🔥 Stock Idea: Colgate-Palmolive

During times of market turmoil, investors often run to consumer staples companies.

That’s because companies like Colgate-Palmolive provide stability and predictable dividend growth.

So, Is Colgate an interesting stock today? Let’s find out.

Colgate-Palmolive

Colgate-Palmolive is a global leader in household and personal care, serving consumers in over 200 countries.

Colgate is one of the most trusted toothpaste brands in the world.

It controls over 40% of the market and is a Dividend King with 63 consecutive years of dividend increases.

Founded in 1806, Colgate has grown from a small starch, soap, and candle business into one of the world’s most recognizable brands.

🎯 Company Name: Colgate-Palmolive Company

✍️ ISIN: US1941621039

🔎 Ticker: CL

📚 Type: Dividend Growth Stock

📈 Stock Price: $83

💵 Market Cap: $67 billion

📊 Average Daily Volume: $300 million

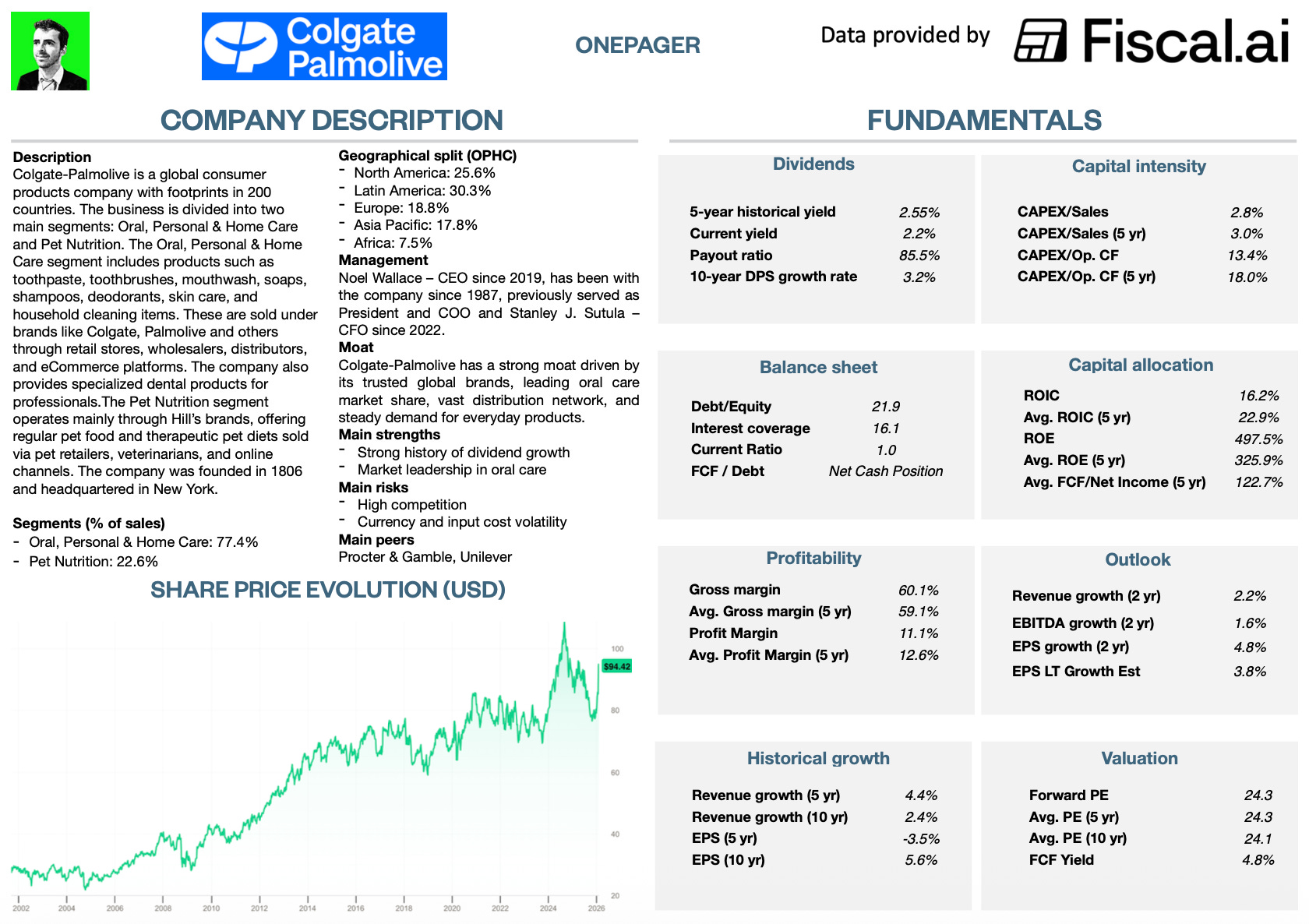

Onepager

Don’t know Colgate-Palmolive?

