What Should Berkshire Do With All That Cash?

The Gabelli Value Investor Conference in Omaha brings together some of the sharpest minds in value investing.

The Berkshire Hathaway panel got asked a very interesting question this year:

’What should Berkshire Hathaway buy with all their cash?’

Let’s see what the 4 panelists answered!

Berkshire’s Cash Pile

At the time of the event, Berkshire Hathaway had nearly 30% of its assets in cash.

That’s around $397 billion.

It’s hard to get your head around such a number, so let’s look at some of the public companies Berkshire could buy outright with that kind of cash pile.

Home Depot: $325 billion

McDonald’s: $192 billion

Booking Holdings: $130 billion

Moody’s: $78 billion

Berkshire has most of that money parked in short term treasuries.

At 4% to 5% interest, simply letting the cash sit there generates $15 to $20 billion a year in pure interest income.

Again, to put it into perspective, here’s the revenue of a few well-known companies:

AutoZone: $19 billion

Texas Instruments: $18.4 billion

Kimberly-Clark: $16.5 billion

Markel Group: $16 billion

Door Dash: $14.7 billion

Here’s a few companies with Net Income around the $15-$20 billion mark:

Comcast: $18.7 billion

MasterCard: $15.5 billion

Coca-Cola: $13.7 billion

So Berkshire makes more profit than Coca-Cola does just by buying short-term Treasury Bills with its cash.

Deploying that much capital is very difficult.

The sheer size of the investments required to move the needle for Berkshire eliminates almost all publicly traded companies.

The target must possess an exceptional moat, outstanding management, and a valuation that makes sense.

Let’s see what companies each of the panelists thought Berkshire should buy.

Christopher Bloomstran

President and Chief Investment Officer, Semper Augustus Investments Group, LLC

Bloomstran is known as a disciplined, fundamental investor.

He founded Semper Augustus in 1998, and runs a concentrated portfolio of well-run, well-capitalized businesses.

He’s also known for his deep analyses of Berkshire Hathaway.

He suggested 2 dominant, cash-generating businesses for Berkshire to consider:

