What's Going On In Private Credit?

For a decade, private credit looked boring, in the best possible way.

Steady yields. Low volatility. No drama.

Then AI arrived, and suddenly everyone wanted to know: what’s actually in these loans?

Howard Marks just released a memo trying to answer that question.

And the most interesting part isn’t where we are, it’s how we got here.

Nothing in finance happens in isolation.

One Thing Leads to Another

Before late 70’s, companies without an investment grade rating almost couldn’t issue bonds.

They had to borrow from banks, or borrow from insurance companies through ‘private placements’.

But Michael Milken is credited with the idea of letting these companies issue bonds if the interest rate was high enough.

Junk bonds allowed Leveraged Buyouts or LBOs to start taking place in the 80’s.

A Leveraged Buyout (LBO) is the purchase of a company using a small amount of your own cash and a very large amount of borrowed money.

How LBOs Work:

An investment firm (private equity) identifies a company they want to buy.

They borrow massive amounts of money, often in the form of high-yield bonds or private loans, to fund the purchase.

The firm uses the assets and future cash flows of the target company to guarantee and service that debt.

Using leverage allows the firm to acquire much larger companies than they could afford with their own capital alone.

Leveraged Buyouts eventually turned into the Private Equity industry we know today.

As buyouts got bigger, the financing had to get bigger too.

That’s why Wall Street came up with ‘broadly syndicated loans’.

Before these, if a company wanted to borrow more money than one bank could provide, three or four banks might come together to share the loan.

In the 90’s, Wall Street realized they could sell these loans to institutional investors (like pension funds, insurance companies, and huge investment firms) instead of just other banks.

Instead of 4 banks splitting a loan, a broadly syndicated loan is hundreds of different investors buying small pieces of it.

This made even more money available for Private Equity to really take off.

When the tech bubble popped in 2000, the S&P 500 declined for 3 years, and investors stayed away from stocks.

At the same time, central banks reduced interest rates, meaning government bonds couldn’t give investors the yield they were looking for.

Where’d they go?

Private equity.

Another thing that investors were buying up?

‘Structured credit’ products like Mortgage Backed Securities and Collateralized Debt Obligations, or CDOs.

| Definition & History")

The demand was so great that mortgage lenders were incentivized to create all the ‘liar loans’ or NINJA (no income, no job, no assets) loans to provide the raw material to create the CDOs that eventually caused the 2008 Great Financial Crisis.

How 2008 Led to Today’s Private Credit

The banks jumped on board the CDO craze in the 90’s, and ended up needing bailed out in 2008.

That led to way more regulation and an unwillingness to loan to Private Equity and private companies.

Investment managers were all too happy to fill this liquidity vacuum.

