💸 The Market Is Becoming Less Efficient

Something special is happening on June 23rd that you won’t want to miss.

If you want behind-the-scenes updates and early access to our upcoming high-yield reports, join the High-Yield VIP List, and you’ll get the following immediately when you join for free:

My high-yield stock watchlist

A Checklist of Dividend Investing Mistakes

The Highest Yielding Dividend Aristocrats

Get on the list by leaving your email here.

Yes, the title of this article is a bit provocative.

But some seriously smart people agree with the idea that the market is becoming less efficient over time.

Let's dive into the evidence, and what that means for investors.

Explained: Key Insights for Smarter ...")

Let’s start very quickly with what we typically mean by ‘markets are efficient’.

The Efficient Market Hypothesis (EMH) is the idea that a stock’s current price always reflects all available information in the world right now.

Because everyone has access to the same news and data, stock prices instantly adjust to reflect it.

That means that stocks are always correctly priced - if a stock were a good deal, investors would have already bought it and driven the price up.

Is the market really less efficient?

The efficient market hypothesis is difficult to test.

On the surface, it does make some sense that asset prices would reflect all the available information.

But the hypothesis assumes that everyone paying attention to the same information, weighting it the same, and inviting in the same way.

This obviously isn’t true.

One problem with testing the Efficient Market Hypothesis is that we don’t have a perfect market or model to compare the actual market to.

We don’t know what prices should be.

But, sometimes it’s pretty easy to spot what prices shouldn’t be.

SpaceX

SpaceX will IPO on Friday.

Apparently, the folks bringing this company public are very strong believers in the Efficient Market Hypothesis.

In a typical IPO, the price is set as a range - say $100 to $120 per share.

But SpaceX knows exactly what it’s worth, and has set the price at $135 per share.

That’s about $1.7 trillion for the whole company.

What do you get for that price?

A company that had $18.7 billion in revenue in 2025, and lost $4.9 billion.

That puts the IPO price at about 94x sales.

For perspective, here’s the Price/Sales of the Mag 7:

Nvidia: 21.3

Tesla: 15.1

Alphabet: 10.7

Apple: 10.3

Microsoft: 10.0

Meta: 7.5

Amazon: 3.7

Some Quick AI Math

Let’s also quickly take the example of AI.

