Why Buying Cheap Isn't Enough Anymore

Unless you're a dividend investor...

I recently listened to an episode of the ‘Value Investing With Legends’ podcast that did a good job of putting a lot of my own thoughts on the markets and investing into a nice structure.

The guest was Ricky Sandler.

His message? Markets have changed because investors have changed.

Let’s dive into what he said!

Ricky Sandler is the Founder and CEO of Eminence Capital, an $8 billion global equity firm launched in 1999.

He invests based on company fundamentals, using a long-short strategy.

They do deep research and he tends to have a contrarian mindset.

His Investment Philosophy

Sandler says he focuses on the gap between the market’s perception and the business’ reality.

He’s looking for good businesses that are out of favor with the market for some reason.

Here’s a bit more about his philosophy:

Quality & Moats: He looks for companies with strong Return on Invested Capital (ROIC) and sustainable competitive advantages.

Owner’s Mindset: Sandler will engage with boards to improve Capital Allocation, making sure profits are used to create shareholder value.

Diversification: He holds around 40 positions, and his largest are <5% of the portfolio.

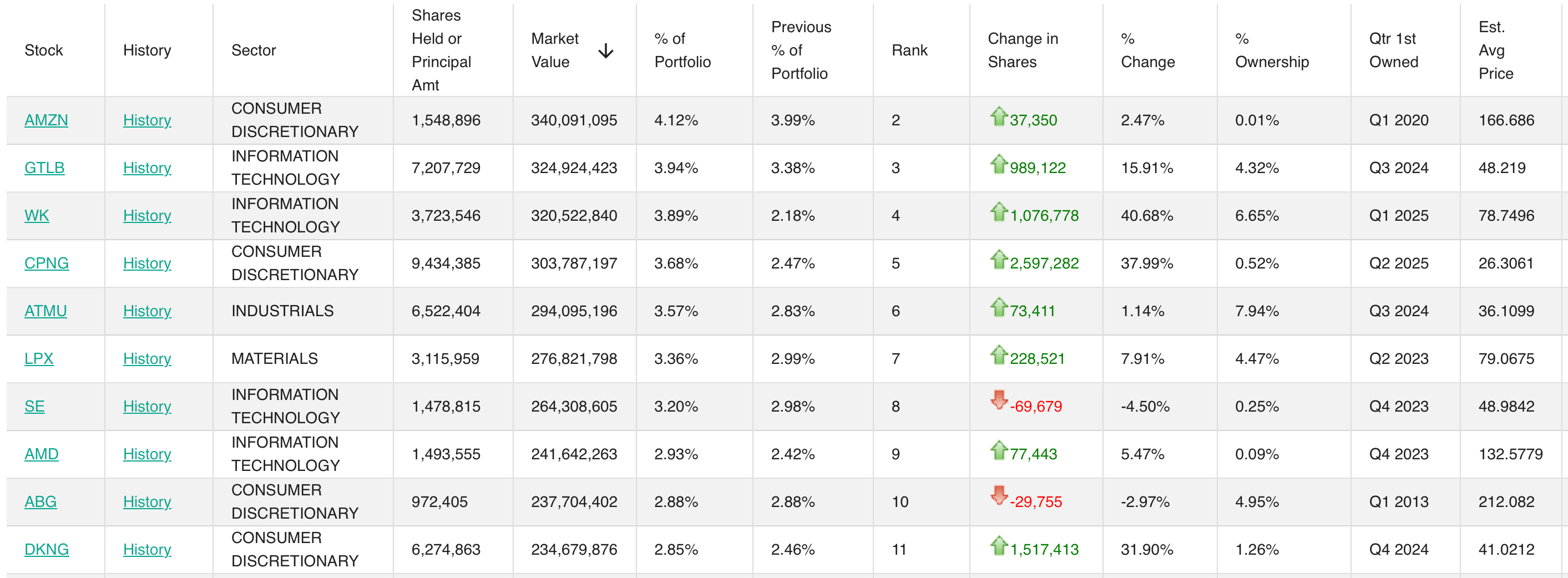

Here are the top 10:

So far, that sounds like a pretty standard approach, but the interesting part is how his strategy has evolved.

When he started 30 years ago, buying a good business cheap was enough.