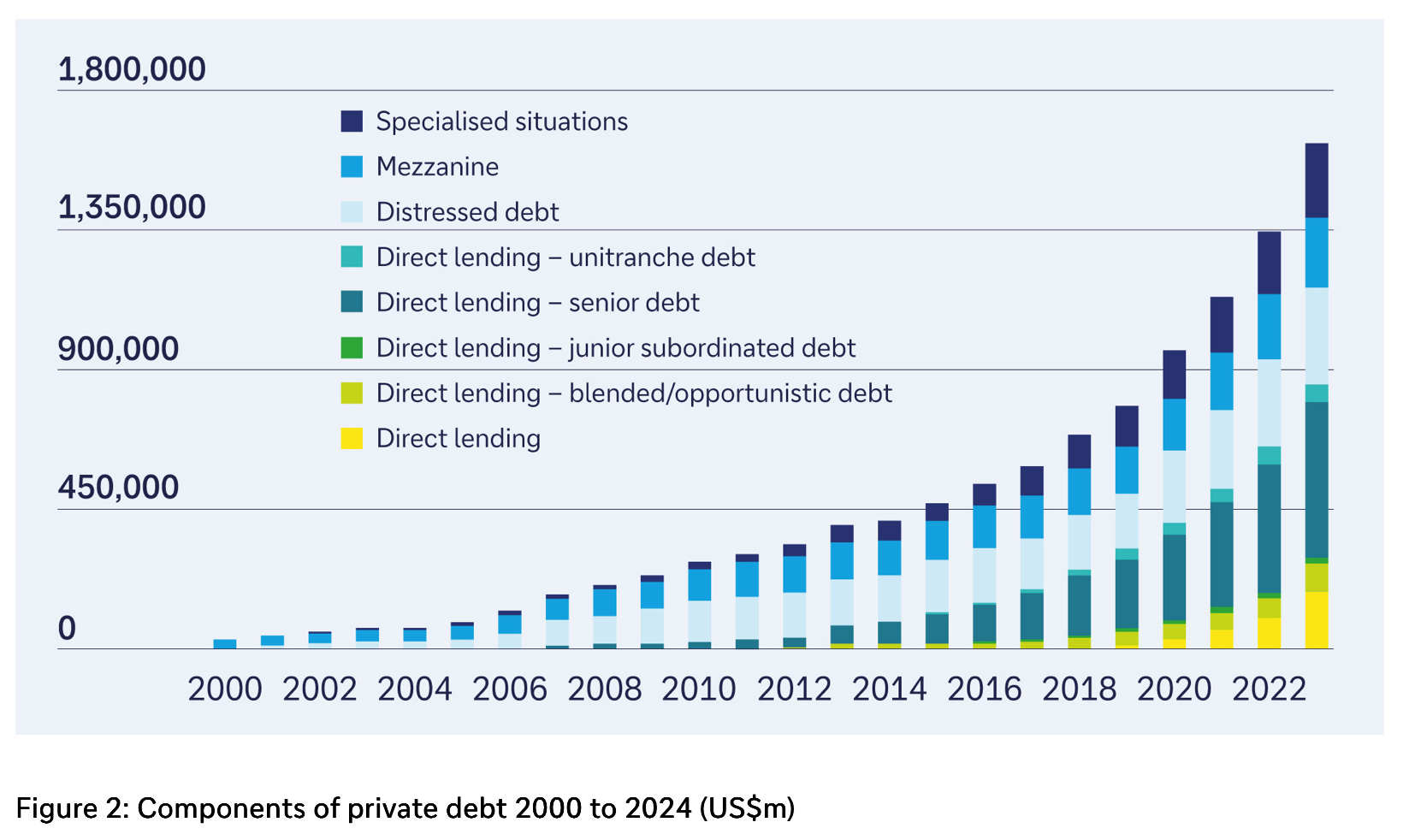

This gave birth to the modern era of direct lending, a specific subset of private credit where non-bank lenders provide capital directly to mid-market companies.

After 2008, interest rates were slashed again, meaning government bonds hardly yielded anything.

Direct lending offered higher yields than public bonds with the added (false) benefit of low price volatility.

Because these are private deals, they aren’t marked to market daily, which made their prices look stable.

But stability and safety aren’t the same thing.

Investor demand led hundreds of new investment firms to join the space, and a race to the bottom began:

Too much money was chasing too few high-quality deals.

To win deals and put capital to work, lenders began competing by accepting lower yields and narrower interest spreads.

Lenders began stripping away covenants, the rules and safety nets in loan documents that protect the lender if a company’s performance falters.

For years, a benign economic environment hid these weakening standards.

But as Warren Buffett likes to remind us:

