Who Will Buy If Passive Sells?

Welcome back to Part 2 of our series on the structural shift happening in the stock market.

In Part 1, we looked at why Terry Smith, one of the world’s best quality investors, was forced to change his strategy

We also broke down how index funds are now driving prices by buying and selling without looking at business fundamentals.

Today, we’ll look at the volatility this is causing, and why the structure of the U.S. retirement system could make the problem much worse.

Let’s dive in.

Passive and Increased Volatility

This passive or automated buying and selling could lead to a lot of volatility.

Smith makes the point that we’ve seen exactly that.

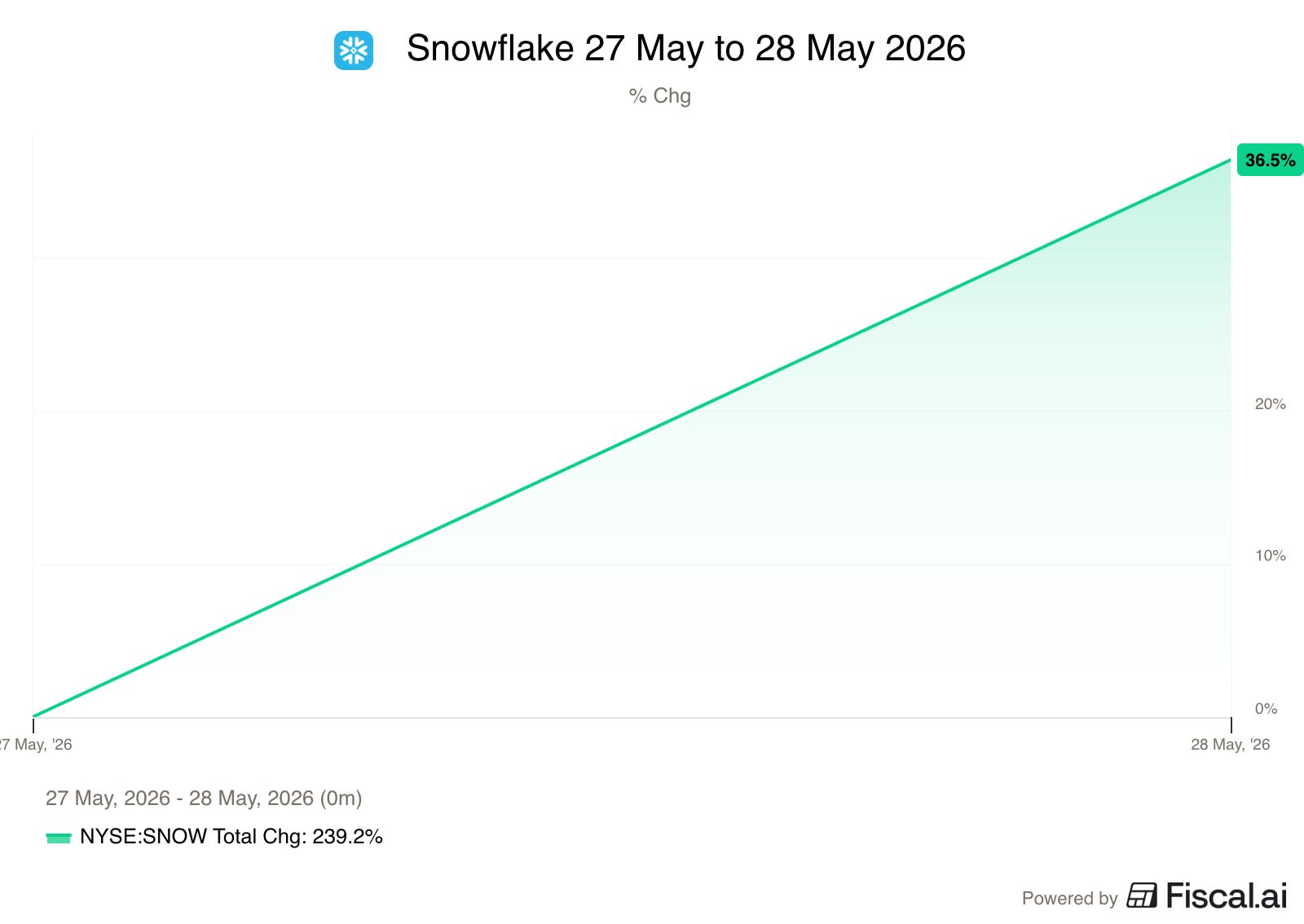

Every day we seem to be presented with examples of what the rise of passive investment is doing to the market in terms of volatility. On Wednesday 27th May Snowflake (SNOW US), a database company closed trading as a $60bn company and opened on Thursday as an $82bn one.

