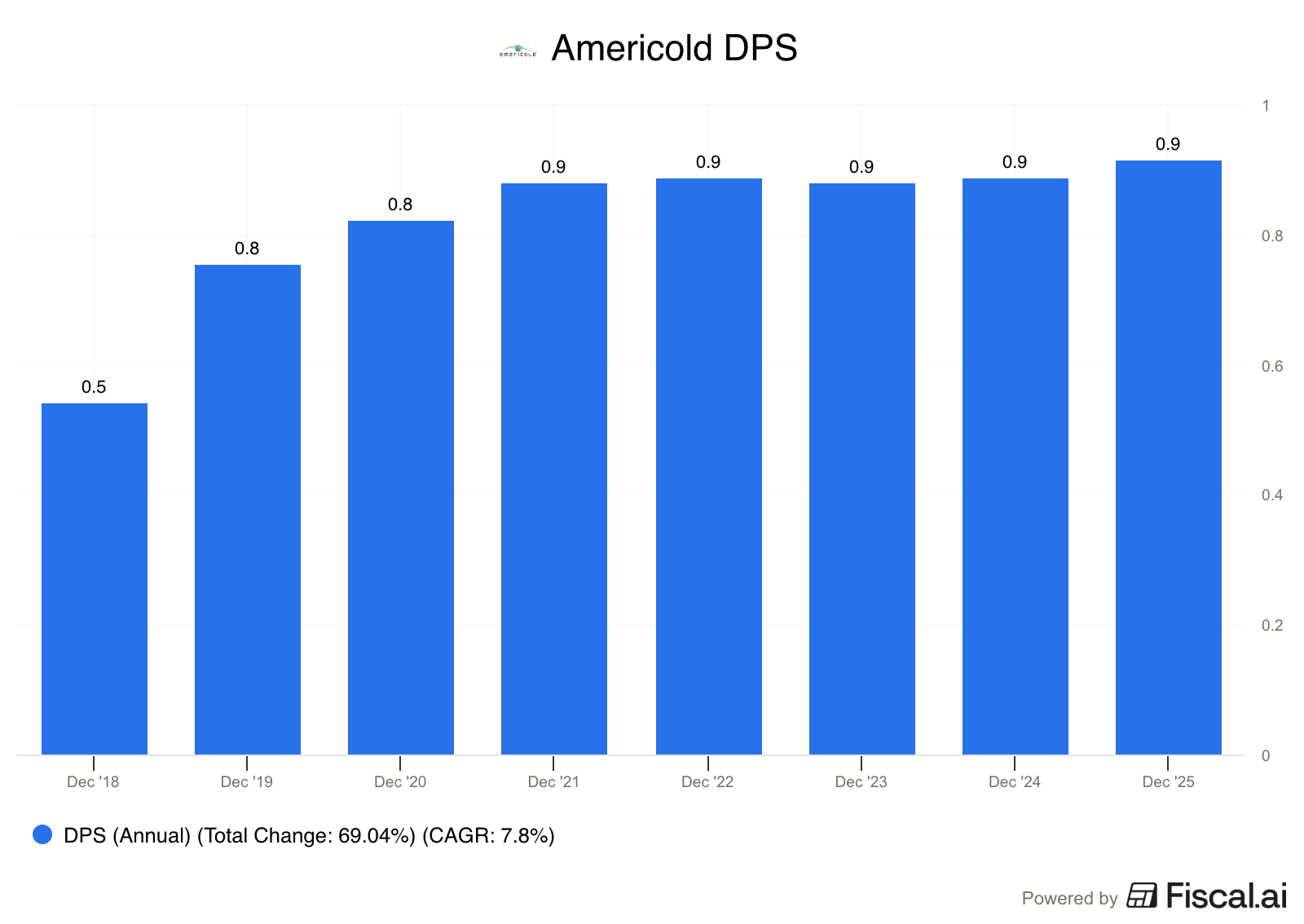

Americold went public in 2018, and has paid dividends consistently since then but has not raised them every single year.

They have grown the dividend by 2.3% per year over the last 5 years, but if we look back to their IPO, the dividend growth rate is 7.8%.

The dividend was raised 5% in January of 2026.

