Why Berkshire is selling world-class businesses

Every quarter, managers with over $100 million in assets have to report their holdings.

This year, Berkshire Hathaway’s 13F was particularly interesting.

It represents the first quarter since Greg Abel took over and there were some big changes, and some big lessons we can take away - let’s dive right in!

First, let’s look at the changes made to the Berkshire Hathaway portfolio.

In the first quarter, Greg Abel:

Added to 4 existing positions

Bought 2 new companies

Reduced holdings in 6 companies

Completely sold out of 16 (!) companies

This looks dramatic - it’s rare for Berkshire to completely exit so many businesses in a quarter.

There was lots of chatter on social media about it.

But this is a great example of needing to have a deep understanding of what’s going on.

For anyone following the company, we knew a month ago that there would be positions that were completely sold.

Todd Combs’ Exit

What looks like a sudden portfolio housecleaning is really the result of a shift in Berkshire’s investment team.

Todd Combs departed Berkshire Hathaway to lead a new $10 billion Strategic Investment Group at JPMorgan Chase in December.

For a quick refresher: Todd Combs was one of Warren Buffett’s two hand-picked investment lieutenants, working alongside Ted Weschler for 15 years.

In addition to managing a multi-billion dollar portion of Berkshire’s equity portfolio, Combs was also the CEO of GEICO.

When he left, Greg Abel and Ted Weschler were left holding an equities portfolio sprinkled with legacy positions they didn’t personally pick.

Why Abel Cleaned House

Looking down the list of the sold positions, you might find yourself scratching your head.

Berkshire fully dumped companies like Amazon, Visa, Mastercard, and Atlanta Braves Holdings.

If you look at the fundamentals, these are world-class operations:

Visa and Mastercard have a virtually unbreakable global payments duopoly

Amazon remains an absolute juggernaut in e-commerce and cloud infrastructure

The Atlanta Braves are a unique, one-of-a-kind sports franchise asset

So, why did Abel sell? Did these businesses suddenly turn into bad investments?

Absolutely not.

The problem isn’t the underlying businesses, it’s that he doesn’t own the investment thesis.

Greg Abel and Ted Weschler obviously understand how Visa or Amazon work.

But they didn’t initiate these specific positions, they were Todd Combs’ picks.

If you inherit someone else’s stocks without doing the work on them yourself, you simply don’t have the conviction to defend them when the market gets volatile.

- by Edward Finley—Richardson")

They didn’t build the original valuation models or live and breathe the day-to-day thesis of these specific holdings the way Combs did.

Which creates a serous problem - they won’t know when to sell.

They may not recognize exactly when a core thesis is breaking, or when the valuation is completely ridiculous.

Instead of holding assets they don’t closely track, Berkshire’s remaining team decided to sell them.

They cleared out any positions they didn’t have 100% intellectual ownership of.

What Abel Is Buying

Abel did redeploy capital into businesses where the current team does have conviction.

This quarter, Berkshire made a few large moves:

Delta Air Lines (DAL): Berkshire has been wary of airlines in the past, and got surprised by the Covid pandemic the last time they invested in them, but they’ve built a $2.65 billion stake in Delta, betting heavily on the carrier’s surging premium cabin and loyalty revenue.

Alphabet (GOOGL) & The New York Times (NYT): They added significantly to their positions in Google and built a $1 billion+ stake in the Times.