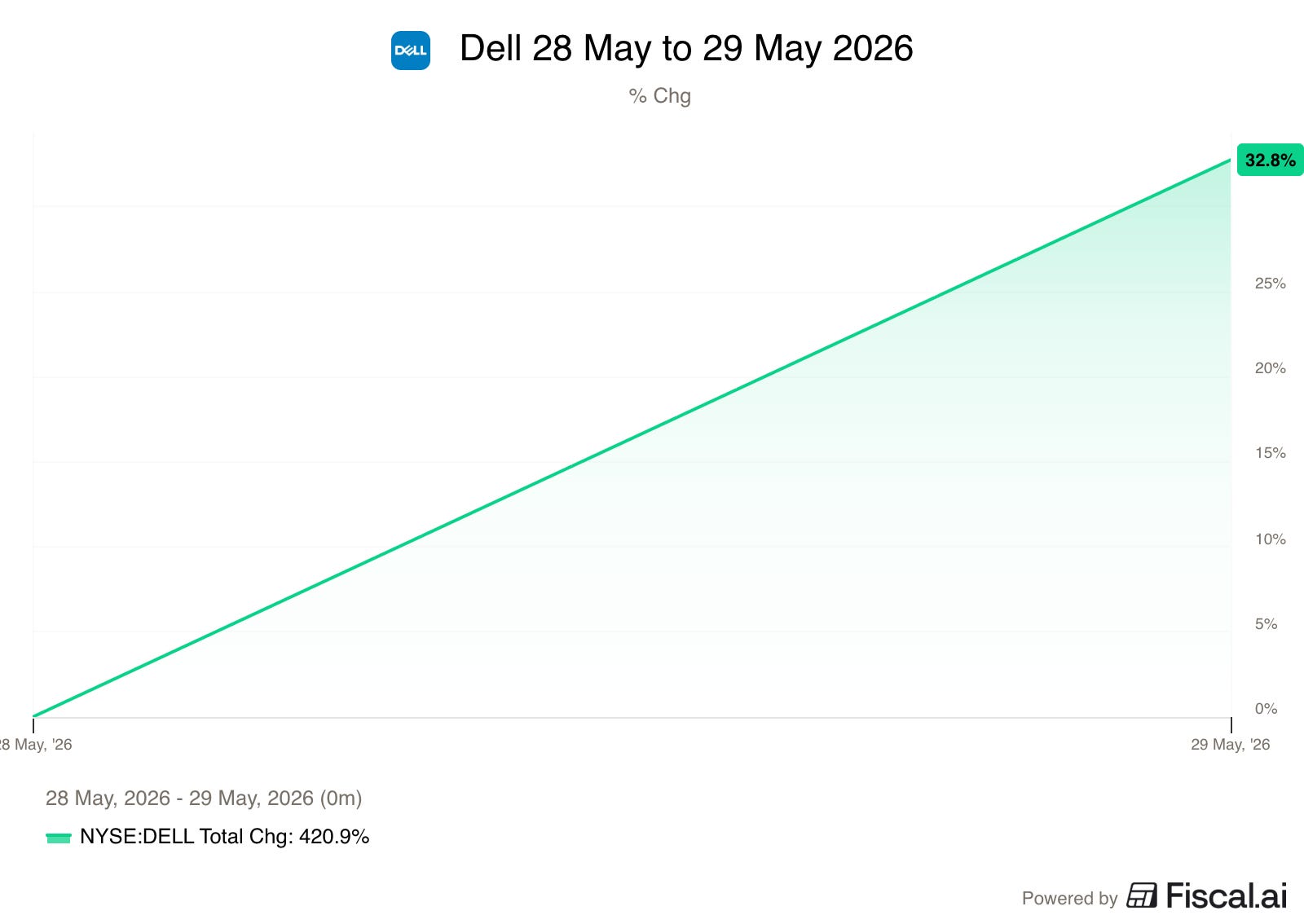

On that Thursday, the baton of volatility was passed to Dell Technologies (DELL US), the computer hardware company. Its stock closed as a $205bn company and opened on Friday as a $273bn one. That opening increase of 33% is after the shares had already doubled since the beginning of March.

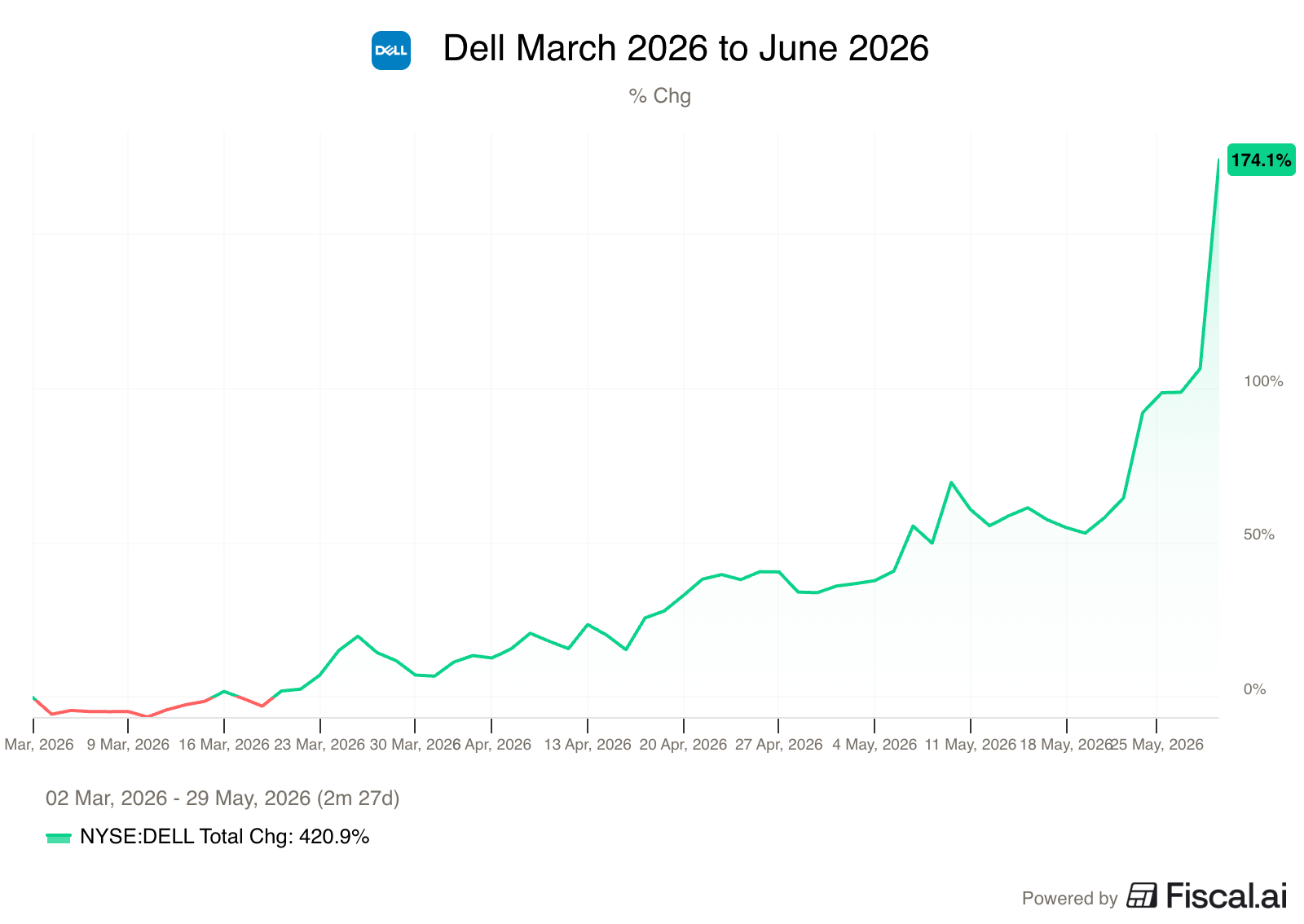

Here’s Dell’s three month run to a 174% gain in price.

There’s also the rise of concentrated ETFs to consider.

Let’s look at Cathy Wood’s ARK Innovation ETF ($ARKK) that became incredibly popular in 2020.

Here’s the flow of money into her fund.

Here’s the top 10 holdings of her fund in November of 2020.