4. Is the company active in an attractive end market?

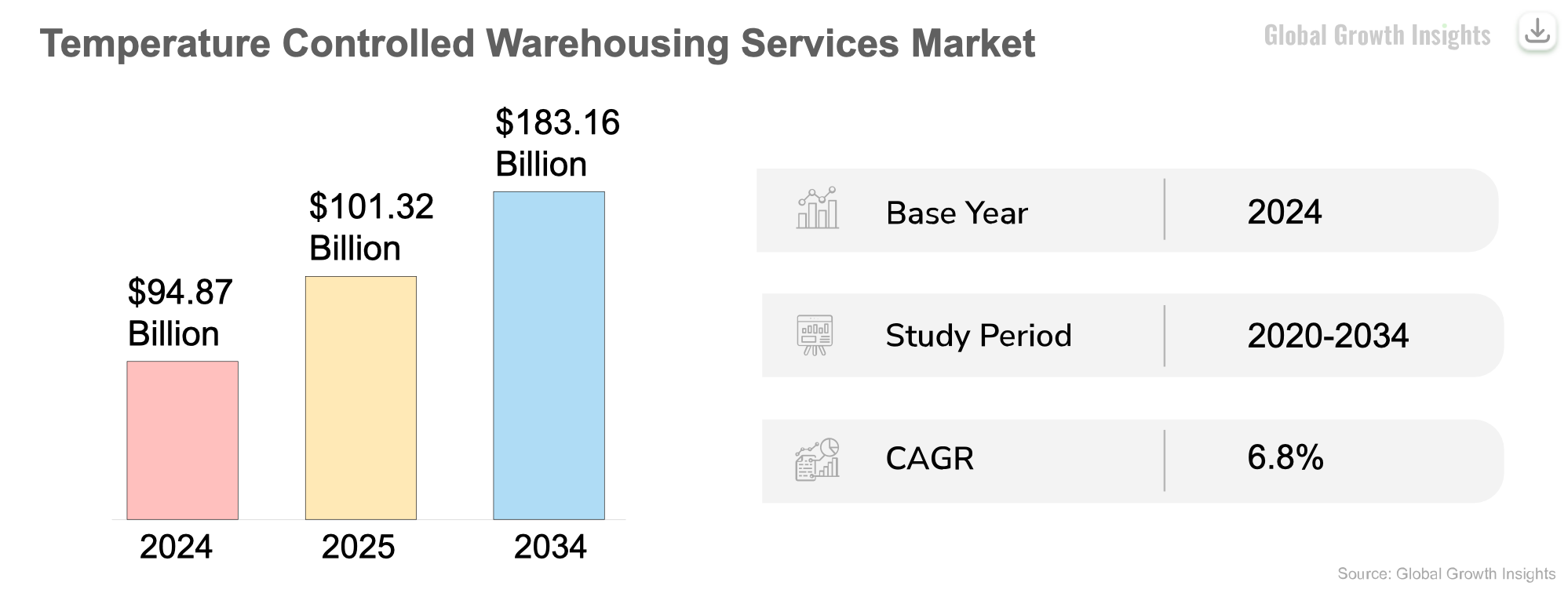

The temperature-controlled warehouse market is generally stable and growing, driven by food consumption.

The projected growth rate of the market is 6.8% per year.

It’s an attractive market because:

Food is Essential: Demand for food is relatively inelastic - people eat regardless of the economy.

Outsourcing Trend: Food producers and retailers increasingly prefer to outsource their cold storage needs rather than owning and operating their own expensive freezers.

Demographics: Population growth and urbanization drive demand for frozen and perishable foods.

5. What are the main risks for the company?

Oversupply & Competition

Competitors (like Lineage Logistics and new developers) built a lot of new warehouses recently. This excess supply is driving down occupancy and limiting how much Americold can charge.

Mitigation: Americold focuses on production-advantaged sites (attached to factories) which are harder to replicate and have stickier customers. The market is also growing, so demand will eventually catch up to supply

Labor Costs & Availability

Running these warehouses requires a lot of labor. Wage inflation or labor shortages can squeeze margins.

Mitigation: They are investing in automation and technology (Project Orion) to make their operations more efficient and less dependent on manual labor.

Debt & Interest Rates

As a REIT, Americold carries significant debt. Higher interest rates increase their borrowing costs and can hurt profitability.

Mitigation: Most of their debt is fixed-rate, but they still have exposure. They are focusing on deleveraging and maintaining their investment-grade credit rating.

6. Does the company have a healthy balance sheet?

The real estate industry runs on debt. That means that we need to look at the balance sheet of a REIT a little differently than we do for a typical company.

We typically look at Debt/Equity, but that number can get skewed in a company that owns a lot of real estate.

Why?

Depreciation. Because of accounting rules, properties lose a lot of value on paper, even if they don’t in real life. That can make equity look artificially low and Debt/Equity artificially high.

So what do we look at instead?

That’s as far as we can go with this free preview.

Want the rest of the investment case, and to find out if Americold earns a spot in the Compounding Dividends or High Yield Portfolio?

You can join us here:

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.