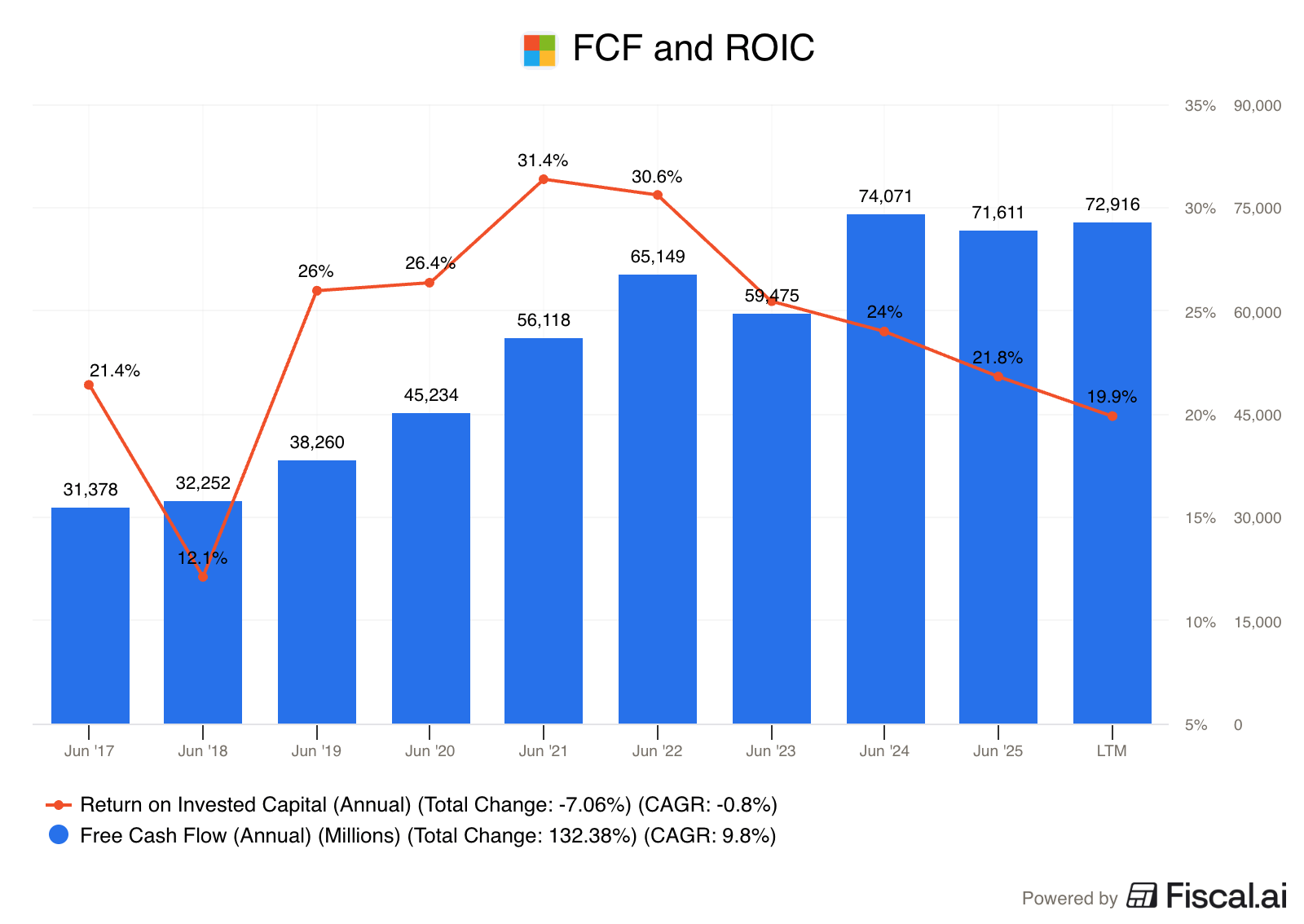

Microsoft

How does Microsoft make money?

Microsoft sells cloud services, software, and hardware. They also earn from ads on Bing, LinkedIn, and subscriptions like Microsoft 365 and Xbox Game Pass.

Why Microsoft would fit Berkshire’s Portfolio

Microsoft has a very strong moat - the Office products like Word and Excel are standards in corporations across the world, there are switching costs to move away from Microsoft as your cloud provider, and LinkedIn is the only social network focused on professionals

It’s a great business - Microsoft generates a lot of Free Cash Flow, high ROIC, and has a strong balance sheet, all things Berkshire typically loves