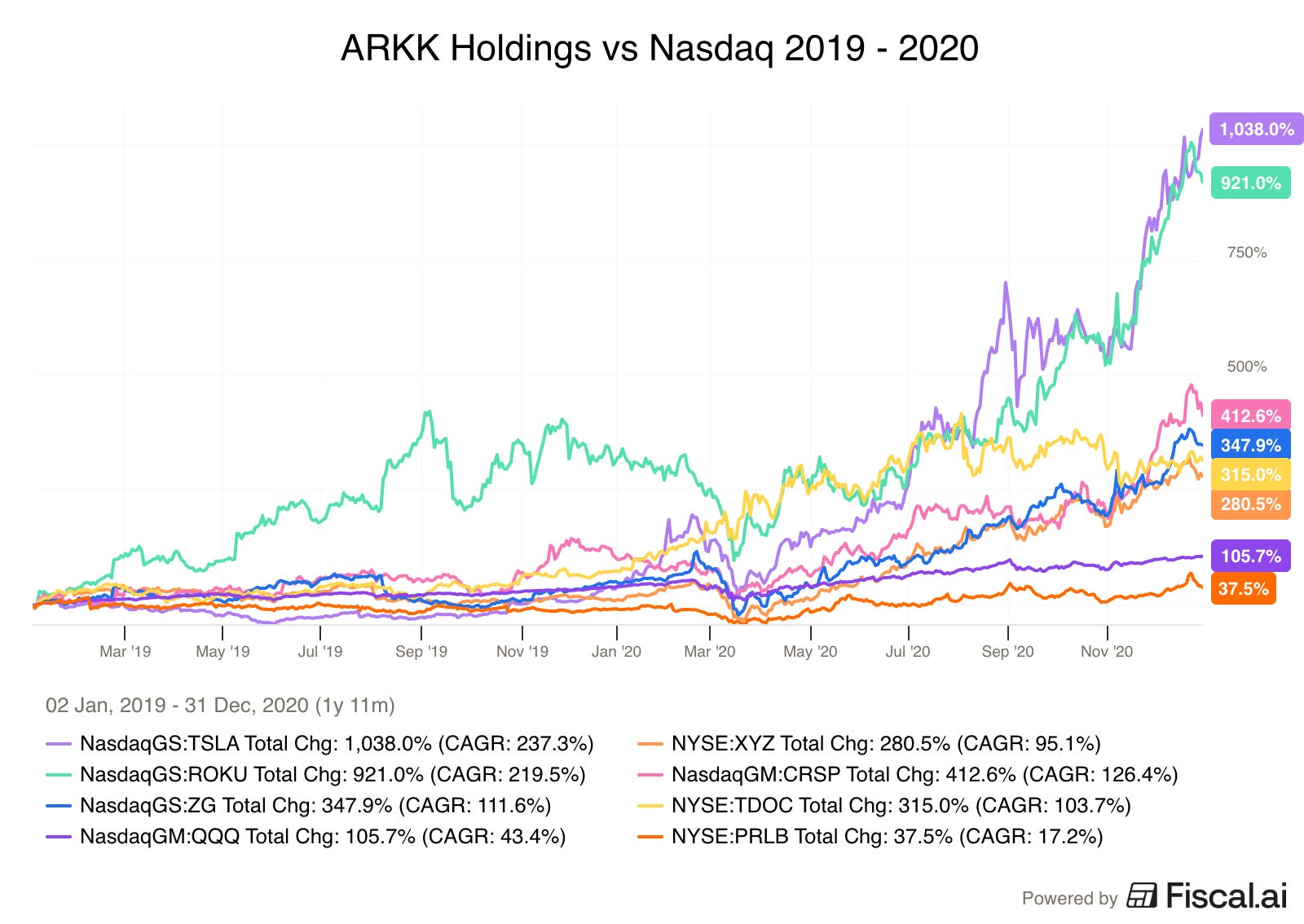

Here’s how they performed against the Nasdaq 100 from 2019 to 2020 during that massive inflow of funds.

Nasdaq 100: +102%

Tesla: + 1,038%

Roku: +921%

CRISPR Tech: +412%

Zillow: +347%

Block (Square): +280%

The only stock here that underperformed the Nasdaq was Proto Labs.

You could argue that Kathy Wood is an amazing stock picker, and that the flows into the fund had nothing to do with it.

But here’s the performance of the fund from 2019 through 2024.

And here’s the Assets Under Management.

These charts look incredibly similar, and there’s not an obvious lead or lag between when AUM moves and when the performance moves.

Could it be that when a lot of money flows into a concentrated fund, that fund buys a lot of stock and the prices go up?

And that when a lot of money flows out, the fund sells a lot of stock, and the prices go down?

ARKK isn’t even the worst example here - it’s got something like 40 holdings.

There’s the Mag 7 ETFs that hold… you guessed it - 7 stocks.