Here are the basics (click on the picture to expand):

1. Do I understand the business model?

Colgate-Palmolive is a diversified consumer goods conglomerate.

People think of them as a toothpaste company, but they have four core categories:

Main Business Segments

Oral Care: Includes toothpaste brands like include Colgate, Darlie, and elmex

Personal Care: Includes soaps, deodorants, and shampoos from brands like Palmolive, Softsoap, Irish Spring, and Protex

Home Care: Focuses on dishwashing liquids and household cleaners with brands like Ajax, Fabuloso, and Murphy Oil Soap

Pet Nutrition: Operates through Hill’s Pet Nutrition, providing specialized nutrition for dogs and cats through the Science Diet and Prescription Diet lines.

These are all products people need, and have to buy over and over.

This creates stable demand - something we love to see.

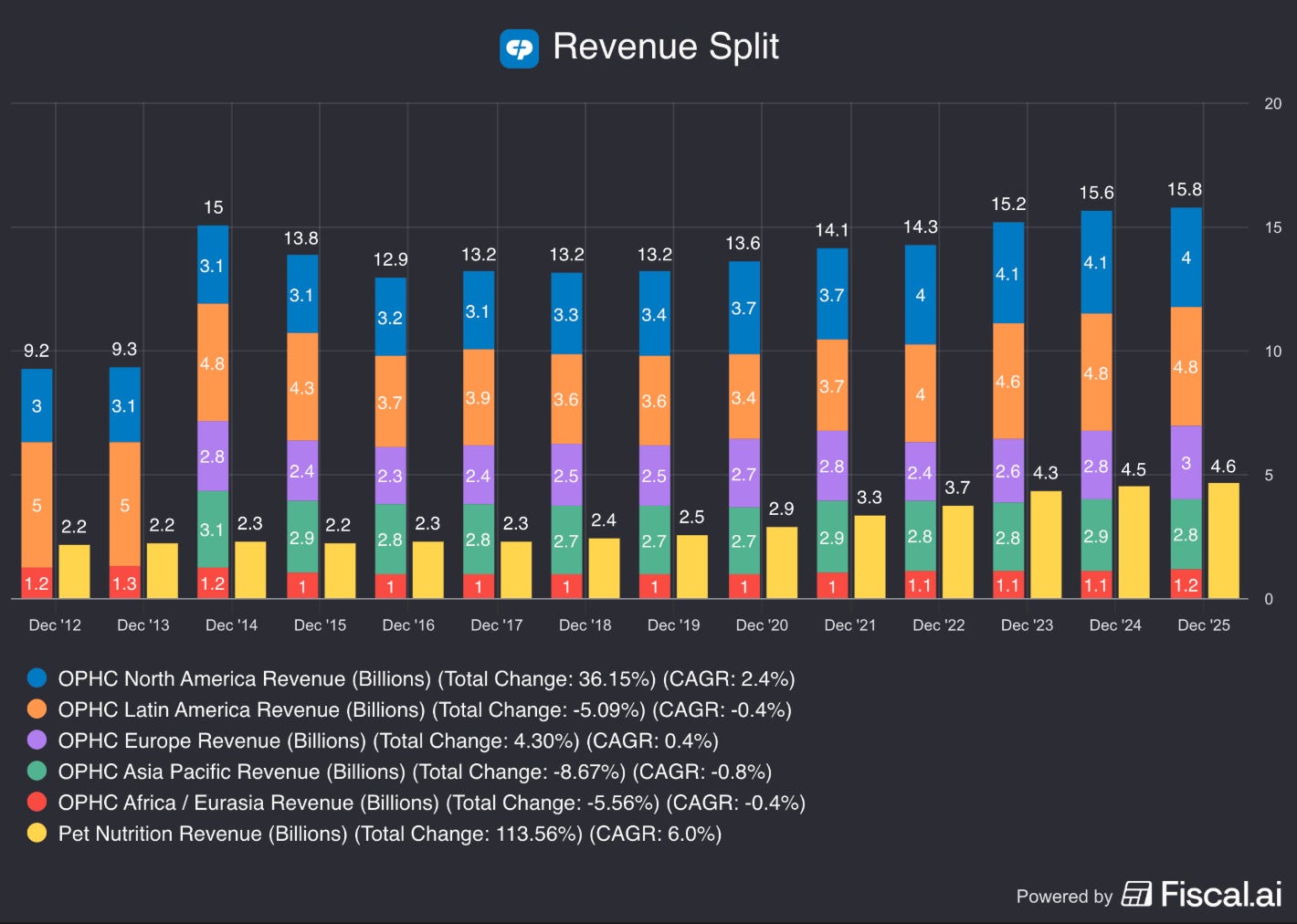

Revenue Split

Most of the revenue comes from Oral, Personal and Home care segment.

