Why Terry Smith is Changing His Strategy

Terry Smith made a lot of waves with his latest investment letter.

He doesn’t typically trade much, but in the first 6 months of 2026, he turned over more than 50% of his portfolio, and announced a shift in his investment style.

It seems dramatic, and it is.

Terry is making these huge changes because he believes the underlying structure of the market is changing.

This will be the first of a three-part series where we’ll talk about what Terry is seeing, if he’s right, and most importantly what you should do about it.

Let’s dive in!

Who is Terry Smith?

Often called “the English Warren Buffett,” Terry Smith is one of the world’s top Quality Investors.

He’s typically been a very straightforward and independent investor.

Here’s a quick bit of background on Terry.

Grew up in East London, was at the top his class in history at Cardiff, and entered banking at Barclays in the 1970s.

In 1992, he wrote Accounting for Growth, a book that exposed corporate accounting tricks and was so controversial that it got him fired.

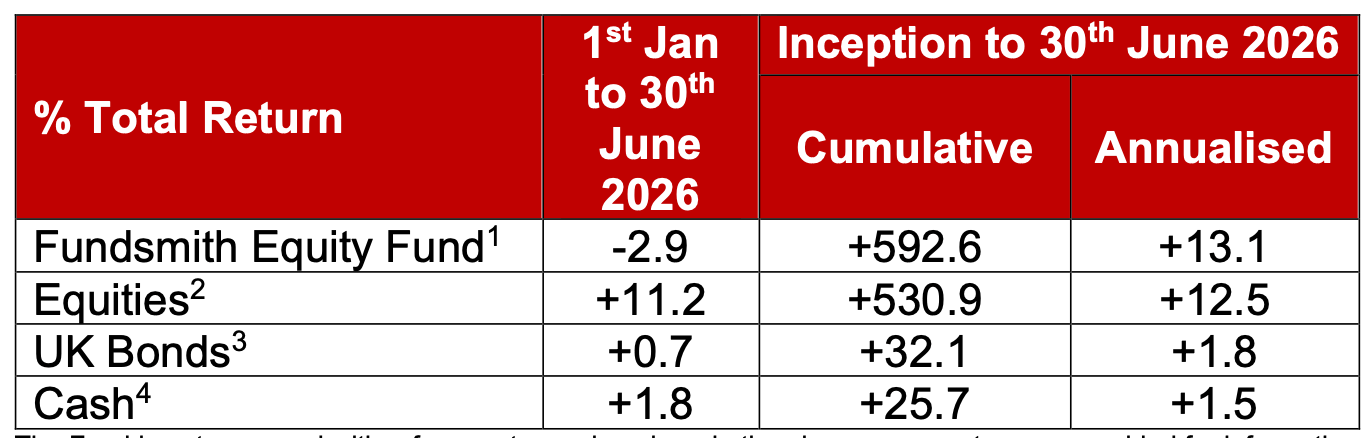

Launched Fundsmith in 2010. Today, it manages £12 billion and has achieved an impressive 13.1% CAGR after fees since inception.

His Investment Style

Terry Smith’s philosophy is simple.

He boils it down to three steps.

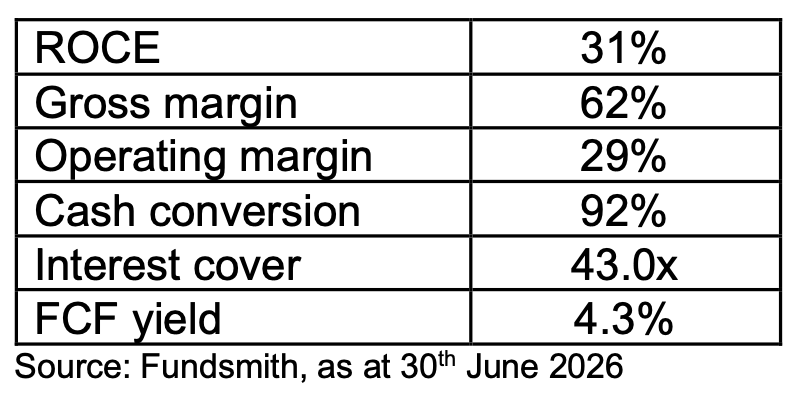

1. Buy Good Companies

Terry Smith looks to buy high-quality businesses that dominate their markets.

High ROCE: Looks for a Return on Capital Employed of 15–20%+

Wide Moats: Focuses on companies with pricing power and high gross margins

Cash is King: Prioritizes strong organic growth and businesses that convert a lot of their net earnings into free cash flow.

“I am constantly amazed at the number of people who talk about investment and spend most or all of their time talking about asset allocation, sector weightings, economic forecasts... and never mention any need to invest in something good.” — Terry Smith

2. Don’t Overpay

While quality comes first, valuation still matters.