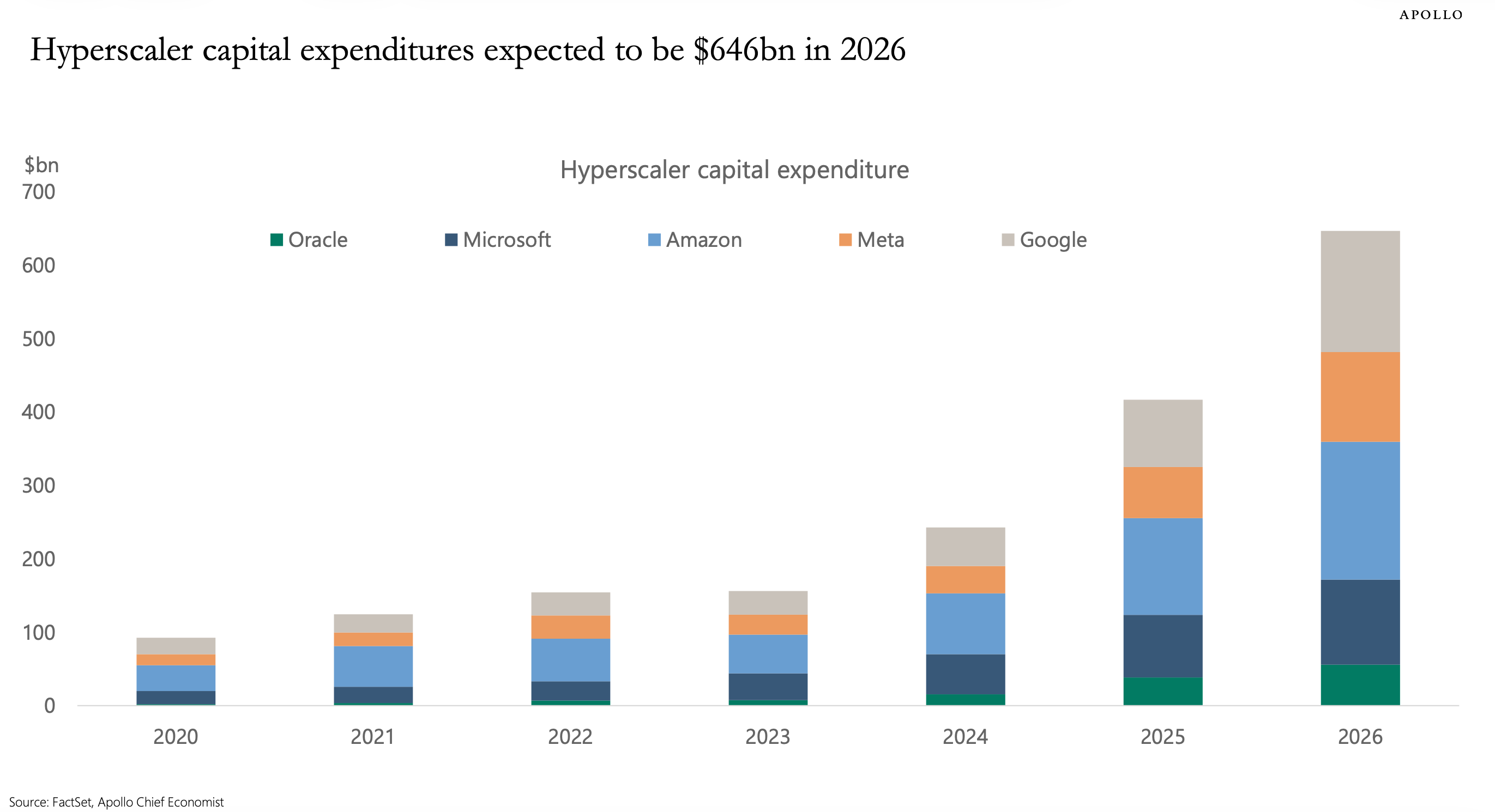

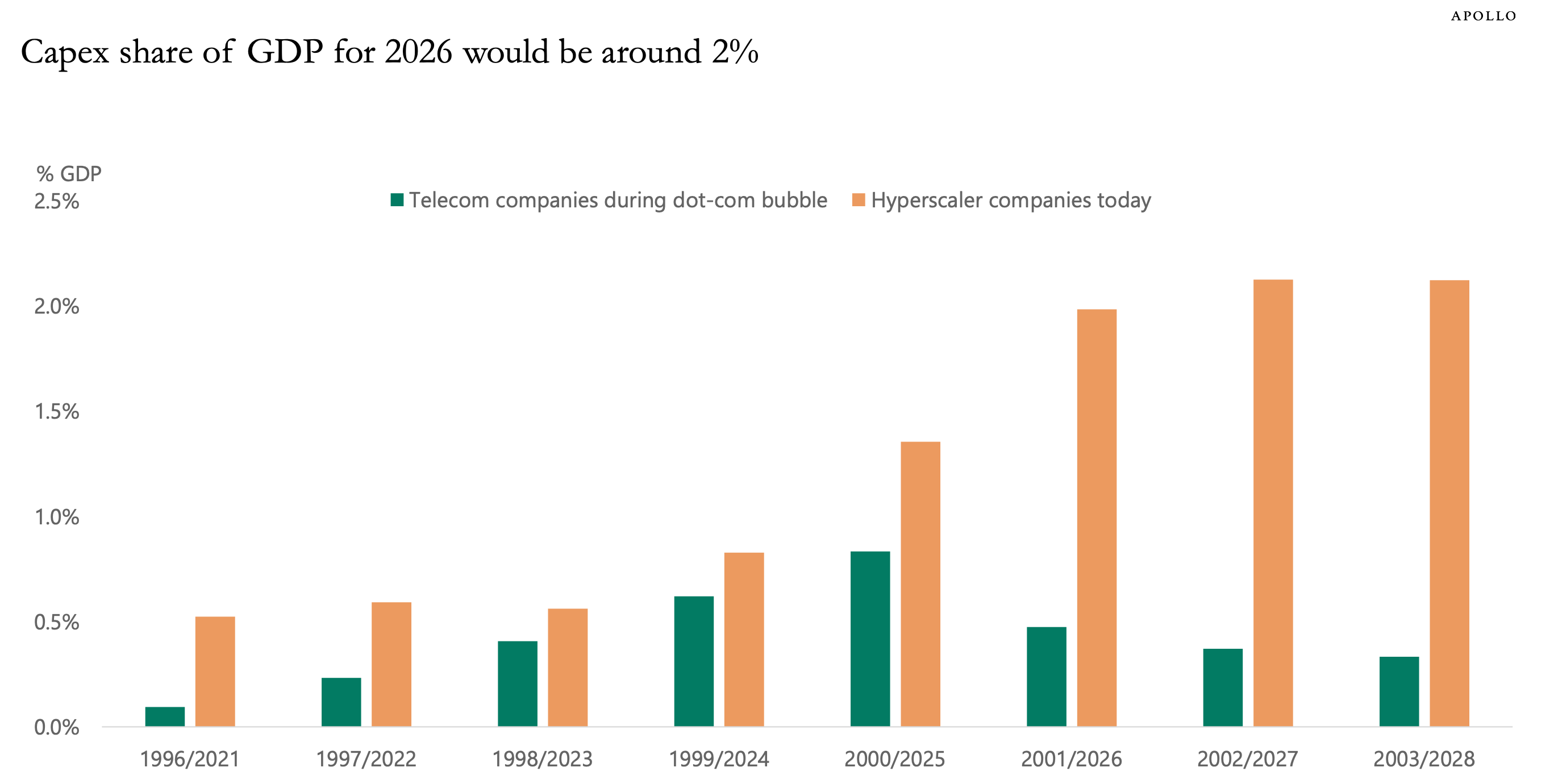

The buildout of data centers continues at a rapid pace, and 5 companies are expected to spend more than $600 billion on it in 2026.

That’s about 2% of GDP.

More than double what was spent at the peak of the dot com boom in 2000.