Here is the revenue split for fiscal year 2025:

Oral, Personal and Home care: $15.8 billion (77% of revenue)

Oral care: (43% of OPHC revenue)

Personal care: (17.8% of OPHC revenue)

Home care: (16.2% of OPHC revenue)

Pet Nutrition: $4.6 billion (23% of revenue)

Geographic Split

The geographic revenue mix has stayed largely stable over the years.

Latin America is the largest market, with North America next in line.

Asia and Africa contribute the smallest share of revenue.

What is Colgate’s Moat?

Colgate’s moat is built on two main strengths:

Strong brand power

Colgate is often the first name people think of for toothpaste, which keeps customers loyal and supports pricing power.

That is why it consistently ranks among the bestsellers in Amazon.

Global distribution

Its products reach deep into small towns and rural markets where many competitors have limited presence.

2. Is management capable?

You want to invest in companies led by great managers.

Noel Wallace - Chairman, President & CEO

Mr. Wallace has been with Colgate since 1987 and was appointed CEO in April 2019

Wallace has spent over 30 years at the company and has led major regions like North America, Latin America, and Africa–Eurasia

He is the architect of the company’s current 2030 Strategic Plan, which focuses on integrating digital and physical retail, and aggressively expanding into premium health categories

Under his leadership, annual sales crossed $20 billion in 2024, with organic sales growth continuing for six straight years through 2025

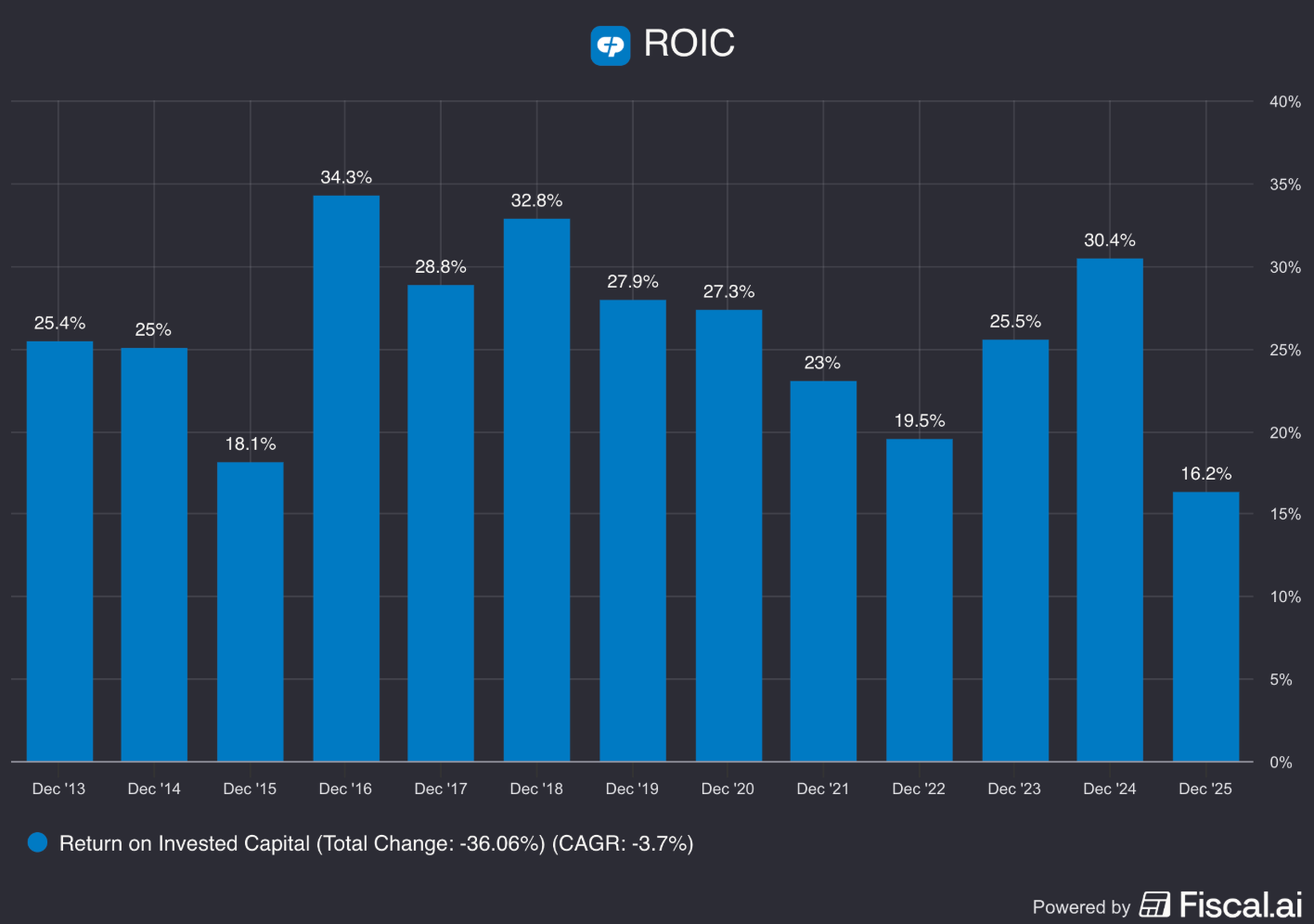

Colgate has consistently high ROIC numbers, showing us that management allocates capital well.