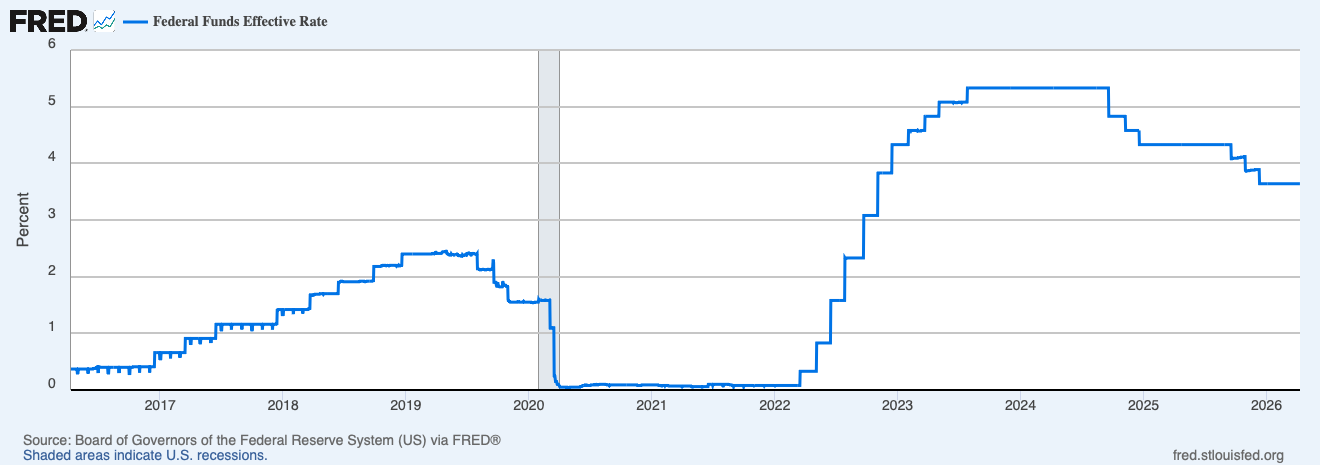

The 400-basis-point increase in rates since 2022 is what’s pulled the tide out from the direct lenders.

The first cracks happened in the middle of 2025 when companies like First Brands and Tricolor, went bankrupt.

This raised some red flags about potential fraud and poor underwriting.

But the market seemed to accept these as isolated incidents.

The release of Claude Code changed that.

Here’s how Howard Marks put it in his memo:

To understand what's happening now, it helps to separate two things:

The changes in the fundamentals of borrowers and the safety of the loans

The reactions and emotions of investors

Let’s look at what Marks says about each.

The fundamentals of the loans

Most software companies are still making money.

The problem is that their future is suddenly uncertain, causing multiple compression in the stock market and falling stock prices.

Here’s how that affects the credit investments in software companies:

When a firm lends money to a company, they rely on the equity cushion. This is the value of the company that sits below the debt. If a company is worth $100 million and has $60 million in debt, there is a $40 million cushion of equity.

Because investors are now worried about AI disruption, they have marked down the equity value of these software companies. As the equity value drops, that safety cushion for the lenders disappears.

Marks summed it up with a quote from an internal Oaktree memo:

“The disruptions and headlines are largely flow- and sentiment-driven rather than the result of credit deterioration.”