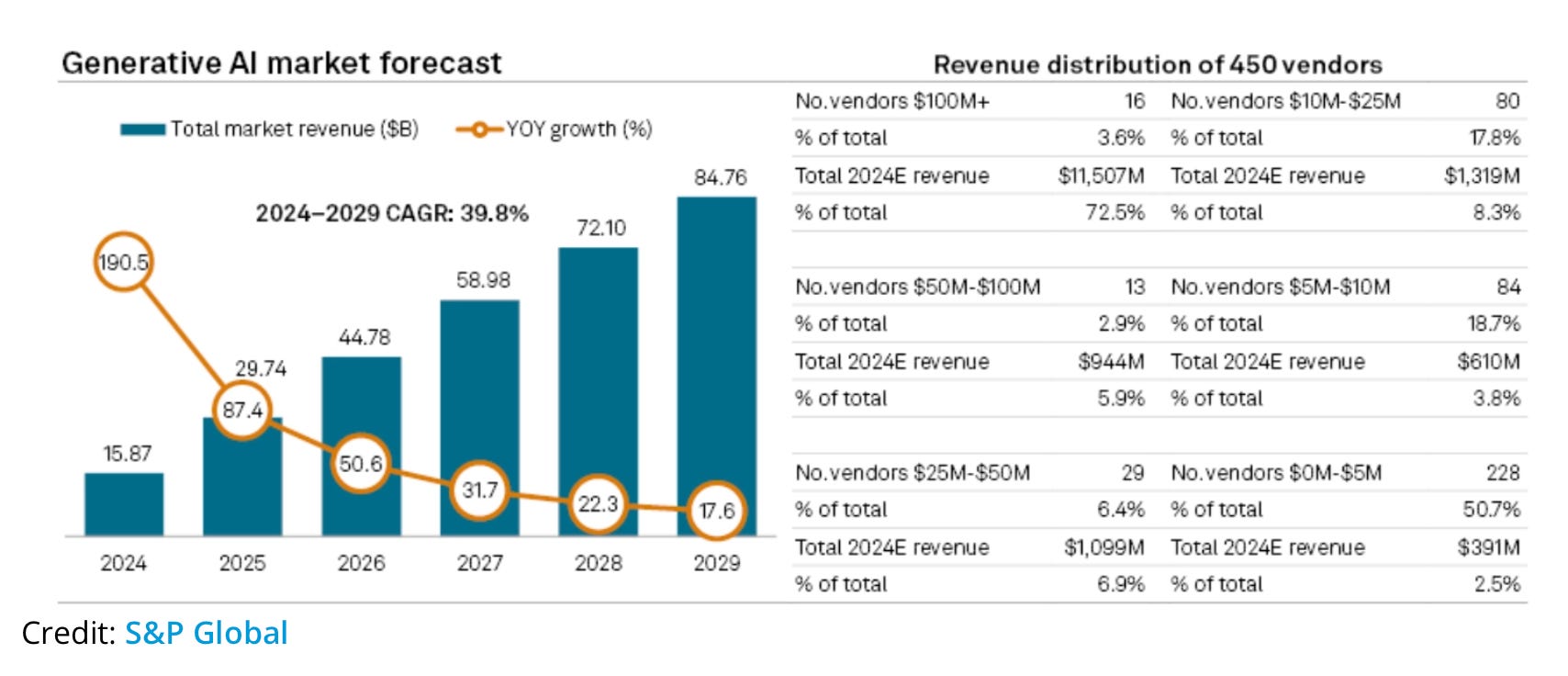

Contrast that with S&P Global’s projection of around $45 billion in AI revenue in 2026.

Eventually, all that spending needs to make a profit, so let’s just use $650 billion in 2026 spending as a starting place.

A 10% return on investment would require $60 billion in profit.

We don’t know the profit margin on AI yet, but let’s take a few guesses.