3. Has the company grown the dividend attractively?

You want to invest in companies with a history of growing their dividends.

The higher the dividend growth, the better.

We look for 2 things in the company’s dividend history:

At least 10 years of dividend growth

A 5-year record of growing dividends by 5% or more

Colgate:

Colgate is a Dividend King with 63 years of dividend growth

5-year dividend growth for Colgate is 3.3%, less then our target 5%.

4. Is the company active in an attractive end market?

You want to invest in companies that are in stable or growing market.

Here are a few characteristics we look for:

The company sells a necessary product

Recurring sales

A secular tailwind

Colgate meets all 3 of these qualities:

They sell necessary products like toothpaste, soap, and pet food

These are high-frequency consumables that must be replaced every few weeks

They benefit from people treating pets more like family through the Hill’s brand and from rising hygiene awareness in emerging markets

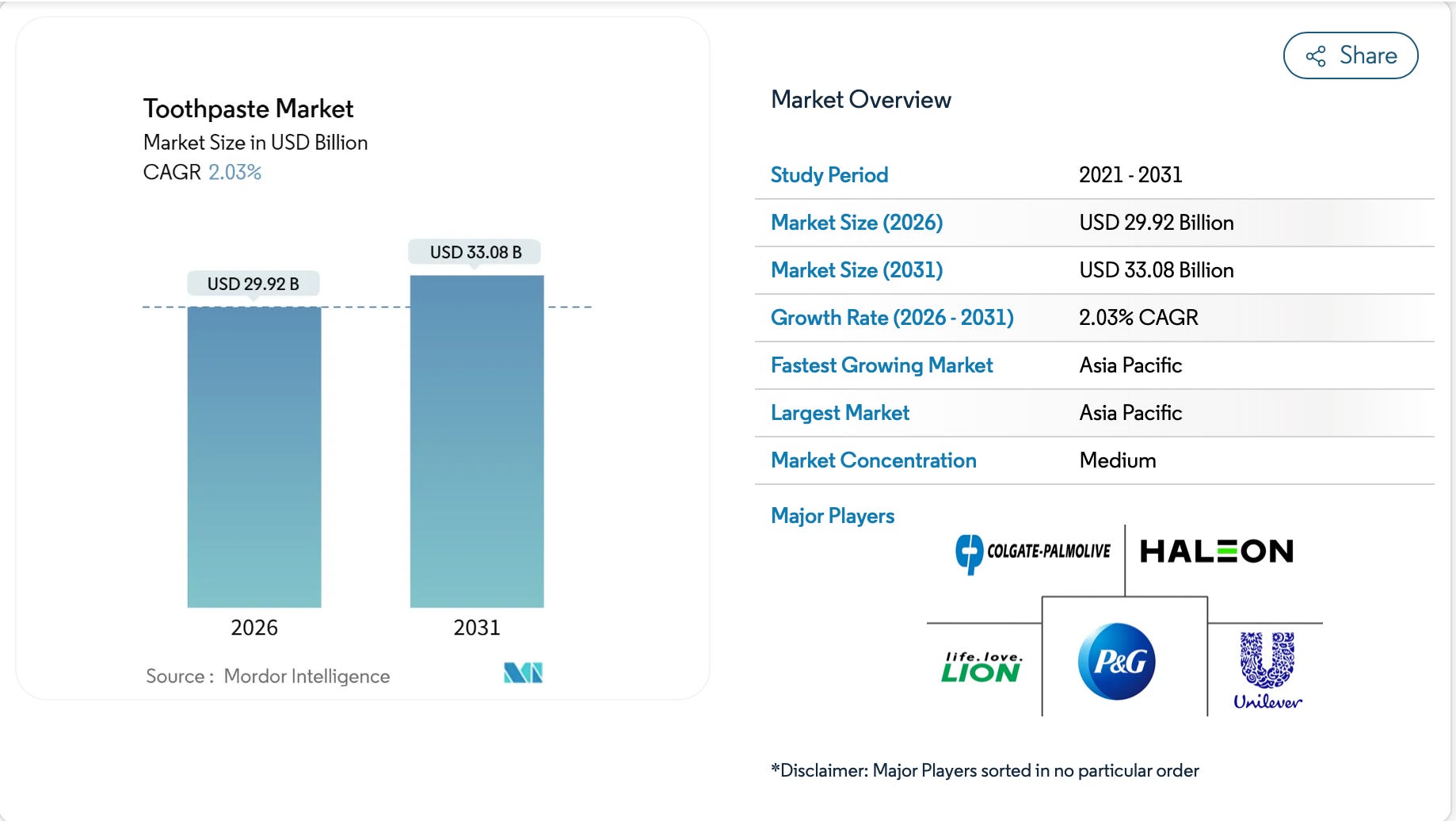

The market for consumer goods like toothpaste is slower growing, projected around 2% yearly growth.