Here’s what he said in the interview:

“early in my career, it was enough to have the right business at the right price and things took care of themselves because most market participants were doing bottoms up research and in time, the gap between what we thought fundamental value was and the market's price would close and we would be able to earn that higher compounding rate of both a business that compounds and a business that rerates.”

Sandler doesn’t think that’s still true.

The Market Has Changed

Sandler realized that in a post-GFC world, buying cheap is no longer enough.

He says that the market has changed because the investor base has changed.

The market is no longer dominated by bottom-up fundamental investors.

Today, it is driven by:

Passive Flows: Automatic buying that ignores intrinsic value

Thematic Investors: Short-term traders focused on stories rather than businesses

Algorithmic Trading: Machines reacting to data and price patterns, not business quality

Pod Shops: Hyper-focus on short-term inflections, leading to extreme volatility

None of these investors are looking at business fundamentals.

That means that when a stock falls out of favor (or becomes popular) the rubber band of mispricing can stretch further, and stay that way for longer than it did 20 years ago.

Here are some of the shifts and opportunities this creates.

Momentum

Momentum is such a strong force in today’s market, it deserves its own section.

Here’s the simple way to think about it:

Momentum is the market’s tendency to keep moving in the same direction.

If a stock’s price has been rising over the last 6 to 12 months, investors and algorithms bet it will keep rising.

It is the opposite of investing based on fundamentals.

While we focus on things like Free Cash Flow, momentum ignores the business and trades the chart.

In today’s market, momentum has become a self-fulfilling prophecy driven by three main groups:

Quants: Their models have momentum explicitly programmed into them

Pod Shops: Focus on 90-day performance, so they only want to own what is working right now

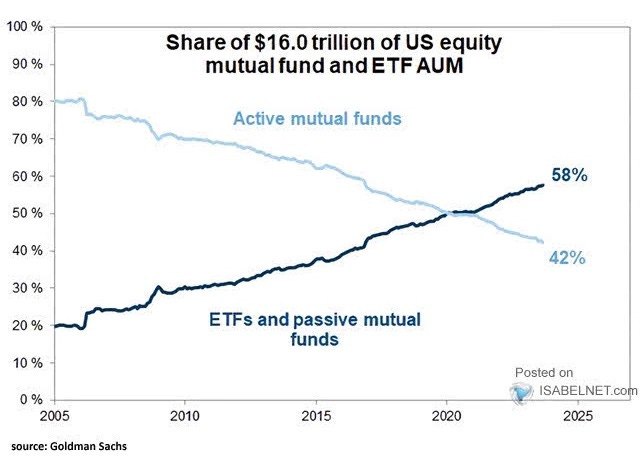

Passive Flows: Cap weighting means the biggest winners get the most money, pushing their valuations higher and pulling in even more money