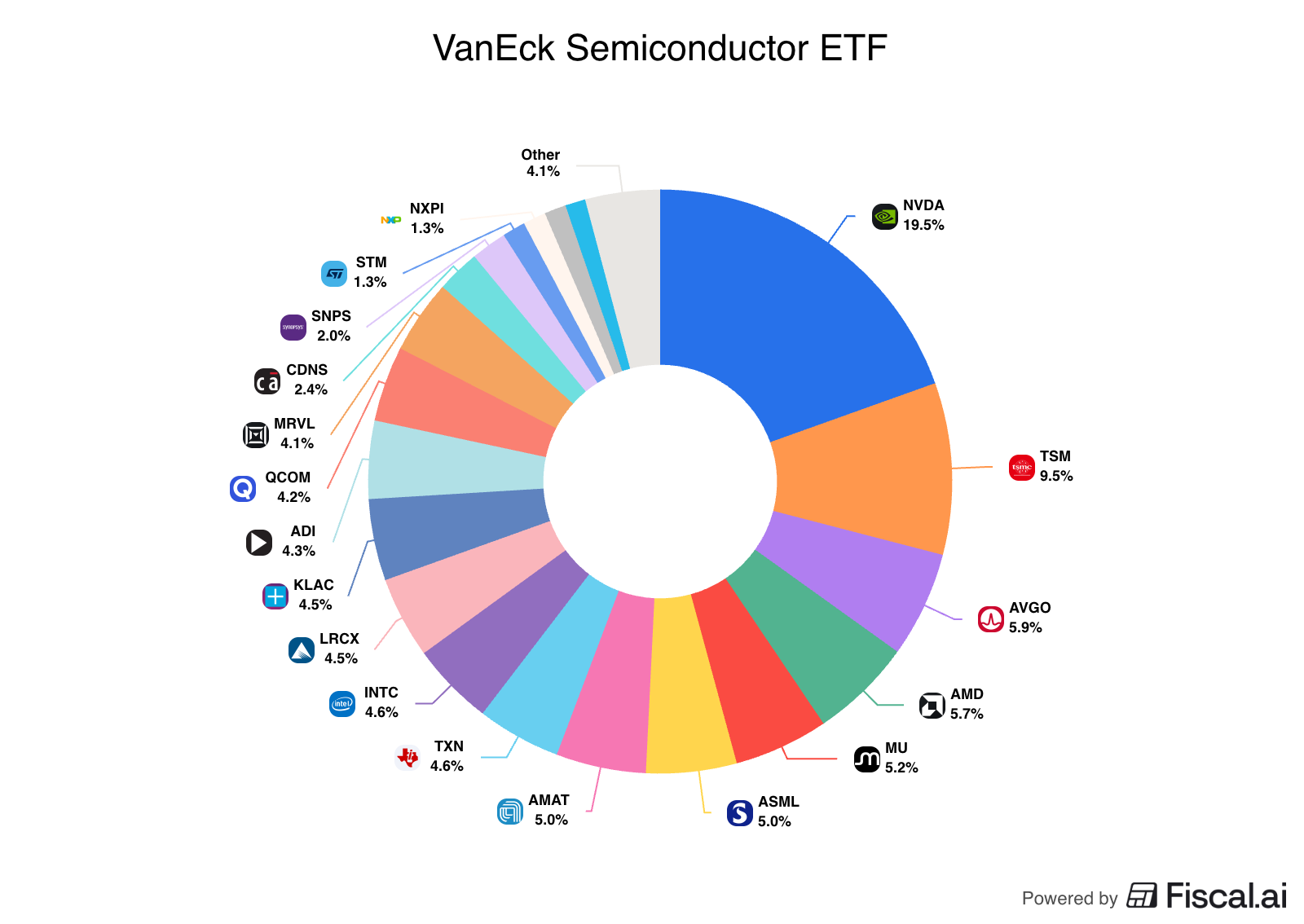

There’s the VanEck Semiconductor ETF, with 20 holdings, and nearly 20% of the entire fund in Nvidia.

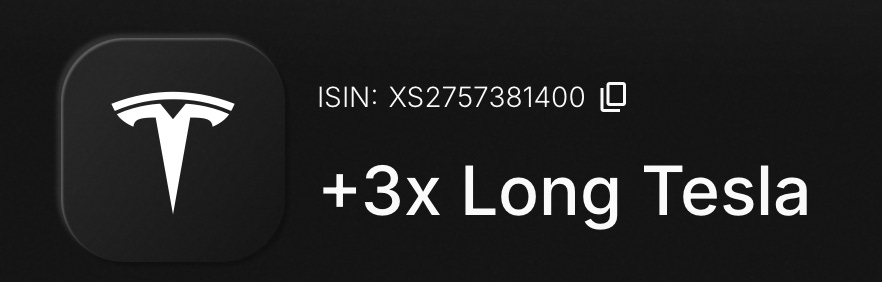

And if that’s not enough concentration in an ETF for you, there’s always options like the triple levered Tesla ETF from Leverage Shares.

Markets aren’t as elastic as we thought

A lot of investors assume that because stocks like Nvidia or Tesla are so large that flows in and out of ETFs or index funds wouldn’t affect them much.

And that’s the assumption the academics made for a long time.

Standard asset-pricing models assume that the market is elastic.

Meaning that it doesn’t react a lot to buying or selling.

These classic models use an elastic multiplier somewhere between 0.05 and 0.1 for the U.S. stock market,

With a multiplier of 0.05, a buyer of 10% of the stock market will lead to just a 0.5% increase in prices.

But a paper published in 2021 called ‘The Inelastic Markets Hypothesis’ found that the multiplier could be as high as 5.

In that world, a buyer of 10% of the stock market would cause prices to rise by 50%.

The volatility we’ve seen so far may be a small preview of what’s possible

So far we’ve only seen assets added to passive vehicles.

Part of this is due to the low cost, and the feedback loop that may have driven up the performance.

But part of it is also the U.S. retirement system.