But the pet food market is expected to grow more than 2x as fast, at around 5% per year.

5. What are the main risks for the company?

Competition

Colgate competes against massive global conglomerates with deep pockets:

Procter & Gamble (P&G): Their primary rival in oral care (Crest, Oral-B) and personal care

Unilever: A major threat in emerging markets with brands like Pepsodent and Dove

Mars & Nestlé: Intense competition in the pet nutrition space (Hill’s vs. Royal Canin and Purina)

Input Cost Volatility & Currency Risks

Colgate has its presence accoss the globe.

This does give them diversification, but it also exposes them to some risks:

Foreign Exchange (FX): When the U.S. dollar is strong, the money they earn abroad is worth less when converted back, which can eat into profits

Commodity Prices: Fluctuations in the cost of raw materials like essential oils and resins for packaging can directly impact their margins

Mature Business & Growth Uncertainty

Colgate is a highly established global brand. While this creates stability, it also brings growth limitations:

Slower Revenue Growth: Core oral care and personal care markets are already highly penetrated, limiting high growth potential

Dividend Growth Uncertainty: With earnings growing slowly and the payout ratio growing, the dividend may not grow as fast as it has in the past

Reinvestment Needs: Expansion into newer segments like pet care requires capital, which can temporarily reduce dividend flexibility

Now let’s dive into the most important part: the Fundamentals.

6. Does the company have a healthy balance sheet?

We always want to invest in financially healthy companies.

A strong balance sheet helps companies share profits with shareholders, stay flexible, and take advantage of opportunities.