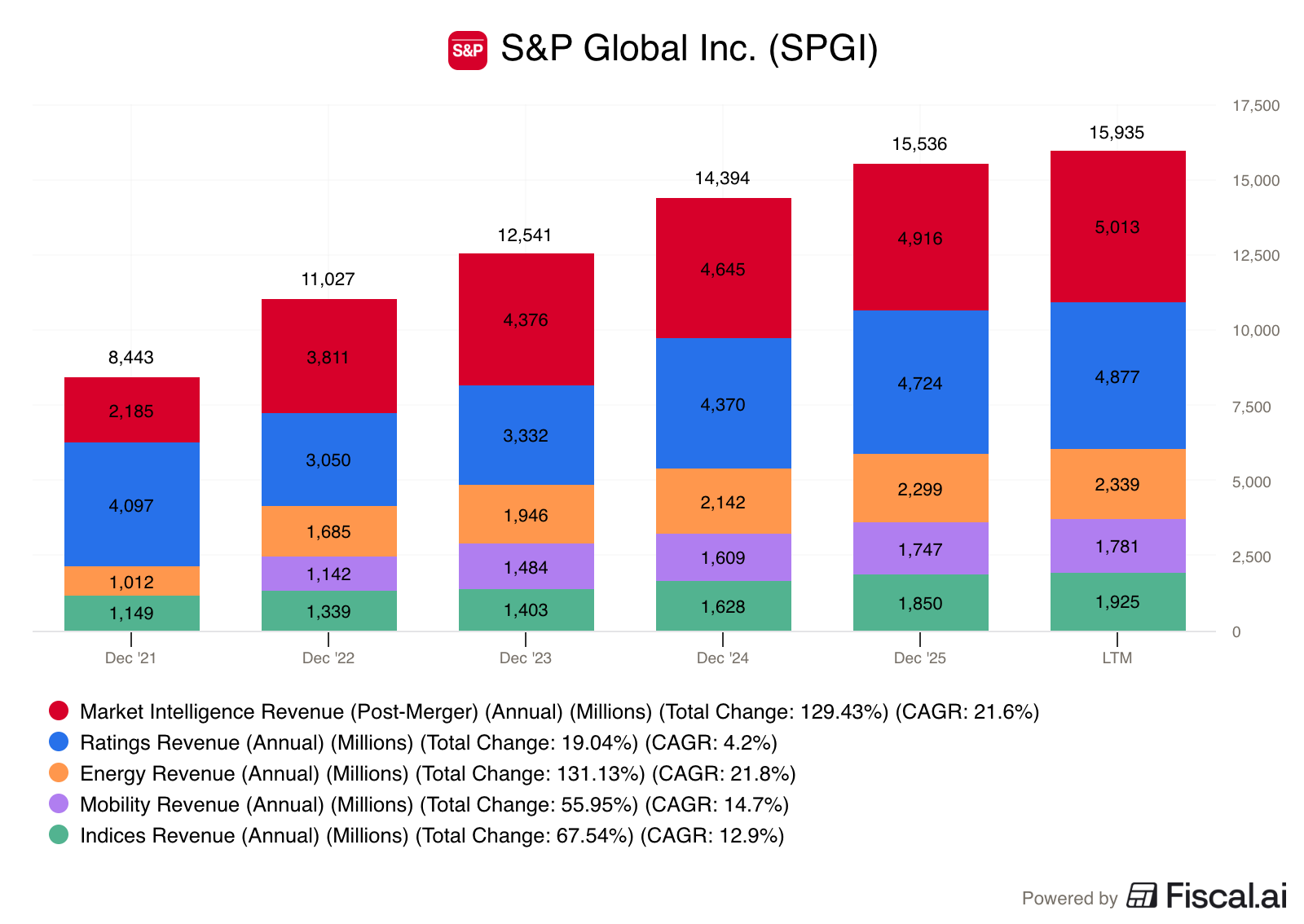

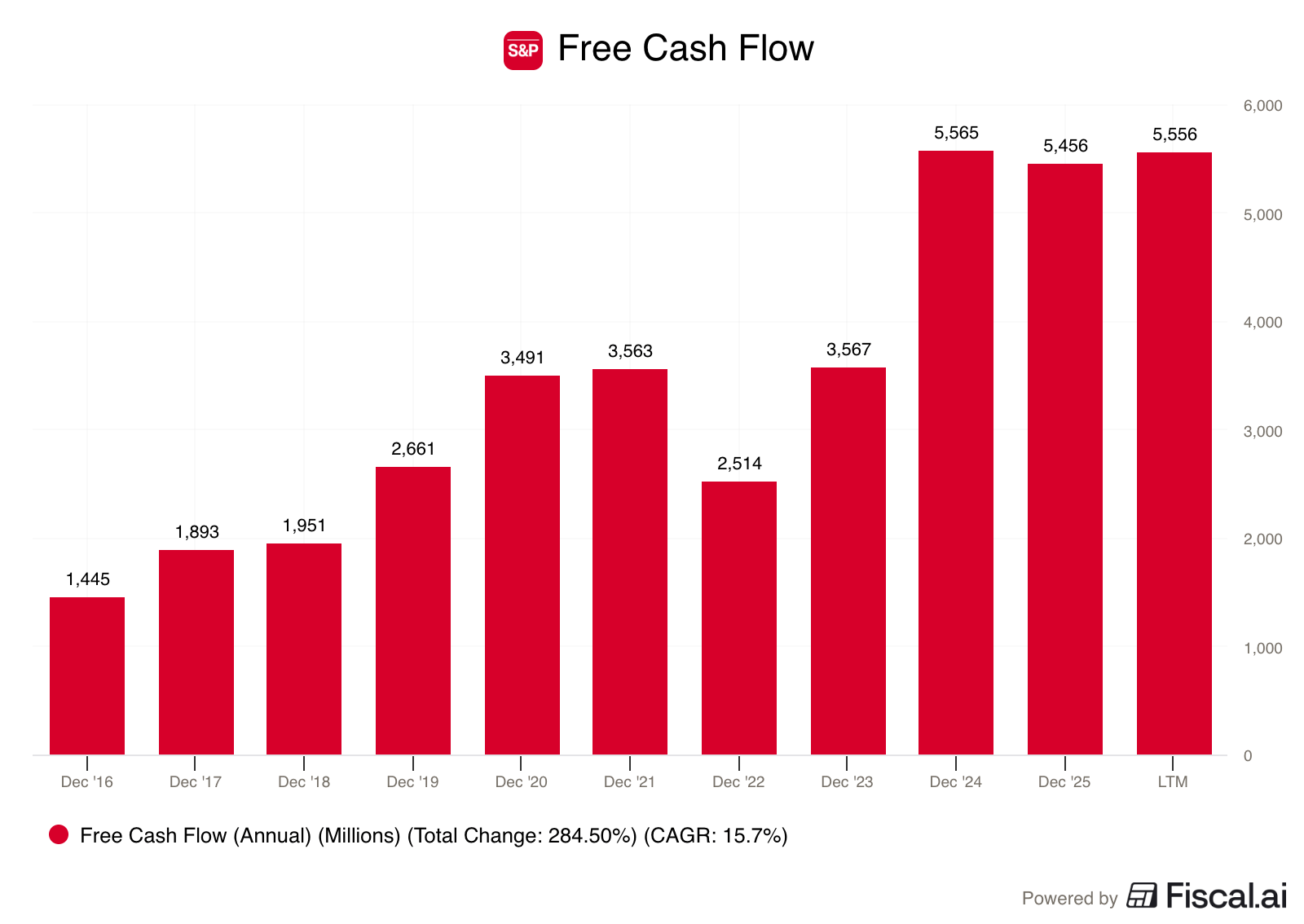

S&P Global

How does S&P Global make money?

S&P Global provides financial market intelligence, credit ratings, and benchmarks that help investors and institutions evaluate risk and make decisions. The company earns revenue mainly through subscriptions to its data products, along with fees from its ratings and index businesses.

Why S&P Global would fit Berkshire’s Portfolio

It operates in oligopolies – The credit rating industry is dominated by just a few players, indexes are dominated by S&P and MSCI, S&P Global has limited competition in every segment

It’s capital-light – The business requires very little capital to operate and grow, which means massive, highly predictable free cash flow that would go back to Berkshire for them to deploy - S&P Global is small enough, Berkshire could buy the whole thing

Adam Mead

CEO and Chief Investment Officer, Mead Capital Management, LLC

Mead is the author of The Complete Financial History of Berkshire Hathaway, a massive 880-page chronological analysis of the company.

He also runs Mead Capital Management, which he founded in 2014.

He suggested Berkshire adda dominant family business to the portfolio.