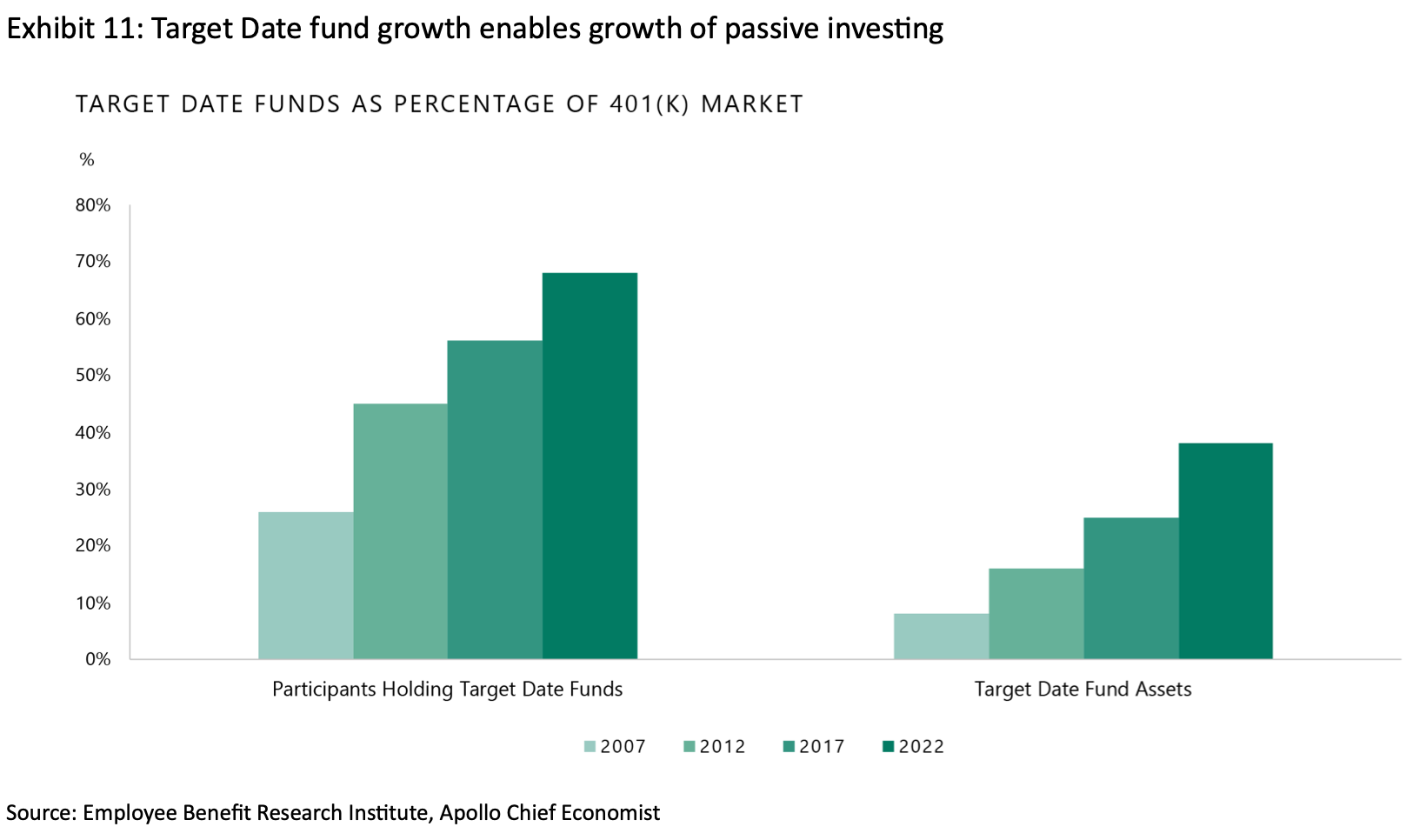

In the U.S., most workers save for retirement using an account called a 401(k).

Instead of the company guaranteeing a pension, employees automatically have a portion of their paycheck deducted every single month to invest for themselves.

Because of legislation passed in 2006, when a new employee starts a job, they are automatically enrolled into this system.

If they don’t explicitly choose where to put their money, the system default to putting their investment into a Target Date Fund (TDF).

Assets held in TDFs have gone up every single year since 2006.