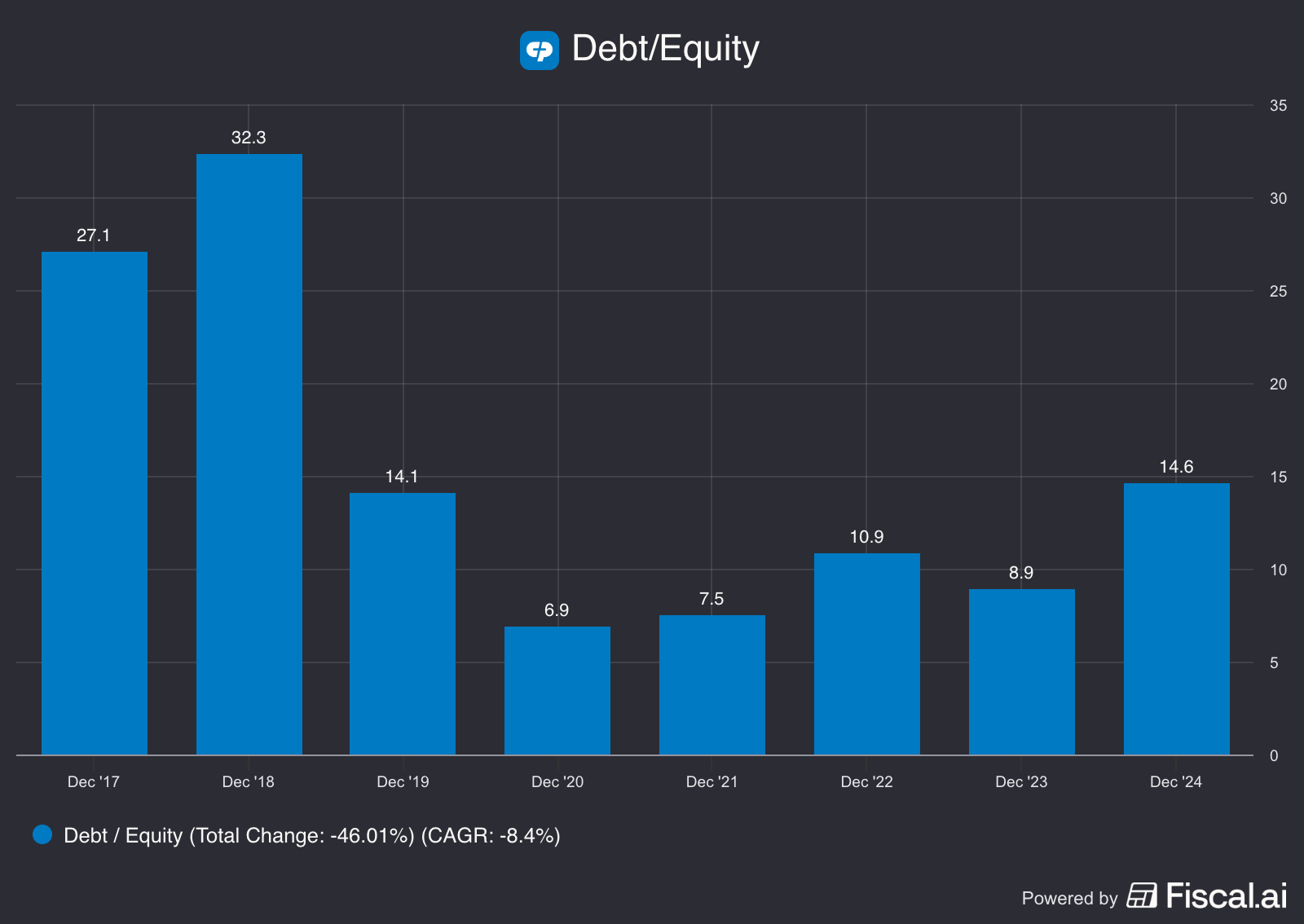

We typically like to see a Debt/Equity ratio of < 0.5.

Colgate’s has consistently been above this.

Part of the reason this level looks so high?

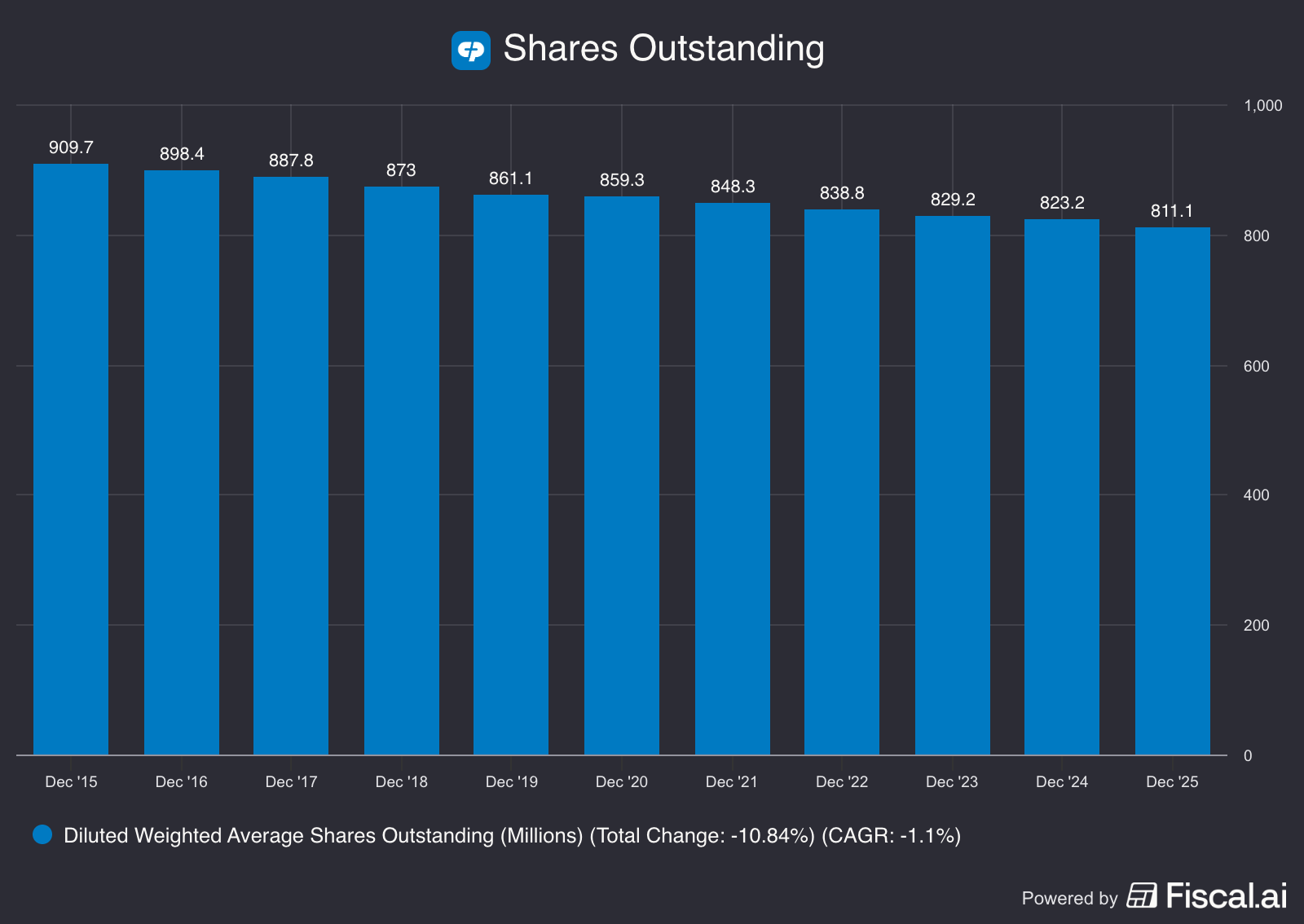

Colgate consistently spends $1 billion+ every year on buybacks, which lowers the equity portion of the calculation - this is a good thing!