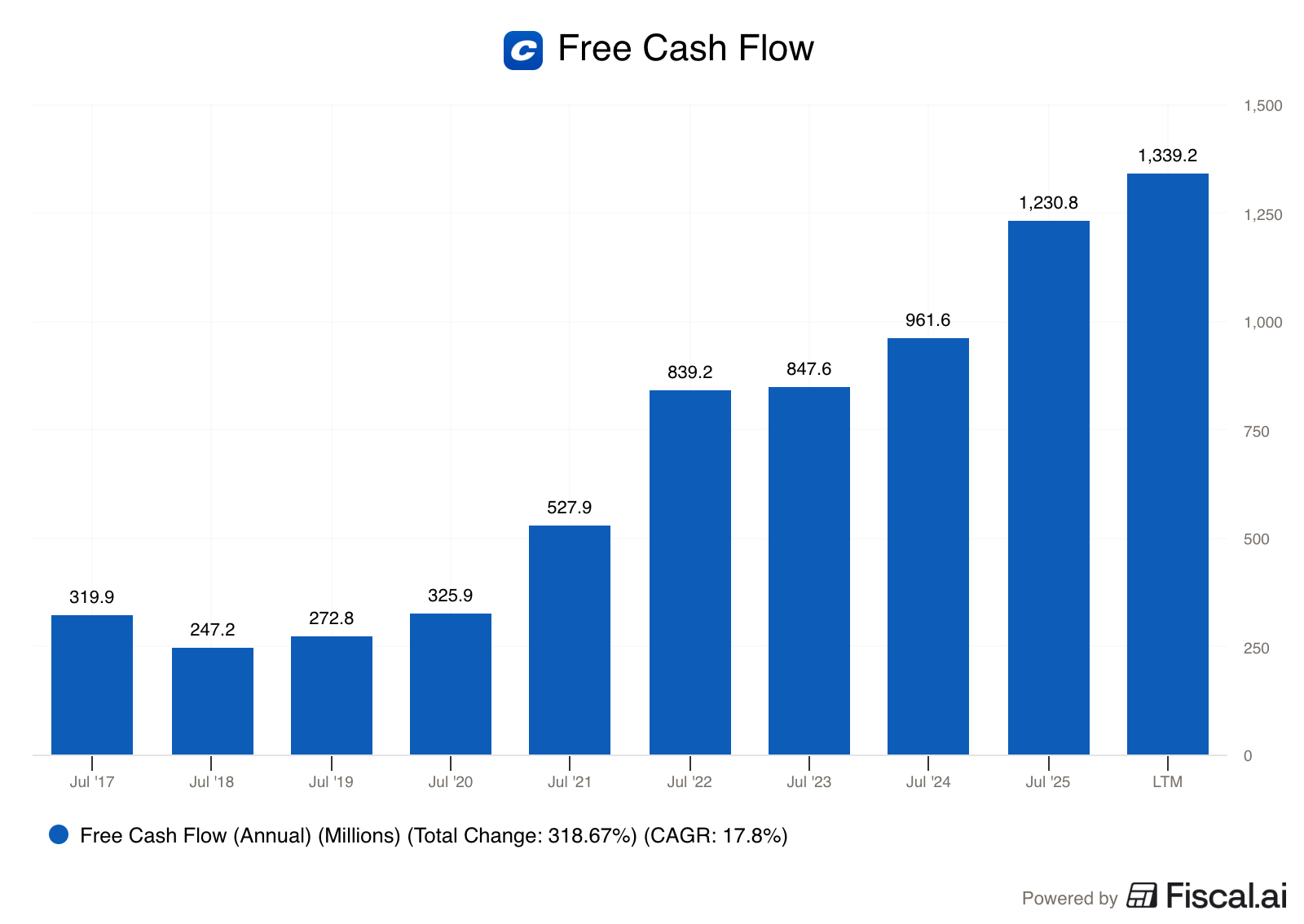

Copart

How does Copart make money?

Copart ($CPRT) makes money by auctioning and storing used, damaged, or salvaged vehicles for insurance companies and other sellers.

Why Copart would fit Berkshire’s Portfolio

The moat is impossible to replicate – Building out a comparable network of salvage yards, alongside deep, decades-long relationships with major auto insurers is impossible, which means very limited competition

It aligns with Berkshire’s culture – Copart is a family-run business that dominates an unglamorous niche while generating huge amounts of cash

Brett Gardner

Author, “Buffett’s Early Investments”

Gardner’s book went back to the original documents Buffett used in the 1950s and 1960s to make his first millions through lesser-known, highly concentrated early bets.

He suggested Berkshire buy the rest of a business that’s already in their portfolio.

Occidental Petroleum

How does Occidental Petroleum make money?

Occidental makes money mainly from producing oil and gas.

Why Occidental would fit Berkshire’s Portfolio

Path of least resistance – Berkshire already owns a massive stake in the company, understands it, and already fully acquired the chemical division. Buying the rest of the company is just finishing the job they’ve already started.

It’s a better private company than a public one – OXY’s results are volatile due to oil price fluctuations. Operating OXY under the Berkshire umbrella protects the business from the emotional swings and short-term pressures of the public markets.

Pieter Slegers

Founder, Compounding Quality

Does Pieter need an introduction?

He stayed true to his Quality philosophy and suggested a very well run, founder-led business that would fit very well in Berkshire’s portfolio.