He is willing to pay a fair premium for an exceptional business but tries to avoid overpaying.

3. Do Nothing

Minimizing trading keeps fees low and lets compounding do the work over time.

Patience has been one of Terry’s main advantages.

His Performance

Fundsmith does hold a portfolio of companies with great fundamentals.

And over the long term it has allowed the fund to outperform, with a CAGR of 13.1% after fees.

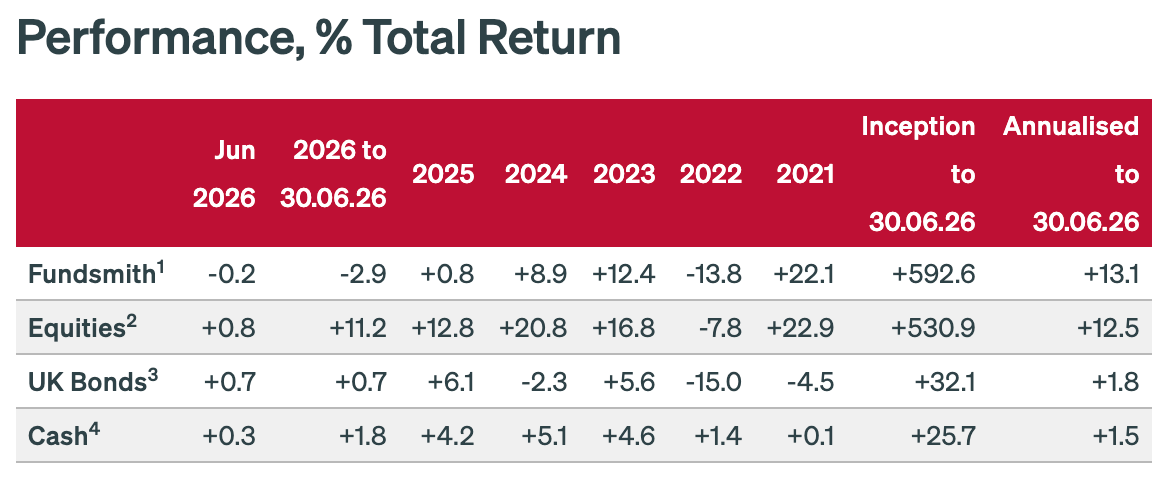

But it’s been underperforming each year for the past 5 years.

Which brings us to the letter Terry Smith recently wrote to his investors.

You can read it here. (I recommend that you do.)

His Letter

There are two things I want to focus on from Terry’s letter.

Why he thinks he’s underperformed

How he’s shifting his strategy

Why he’s underperformed

The letter says that the fund has underperformed because the market has shifted away from caring about business fundamentals and being driven by momentum.

I think that’s true and we’ll go into the argument Terry makes in a minute.

How he’s shifting strategy

Because of that, Smith says that the fund will be changing strategy and taking momentum into account.

That means it will be doing more buying and selling than it has historically.

In other words, Buy Good Companies, and Don’t Overpay are still in effect.

There will be a little bit less ‘Doing Nothing’ going forward.

The interesting part here is why Terry is making this shift.

It’s not because he thinks it’s the right investment decision.

It’s because if he didn’t do something, the fund would go out of business.

“We run open-ended funds, and you can and increasingly have been taking money out, we suspect mostly to join the exodus from active to passive, or possibly to invest in mangers who profess that they understand quality better than we do. They may be right, or they may just be closet momentum investors, which will be fine until it isn’t. However, there will be little point being proved right about the dangers of passive or momentum investment after our Fund has closed…In a market in which share price moves of 33% per day for even large stocks are not uncommon a buy and hold strategy can only work if you are not subject to flows, and we are. Sticking to our current approach may well fall foul of the adage that the market can remain illogical longer than we can remain in business. You should therefore expect that we will be more active in future.”