Are the debt levels safe?

The reason we’re interested in debt is because it can bankrupt a company.

We look at a few ratios to get an idea to see if the debt levels are dangerous:

Interest coverage ratio: this tells us if GPC can afford the interest payments

Current ratio: tells us if they might have trouble meeting upcoming debt obligations

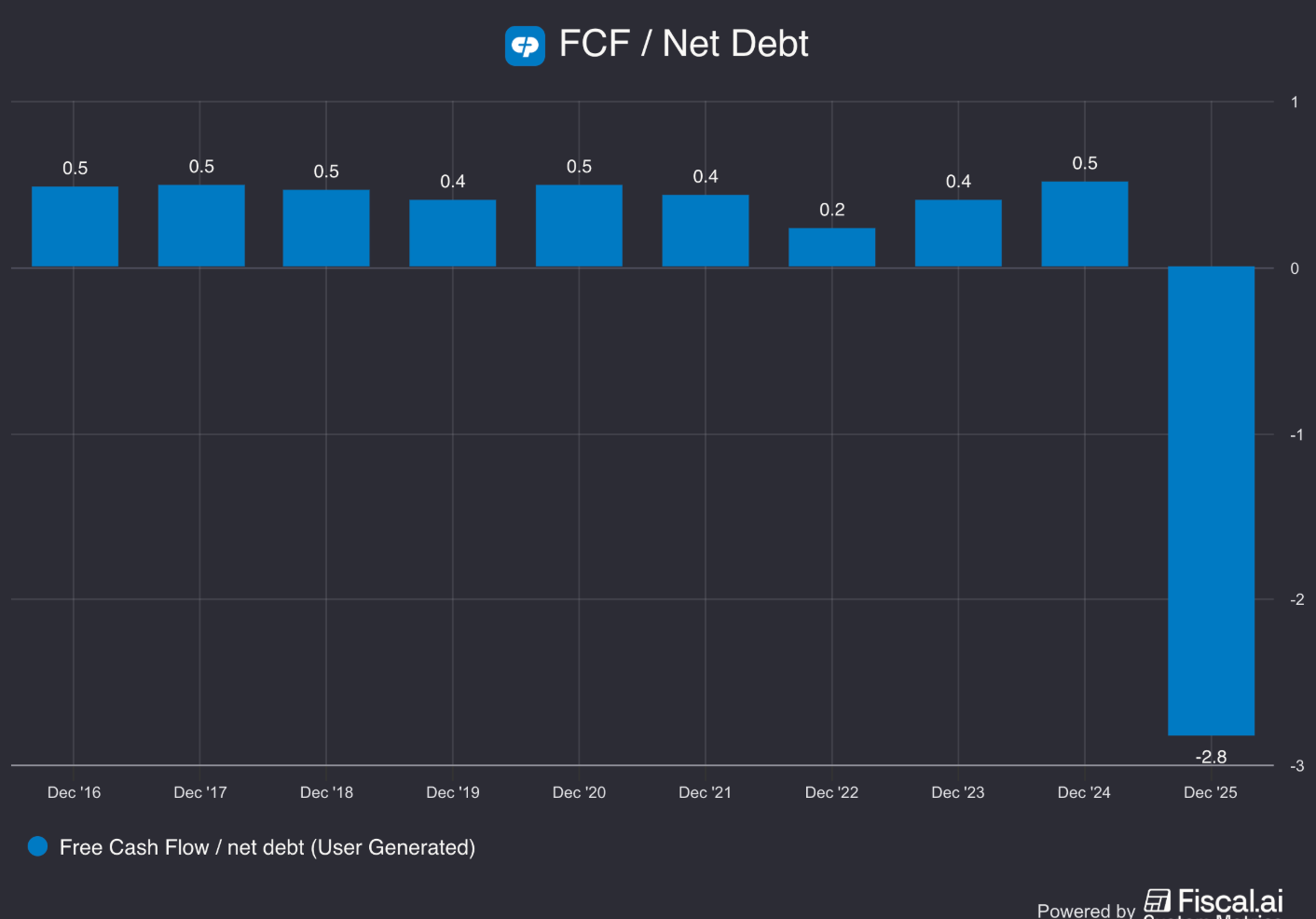

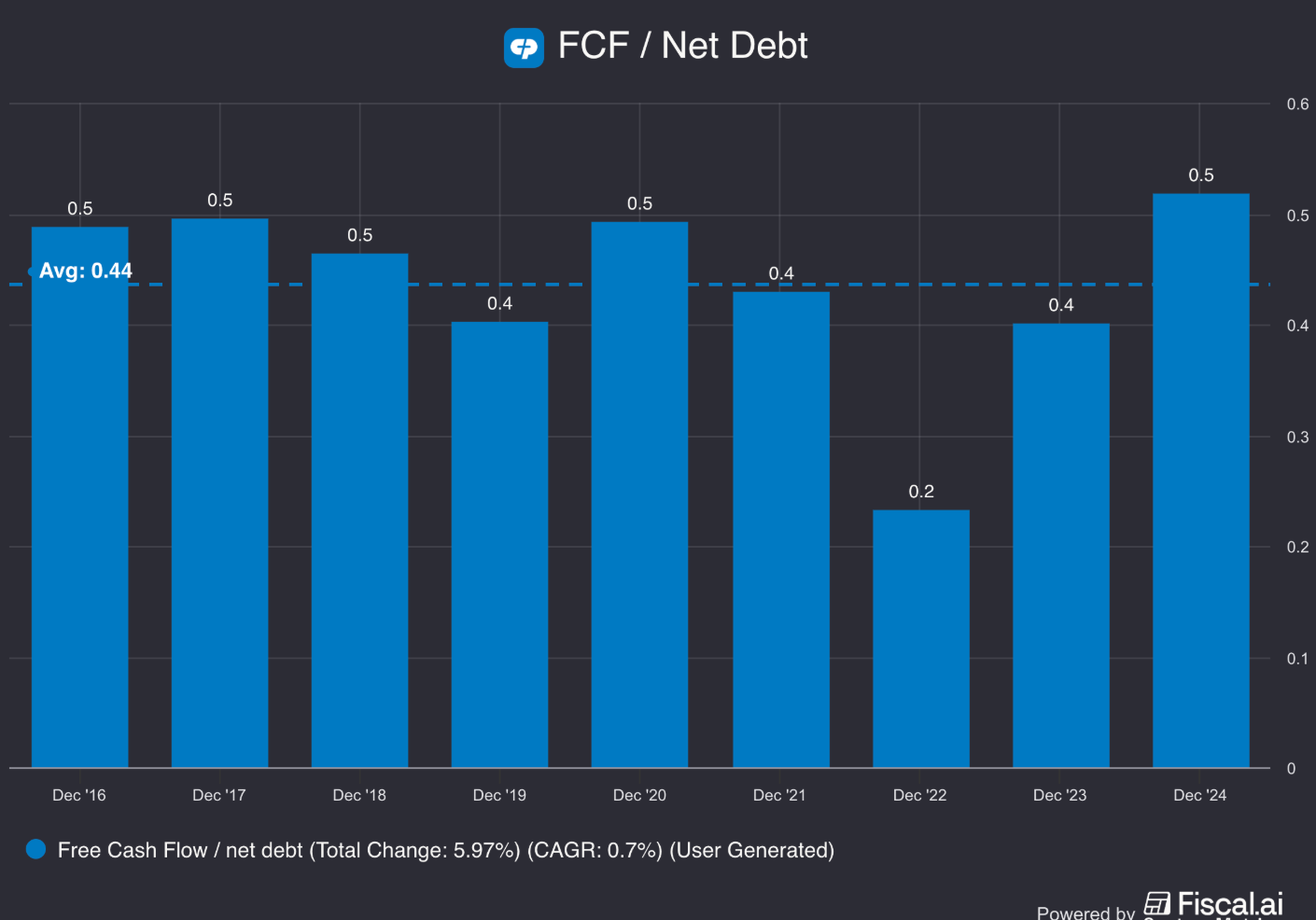

FCF / Debt: Tells us how easy it would be to pay off the debt with existing cash flow

Here’s how they look for Colgate:

Interest coverage ratio: 16.1x

Current ratio: 1.0x

FCF / Debt: Net Cash Position (-2.8x)

Overall, the balance sheet still looks safe.

The unusual FCF to net debt figure is due to a one-time accounting impact.

• Non-cash impairment charge reduced reported earnings

• Buybacks and dividends lowered cash during the period

• Debt stayed elevated after refinancing and strategic spending

Historically, this ratio averages 0.4x, which is healthy.

7. Is the company a great capital allocator?

Capital allocation is management’s most important task.

That’s as far as we can go with this free preview.

Want the rest of the investment case, and to find out if Colgate-Palmolive has great capital allocation, or earns a spot in the Compounding Dividends or High Yield Portfolio?

You can join us here:

.One Dividend At A Time

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.

First class analysis. Very useful for existing and potential Colgate Palmolive shareholders

I loved the way you explained it. Great work!