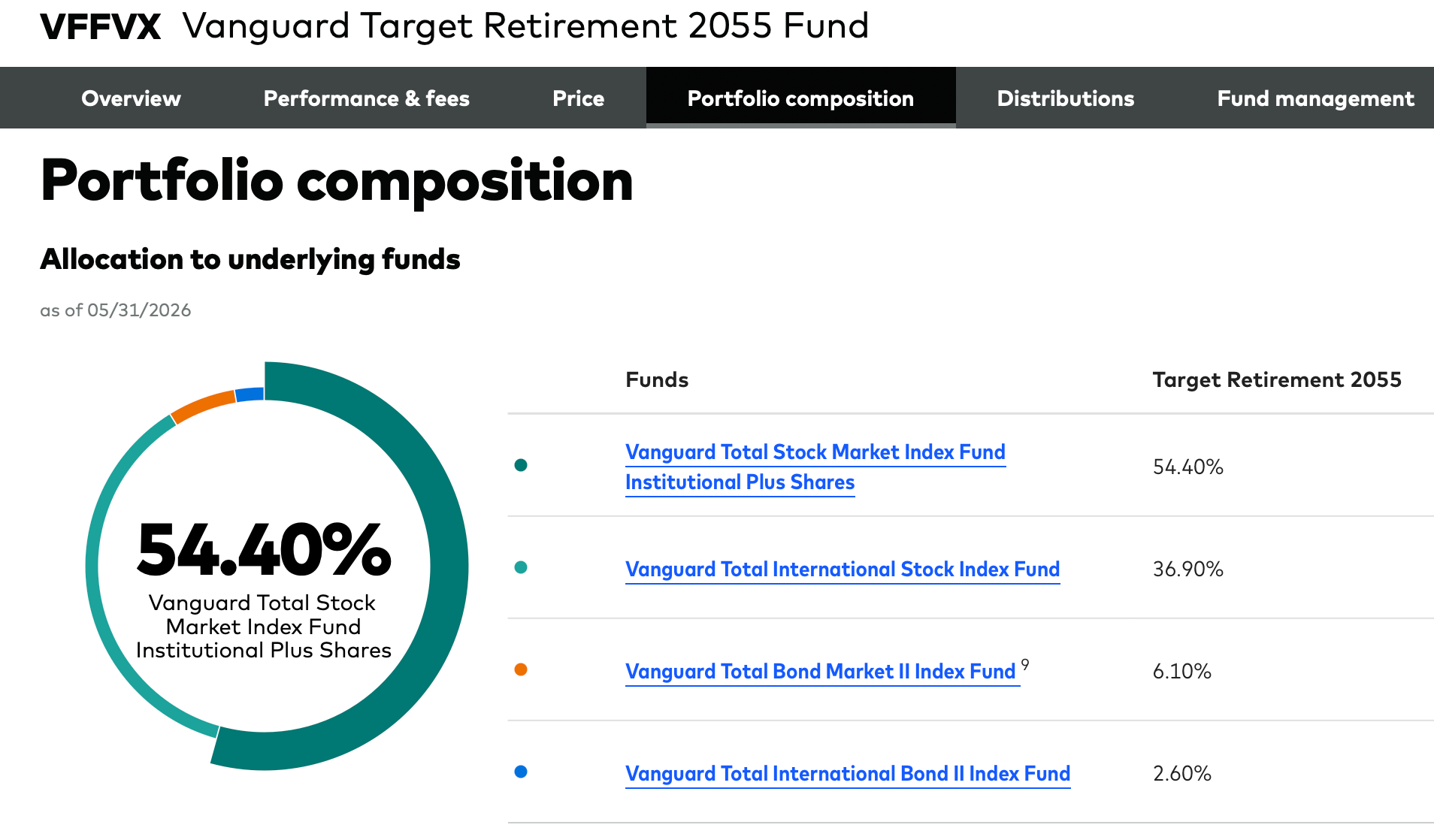

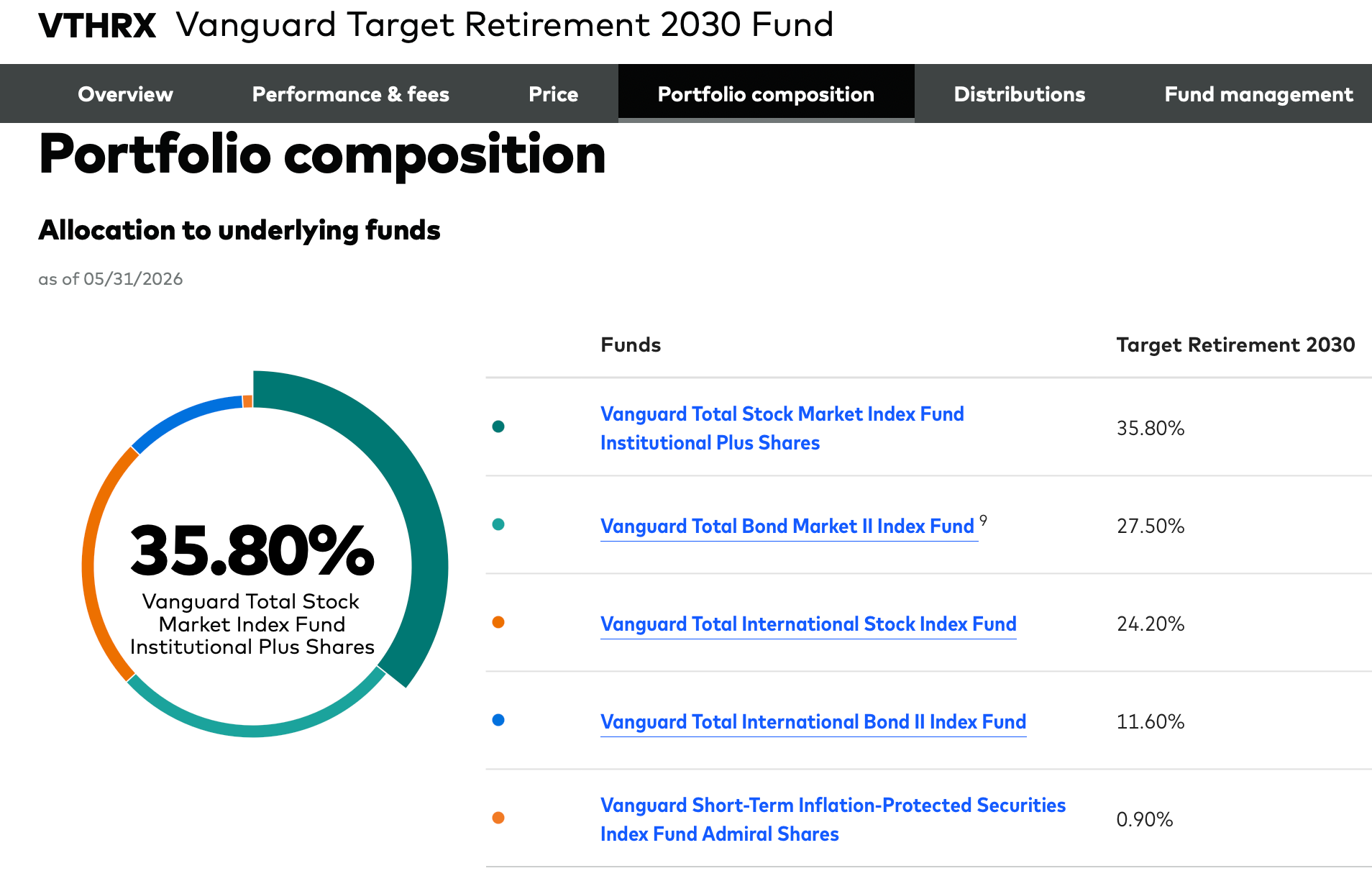

Target Date Funds are a mix of investments that automatically adjusts the risk level based on the year the worker plans to retire.

The vast majority are made up of some mix of passive index funds.

A worker that plans to retire in 30 years might end up in Vanguard’s 2055 TDF.

That would put them in a mix of 90% stocks and 10% bonds.

But someone retiring in 5 years might be in Vanguard’s 2030 TDF.

They would be in roughly 60% stocks and 40% bonds.