Passive Investing and Momentum

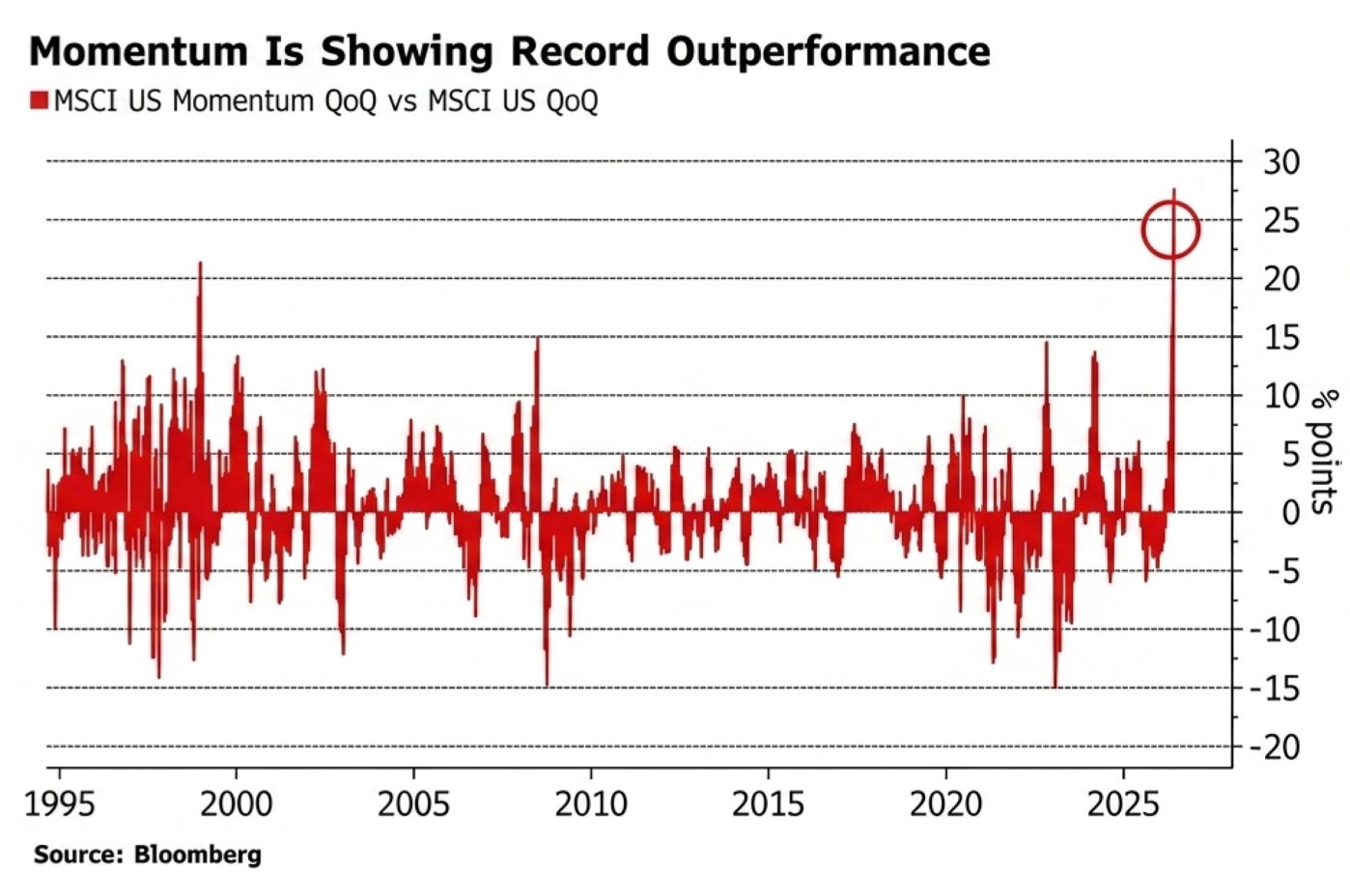

Terry has been talking about the markets becoming increasingly more momentum driven for quite some time.

And there’s no argument that he’s wrong, look at how momentum has been outperforming everything else lately.

He sets up his letter by saying that the shift to ETF investing and the excitement around AI means that the market no longer cares about the underlying businesses.

“a market which is dominated by so-called passive or index funds (of which the majority are ETFs) and the boom surrounding AI which have combined to produce a market dominated by momentum rather than any fundamental factors like profitability, returns on capital and growth — in other words the factors we focus on.”

What’s the point of passive investing?

Passive investing was popularized by John Bogle, who founded Vanguard.

Bogle’s argument was pretty simple:

Most active funds don’t beat the index, and they charge you fees which drag on your returns

By removing the cost and taking the average performance, investors wind up with more money (based on the cost savings)

Makes sense, but if that argument holds true, then shouldn’t the index and the average manager perform similarly?

They used to, but that’s started to change:

“In the UK, for example, Vanguard’s UK All Share tracker has made 66% over five years, trouncing the average UK equity fund’s return of just 32%.”

Some people argue that this is evidence that the average fund manager is terrible, and this is evidence on why everyone should just switch to passive.

Passive is now driving the market

Maybe, but Terry offers another explanation - a momentum driven feedback loop.

Passive fund does well → becomes popular → takes in more capital → buys more of what it already owns → drives share price up → passive fund does even better → takes in more capital → buys what it owns → prices go up → etc.

There’s pretty good evidence this is correct.