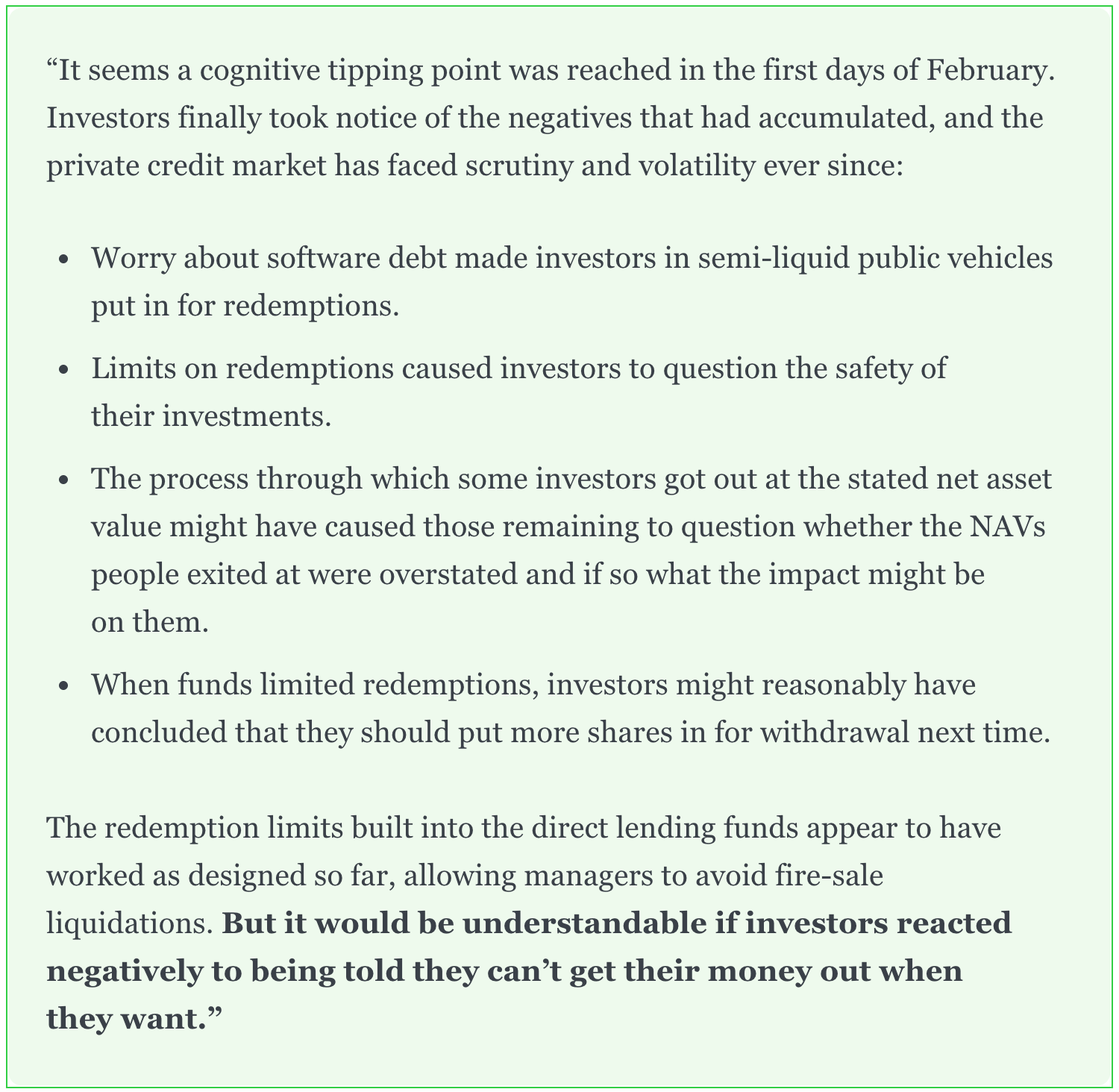

The reaction of investors

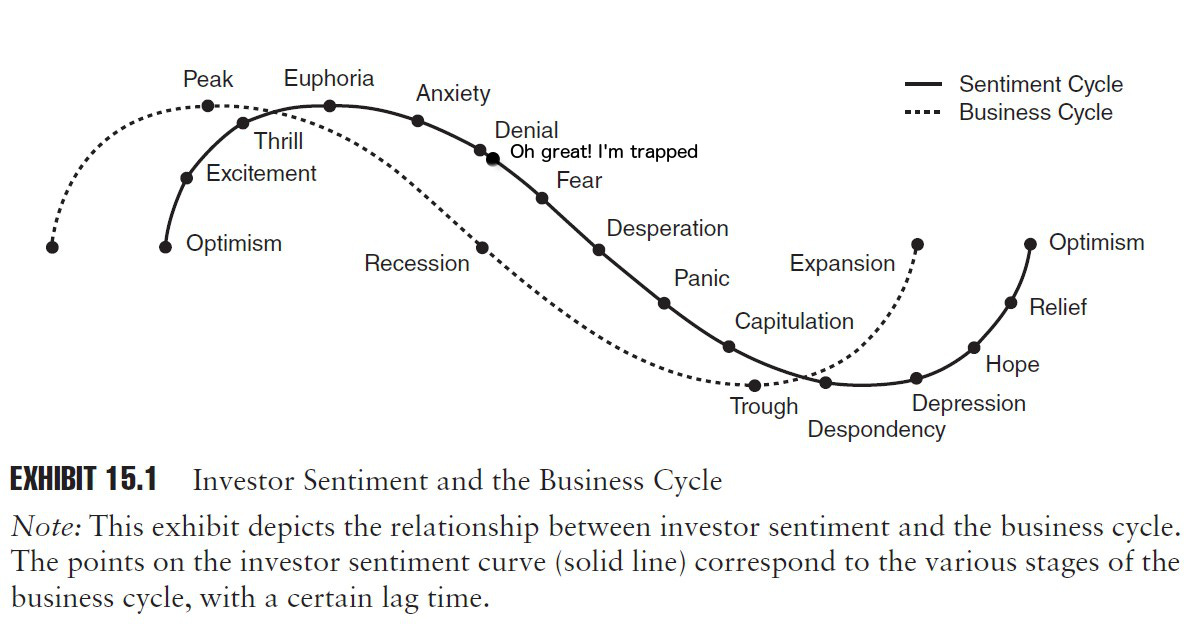

The market is rarely a cold, calculating machine.

Instead, it’s a pendulum that swings between two extremes.

When it comes to investor sentiment, the pendulum usually swings between flawless and hopeless.

For years, sentiment around private credit was flawless.

But when the mood shifted in February, the pendulum swung hard:

Investors went from ignoring risks to seeing them everywhere.

Private credit funds aren’t like stocks. You can’t always sell them instantly. When investors got scared and asked for their money back, many funds hit their redemption limits (gates).

That of course caused panic, and even more people to line up at the exit, creating a self-fulfilling prophecy of illiquidity.

The safety and standards that were stripped away during the good times are being missed now that the tide has gone out.

Marks reminds us that the “new thing” rarely pays off as expected when people stop asking questions and start chasing easy profits.

How Private Equity and Direct Lending will impact each other going forward

Direct lending has become a primary source of the debt PE firms use to buy companies.

For much of the last 40 years, falling interest rates provided a massive tailwind for private equity.

Low rates made it cheap to borrow money and increased the value of the companies being bought.

This created a virtuous circle:

PE firms used cheap direct loans to buy companies.

A strong stock market made it easy to sell those companies at a profit.

Investors got large payouts, which they immediately reinvested into new PE funds.

The rise in interest rates since 2022 has disrupted this cycle.

Both sectors have seen issues from this:

Lower Profits: Portfolio companies now have higher interest costs, and lower profits, making them less valuable to future buyers.

Refinancing Issues: Companies are struggling to refinance low rate debt because their earnings don’t cover the higher interest costs as easily.