This all means that every single month, millions of American paychecks are automatically docked, and billions of dollars are put into these passive funds, regardless of stock valuations or market conditions.

It also means as the people who hold them age, there will be automatic selling of stocks to buy bonds.

The 401(k) hasn’t been around that long.

It came into law in 1978, and started to get popular in the 1980’s.

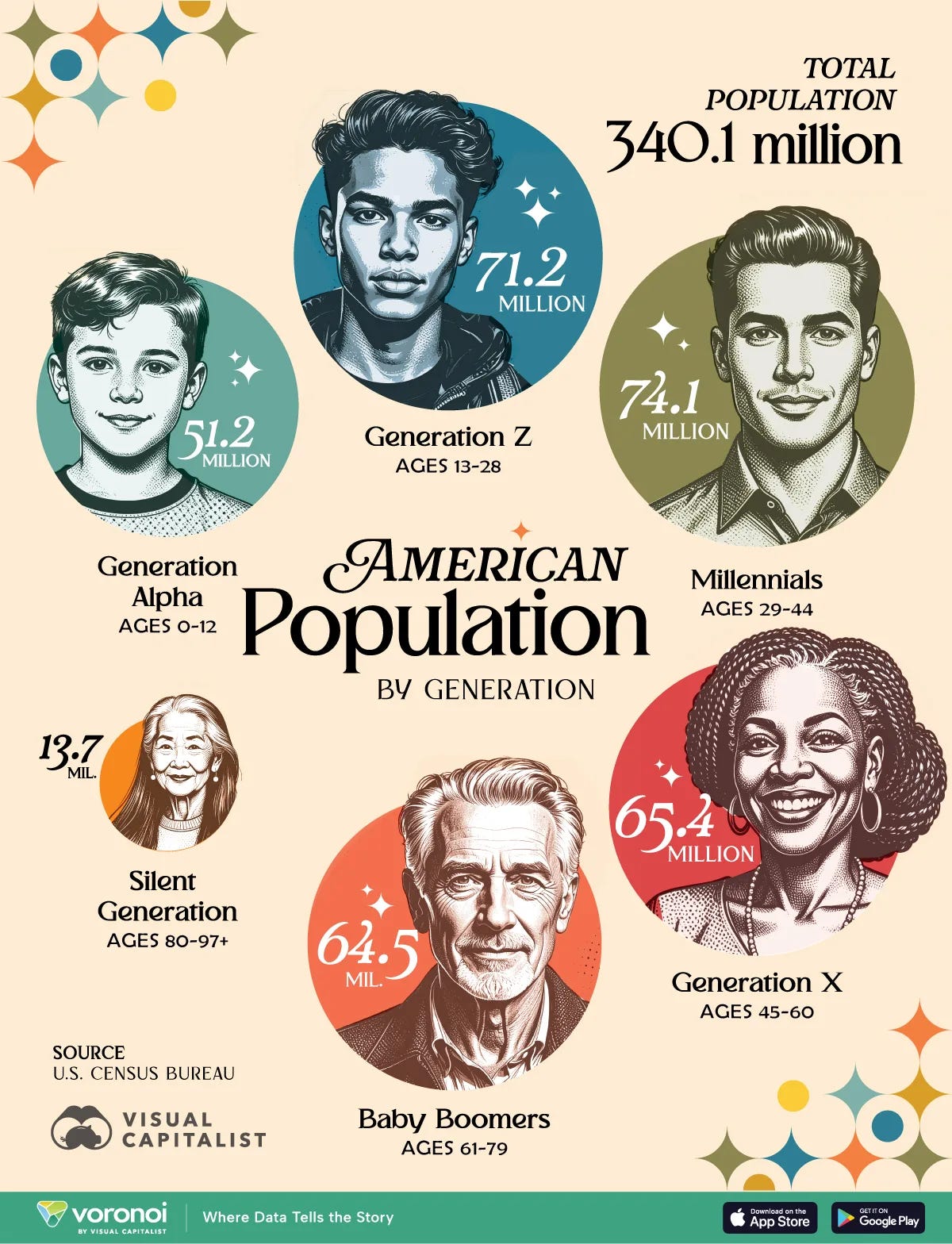

That means that most of the Baby Boomers have traditional pensions, and it’s really Generation X that will be the first to retire mainly on 401(k) assets.