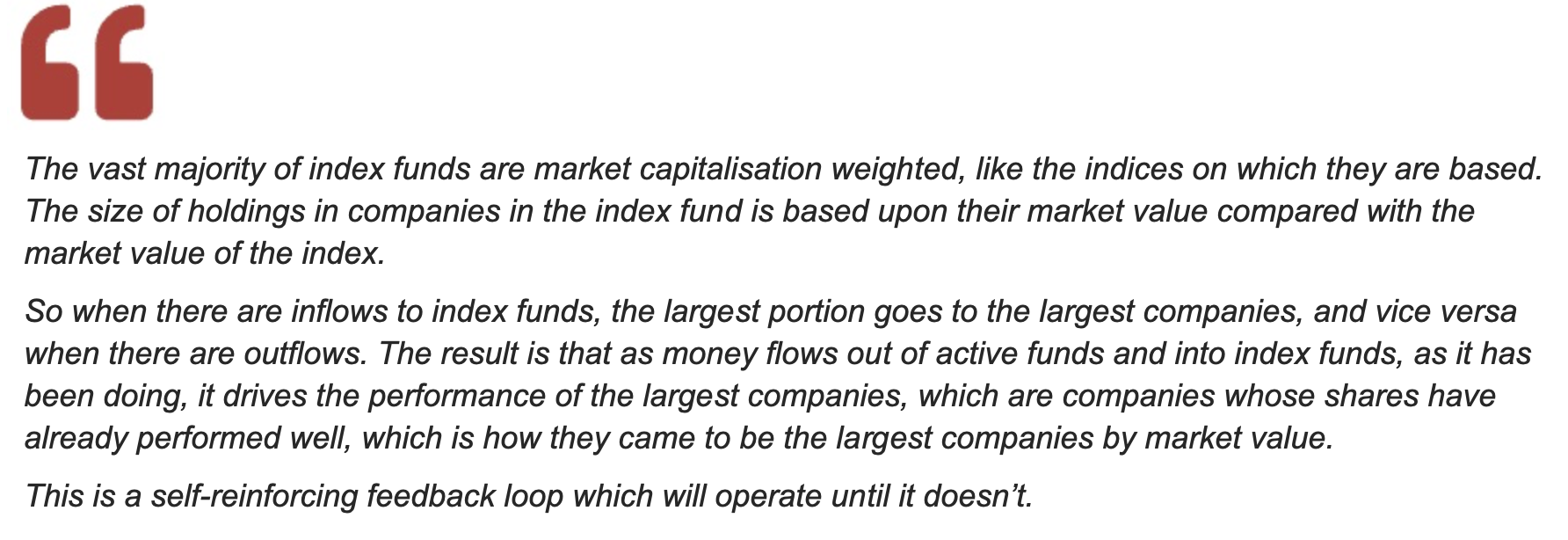

Here’s what Terry Smith said in his 2025 annual letter about passive flows:

Because everyone is looking at the same signals, momentum alone can cause the valuation rubber band to stretch further than ever before.

Overvaluation: Good stories become bubbles as momentum investors - you can also look at the concentration in the top stocks of the S&P 500 to see this effect

Undervaluation: Great businesses with a short-term problem get sold, then the selling accelerates because they have negative momentum

Negative momentum can actually explicitly prevent funds from buying companies

How Sandler Takes Advantage

Knowing these shifts have happened and understanding the opportunities they create isn’t enough.

If you just wait for the market to realize its mistake, you could be waiting a long time (or forever).

Remember that most investors are looking at the stock instead of the business.

Sandler looks for good businesses, with cheap stocks, and tries to find what will cause a Perception Shift - the change in how the market views a business.

“A stock doesn’t go from 12x to 18x earnings just because you think it’s worth it. It moves because other investors change their minds.”

What triggers a shift?

Removal of an Overhang: Resolving a legal issue, one time charges rolling off the past few years of earnings, divesting or spinning off a bad acquisition, etc.

Negative to Positive Momentum: If a stock stops screening poorly for quants and pods, they’ll start buying

Market Cycles: Changes in interest rates, a market going from oversupply to undersupply, or macroeconomic cycles can all change investor perception

If you don’t understand why a stock is cheap and what will change that perception, you risk holding a value trap for years.

If you get them all right, you can generate serious returns.

Three Engines of Returns

We can get returns on an investment from 3 places:

Business growth: The business continues to compound its Earnings Per Share (EPS) and Free Cash Flow while the market is looking the other way

Multiple expansion: When the perception shifts, the P/E ratio rerate (e.g., from 12x to 18x) gives you a one-time boost to your returns

Shareholder yield: Buying at a low price gives you a higher starting yield, and makes any buybacks a lot more valuable

The Dividend Investor Advantage

I think shareholder yield is the most under appreciated part.

For an investor that’s focused on stock prices, holding an undervalued company for a long time is a risk to their returns.

For an investor focused on shareholder yield, it’s a huge advantage.

Here’s why:

Higher Starting Yield: If a company pays a $2.00 dividend, you get a 4% yield at a $50 stock price, but only 2%at $100 - a lower price means you are being paid more to wait

Accelerated Buybacks: When a company buys back stock at a low multiple, it retires more shares per dollar

This either reduces the total dividend outlay for the company, or raises your dividend per share while increasing your ownership of the company.

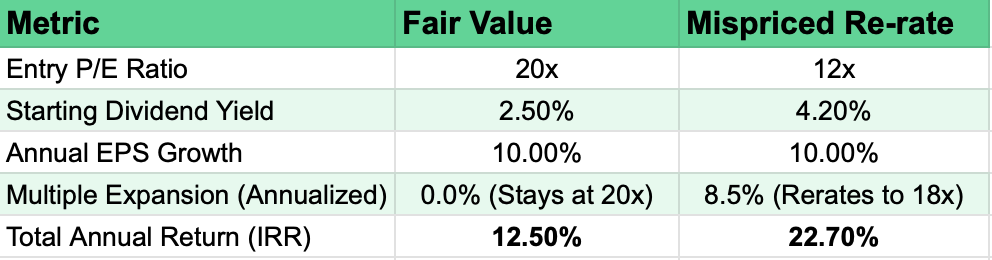

The table below compares a company bought at fair value, and one that was bought misprcied and re-rated.