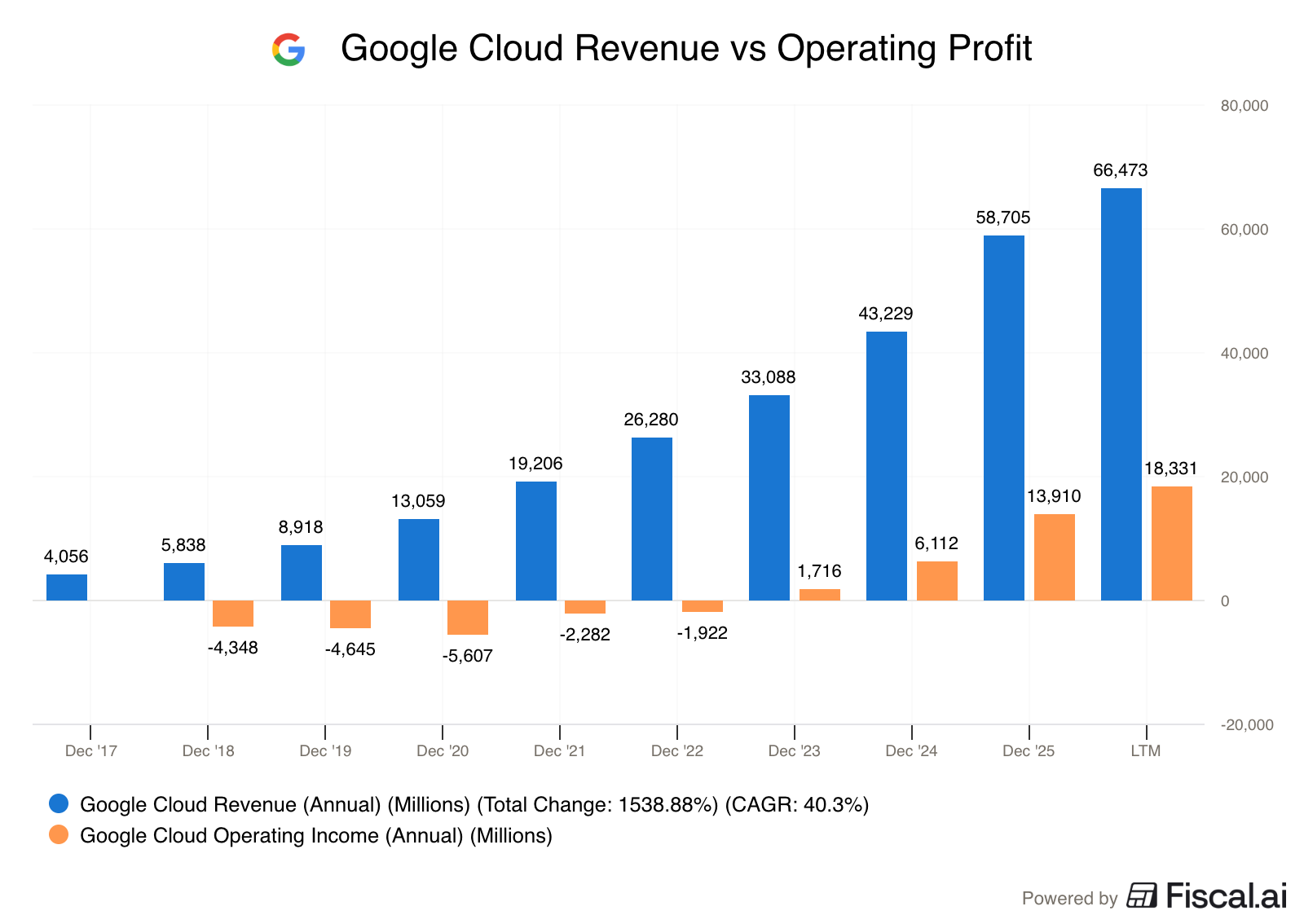

Google Cloud brought in about $66.5 billion in Revenue and had $18.3 billion in operating profits in the last 12 months.

That’s a 27.5% Operating Margin.

If we start there, then to get $60 billion in profit, AI needs to bring in about $218 billion in revenue.

That’s about:

50% of Google’s total revenue right now

Equal to the revenue of:

Costco

JP Morgan

NVIDIA

BP

If we assume that AI is more capital intensive than the general cloud business - probably reasonable - and put a 20% margin on it, now we need $300 billion in revenue to get a 10% return on 2026’s AI CapEx.

These are massive numbers.

And the AI CapEx spending is only projected to go up from here.

Who Else Agrees?

Cliff Asness is a co-founder of AQR Capital Management, a quantitative investment firm known for its data-driven approach to asset management.

He’s also a respected researcher and publishes a lot of papers related to investing and markets.

He released a paper in August of 2024 called “The Less-Efficient Market Hypothesis”.

In it, he argues that the market has become less efficient over his 30-year career.

He makes the point that perfect efficiency probably isn’t a reasonable expectation.

But that we should be asking:

How efficient is the market currently?

Has this changed over time?