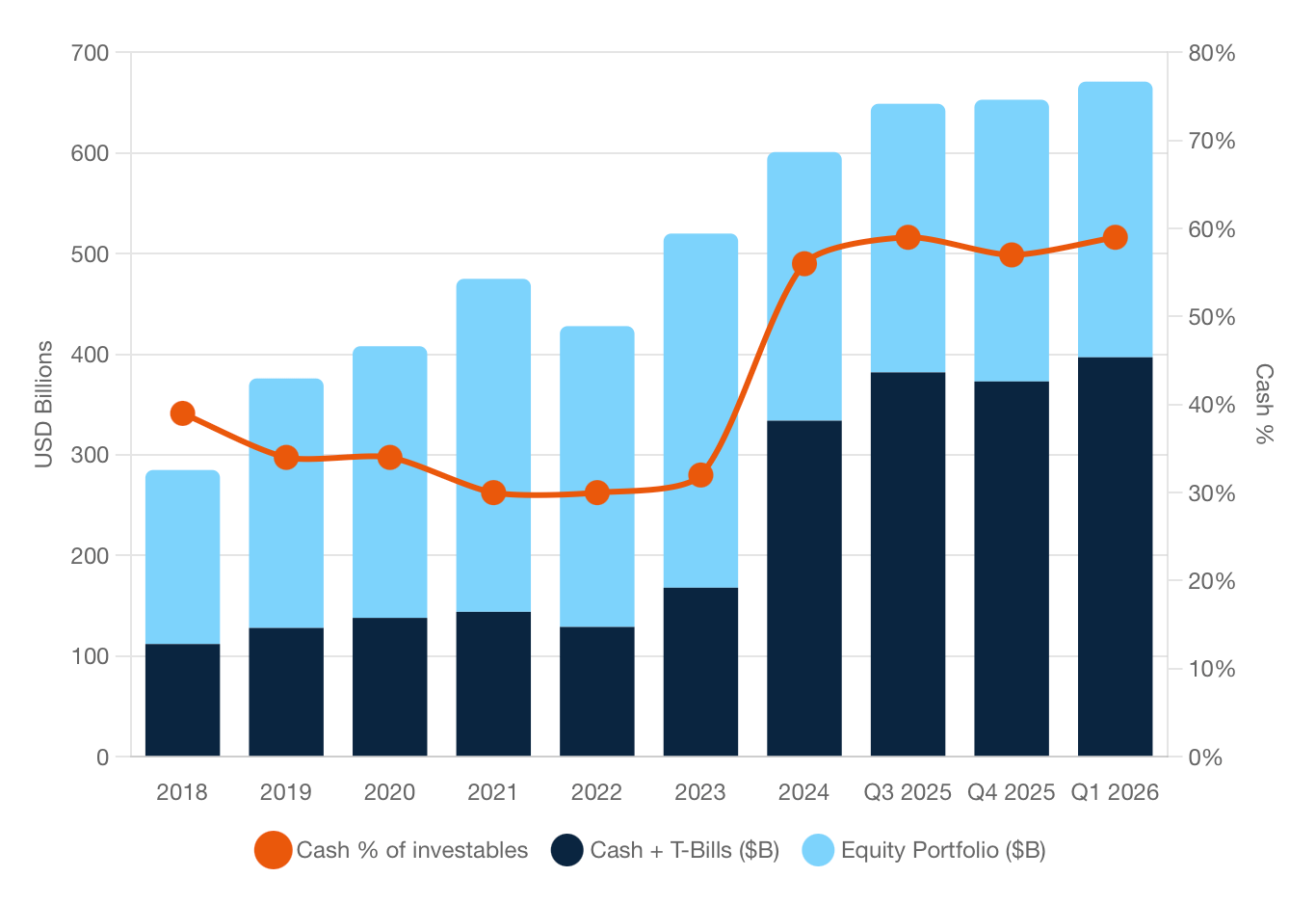

Meanwhile, what they didn’t deploy into equities went straight to the balance sheet.

Berkshire’s cash hoard is now a record $397.38 billion.

That means cash is now nearly 60% of Berkshire’s investable assets.

There was one other notable buy - Greg Abel personally bought $15 million worth of Berkshire Hathaway stock.

Again, not a surprise for anyone following the company as Abel announced that he planned to spend his salary on Berkshire stock a while ago.

But it does show that he is aggressively eating his own cooking.

You Can’t Borrow Conviction

This brings us to the important lesson that every investor needs to remember.

13F filings are an incredible tool for idea generation.

Seeing what the brightest minds in finance are buying can help you find businesses that you otherwise might have completely overlooked.

But that is where the utility of a 13F begins and ends.

You can easily borrow an investment idea, but you can never borrow conviction.

When you buy a stock because Berkshire (or any other money manager) is holding it, you are outsourcing your critical thinking.

What happens when the stock drops 20% (or more)? If you don’t know the exact thesis, you could panic and sell at the worst possible time.

What happens when the competitive landscape shifts? If you didn’t do your own research, you won’t know if the company’s moat is still intact.

You have to do your own homework, develop your own deep understanding of the business, and make your own informed decisions.

Knowing what you own and why you own it is what keeps you rational during market volatility.

Build your own conviction, map out your own circle of competence, and invest accordingly.

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data