Slower Payouts: Because companies are harder to sell in this environment, investors (Limited Partners) are receiving fewer distributions. This makes it more difficult for them to commit capital to new funds.

Going Forward

Success will depend more on the actual skill of the managers, how they select and run companies, instead of just relying on falling interest rates.

Lenders who performed good due diligence, kept high standards and made good decisions will be fine.

Lenders who lowered standards, lent to less strong companies, or took lower positions in the repayment stack will have more trouble.

Direct lending is expected to remain a permanent source of funding, it may have to go through a difficult credit cycle, with some loans failing before the market reaches a healthier state.

As Howard Marks has written before, you can't judge the quality of a decision by its outcome alone.

The decisions made during the boom years of private credit are only now being graded.

For many lenders, it will be a difficult test, not because the market has changed, but because it has finally started paying attention.

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.

This is a great breakdown, especially the point that “stability and safety aren’t the same thing.” That’s where most people get fooled.

What stands out to me is how similar this is to what happens in options markets. When conditions are calm and premiums feel easy, standards slip. People sell risk without fully respecting what’s underneath it. Then the environment shifts and suddenly everyone “rediscovers” risk at the same time.

Private credit feels like it went through the same cycle. Years of smooth returns created the illusion of safety, when in reality the risk was just hidden by structure and lack of mark-to-market pricing.

The part that matters now is exactly what you said. Skill starts to matter again. Underwriting, structure, discipline.

Same in trading. Same in real estate.

Easy environments reward participation. Harder environments expose process.

We’re just starting to see which is which.