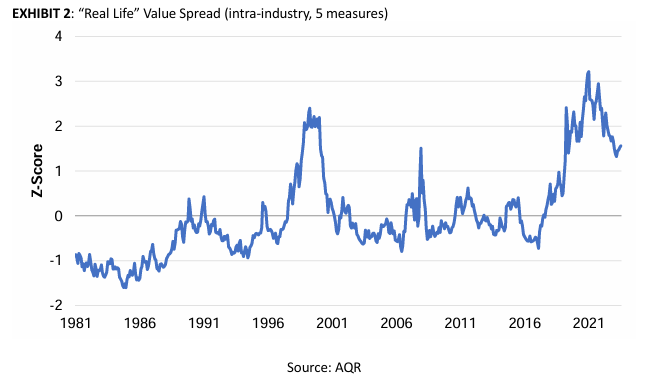

Instead of examples of excess like I just gave you, Asness looked at the value spread - the ratio of expensive stocks to cheap stocks.

He used a traditional price to book model:

And a more complex “quant” model using 5 different ratios:

Price to book

Price to cash flow

Trailing PE

Forward PE

EV / sales

You’ll notice they both looked similar, showing pretty extreme spreads in 2000 and 2019-2020.

They looked for reasons that “this time was different”

Were the spreads a function of tech stocks?

Did intangibles drive the spread?

Was it the FAANG or Mag 7?

Was value less attractive because things like ROA, profitability, etc were lower?

Was it the low interest rates?

The answer for all of them was “no”.

This was a 2024 paper, so you might wonder if that valuation gap has closed up at all since then.

Again, the answer is “no”.

If we use a 5-year moving average, things look even worse:

An efficient market is important for society.

Efficient markets matter.

The market’s job is to help allocate capital and resources to the best use.

A more efficient pricing system leads to a more effective economy.

Inefficient markets lead to inefficient and less innovative economies.

Conclusion

Right now, the market is voting for hype and narratives.

But as long-term dividend investors, we should remember that cash flow is what gives a business weight.

Here is what you should remember about market inefficiency:

Capital is being misallocated: The market is currently funneling trillions into hype, narratives about the future, and momentum. A lot of this is capital destruction, but it does create opportunities for investors willing to look at the businesses that are being ignored.

Stocks are pieces of businesses: Even though it may not seem like it now, eventually, the cost of capital matters. Debt comes due. Investors want a return. The narrative must eventually produce cash, or it collapses.

Cash flow is financial weight: If the market completely ignores excellent businesses, management will use their free cash flow to buy back their own undervalued shares and pay consistently compounding dividends. Let the business fund your return, not the market.

You don’t need a perfectly efficient market to build wealth.

In fact, an inefficient market is a great advantage, even if it creates short term pain and frustration.

Just keep buying high-quality businesses with durable competitive advantages, great management, and strong cash flow.

Let the underlying business do the work, and ignore the market.

Coming Next: Part 2

If the market is less efficient than it was a few decades ago, we still need to talk about why?

That’s exactly what we’ll talk about in Part 2!

One Dividend At A Time

-TJ

P.S.

On June 23rd, we are kicking off a series all about high yield investing.

If you want to maximize your portfolio’s income without sacrificing business quality, jump on the VIP Waitlist.

You’ll get behind-the-scenes updates and the very first invite to download our brand-new high-yield special reports the minute we go live.

Don’t forget that you’ll also get the following just for joining the VIP list:

My high-yield stock watchlist

A Checklist of Dividend Investing Mistakes

The Highest Yielding Dividend Aristocrats

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.

And Yes I do agree with this transaction and reports I also feel it also depends what direction where gasoline prices go UP is the incorrect Down in prices is better. YET, I doubt very much .It will be latter I am blessed I bought and financed used hybrid vehicle The place I drove from Wilmington Delaware to Bridgeton NJ and return I received 60 mpg on my 2019 Hyundai IONIQ I am not selling it.I praise God for this technical wonder.

Nice article, the market may be “efficient “ in that all the information gets reflected in price. However, since there is so much variation in investment strategies, you get diametrically opposed actions to the same information. Simple example, a momentum investor may buy a stock that has a big move up, while a value investor may sell because the stock has become too richly valued.