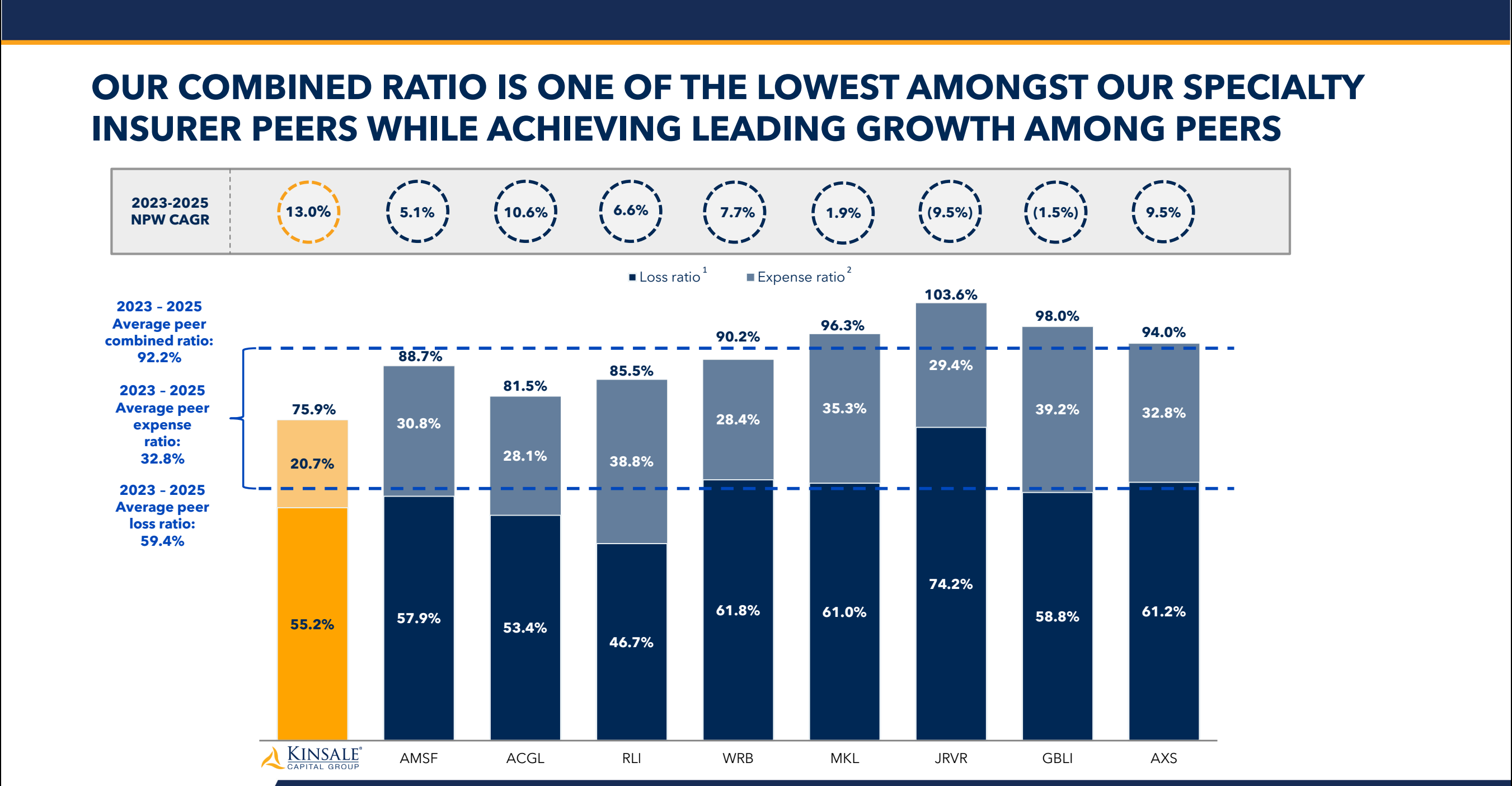

Kinsale Capital Group

How does Kinsale Capital make money?

Kinsale Capital is an established and expanding specialty insurance company focused exclusively on the excess and surplus lines (“E&S”) market in the United States.

Why Kinsale Capital would fit Berkshire’s portfolio:

It add more float to Berkshire’s insurance engine – Kinsale is a conservative underwriter and would add more high-quality, profitable float to the broader Berkshire insurance operations

The culture matches – It’s a founder-led business with extreme discipline. Like Berkshire’s own insurance operations, Kinsale’s management won’t chase top-line growth if it means writing unprofitable or risky policies.

Conclusion

Here’s what you should remember from today’s article:

Berkshire Hathaway holds a massive $397 billion cash pile, nearly 30% of its assets

That is enough cash to buy companies like Home Depot or McDonald’s outright, entirely in cash.

Deploying this much capital into high-quality businesses with strong moats is incredibly difficult

Here are the five companies the panelists suggested:

Microsoft: A strong software/cloud moat with recurring cash flows.

S&P Global: A capital-light oligopoly that serves as a toll bridge for global financial markets.

Copart: A family-run cash cow with a network of physical salvage yards that is virtually impossible to replicate.

Occidental Petroleum: A natural choice to “finish the job” on a massive existing stake

Kinsale Capital Group: A disciplined, founder-led specialty insurer that would feed high-quality float directly into Berkshire’s core machine.

One Dividend At A Time

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.