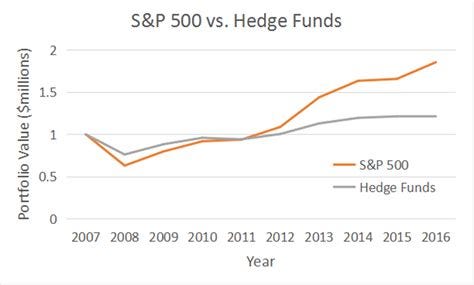

Here’s the performance of the S&P 500 vs Hedge Funds from 2007 to 2016.

I’d say that’s a pretty good representation of passive vs active performance.

They run close together until somewhere in 2012 or 2013, then diverge and widen.

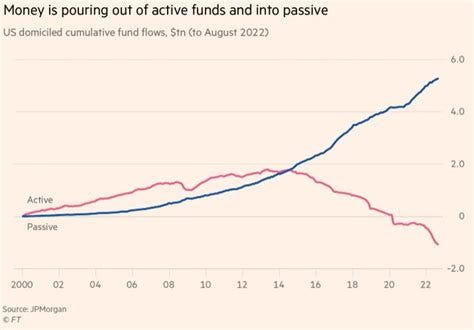

Here’s flows of capital for active and passive funds from 2000 to 2022.

Flows into active funds peak somewhere around 2012 or 2013 then decline while flows into passive funds keep going up.

So there’s really 2 feedback loops here:

Passive takes in money → buys more of what it owns → funds go up → more capital come in

Active loses money → sells what it owns → funds go down → more capital flows out

So the things passive funds own get more expensive, and the things active funds own get cheaper.

Which makes passive performance better and active performance worse, just from the shift in capital.

Passive now has more than 60% of the total Assets Under Management.

Trades set prices

The stock market is an ongoing, fast-paced auction.

That means prices are set by buyers and sellers when a trade happens.

Every Trade Needs Two Sides

You can’t buy a stock unless someone else is willing to sell it to you, and you can’t sell a stock unless someone else is willing to buy it from you.

It sounds simple, but it’s important.

When stock prices change, what you’re seeing is the price of the very last transaction that two real people agreed on.

How the auction works

To make trades happen, the stock market uses an ongoing list of offers called the Bid and the Ask.

The Bid: is the highest price a buyer is currently willing to pay for the stock

The Ask: is the lowest price a seller is currently willing to accept

The difference between these two numbers is called the spread.

It’s all tracked in the order book, which looks like this:

In the image, there are a lot of people willing to buy at $37.37.

But the lowest price anyone is willing to sell is $37.38.

No trades can happen right now.

How the Price Actually Moves

For a stock price to move, someone has to blink.

If buyers are aggressive: They’ll decide they don’t want to wait, and buy at $37.38, which will push the current price up to that number. If more buyers keep buying at the Ask, the price goes up.

If sellers are anxious: They’ll agree to take the buyer’s price of $37.37. A trade happens, and the price drops. If more people sell at the Bid, the price goes down.

Who’s making the trades?

If trades set prices, then we need to understand who’s making the trades.

Terry Smith tells us:

“Moreover, whilst AUM in index funds is now >60%, in terms of volume of trades, active fund managers are an even smaller minority than this implies. According to Cboe Global Markets, having been 80% of trades in the 1990s, active funds share of trades is now down to just 10%.”

When Jack Bogle rolled out index funds, the plan was for them to be a small minority that piggybacked off the research carried out professional stock pickers.

Back then, they made up nearly all of the market.

But that’s not the case anymore.

Now the market is made up of some combination of index buyers, ETFs, quant funds, and momentum traders, with something like 10% of the volume being traded by people who are actually reading reports and doing company research.

Index funds and ETFs run on a very simple model:

Money comes in → Buy

Money goes out → Sell

They don’t care at what price - so go back to the auction model.

If a lot of flows come in, and there aren’t a lot of sellers, the price will go up a lot.

The same is true when funds flow out.

What happens next?

When index funds blindly buy and sell regardless of price, it fundamentally changes how the stock market operates.

But what happens when this automated trading meets a market that isn’t as liquid as we think?

In Part 2, we are going to look at the massive volatility this is already causing, and show you the time bomb that could be hidden inside the U.S. retirement system.

Don’t miss it.

One Dividend At A Time,

-TJ

Used sources

Interactive Brokers: Portfolio data and executing all transactions

Fiscal.ai: Financial data

Disclaimer

As a reader of Compounding Dividends, you agree with our disclaimer. You can read the full disclaimer here.

We would be somewhat wary of any decision to change strategy based on investment fashion. Can’t remember one occasion over the decades when the real Warren Buffet deferred to the stance taken by other investors

This line is the key point that few people remember anymore: "When Jack Bogle rolled out index funds, the plan was for them to be a small minority that piggybacked off the research carried out professional stock pickers."