$10,000 at a 12.5% return over 5 years becomes $18,020

$10,000 at a 22.7% return over 5 years becomes $27,811

Final Thoughts

Ricky Sandler’s view is that the market can now remain a voting machine for much longer than it has in the past.

Between passive flows, algorithmic trading, quants, and pod shops the gap between a business’s reality and its market perception can stay wide for years.

For a lot of investors, this volatility is a source of anxiety.

For the Dividend Growth investor, it’s a massive opportunity to Live Rich.

Our Strategy

When the valuation rubber band gets stretched too far down, we don’t panic.

We know we own great companies that can keep paying us our dividends.

At lower prices, we’re excited that we can buy at higher starting yields, and that our companies can buy back shares at lower valuations.

Here’s why I’m very comfortable with what we own:

✅ Dividend Safety: We make sure our companies have sustainable Payout Ratios so the checks keep coming, even when the market perception is down

👑 Quality Moats: Our companies have strong competitive advantages that will let them keep compounding

📈 Sustainable Growth: Our companies have an average dividend growth of more than 15% per year over the past 5 years - I expect our dividends to keep compounding in the future.

In a market that’s becoming more short-term. your ability to focus on Shareholder Yield is a massive advantage.

The quants and algorithms can chase momentum.

We’ll be busy collecting a Higher Starting Yield and benefiting from Accretive Buybacks that increase our long-term ownership.

We’re getting paid a premium to own high-quality businesses at a discount.

When the Perception Shift finally hits, the rubber band snapping back with multiple expansion is just the cherry on top.

One Dividend At A Time,

-TJ

Don’t Miss Out

I am opening a limited number of discounted membership spots on February 24.

If you sign up for the waiting list today, I will send you My 10 Favorite Cannibal Stocks immediately. No waiting.

Why join the list?

Deep Discounts: Lock in one of our limited, discounted membership rates

Exclusive Bonuses: Waitlist members will receive a suite of exclusive bonuses (including 10 Dividend Stocks to Own Forever) that won’t be available to the general public:

📘 E-book with one-pagers of all our stocks

📊 Spreadsheet with the dividend growth of the portfolio

🚀 2 exclusive stock ideas for the launch

🎥 Video course: How to find great dividend stocks

🛒 Report: 3 Dividend Stocks to Buy

⭐ Report: Pieter’s 3 Favorite Stocks

🔍 Report: How to find 100-baggers

💵 10 Dividend Stocks to Own Forever

🏗️ Masterclass: Build Your Dividend Machine

🙋♂️ Exclusive Q&A With TJ and Pieter

Don’t leave your wealth to chance. Join the waiting list now.

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.

Very enlightening for a hardcore value investor long term investor like myself

I’ve always assumed the same about momentum; seems like hot potato to me. Glad to see some pros think like me. I’m thankful that after reading Buffet & Graham, I read Dremon & Neff too, strengthening my foundation of contrarian thinking. Taught me to be comfortable flipping stocks in 3-12 month windows, or longer, when opportunity presents itself. I have courage in my convictions & trust my methods & analysis. I look for value, but I look for companies growing faster than peers, while being more profitable, & at a cheaper valuation; stocks like SFM right now. Or I look at the numbers & find instances of fundamentals not matching valuation. Everybody knows FCF, profit margins, & ROIC have strong correlation to outperformance, but shareholder yield and the Piotroski F-score have some research backing them as well.

Buying PYPL at $40 earlier this month, I assume most people would think I was crazy, but it’s up 17% in 2-3 weeks (much faster than I anticipated happening) But looking at PYPL, I see shareholder, FCF, and earnings yields all > 10%, Piotroski score is 8/9, 5 year revenue and eps CAGR is almost 10%, 5 yr fwd EBITDA is almost 10%, ROCE,

& CROIC 17-18%, 5 year avg ROE & ROIC of 20 & 12, while supporting a P/E, EV/FCF, and EV/EBITDA multiple of 6-8.

Now hopefully momentum will do its thing with that initial spurt. We’ll see if the acquisition is legit.