Many of them may not be in TDFs, but there is another mechanism that will force selling.

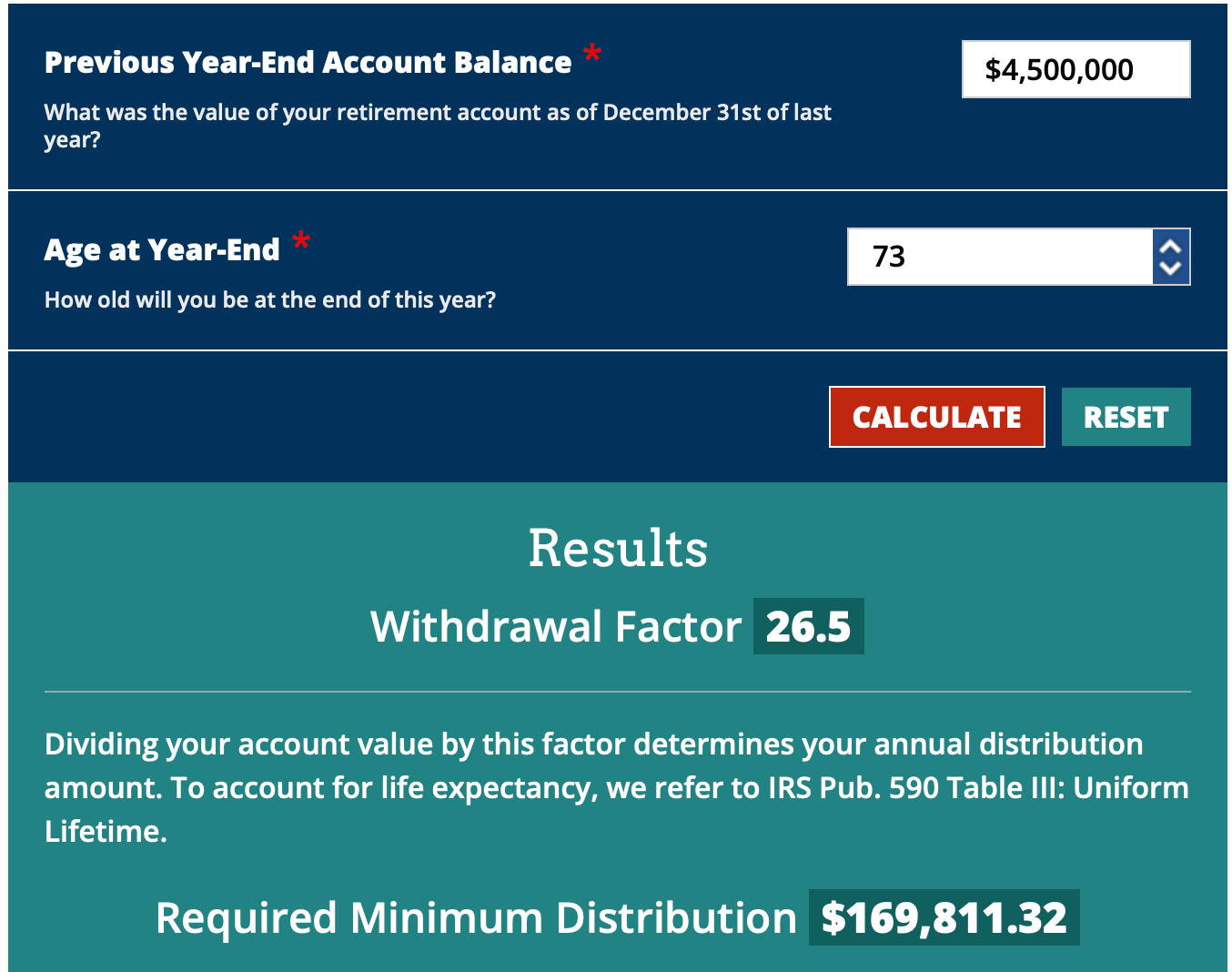

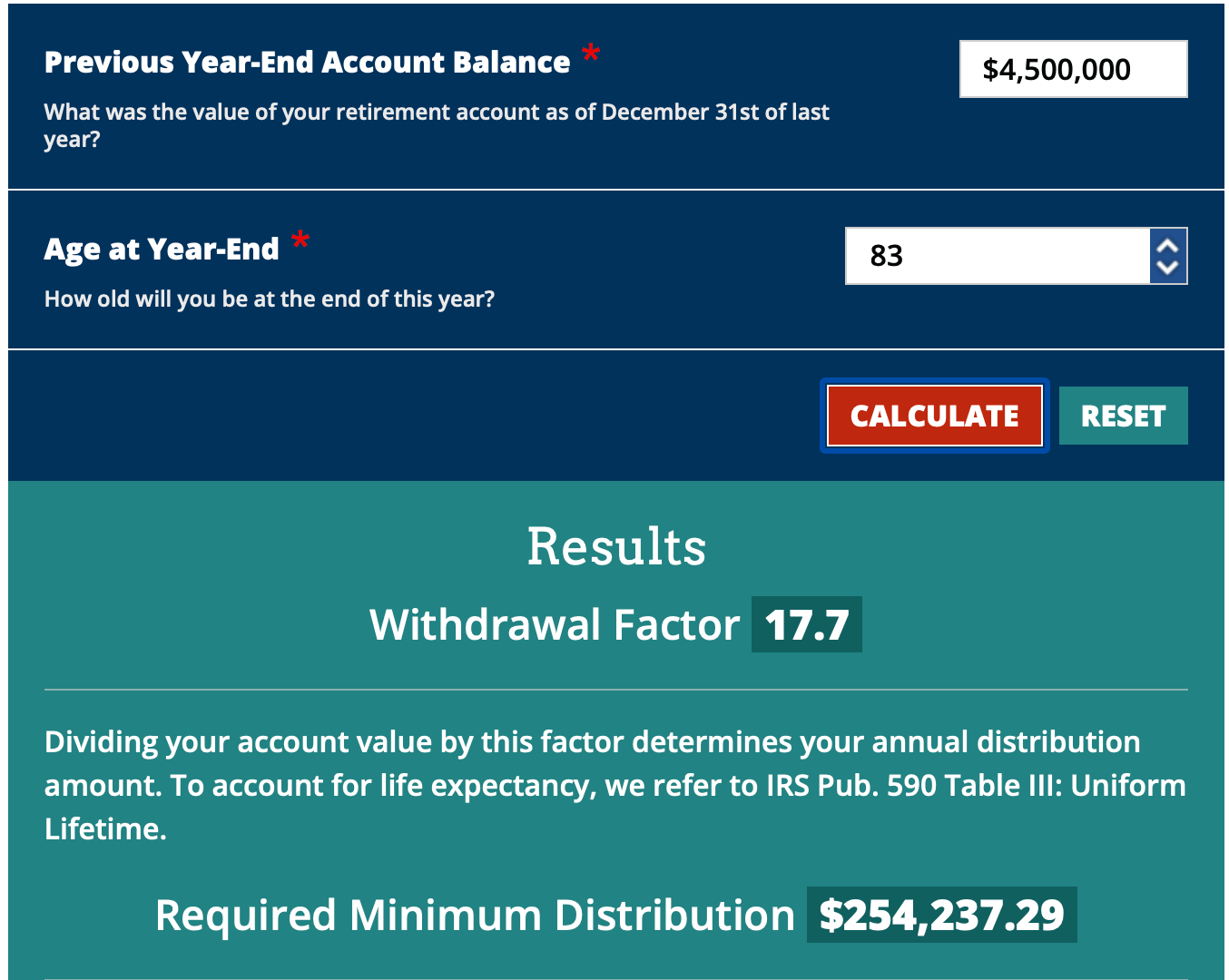

The Required Minimum Distribution (RMD) says that when you turn 73, you must start taking withdrawals from your 401(k).

How much depends on your age, but let’s do some rough math.

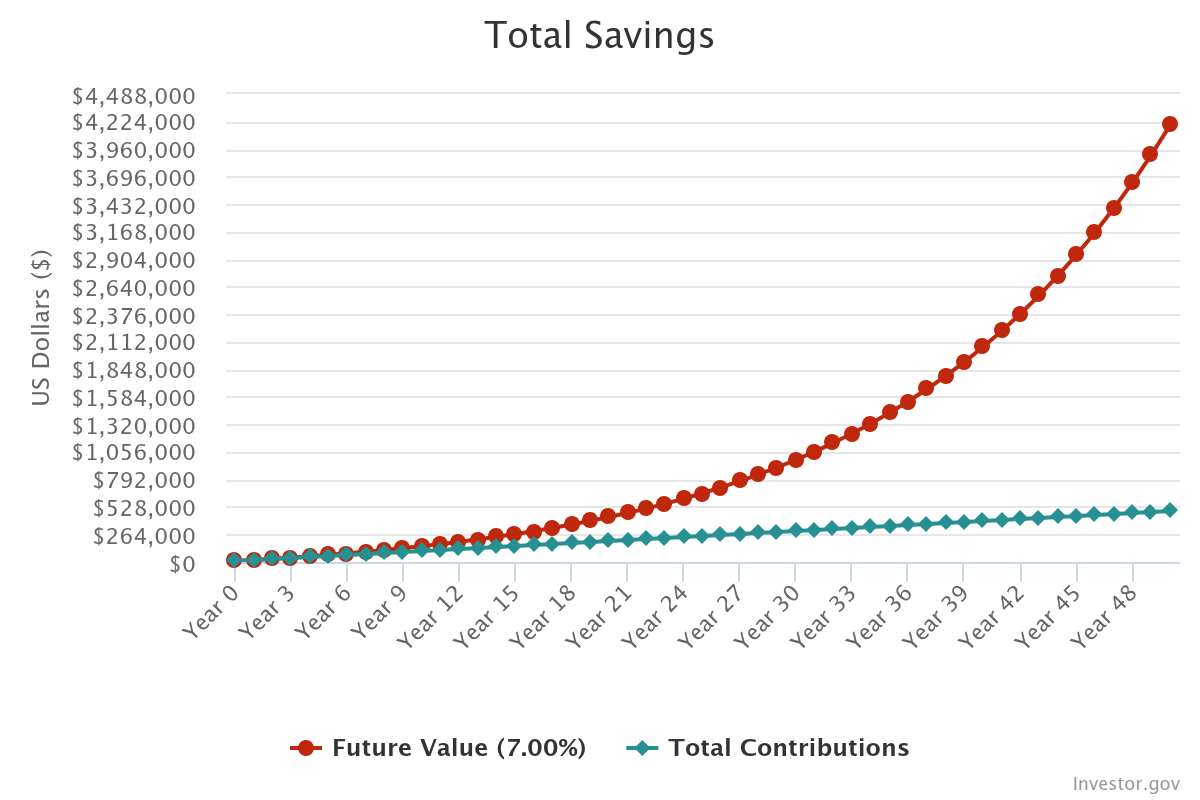

Let’s say an investor is turning 73 this year.

They started saving at 23, so they’ve been investing 50 years

Initial contribution: $10,000

Monthly investment: $800

Rate of Return: 7% per year

That investor now has nearly $4.5 million in their 401(k).

Now let’s figure out what they have to withdraw this year.

This investor’s RMD is roughly $170,000.

If we apply the 5x elasticity factor, to all of the RMDs, they could have significant impacts on the market.

And the older you get, the higher this number goes.

Here’s what happens when that same investor turn 83.

So at some point, we’ll have Generation X automatically selling stocks because of RMDs and Millennials automatically selling stocks as their TDFs buy bonds to reduce risk.

If the younger generations aren’t doing enough passive buying to offset this, we could see passive flows shift negative.

At that point, the feedback loops that have driven the U.S. market up could start to work in reverse.

How do we survive this?

If the U.S. stock market is driven by an automated retirement machine, and passive investing is taking the capital from active investor, who’s going to be around to buy when passive investors start selling?

In Part 3, I’ll show you what I’ve done to protect against this.

I’ll show you why Terry Smith had to panic, why you don’t have to, and how to actually turn this market distortion into an advantage.

Keep an eye on your inbox.

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.